|

시장보고서

상품코드

2064346

북미의 백색 LED 패키지 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America White LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

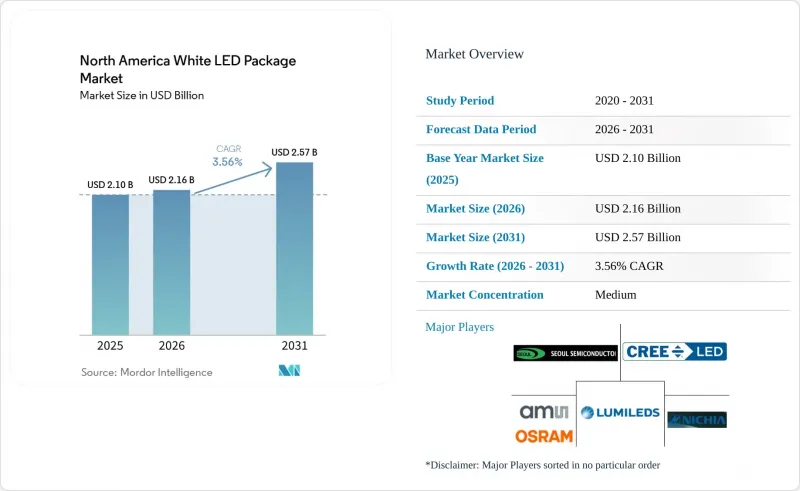

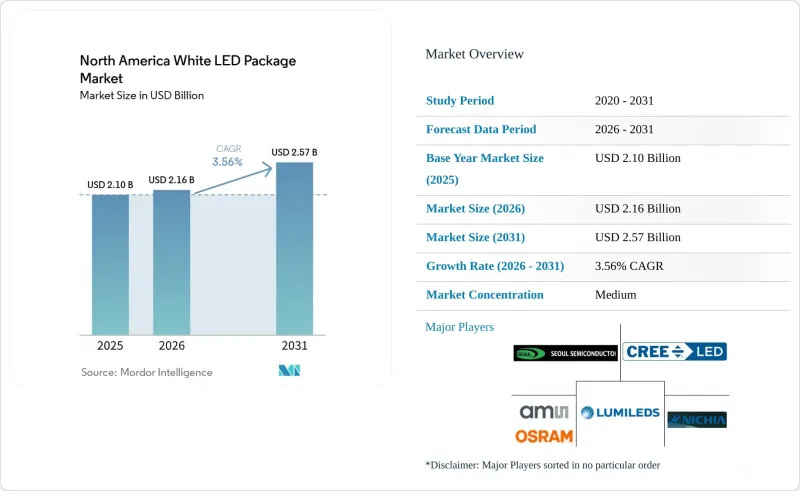

Mordor Intelligence에 의하면, 북미 백색 LED 패키지 시장 규모는 2025년 21억 달러, 2026년 21억 6,000만 달러에서 2031년까지 25억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 3.56%를 나타낼 것으로 예측됩니다.

본 보고서는 패키지 구조(SMD, COB, CSP 및 플립칩 LED 패키지), 전력 등급(저전력, 중전력 및 고전력), 용도(일반 조명, 자동차용 조명, 디스플레이 및 백라이트, 특수 용도) 및 지역(미국, 캐나다, 멕시코)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

북미 백색 LED 패키지 시장 동향 및 분석

연방 및 주 차원의 효율성 의무화가 LED로의 전환을 가속화하고 있습니다.

2024년에 확정된 새로운 일반용 램프 규정에 따르면, 전방향성 램프의 경우 810 lm의 출력에서 약 125 lm/W를 달성해야 하며, 이에 따라 LM-80 및 TM-21의 수명 프로토콜을 충족하기 위해 형광체 배합 및 드라이버 회로의 재설계가 권장되고 있습니다. 9개 주에서 동시에 시행되고 있는 수은등 금지 조치로 인해 형광등용 안정기 수요가 사라졌으며, 연방항공청(FAA)은 현재 활주로 위치 표시 시스템용으로 시판되는 LED 램프를 지정하고 있어, 20개 이상의 공항에서 조기 도입을 추진하고 있습니다. 이러한 조치들이 복합적으로 작용하여 개조 주기가 7년에서 4년으로 단축되었으며, 엄격한 광속 유지 기준을 충족하는 중출력 및 고출력 패키지의 출하량이 증가하고 있습니다.

루멘당 비용 절감 및 효율 향상

기존의 형광체 변환 패키지의 경우, 웨이퍼 직경이 4배로 확대되고 수율이 3배로 향상됨에 따라 2003년부터 2020년 사이에 제조 비용이 95.5% 감소했습니다. 같은 기간 동안 따뜻한 백색 디바이스의 효율은 5.8%에서 38.8%로 상승했으며, 앞으로는 분광 효율과 적색 형광체 변환이 다음 과제로 대두되고 있습니다. 2008년부터 2020년까지 조명 기구의 소매 가격은 연평균 27.3% 하락했으며, 많은 상업용 리모델링 프로젝트에서 단순 회수 기간이 12개월 미만이 되었습니다. 한편, 패키징이 칩 단가의 주요 비용 요인으로 작용하고 있어, 정밀 광학 시스템과 저열저항 기판을 대규모로 통합하는 공급업체가 유리한 입지를 점하고 있습니다.

관세 변동과 기판 공급망의 혼란

수입 LED 칩에 부과된 제301조 관세로 인해 입고 비용이 예측 불가능해지면서, 지자체 입찰 참가자들은 견적 유효 기간을 단축할 수밖에 없게 되었고, 장기 가격 계약으로 제품을 판매하는 조명 기구 제조업체의 이익률이 압박받고 있습니다. 사파이어 웨이퍼공급은 여전히 아시아를 중심으로 이루어지고 있으며, 물류 차질이 발생하면 그 영향이 즉시 북미의 패키징 라인으로 파급되어, 개조 수요가 가장 많은 성수기의 리드 타임을 길어지게 하고 있습니다.

부문별 분석

자동차 전조등 설계자들이 낮은 열저항과 얇은 광학 시스템을 우선시함에 따라, 칩 스케일 기술 시장 점유율 확대가 예상됩니다. 표면 실장 소자는 기존의 픽 앤 플레이스 라인에서 공구를 교체할 필요 없이 처리할 수 있기 때문에 비용을 중시하는 일반 조명 분야에서는 여전히 주류를 이루고 있습니다. 플립 칩의 변형 방식은 와이어 본딩을 필요로 하지 않으며, 접합부에서 기판으로의 저항을 2°C W-1 미만으로 낮춤으로써 더 높은 구동 전류를 가능하게 합니다. 칩 온 보드는 추가 조립 공정이 필요함에도 불구하고, 높은 루멘 밀도의 이점을 누릴 수 있는 트럭 조명이나 하이베이 조명 분야에서 여전히 선호되고 있습니다.

고액의 교차 라이선스 사용료가 플립칩 분야로의 신규 진입을 제한하고 있어, 기존 기업들의 이익률을 유지하고 있습니다. 그러나 ‘Build America’ 요건에 따라 공급업체들은 미국 내 조립 라인을 개설해야 하는 상황에 놓여 있으며, 이로 인해 단가가 점차 하락함에 따라 CSP의 도입이 가속화될 가능성이 있습니다. 북미 백색 LED 패키지 시장에서 칩 스케일 디바이스는 Tier 1 자동차 제조업체와의 계약이 와이어 본딩 어레이에서 전환됨에 따라 추가 수익을 창출할 것으로 전망됩니다. 레트로핏 램프 분야에서 SMD가 지속적으로 우위를 점하고 있는 것은 전반적인 아키텍처의 다양성 균형을 유지하고 있기 때문입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the north america white LED package market size is projected to expand from USD 2.10 billion in 2025 and USD 2.16 billion in 2026 to USD 2.57 billion by 2031, registering a CAGR of 3.56% between 2026 and 2031.

This report is Segmented by Package Architecture (SMD, COB, CSP, and Flip-Chip LED Packages), Power Class (Low Power, Mid Power, and High Power), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America White LED Package Market Trends and Insights

Federal And State Efficiency Mandates Accelerating LED Retrofits

New general-service-lamp rules finalized in 2024 require omnidirectional lamps to reach about 125 lm W-1 at 810 lm output, triggering redesigns of phosphor blends and driver circuits to meet LM-80 and TM-21 lifetime protocols. Parallel mercury-lamp bans across nine states eliminate fluorescent ballast demand, and the Federal Aviation Administration now specifies off-the-shelf LED lamps for runway alignment systems, bringing more than 20 airports into early adoption. Together these actions are shrinking retrofit cycles from seven to four years, lifting volumes of mid-power and high-power packages that satisfy strict lumen-maintenance criteria.

Declining Cost-Per-Lumen And Efficacy Gains

Classic phosphor-converted packages saw manufacturing cost drop 95.5% between 2003 and 2020 as wafer diameters quadrupled and yields tripled. Warm-white device efficiency climbed from 5.8% to 38.8% over the same horizon, leaving spectral efficiency and red-phosphor conversion as the next frontiers. Retail luminaire prices fell 27.3% annually from 2008 to 2020, cutting simple payback to under twelve months for many commercial retrofits, while packaging now dominates per-chip cost, favoring suppliers that integrate precision optics and low-thermal-resistance substrates at scale.

Tariff Volatility And Substrate Supply-Chain Disruptions

Section 301 duties on imported LED chips create unpredictable landed costs, forcing municipal bidders to hold quotes for shorter windows and eroding margins for fixture makers that sell under long-term price agreements. Sapphire wafer supply remains Asia-centric, and any logistics shock quickly ripples into North American packaging lines, lengthening lead times during peak retrofit seasons.

Other drivers and restraints analyzed in the detailed report include:

- Smart-City Infrastructure Investments Boosting High-Power Packages

- Automotive OEM Shift To LED Headlamps And DRLs

- High Capex For Advanced Packaging Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chip-scale technology is set to widen its share as automotive forward-lighting designers prioritize low thermal resistance and thinner optics. Surface-mount devices still anchor cost-sensitive general lighting because existing pick-and-place lines handle them without retooling. Flip-chip variants eliminate wire bonds, dropping junction-to-board resistance below 2 °C W-1 and enabling higher drive currents. Chip-on-board remains preferred for track and high-bay luminaires that benefit from high lumen density despite extra assembly steps.

High cross-licensing fees limit new entrants in flip-chip, preserving margins for incumbents. Yet Build America thresholds are nudging suppliers to open U.S. die-attach lines, which may gradually lower unit costs and speed CSP adoption. The North America white LED package market size for chip-scale devices is on course to capture incremental revenue as Tier-1 automotive contracts shift away from wire-bonded arrays. Sustained SMD dominance in retrofit lamps keeps overall architecture diversity balanced.

List of Companies Covered in this Report:

- Cree LED, Inc.

- Lumileds Holding B.V.

- Nichia Corporation

- ams-OSRAM GmbH

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Samsung Electronics Co., Ltd. (LED Division)

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Stanley Electric Co., Ltd.

- Epistar Corporation

- Bridgelux, Inc.

- Luminus Devices, Inc.

- Stanley Electric Co., Ltd.

- Citizen Electronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Market Drivers

- 4.6.1 Federal And State Efficiency Mandates Accelerating LED Retrofits

- 4.6.2 Declining Cost-Per-Lumen And Efficacy Gains

- 4.6.3 Smart-City Infrastructure Investments Boosting High-Power Packages

- 4.6.4 Automotive OEM Shift To LED Headlamps And DRLs

- 4.6.5 Build America, Buy America Sourcing Rules Reshaping Supply Chain

- 4.6.6 Vertical Farming Demand For High-CRI Tunable White Packages

- 4.7 Market Restraints

- 4.7.1 Tariff Volatility And Substrate Supply-Chain Disruptions

- 4.7.2 High Capex For Advanced Packaging Lines

- 4.7.3 Dark-Sky Compliance Ordinances Curbing Outdoor Lumens

- 4.7.4 Patent Cross-Licensing Barriers For Flip-Chip Architectures

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 COB (Chip-on-Board)

- 5.1.3 CSP (Chip Scale Package)

- 5.1.4 Flip-Chip LED Packages

- 5.2 By Power Class

- 5.2.1 Low Power (Less Than 0.5 W)

- 5.2.2 Mid Power (0.5 - 1 W)

- 5.2.3 High Power (Greater Than 1 W)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display And Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cree LED, Inc.

- 6.4.2 Lumileds Holding B.V.

- 6.4.3 Nichia Corporation

- 6.4.4 ams-OSRAM GmbH

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 LG Innotek Co., Ltd.

- 6.4.7 Samsung Electronics Co., Ltd. (LED Division)

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Citizen Electronics Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Stanley Electric Co., Ltd.

- 6.4.12 Epistar Corporation

- 6.4.13 Bridgelux, Inc.

- 6.4.14 Luminus Devices, Inc.

- 6.4.15 Stanley Electric Co., Ltd.

- 6.4.16 Citizen Electronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment

(주말 및 공휴일 제외)