|

시장보고서

상품코드

2064347

미국의 중출력 LED 패키지 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)United States Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

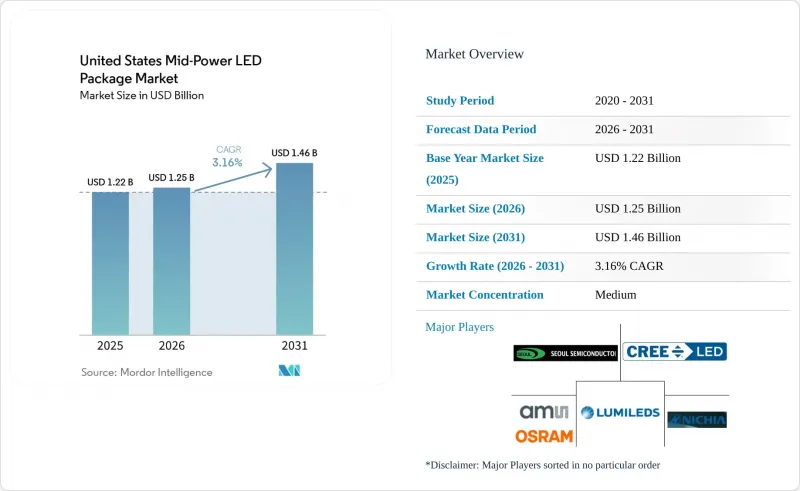

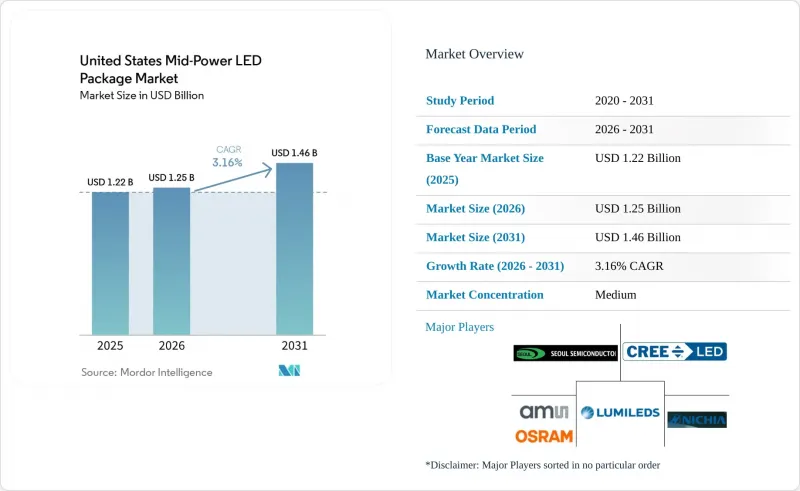

Mordor Intelligence에 의하면, 미국의 중출력 LED 패키지 시장 규모는 2025년에 12억 2,000만 달러로 평가되었고, 2026년에 12억 5,000만 달러로 추정되며, 2031년까지 14억 6,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 3.16%로 성장할 것으로 전망됩니다.

본 보고서는 출력 범위별(0.2W-0.5W, 0.5W-1W), 패키지 구조별(SMD, CSP), 용도별(일반 조명, 자동차용 조명, 디스플레이 및 백라이트, 특수 및 니치 용도)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 중출력 LED 패키지 시장 동향 및 분석

상업 시설 개보수 과정에서 에너지 절약형 조명의 급속한 보급

현재 전력 회사의 리베이트 프로그램은 미국 전력 소비자의 약 4분의 3을 대상으로 하고 있으며, 2026년 프로그램 확대에 따라 네트워크 지원 조명 기기가 대상 제품 목록에 추가됨에 따라 건물 소유주들은 2세대 LED로 업그레이드하는 방향으로 나아가고 있습니다. 인플레이션 억제법에 따라, 조명 에너지 소비를 25% 이상 절감하는 프로젝트에 대한 섹션 179D 감가상각 한도가 1제곱피트당 5달러로 인상됨에 따라, 높은 연색성(CRI)을 갖춘 중출력 LED 어레이의 투자 회수 기간이 실질적으로 3년 미만으로 단축되었습니다. 400W 메탈 할라이드 조명 기구를 150W LED 하이베이 조명으로 교체한 창고에서는 60%의 에너지 절감 효과와 수직 방향의 조도 향상이 보고되었습니다. 한편, 인체 감지 센서나 자연광 활용으로의 전환에 따라, 1대당 발광 소자 수가 증가하고 있습니다. 조명 기구의 총 출하량은 정체 국면에 접어들었으나, 발광 소자 밀도의 향상으로 인해 패키지 수요는 증가하고 있으며, 건설 시장이 성숙기에 접어든 상황에서도 미국의 중출력 LED 패키지 시장을 지탱하고 있습니다. 캘리포니아주와 뉴욕주의 지역 프로그램에는 플리커 및 색도에 관한 엄격한 목표가 추가되었으며, 이로 인해 국내 공급업체에게 더 높은 이익률을 가져다주는 프리미엄 등급 제품의 채택이 촉진되고 있습니다.

자동차 외장 조명 분야의 LED 보급 확대

연방 자동차 안전 기준(FMVSS) 108에 따라 미국 전역에서 어댑티브 드라이빙 빔이 허용됨에 따라, 포드, 제너럴 모터스, 스텔란티스는 2027년형 경트럭 전 차종에 매트릭스 헤드램프를 도입할 계획입니다. 각 모듈에는 개별적으로 제어 가능한 중출력 LED(일반적으로 0.5W CSP)가 40-120개 통합되어 있으며, 눈부심을 방지하기 위해 특정 구역을 조광합니다. LG 이노텍은 이미 88개 차종에 걸쳐 146건의 수주를 확보한 ‘Nexlide Pixel’ 플랫폼을 바탕으로, 2030년까지 자동차용 조명 부문 연간 매출 7억 3,100만 달러를 달성하는 것을 목표로 하고 있습니다. 후미등 역시 애니메이션 및 차량 간 통신을 위한 부문형 LED로 전환되고 있으며, 패키지 수는 기존의 정적 배열에 비해 2배로 늘어났습니다. 자동차 제조업체들이 AEC-Q102 규격과 15년 보증을 요구하고 있기 때문에 평균 판매 가격(ASP)은 일반 조명 등급을 괴롭히는 가격 압박의 영향을 받지 않고, 미국 중출력 LED 패키지 시장의 성장을 뒷받침하고 있습니다.

아시아의 치열한 경쟁으로 인한 가격 하락

Nationstar와 Everlight 같은 중국 제조업체들이 수직 통합된 사파이어 및 에피택시 생산 라인을 활용하여 0.5W 부품당 현금 원가를 0.02달러 미만으로 낮춘 결과, 2025년까지 4년 동안 중출력 패키지의 평균 판매 가격은 30-40% 하락했습니다. 2026년 1월 금과 구리선의 현물 가격 급등에 따라 중국 본토공급업체들은 정가를 최대 10% 인상하여 미국 공급업체들에게 일시적인 안도감을 안겨주었지만, 구조적인 비용 격차는 여전히 남아 있습니다. 따라서 조명 기구 OEM 제조업체는 듀얼 소싱 방식을 채택하여, 범용 SKU는 해외에서 조달하는 한편, 추적성 및 맞춤형 비닝으로 인해 15-20%의 가격 프리미엄이 부과되는 AEC-Q102 및 ISO 13485 대응 프로젝트에 대해서는 국내 공급업체를 확보하고 있습니다. 이러한 전략으로 인해 리모델링 시장의 이익률에 대한 압박은 여전히 심각하며, 부문별 호재에도 불구하고 미국 중출력 LED 패키지 시장 전체의 연평균 성장률(CAGR)을 억제하고 있습니다.

부문별 분석

0.5W-1W 미만 등급은 2025년 미국 중출력 LED 패키지 시장 매출의 63.19%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 3.88%로 확대될 것으로 전망됩니다. 400W 메탈 할라이드 조명 기구를 150W LED 하이베이 조명으로 교체하는 산업 시설에서는 일반적으로 24-36개의 이 중급 패키지를 사용하여 160 lm/W로 18,000-22,000루멘을 구현하는 동시에, 패시브 알루미늄 방열판을 사용하여 접합부 온도를 75°C 미만으로 유지하고 있습니다. 원예용 어레이에서도 마찬가지로 이 등급이 선호되고 있습니다. 이는 더 많은 발광 소자에 광자를 분산시킴으로써 수관부의 핫스팟을 최소화하고, 조명 기구를 교체하는 대신 드라이버 설정을 통해 스펙트럼 조정을 간소화할 수 있기 때문입니다.

웨어러블 기기나 엣지 라이트 방식의 간판에는 0.2-0.5W급 소자가 사용되고 있지만, 소비자용 제품의 소형화가 한계에 다다르고, 자동차 설계자들이 배선 작업을 간소화하기 위해 환경 조명 모듈을 소수의 중출력 칩으로 통합하는 경향이 있어 이 분야의 성장 속도는 둔화되고 있습니다. 소독 프로토콜에서는 더 신속한 조사량 공급이 요구되기 때문에 특수 자외선 제품의 전력 소비량은 증가하는 추세에 있습니다. 니치아 화학공업의 280 nm NCSU434D(출력 135 mW)는 과거 저전력이었던 틈새 시장이 중출력 와트 수로 수렴하고 있음을 보여주는 대표적인 사례이며, 미국 중출력 LED 패키지 산업에서 이 등급의 핵심적인 입지를 공고히 하고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the united states mid-power LED package market size is projected to be USD 1.22 billion in 2025, USD 1.25 billion in 2026, and reach USD 1.46 billion by 2031, growing at a CAGR of 3.16% from 2026 to 2031.

This report is Segmented by Power Range (0. 2 W To 0. 5 W, and 0. 5 W To Less Than 1 W), Package Architecture (Surface Mount Device, and Chip Scale Package), and Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty and Niche). The Market Forecasts are Provided in Terms of Value (USD).

United States Mid-Power LED Package Market Trends and Insights

Rapid Adoption Of Energy-Efficient Lighting In Commercial Retrofits

Utility rebate programs now cover roughly three-quarters of U.S. electricity customers, and 2026 expansions added networked luminaires to eligible product lists, pushing building owners toward second-generation LED-to-LED upgrades. The Inflation Reduction Act raised the Section 179D write-off to USD 5.00 per square foot for projects that cut lighting energy by at least 25%, effectively lowering payback to under three years for high-CRI mid-power arrays. Warehouses replacing 400 W metal-halide fixtures with 150 W LED high bays report 60% energy savings and better vertical illumination, while the move to occupancy sensing and daylight harvesting increases emitter count per fitting. Higher emitter density boosts package demand even though total luminaire shipments have plateaued, sustaining the United States mid-power LED package market during a mature construction cycle. Regional programs in California and New York add stretch targets on flicker and chromaticity, driving uptake of premium bin grades that carry healthier margins for domestic suppliers.

Increasing LED Penetration In Automotive Exterior Lighting

Federal Motor Vehicle Safety Standard 108 now allows adaptive driving beams nationwide, prompting Ford, General Motors, and Stellantis to roadmap matrix headlamps across 2027 model-year light-trucks. Each module integrates 40-120 individually addressable mid-power LEDs, typically 0.5 W CSPs, that dim exact zones to avoid glare. LG Innotek targets USD 731 million in annual automotive-lighting sales by 2030 on the back of its Nexlide Pixel platform, which has already booked 146 orders spanning 88 vehicle models. Rear lamps are also migrating to segmented LEDs for animation and vehicle-to-vehicle signaling, doubling package counts versus static arrays. Because automakers require AEC-Q102 and 15-year warranties, ASPs remain insulated from the price compression hurting general-lighting grades, sustaining growth in the United States mid-power LED package market.

Price Erosion Owing To Intense Asian Competition

Average selling prices for mid-power packages fell 30-40% in the four years to 2025 as Chinese makers such as Nationstar and Everlight leveraged vertically integrated sapphire and epitaxy lines to push cash costs below USD 0.02 per 0.5 W part. A January 2026 spot hike for gold and copper wire prompted mainland suppliers to lift list prices by up to 10%, offering temporary relief to U.S. vendors, yet the structural cost gap persists. Luminaire OEMs therefore dual-source, procuring commodity SKUs offshore while reserving domestic suppliers for AEC-Q102 or ISO 13485 projects that carry 15-20% price premiums for traceability and custom binning. The tactic keeps margin pressure acute in retrofit channels, restraining the overall United States mid-power LED package market CAGR despite segment-specific tailwinds.

Other drivers and restraints analyzed in the detailed report include:

- Growing Use Of Horticultural Lighting By U.S. Vertical Farms

- Federal Incentives For Domestic Semiconductor Packaging Under CHIPS Act

- Thermal Management Challenges In Compact Luminaire Designs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 0.5 W to Less Than 1 W class accounted for 63.19% of 2025 revenue in the United States mid-power LED package market, and it is projected to expand at a 3.88% CAGR through 2031. Industrial facilities swapping 400 W metal-halide fittings for 150 W LED high bays typically use 24-36 of these mid-tier packages to achieve 18,000-22,000 lumens at 160 lm W-1 while maintaining junction temperatures below 75 °C with passive aluminum heat sinks. Horticultural arrays likewise favor this class because distributing photons across a larger emitter count minimizes canopy hotspots and simplifies spectral tuning via driver settings rather than fixture swaps.

Wearables and edge-lit signage rely on 0.2-0.5 W devices, but that slice is expanding more slowly as consumer miniaturization plateaus and automotive designers consolidate ambient modules into fewer mid-power chips to simplify harnessing. Specialty ultraviolet products are nudging power upward as disinfection protocols demand faster dose delivery. Nichia's 280 nm NCSU434D at 135 mW output exemplifies how once-low-power niches are converging toward mid-range wattages, reinforcing the core position of this class in the United States mid-power LED package industry.

List of Companies Covered in this Report:

- ams OSRAM AG

- Nichia Corporation

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Cree LED, a business of Smart Global Holdings

- Samsung Electronics Co., Ltd.

- Lite-On Technology Corporation

- Everlight Electronics Co., Ltd.

- Lextar Electronics Corporation

- LG Innotek Co., Ltd.

- Nationstar Optoelectronics Co., Ltd.

- Bridgelux, Inc.

- Dominant Opto Technologies Sdn. Bhd.

- Epistar Corporation

- Sanan Optoelectronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Citizen Electronics Co., Ltd.

- Stanley Electric Co., Ltd.

- Osram Opto Semiconductors GmbH

- Refond Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Energy-Efficient Lighting in Commercial Retrofits

- 4.2.2 Increasing LED Penetration in Automotive Exterior Lighting

- 4.2.3 Growing Use of Horticultural Lighting by U.S. Vertical Farms

- 4.2.4 Federal Incentives for Domestic Semiconductor Packaging Under CHIPS Act

- 4.2.5 MiniLED Backlight Proliferation in High-End TVs and Monitors

- 4.2.6 Emergence of Tunable White Standards in WELL and LEED Buildings

- 4.3 Market Restraints

- 4.3.1 Price Erosion Owing to Intense Asian Competition

- 4.3.2 Thermal Management Challenges in Compact Luminaire Designs

- 4.3.3 Supply-Chain Risk From Indium and Gallium Price Volatility

- 4.3.4 Slow Standardization of CSP Reliability Testing Protocols

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 0.2 W - 0.5 W

- 5.1.2 0.5 W - Less Than 1 W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050 etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams OSRAM AG

- 6.4.2 Nichia Corporation

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Cree LED, a business of Smart Global Holdings

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Lite-On Technology Corporation

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Lextar Electronics Corporation

- 6.4.10 LG Innotek Co., Ltd.

- 6.4.11 Nationstar Optoelectronics Co., Ltd.

- 6.4.12 Bridgelux, Inc.

- 6.4.13 Dominant Opto Technologies Sdn. Bhd.

- 6.4.14 Epistar Corporation

- 6.4.15 Sanan Optoelectronics Co., Ltd.

- 6.4.16 Toyoda Gosei Co., Ltd.

- 6.4.17 Citizen Electronics Co., Ltd.

- 6.4.18 Stanley Electric Co., Ltd.

- 6.4.19 Osram Opto Semiconductors GmbH

- 6.4.20 Refond Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment