|

시장보고서

상품코드

2072770

이탈리아의 카톤 보드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Italy Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

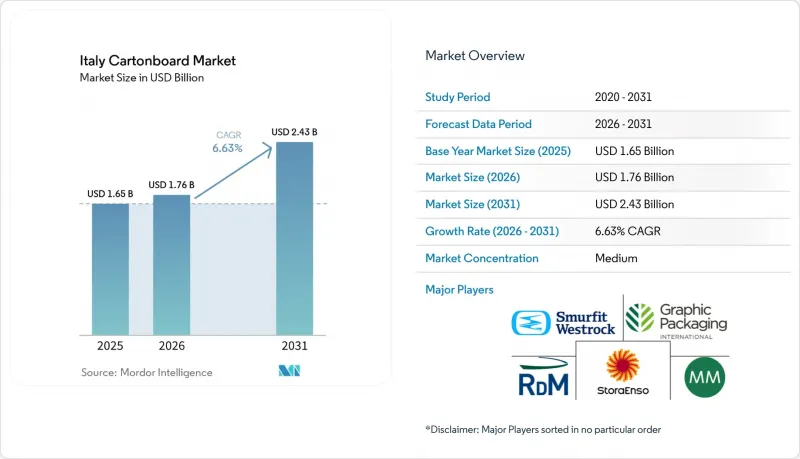

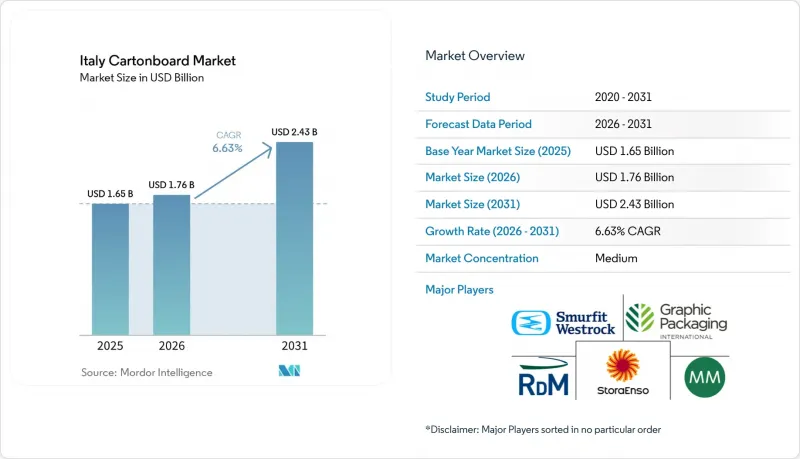

Mordor Intelligence에 의하면, 이탈리아의 카톤 보드 시장 규모는 2025년 16억 5,000만 달러로 평가되었고, 2026년에는 17억 6,000만 달러로 추정되고, 2031년까지 24억 3,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 6.63%로 성장할 전망입니다.

본 보고서는 제품 등급별(고형 표백 카톤 보드, 고형 미표백 카톤 보드, 접이식 상자용 카톤 보드, 화이트 라이닝 칩보드, 액체 포장용 카톤 보드, 푸드서비스용 카톤 보드), 포장 형태별(접이식 상자, 액체 포장, 슬리브 및 트레이 등), 그리고 최종 사용자 산업별(식품, 음료, 제약 및 헬스케어, 담배, 화장품 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

이탈리아의 카톤 보드 시장 동향 및 분석

소비자용 포장재에서 플라스틱을 종이로 대체

플라스틱에서 종이로의 전환은 이탈리아 카톤 보드 시장에서 여전히 단기 수요를 견인하는 가장 큰 요인으로 작용하고 있습니다. PPWR(플라스틱 포장 규제)는 2025년 2월에 발효되며, 2026년 8월 12일부터 광범위하게 적용될 예정입니다. 이에 따라 새로운 EU 포장 규정 체계 하에서는 많은 플라스틱 대체재보다 재활용이 가능한 섬유 기반 포장재가 더 쉽게 자리 잡을 수 있게 되었습니다. 소비자들의 인식도 같은 방향으로 나아가고 있습니다. Pro Carton의 2025년 보고서에 따르면, 유럽 5개국에서 조사 대상 성인 중 89%가 플라스틱 포장보다 카톤 보드 포장을 선호하는 것으로 나타났으며, 특히 이탈리아와 독일의 응답자들은 지속 가능한 포장을 위해 더 높은 가격을 지불할 의향이 가장 높은 그룹에 속했습니다. 이러한 변화가 중요한 이유는 수요가 더 이상 카톤 보드 운송용 포장에 국한되지 않고 냉동 식품, 화장품 및 기타 매장용 소비재용 접이식 상자로 더욱 깊이 확산되고 있기 때문입니다. 가공업체들이 과거 플라스틱 블리스터 팩이나 연포장이 주류를 이루던 용도 분야에서 더 가벼운 코팅지를 적극적으로 활용함에 따라, 이탈리아의 카톤 보드 시장은 수량 면에서도 금액 면에서도 새로운 기회를 얻고 있습니다. 이러한 효과는 브랜드 소유자가 하나의 패키지에서 재활용성, 인쇄 품질, 그리고 고급스러운 외관을 동시에 추구하는 경우에 가장 두드러지게 나타납니다.

PPWR을 통한 패키지 재설계 및 공극 감소

PPWR 주도의 재설계는 단순한 소재 대체를 넘어, 이탈리아 카톤 보드 시장에서 두 번째 수요층을 창출하고 있습니다. 이 규제는 포장 디자인 및 폐기물 감축에 관한 EU 차원의 공통 규정을 도입하는 것으로, 브랜드 소유주들에게 2026년 8월 시행일까지 포장 공간을 줄이고 소비자에게 직접 제공되는 포장의 구조를 재검토하도록 촉구하고 있습니다. 수출 중심의 이탈리아 식품·의약품 가공업체들에게 있어 이러한 압박은 특히 중요한 의미를 지닙니다. 규정을 준수하지 않는 디자인은 EU 단일 시장 전체에 대한 접근을 제한할 가능성이 있기 때문입니다. 이에 따라, 평량과 포장 치수를 줄이면서도 강도를 유지할 수 있는 경량이며 강성이 높은 접이식 상자용 카톤 보드 등급에 대한 수요가 증가하고 있습니다. 또한, 고객들은 업무에 미치는 지장을 최소화하면서 재설계 작업을 진행할 수 있는 포장 파트너를 점점 더 선호하고 있기 때문에 설계, 시험, 문서화 역량이 뛰어난 가공업체에게도 유리하게 작용하고 있습니다. 실제로 이탈리아의 카톤 보드 시장은 카톤 보드 수요 증가뿐만 아니라, 더 높은 사양의 등급과 더 정교하게 설계된 포장재로 전환되는 추세에서도 혜택을 보고 있습니다.

버진 펄프 및 전력 비용의 변동

비용 변동성은 여전히 이탈리아 카톤 보드 시장에서 가장 뚜렷한 사업적 제약 요인으로 남아 있습니다. 마이어-멜른호프사는 2026년 1분기 실적 속보에서 중동의 최근 정세 악화로 인해 2026년 3월 이후 에너지, 운송, 화학제품 분야에 대한 압박이 커졌습니다고 밝혔습니다. 또한, 2026년 4월 투자자 대상 프레젠테이션에서 이 회사는 시장 환경의 침체와 구조적인 공급 과잉이 여전히 지속되고 있다고 지적했습니다. 이는 생산자가 판매량 감소 위험을 감수하지 않고도 비용 상승분을 공급망에 전가할 수 있는 여지가 제한적임을 의미합니다. 이러한 상황은 원목 펄프 및 재생 펄프 보드 생산자 모두에게 어려운 여건을 초래하고 있습니다. 제지 제조업체는 비용을 회수해야 하지만, 가공업체들은 여전히 가격에 매우 민감하기 때문입니다. 주요 재생 카톤 보드 제조업체들의 재정적 어려움도 우려 요인으로 꼽히고 있습니다. RDM사는 생산과 출하가 평소와 같이 계속되고 있음에도 불구하고, 2026년 3월에 채무 상환 유예 계약을 체결했습니다. 에너지, 운임, 원자재 시세가 안정될 때까지는 기초 수요가 견조함에도 불구하고, 이탈리아 카톤 보드 시장은 계속해서 이익률 압박에 직면하게 될 것입니다.

부문별 분석

2025년, 이탈리아 카톤 보드 시장에서 접이식 카톤 보드는 34.21%의 점유율을 차지했으며, 금액 기준으로 가장 큰 비중을 차지하는 제품 등급이 되었습니다. 이러한 우위는 식품, 일반의약품, 화장품, 담배 상자 등 폭넓은 분야에서 활용되고 있다는 점에 기인하며, 이러한 분야에서는 기본적인 보호 기능과 더불어 강성, 인쇄 품질, 표면 마감도 중요하게 여겨지고 있습니다. 화이트 라이닝 칩보드는 재활용 섬유 함유율과 원가 관리가 구매 결정의 핵심 요소가 되는 대중 시장용 포장재 및 매장 진열용 소매 용품 분야에서 여전히 중요한 위치를 차지하고 있습니다. 무표백 고형판 및 표백 고형판은 특히 외관, 강도 또는 특수한 가공 요건이 더욱 엄격하게 요구되는 보다 제한적인 프리미엄 틈새 시장에 계속해서 공급되고 있습니다.

이탈리아의 액체 포장용 카톤 보드 시장 규모는 2031년까지 연평균 성장률(CAGR) 7.31%로 확대될 것으로 예상되며, 이는 제품 등급 중 가장 빠른 성장 속도입니다. 테트라팩이 2026년 4월에 'Sterilgarda Alimenti'를 출시한 것은 종이 기반 배리어 기술이 상업용 무균 카톤 분야로 진출하여 더 이상 개발 단계에 머물지 않음을 보여줍니다. 또한, 테트라팩이 2026년 1월에 종이 기반 배리어 개발을 위한 파일럿 플랜트에 6,000만 유로(7,120만 달러)를 투자하기로 결정한 것도, 이러한 등급 전환을 뒷받침하는 지속적인 투자를 시사하고 있습니다. 이탈리아 카톤 보드 업계 전반에 걸쳐, 등급 간 경쟁은 더 가벼운 구조, 더 단순한 차단 기능, 그리고 더 낮은 재료 중량으로 고성능화를 추구하는 방향으로 전환되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the italy cartonboard market size is expected to increase from USD 1.65 billion in 2025 to USD 1.76 billion in 2026 and reach USD 2.43 billion by 2031, growing at a CAGR of 6.63% over 2026-2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Italy Cartonboard Market Trends and Insights

Plastic-To-Paper Substitution Across Consumer Packaging

Plastic-to-paper substitution remains the strongest near-term demand driver for the Italy cartonboard market. The PPWR entered into force in February 2025 and will apply broadly from August 12, 2026, which makes recyclable fiber-based formats easier to position under the new EU packaging framework than many plastic alternatives. Consumer attitudes are also moving in the same direction, with Pro Carton reporting in 2025 that 89% of surveyed adults across 5 European countries preferred cartonboard to plastic packaging, while Italian and German respondents were among the most willing to pay more for sustainable packaging. That change matters because demand is no longer limited to corrugated shipping packs and is moving deeper into folding cartons for frozen food, cosmetics, and other shelf-facing consumer products. As converters make lighter coated grades work in applications once dominated by plastic blisters or flexible formats, the Italy cartonboard market is gaining both volume and value opportunities. The effect is strongest where brand owners need recyclability, print quality, and premium presentation in the same pack.

PPWR-Driven Packaging Redesign And Void-Space Reduction

PPWR-led redesign is creating a second layer of demand for the Italy cartonboard market beyond simple material substitution. The regulation introduces common EU rules on packaging design and waste reduction, pushing brand owners to reduce space and reassess the structure of consumer-facing packs before the application date in August 2026. For Italy's export-oriented food and pharmaceutical converters, that pressure is especially relevant because non-compliant designs can restrict access across the full EU single market. This is increasing demand for lighter but stiffer folding boxboard grades that can preserve pack strength while trimming basis weight and pack dimensions. It also favors converters with deeper design, testing, and documentation capabilities, since customers increasingly want a packaging partner that can help them move through redesign work with less disruption. In practice, the Italian cartonboard market is benefiting not only from more board demand but also from a shift toward higher-specification grades and better-engineered packs.

Virgin Pulp And Electricity Cost Volatility

Cost volatility remains the clearest operating restraint for the Italy cartonboard market. Mayr-Melnhof stated in its first-quarter 2026 trading update that recent escalations in the Middle East increased pressure on energy, transportation, and chemicals from March 2026 onward. In its April 2026 investor presentation, the company also said that weak market conditions and structural overcapacity persisted, which means producers have limited room to pass higher costs through the chain without risking volume loss. That combination creates a difficult environment for both virgin-fiber and recycled-board producers, as mills need to recover costs while converters remain highly price-sensitive. Financial stress at major recycled-board players adds to the caution, as RDM entered a forbearance agreement in March 2026 even though production and deliveries continued normally. Until energy, freight, and raw-material conditions stabilize, the Italy cartonboard market will continue to face margin pressure, even as underlying demand remains healthy.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization In Food, Beauty, And OTC Packaging

- High Italian Paper And Board Recycling Performance

- Competition From Plastic And Alternative Liquid-Pack Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard held 34.21% of the Italy cartonboard market share in 2025, making it the largest product grade by value. Its lead came from broad use across food, OTC pharmaceuticals, cosmetics, and tobacco cartons, where stiffness, print quality, and surface finish matter as much as basic protection. White-lined chipboard remained important in mass-market packs and shelf-ready retail formats, where recycled fiber content and cost control are central to buying decisions. Solid bleached board and solid unbleached board continued to serve narrower premium niches, especially where appearance, strength, or specialty conversion requirements were more demanding.

The Italy cartonboard market size for liquid packaging board is projected to expand at a 7.31% CAGR through 2031, the fastest pace among product grades. Tetra Pak's April 2026 launch with Sterilgarda Alimenti showed that paper-based barrier technology has moved into commercial aseptic cartons and is no longer limited to development work. Tetra Pak's earlier January 2026 decision to invest EUR 60 million (USD 71.2 million) in a pilot plant for paper-based barrier development also points to sustained investment behind this grade transition. Across the Italy cartonboard industry, grade competition is shifting toward lighter structures, simpler barriers, and higher performance at lower material weight.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Mayr-Melnhof Karton AG

- Reno De Medici S.p.A.

- Stora Enso Oyj

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Fedrigoni S.p.A.

- Seda International Packaging Group S.p.A.

- Tetra Pak Italiana S.p.A.

- SIG Combibloc Italia S.r.l.

- Elopak Italia S.r.l.

- Palladio Group S.p.A.

- DS Smith Packaging Italia S.p.A.

- Pozzoli S.p.A.

- Lucaprint S.p.A.

- BOX MARCHE S.P.A.

- Eurpack S.r.l.

- CM Cartotecnica Moderna S.r.l. Benefit

- Industria Grafica Umbra s.r.l.

- Eurographic s.r.l.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Plastic-to-Paper Substitution Across Consumer Packaging

- 4.3.2 Premiumization in Food, Beauty, and OTC Packaging

- 4.3.3 Retail-Ready and Shelf-Ready Carton Demand

- 4.3.4 High Italian Paper and Board Recycling Performance

- 4.3.5 PPWR-Driven Packaging Redesign and Void-Space Reduction

- 4.3.6 PFAS-Free and Simpler Food-Contact Barrier Structures

- 4.4 Market Restraints

- 4.4.1 Virgin Pulp and Electricity Cost Volatility

- 4.4.2 Competition From Plastic and Alternative Liquid-Pack Formats

- 4.4.3 PPWR Documentation and Conformity Burden for SMEs

- 4.4.4 Food-Contact Reformulation and Testing Costs After PFAS and BPA Changes

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mayr-Melnhof Karton AG

- 6.4.2 Reno De Medici S.p.A.

- 6.4.3 Stora Enso Oyj

- 6.4.4 Smurfit Westrock plc

- 6.4.5 Graphic Packaging International, LLC

- 6.4.6 Fedrigoni S.p.A.

- 6.4.7 Seda International Packaging Group S.p.A.

- 6.4.8 Tetra Pak Italiana S.p.A.

- 6.4.9 SIG Combibloc Italia S.r.l.

- 6.4.10 Elopak Italia S.r.l.

- 6.4.11 Palladio Group S.p.A.

- 6.4.12 DS Smith Packaging Italia S.p.A.

- 6.4.13 Pozzoli S.p.A.

- 6.4.14 Lucaprint S.p.A.

- 6.4.15 BOX MARCHE S.P.A.

- 6.4.16 Eurpack S.r.l.

- 6.4.17 CM Cartotecnica Moderna S.r.l. Benefit

- 6.4.18 Industria Grafica Umbra s.r.l.

- 6.4.19 Eurographic s.r.l.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment