|

시장보고서

상품코드

2072772

프랑스의 카톤 보드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)France Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

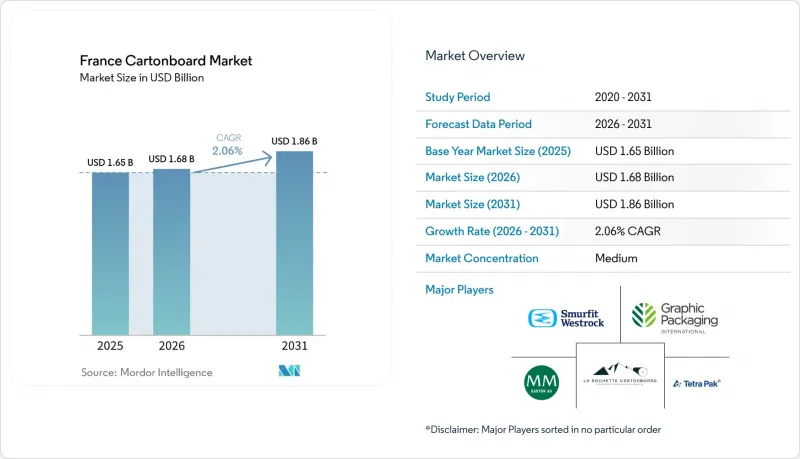

Mordor Intelligence에 의하면, 프랑스의 카톤 보드 시장 규모는 2025년에 16억 5,000만 달러로 평가되었고, 2026년에 16억 8,000만 달러로 추정되고, 2031년까지 18억 6,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 2.06%로 성장할 전망입니다.

본 보고서는 제품 등급별(고형 표백 카톤 보드, 고형 미표백 카톤 보드, 접이식 상자용 카톤 보드, 화이트 라이닝 칩보드, 액체 포장용 카톤 보드, 푸드서비스용 카톤 보드), 포장 형태별(접이식 상자, 액체 포장, 슬리브 및 트레이 등), 최종 사용자 산업별(식품, 음료, 의약품 및 헬스케어, 담배 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

프랑스의 카톤 보드 시장 동향 및 분석

AGEC 및 PPWR을 기반으로 한 플라스틱에서 섬유로의 대체

플라스틱에서 섬유로의 대체는 예측 기간 동안 프랑스 카톤 보드 시장의 가장 지속적인 수요 견인 요인이 될 것입니다. EU의 포장 및 포장 폐기물 규정(AGEC)은 2025년 2월 11일에 발효되며, 2026년 8월 12일부터 적용됩니다. 이로 인해 2030년까지 재활용 가능성을 입증해야 하는 포장 형태에서 카톤 보드는 규정 준수 측면에서 더욱 확고한 우위를 확보하게 될 것입니다. 프랑스의 AGEC법 역시 1.5kg 미만의 신선 과일 및 채소에 대한 금지 조치를 포함해, 일회용 플라스틱 포장에 대한 국내 규제를 통해 이와 유사한 방향성을 강화해 왔습니다. 이러한 시너지 효과 덕분에 브랜드 소유주들은 향후 규정 준수 기한을 기다릴 필요 없이, 섬유를 중심으로 한 패키지 재설계를 위한 충분한 전환 기간을 확보하게 되었습니다. 프랑스의 카톤 보드 시장은 다층 플라스틱 구조에 비해 단일 소재 카톤 보드 솔루션이 새로운 규제 체계 내에서 위치를 정립하기 더 쉽기 때문에 그 혜택을 누리고 있습니다. 또한, 프랑스의 가공업체들은 AGEC법에 따라 일찍부터 포장재 재설계 경험을 쌓아왔기 때문에 더 많은 용도가 재활용 가능한 카톤 보드 형태로 전환되는 가운데 고객에게 신속하게 대응하고 이익률을 높일 수 있습니다.

즉석식품 및 신선식품 부문의 식품 포장 수요

식품은 여전히 프랑스 카톤 보드 시장의 주요 수요 기반이며, 즉석식품 및 신선식품 부문 수요가 그 안정성을 더욱 높여주고 있습니다. 유제품, 제빵 제품, 신선 식품, 냉동 식품, 상온 식품 분야에서는 이미 전국적으로 카톤 보드 사용이 보편화되어 있습니다. 식품 제조업체들이 포장을 재활용이 더 용이한 형태로 전환함에 따라, 접이식 상자용 카톤 보드는 진열 효과와 취급상의 요구 사항을 모두 충족하는 슬리브, 트레이 및 식품과 직접 접촉하는 구조물에 사용되고 있습니다. AGEC의 적용 하에서 플라스틱 대체가 비교적 용이한 용도에서는 이러한 전환이 초기 단계에서 가장 두드러지게 진행되고 있지만, 냉장 식품 분야에서는 여전히 더 많은 전환 여지가 남아 있습니다. 이에 따라 수요 패턴은 더욱 선택적으로 변하고 있으며, 재활용 가능한 카톤 보드 시스템 중에서 내습성, 인쇄 품질, 그리고 신뢰성 높은 식품 포장 성능을 모두 갖춘 공급업체로 가치가 이동하고 있습니다. 따라서 프랑스의 카톤 보드 시장은 포장재의 보급 확대뿐만 아니라, 보다 전문화된 등급 및 가공 능력으로의 단계적 전환을 통해 식품 수요의 혜택을 누리고 있습니다.

변동이 심한 펄프, 재생 섬유 및 에너지 비용

원자재 비용의 변동은 여전히 프랑스 카톤 보드 시장에 있어 가장 시급한 걸림돌로 남아 있습니다. 마이어-멜른호프사의 2026년 1분기 실적 보고서에서는 수요 부진, 구조적인 공급 과잉, 치열한 경쟁과 같은 사업 환경이 설명되어 있으며, 지정학적 압력이 에너지, 운송, 화학제품 비용에 영향을 미치고 있다고 지적하고 있습니다. 메차 보드사도 2026년 4월, 이란 정세로 인한 원유 및 천연가스 가격 급등으로 인해 2026년 2분기 영업이익이 1,000만 유로 감소할 것으로 전망한다고 발표했으며, 이는 외부 충격이 카톤 보드 업계의 수익성에 얼마나 신속하게 영향을 미치는지를 보여주고 있습니다. 프랑스의 카톤 보드 시장에서 이러한 압박은 특히 중요한 의미를 지닙니다. 왜냐하면, 가공업체들은 이익률이 압박받는 상황에서도, 고객이 여전히 서비스의 신뢰성과 기술적 요건의 준수를 기대하는 환경 속에서 경쟁을 벌일 수밖에 없기 때문입니다. 비용 변동은 제품 구성에도 영향을 미칩니다. 왜냐하면 재생 섬유와 에너지 비용이 동시에 변동할 경우, 재생 섬유의 등급이 더 큰 영향을 받기 때문입니다. 그 결과, 기술력이 뛰어나거나 보다 통합된 공급업체는 가격 결정력이나 조달 능력이 부족한 소규모 가공업체보다 유리한 입장에 서게 됩니다.

부문별 분석

2025년, 접이식 카톤 보드는 프랑스 카톤 보드 시장에서 42.25%의 점유율을 차지했으며, 해당 시장의 주요 제품 등급으로서의 입지를 유지했습니다. 이러한 위상은 식품, 의약품, 가정용품, 전자상거래 등 폭넓은 분야에서 활용되고 있음을 반영하며, 이러한 분야에서는 인쇄 적합성, 강성, 재활용성이 일상적인 상업적 의사결정에서 모두 중요한 요소로 작용하고 있습니다. 솔리드 블리치드 보드는 가장 빠르게 성장하는 등급으로, 2031년까지 연평균 성장률(CAGR) 5.19%로 확대될 것으로 전망됩니다. 이는 프랑스 카톤 보드 업계에서 고사양 용도로의 가치 전환이 얼마나 진행되고 있는지를 보여줍니다. 이러한 변화는 단순한 수량 증가라기보다는 고급품, 의약품, 프리미엄 식품을 구매하는 고객층 수요 증가에 기인한 것입니다. 그 결과, 프랑스 카톤 보드 시장에서는 총 톤수가 급격하게 변동하지 않는 경우에도 금액 기준 프리미엄 등급 시장 점유율이 확대되고 있습니다.

2025년 9월, 스토라 엔소(Stora Enso)가 출시한 'Ensovelvet'는 공급업체가 프리미엄 향수 및 퍼스널케어 제품용 패키지에 맞추어 설계된 SBS 등급을 통해 이러한 트렌드에 어떻게 대응하고 있는지를 보여주는 명확한 예입니다. 2026년 2월, 스마핏 웨스트록사가 라 투크의 SBS 생산 라인을 폐쇄한 것은 범용 제품의 생산 능력 확대가 아니라, 더 높은 사양의 SBS 공급을 위한 포트폴리오 전략의 일환이었습니다. 화이트 라이닝 칩보드는 여전히 가격에 민감한 용도와 밀접하게 연관되어 있어, 에너지 비용이나 코팅 규제에 대응하기 어려워질 경우 더 큰 영향을 받기 쉽습니다. 무표백 고형 카톤 보드는 외관보다 강도가 중시되는 외식 산업 및 산업용 분야에서 여전히 중요한 역할을 수행하고 있는 반면, 액체 포장용 카톤 보드와 외식 산업용 카톤 보드는 플라스틱 용기를 지속적으로 대체해 나가는 추세에 힘입어 혜택을 보고 있습니다. 실용적인 관점에서 볼 때, 프랑스 카톤 보드 시장에서는 표면 품질, 규제 대응 능력, 그리고 신뢰할 수 있는 납품 능력을 모두 갖추고, 더 이상 저비용 카톤 보드만으로는 충족할 수 없는 최종 용도에 대응할 수 있는 인증된 버진 펄프 공급업체가 높이 평가받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the france cartonboard market size is projected to be USD 1.65 billion in 2025, USD 1.68 billion in 2026, and reach USD 1.86 billion by 2031, growing at a CAGR of 2.06% from 2026 to 2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Food, Beverage, Pharmaceutical and Healthcare, Tobacco, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Cartonboard Market Trends and Insights

Plastic-To-Fiber Substitution Under AGEC and PPWR

Plastic-to-fiber substitution is the most durable demand support for the France cartonboard market over the forecast period. The EU Packaging and Packaging Waste Regulation entered into force on February 11, 2025, and applies from August 12, 2026, which gives cartonboard a stronger compliance position in packaging formats that must demonstrate recyclability by 2030. France's AGEC law has been reinforcing the same direction through national restrictions on single-use plastic packaging, including the ban that France implemented for fresh fruit and vegetables below 1.5 kg. This combination has created a long transition window in which brand owners can redesign packs around fiber rather than wait for a later compliance deadline. The France cartonboard market benefits because mono-material paperboard solutions are easier to position within the new regulatory framework than multilayer plastic structures. French converters also enter this phase with earlier redesign experience under AGEC, which supports faster customer response and better margin capture as more applications move toward recyclable board formats.

Food Packaging Demand From Ready-To-Eat and Fresh Categories

Food remains a core volume base for the France cartonboard market, and demand from ready-to-eat and fresh categories is adding to that stability. Dairy, bakery, fresh produce, frozen meals, and ambient food applications already anchor cartonboard use across the country. As food producers shift more packaging into recyclable formats, folding boxboard is being used in sleeves, trays, and direct-contact structures that support both shelf presentation and handling needs. The early phase of conversion has been strongest in applications where plastic replacement is easier to execute under AGEC, while chilled formats still offer room for further migration. That creates a more selective demand pattern, where value moves toward suppliers that can handle moisture resistance, print quality, and reliable food-packaging performance within recyclable board systems. The France cartonboard market therefore gains from food demand not only through broader pack adoption, but also through a gradual move toward more specialized grades and converting capability.

Volatile Pulp, Recovered Fiber, And Energy Costs

Input cost volatility remains the most immediate brake on the France cartonboard market. Mayr-Melnhof's Q1 2026 trading statement described the operating backdrop as subdued demand, structural overcapacity, and intense competition, with geopolitical pressure feeding through energy, transport, and chemical costs. Metsa Board also stated in April 2026 that rising oil and natural gas prices linked to the Iran conflict were expected to reduce its Q2 2026 operating result by EUR 10 million, which shows how quickly external shocks move into paperboard economics. In the France cartonboard market, these pressures are especially important because converters compete in an environment where customers still expect service reliability and technical compliance even when margins tighten. Cost volatility also affects product mix, since recycled-fiber grades are more exposed when both recovered fiber and energy costs move at the same time. This leaves technically stronger or more integrated suppliers better placed than smaller converters that lack pricing power or procurement leverage.

Other drivers and restraints analyzed in the detailed report include:

- Premium Beauty And Luxury Carton Demand

- Healthcare Serialization And Compliance Packaging Demand

- Alternative Flexible And Lightweight Formats In Selected Uses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard held 42.25% of France cartonboard market share in 2025, which kept it as the leading product grade in the France cartonboard market. Its position reflects broad use across food, pharmaceuticals, household goods, and e-commerce, where printability, stiffness, and recyclability all matter in everyday commercial decisions. Solid Bleached Board is the fastest-growing grade and is forecast to rise at 5.19% CAGR through 2031, which shows how much value is moving toward higher-specification applications in the France cartonboard industry. This shift is tied less to simple volume growth and more to substrate upgrading by luxury, pharmaceutical, and premium food customers. The France cartonboard market is therefore seeing premium grades gain share in value terms even when total tonnage does not change sharply.

Stora Enso's Ensovelvet launch in September 2025 is a clear example of how suppliers are targeting this movement with SBS grades designed for premium fragrance and personal care packaging. The closure of the La Tuque SBS machine in February 2026 by Smurfit Westrock was a portfolio move toward higher-specification SBS supply rather than broader commodity capacity. White-Lined Chipboard remains tied more closely to price-sensitive applications, and that leaves it more exposed when energy costs and coating compliance become harder to manage. Solid Unbleached Board still holds a role in food-service and industrial uses where strength matters more than appearance, while liquid packaging board and food-service board benefit from the ongoing replacement of plastic-based formats. In practical terms, the France cartonboard market is rewarding certified virgin-fiber suppliers that can combine surface quality, regulatory readiness, and dependable delivery across end uses that now require more than low-cost board alone.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging International, LLC

- La Rochette Cartonboard SAS

- Tetra Pak International S.A.

- SIG Group AG

- Elopak ASA

- Metsa Board Corporation

- Stora Enso Oyj

- Billerud AB

- Autajon Group

- Verpack

- FP PACK

- TPG PACK

- SODEPRINT

- Cartonnages Vaillant

- Groupe Lacroix

- Huhtamaki Oyj

- Sonoco Products Company

- Holmen AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Plastic-to-Fiber Substitution Under AGEC and PPWR

- 4.3.2 Food Packaging Demand from Ready-to-Eat and Fresh Categories

- 4.3.3 Premium Beauty and Luxury Carton Demand

- 4.3.4 Healthcare Serialization and Compliance Packaging Demand

- 4.3.5 EPR Eco-Modulation Rewards Design-for-Recycling Cartons

- 4.3.6 Luxury E-Commerce Right-Sizing and Void Reduction Needs

- 4.4 Market Restraints

- 4.4.1 Volatile Pulp, Recovered Fiber, and Energy Costs

- 4.4.2 Alternative Flexible and Lightweight Formats in Selected Uses

- 4.4.3 Migration Testing Burden for Inks, Coatings, and Adhesives

- 4.4.4 Domestic Converting Capacity Gaps and Import Dependence

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Graphic Packaging International, LLC

- 6.4.4 La Rochette Cartonboard SAS

- 6.4.5 Tetra Pak International S.A.

- 6.4.6 SIG Group AG

- 6.4.7 Elopak ASA

- 6.4.8 Metsa Board Corporation

- 6.4.9 Stora Enso Oyj

- 6.4.10 Billerud AB

- 6.4.11 Autajon Group

- 6.4.12 Verpack

- 6.4.13 FP PACK

- 6.4.14 TPG PACK

- 6.4.15 SODEPRINT

- 6.4.16 Cartonnages Vaillant

- 6.4.17 Groupe Lacroix

- 6.4.18 Huhtamaki Oyj

- 6.4.19 Sonoco Products Company

- 6.4.20 Holmen AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment