|

시장보고서

상품코드

2073183

프랑스의 그린 IT 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)France Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

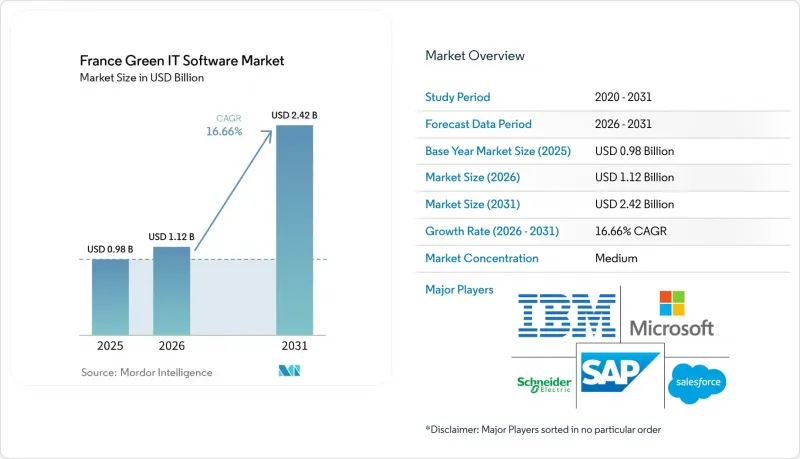

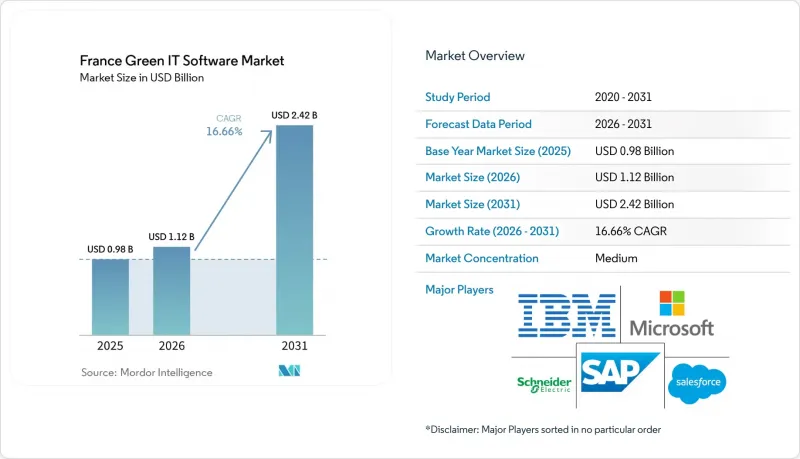

Mordor Intelligence에 의하면, 프랑스 그린 IT 소프트웨어 시장은 2025년 9억 8,000만 달러에서 2026년에는 11억 2,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 16.66%로 성장하여 2031년까지 24억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제공(소프트웨어 및 서비스), 배포 방식(클라우드 기반, On-Premise형, 하이브리드형), 기업 규모(대기업 및 중소기업), 솔루션 유형(탄소 관리·산정 소프트웨어, 에너지 관련 등), 최종 사용자(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 제조업 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

프랑스 그린 IT 소프트웨어 시장 동향과 인사이트

EU 및 프랑스에서 탄소 중립 관련 정보 공개에 대한 압박이 커지고 있습니다.

프랑스는 CSRD(기업 지속가능성 보고 지침)와 관련된 의무 이행에 있어 다른 많은 유럽 국가들보다 앞서 있으며, 이로 인해 현지 기업들은 지속가능성 보고를 위한 플랫폼 선정 및 데이터 준비를 미룰 수 있는 시간이 줄어들었습니다. 대형 상장 기업들은 2025년에 이미 새로운 프레임워크에 따른 보고를 시작했으며, 그 밖의 대기업들도 2026년에 2025 회계연도 보고를 실시할 예정인 만큼, 배출량 산정, ESRS 매핑 및 검증 가능한 기록과 관련된 소프트웨어 수요는 견조한 추세를 보였습니다. “옴니버스 I 지령”에 따라 의무 적용 대상이 새로운 직원 수 및 매출액 기준을 초과하는 기업으로 한정됨에 따라, 이러한 변경으로 인해 단기적으로는 중견 기업을 대상으로 한 파이프라인의 일부가 축소되었습니다. 그럼에도 불구하고, 해당 기업이 조달 및 규정 준수 심사를 통해 공급업체에 지속가능성 데이터 제공을 요청할 때, 프랑스의 그린 IT 소프트웨어 시장은 여전히 그 혜택을 누리고 있습니다. AMF(프랑스 금융시장청)의 감독 및 감사 기준에 부합하는 공시 필요성은 데이터 품질 추적, 통제 지원, 제3자 보증을 위한 기록 작성이 가능한 소프트웨어를 지속적으로 뒷받침하고 있습니다.

IT 배출량 가시화에 대한 기업 수요 증가

프랑스의 그린 IT 소프트웨어 시장은 기본적인 측정 수요의 혜택을 받고 있습니다. 이는 디지털 운영이 환경에 미치는 영향을 기업들이 더 이상 무시하기 어려워졌기 때문입니다. ADEME와 ARCEP의 조사에 따르면, 프랑스의 디지털 부문은 국내 탄소 발자국의 4.4%(29.5 MtCO2e)를 차지하고 있으며, 이 중 데이터센터가 46%, 단말기가 50%를 차지하고 있습니다. 공공 송전망에 연결된 데이터센터의 전력 사용량은 2024년 0.8 TWh에서 2025년에는 1 TWh에 육박할 것으로 예상에 따라, 인프라 이용 현황을 보다 면밀히 모니터링하고 보고 체계를 강화할 필요성이 부각되었습니다. ARCEP의 2025년 환경 조사에 따르면, Orange, Bouygues Telecom, SFR, Iliad 등 4개사의 스코프 2 배출량 합계는 39만 7,000 tCO2e를 기록했으며, 국내 배출량이 감소했음에도 불구하고 전년 대비 4.2% 증가했습니다. 이는 업계 고유의 추적 도구의 필요성을 한층 더 뒷받침해 줍니다. 프랑스의 저탄소 전력망 덕분에 국내 전력 관련 배출량은 비교적 낮은 수준으로 억제되고 있지만, 한편으로 많은 기업들은 프랑스의 그린 IT 소프트웨어 시장에서 수입된 디지털 서비스의 이용, 해외 호스팅에 대한 의존도, 그리고 보다 광범위한 스코프 3 산정에 더 많은 주의를 기울일 수밖에 없는 상황입니다.

레거시 환경에 걸쳐 있는 IT 및 시설 데이터의 분산

프랑스의 그린 IT 소프트웨어 시장에서 여전히 해결되지 않은 과제는 많은 기업이 여전히 IT 장비, 시설, 호스팅 환경 전반에 걸친 정확한 자산 수준 데이터를 보유하고 있지 않다는 점입니다. ESRS E1 보고서를 작성하려면 서버, 네트워크 하드웨어, 디바이스 및 에너지 사용량에 관한 상세한 입력 데이터가 필요하지만, 기존의 IT 서비스 관리 시스템은 이러한 수준의 환경 측정을 염두에 두고 구축되지 않았습니다. ARCEP의 2025년 환경 조사에 따르면, 이미 체계적인 보고에 익숙한 대형 통신 사업자조차도 장비 수준의 상세한 데이터 수집은 여전히 어려운 것으로 나타났습니다. ADEME는 2025년에 호스팅 IT 및 통신 서비스에 관한 조사 방법을 업데이트했으나, 중소규모 사업자나 민간 부문에서의 도입 현황에는 편차가 나타나고 있습니다. 이는 자산 대장이 불완전하거나, 에너지 계량기의 사양이 통일되지 않았거나, 보고 요건을 충족할 만한 데이터 기반이 마련되어 있지 않은 경우, 소프트웨어의 가치가 충분히 발휘되지 않을 가능성이 있음을 의미합니다.

부문별 분석

2025년 매출에서 소프트웨어가 차지하는 비중은 76.14%로, 구독형 플랫폼이 프랑스 그린 IT 소프트웨어 시장에서 여전히 주요 지출 부문임을 보여줍니다. 탄소 회계, ESG 보고, 지속가능성 데이터 관리 및 에너지 최적화는 주로 SaaS 모델을 통해 제공됩니다. 이 모델을 통해 공급업체는 보고 규칙을 일괄적으로 업데이트할 수 있으며, 고객 측의 유지보수 업무를 줄일 수 있습니다. 보고 의무가 끊임없이 변화하고, 공시 요건이 변경될 때마다 수작업에 의한 조정을 최소화하고자 하는 프랑스 기업들에게 이 모델은 유용합니다. 따라서 프랑스의 그린 IT 소프트웨어 업계는 계속해서 “소프트웨어 우선”라는 경향이 더욱 뚜렷해지고 있습니다. 이는 정기적인 업데이트가 가능한 플랫폼이 일회성 사내 개발보다 규제 변경에 더 효율적으로 대응할 수 있기 때문입니다.

소프트웨어가 신뢰할 수 있는 결과를 도출하기 위해서는 도입, 자문 업무 및 체계적인 보고 지원이 필요한 경우가 많기 때문에 서비스 부문 역시 여전히 중요합니다. 서비스 부문은 2031년까지 연평균 성장률(CAGR) 16.91%를 기록하며 성장할 것으로 예상되며, 프랑스 그린 IT 소프트웨어 시장에서 가장 높은 성장세를 보일 것으로 전망됩니다. 많은 기업에서는 배출 범위를 정의하고, 방법을 통합하며, 감사에 대응할 수 있는 업무 흐름을 준비할 수 있는 사내 지속가능성 전문가가 여전히 부족합니다. 슈나이더 일렉트릭의 자문 네트워크는 “2026 Impact 2030”의 최신판에서 컨설턴트 수가 4,000명을 넘어섰으며, 이는 대기업 고객들이 이러한 도입과 관련해 요구하는 지원의 규모를 보여주고 있습니다. 또한, 프랑스의 중견 기업 고객들은 국내 보고 관행에 부합하는 현지 지침이나 실질적인 도입 지원을 선호하는 경향이 있어, 소규모 전문 기업들도 이 부문에서 활약할 기회를 찾고 있습니다.

2025년, 프랑스 그린 IT 소프트웨어 시장 규모 중 64.17%를 클라우드 기반 도입이 차지하고 있으며, 이는 벤더 관리형 제공 방식이 많은 기업 구매자들에게 선호되는 모델임을 뒷받침하고 있습니다. 그 주요 장점은 편의성뿐만 아니라, 사내의 긴 업그레이드 주기를 거치지 않고도 ESRS 규칙, 분류 체계 공개 및 보고 템플릿의 지속적인 업데이트에 대응할 수 있다는 점에도 있습니다. 많은 기업에게 SaaS 방식은 도입 기간을 단축하고, 이미 업무에 쫓기고 있는 IT 팀의 부담을 덜어줍니다. 이로 인해 보고 요건이 더욱 복잡해지더라도, 클라우드 서비스는 프랑스 그린 IT 소프트웨어 시장에서 여전히 중심적인 위치를 차지하고 있습니다.

하이브리드 시장은 2031년까지 연평균 성장률(CAGR) 17.02%로 성장할 것으로 전망됩니다. 그 주된 이유는 규제 대상 부문에서 지속가능성 데이터의 처리 및 저장 장소에 대한 관리 강화가 요구되고 있기 때문입니다. 은행, 보험, 정부 기관, 의료 분야의 사용자들은 기밀성이 높은 업무 데이터나 보고 데이터에 대해 국내 또는 엄격하게 관리되는 인프라를 선호하는 경우가 많습니다. 이러한 수요가 클라우드의 유연성과 On-Premise 관리 요건을 결합한 하이브리드 아키텍처를 뒷받침하고 있습니다. 산업 분야나 국방 관련 환경에서는 여전히 On-Premise 방식이 사용되고 있지만, 벤더들이 클라우드 및 하이브리드 기반 제품 전략에 주력함에 따라 그 역할은 점차 축소되고 있습니다. OVHcloud와 같은 공급업체가 제공하는 소버린 클라우드 및 프라이빗 클라우드 솔루션 역시, 규정 준수 관련 우려와 외부 호스팅의 편의성 사이의 격차를 해소하는 데 일조하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the france green IT software market is expected to grow from USD 0.98 billion in 2025 to USD 1.12 billion in 2026, and reach USD 2.42 billion by 2031, at a CAGR of 16.66% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, and Energy and More), End User (IT and Telecom, BFSI, Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Green IT Software Market Trends and Insights

Strengthening EU and France Decarbonization Disclosure Pressure

France moved ahead of many other European countries in implementing CSRD-related obligations, which gave local enterprises less time to delay platform selection and data preparation for sustainability reporting. Large listed companies had already begun filing under the new framework in 2025, and other large companies are reporting in 2026 for the financial year 2025, which kept software demand tied to emissions accounting, ESRS mapping, and assurance-ready records. The Omnibus I Directive narrowed the mandatory scope to companies above the new employee and turnover thresholds, and that change reduced part of the direct mid-market pipeline in the short term. Even so, the France green IT software market still benefits when in-scope companies push sustainability data requests into their supplier base through procurement and compliance reviews. Oversight from the AMF and the need for audit-grade disclosures continue to favor software that can trace data quality, support controls, and prepare records for third-party assurance.

Rising Corporate Demand For IT Emissions Visibility

The France green IT software market is gaining from a basic measurement need, because the environmental weight of digital operations is now harder for enterprises to ignore. The ADEME and ARCEP study showed that the French digital sector accounted for 4.4% of the national carbon footprint, or 29.5 MtCO2e, with data centers contributing 46% and terminals 50% of that total. Electricity use at data centers connected to the public transmission network reached almost 1 TWh in 2025, up from 0.8 TWh in 2024, underscoring the need for closer monitoring of infrastructure use and stronger reporting controls. ARCEP's 2025 environmental survey also showed that Orange, Bouygues Telecom, SFR, and Iliad recorded aggregate scope 2 emissions of 397,000 tCO2e, a 4.2% year-on-year increase even as national emissions declined, reinforcing the case for sector-specific tracking tools. France's low-carbon grid keeps domestic electricity emissions comparatively low, but that pushes many companies to focus more closely on imported digital use, overseas hosting exposure, and broader scope 3 accounting within the France green IT software market.

Fragmented IT and Facilities Data Across Legacy Environments

A persistent constraint in the France green IT software market is that many companies still do not have clean, asset-level data across IT equipment, facilities, and hosting environments. ESRS E1 reporting needs detailed inputs for servers, network hardware, devices, and energy use, but legacy IT service management systems were not built for that level of environmental measurement. ARCEP's 2025 environmental survey showed that equipment-level granularity remains difficult, even for large telecommunications operators already accustomed to structured reporting. ADEME updated its methodological framework for hosted IT and cloud services in 2025, yet adoption remains uneven across smaller operators and private environments. This means software value can fall short when inventories are incomplete, energy meters are inconsistent, and the underlying data structure is weaker than the reporting requirement.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cloud Cost and Energy Optimization Use Cases

- Sustainability Procurement Requirements From Enterprise Buyers

- Integration Complexity With Existing ITSM, ERP, and Cloud Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 76.14% of revenue in 2025, indicating that subscription platforms remain the core spending category in the France green IT software market. Carbon accounting, ESG reporting, sustainability data management, and energy optimization are primarily delivered through SaaS models that enable vendors to centrally update reporting rules and reduce client maintenance work. That model is useful in France, where reporting obligations continue to change, and enterprises want fewer manual adjustments each time disclosure expectations shift. The France green IT software industry therefore keeps leaning toward software first, because recurring platforms can absorb regulatory updates more efficiently than one-off internal builds.

Services are still important because implementation, advisory work, and managed reporting support are often needed before software can produce reliable results. Services are projected to grow at a 16.91% CAGR through 2031, making them the fastest-growing segment of the France green IT software market. Many companies still lack internal sustainability specialists who can structure emissions boundaries, align methods, and prepare audit-ready workflows. Schneider Electric's advisory network, which exceeded 4,000 consultants in its 2026 Impact 2030 update, shows the scale of support that large enterprise customers are seeking around these deployments. Smaller specialist firms are also finding room in this segment because mid-sized French clients often prefer local guidance tied to national reporting practices and practical onboarding.

Cloud-based deployment captured 64.17% of the France green IT software market size in 2025, which confirms that vendor-managed delivery is the preferred model for many enterprise buyers. The main advantage is not only convenience, but also the ability to handle continuous updates in ESRS rules, taxonomy disclosures, and reporting templates without long internal upgrade cycles. For many enterprises, the SaaS approach also shortens implementation and reduces the burden on already stretched IT teams. This keeps cloud delivery at the center of the France green IT software market even as reporting needs become more complex.

Hybrid deployment is projected to grow at a 17.02% CAGR through 2031, mainly because regulated sectors need more control over where sustainability data is processed and stored. Banking, insurance, government, and healthcare users often want domestic or tightly governed infrastructure for sensitive operational and reporting data. This demand is sustaining hybrid architectures that mix cloud flexibility with local control requirements. On-prem deployments still exist in industrial and defense-linked settings, but their role is gradually narrowing as vendors focus more on cloud- and hybrid-based product paths. Sovereign and private cloud arrangements from providers such as OVHcloud are also helping bridge the gap between compliance concerns and the convenience of external hosting.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By End User

- IT and Telecom

- BFSI

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Government

- Healthcare

- Construction and Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- Salesforce, Inc.

- Microsoft Corporation

- SAP SE

- IBM Corporation

- Schneider Electric SE

- ServiceNow, Inc.

- Accenture plc

- Oracle Corporation

- Workiva Inc.

- Sphera Solutions, Inc.

- Persefoni AI, Inc.

- Watershed Technologies, Inc.

- Plan A Solutions GmbH

- Sweep SAS

- Greenly SAS

- Plan A Solutions GmbH

- Emitwise Ltd.

- Enablon SAS

- EcoVadis SAS

- Siemens AG

- Wolters Kluwer N.V.

- Dakota Software Corporation

- InnoGreen Technologies

- Sopra Steria

- OneStop ESG

- Tata Consultancy Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Corporate Demand for IT Emissions Visibility

- 4.2.2 Strengthening EU and France Decarbonization Disclosure Pressure

- 4.2.3 Expansion Of Cloud Cost And Energy Optimization Use Cases

- 4.2.4 Sustainability Procurement Requirements From Enterprise Buyers

- 4.2.5 Automation Of ESG Reporting Across IT Asset Portfolios

- 4.2.6 AI-Driven Workload Optimization For Data Center Efficiency

- 4.3 Market Restraints

- 4.3.1 Fragmented IT And Facilities Data Across Legacy Environments

- 4.3.2 Limited Internal Carbon Accounting Maturity In Mid-Market Firms

- 4.3.3 Integration Complexity With Existing ITSM, ERP, And Cloud Stacks

- 4.3.4 Budget Prioritization Toward Core Cybersecurity And Cloud Projects

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on The Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Intensity of Competitive Rivalry

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of New Entrants

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management and Accounting Software

- 5.4.2 ESG Reporting and Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy and Resource Optimization Software

- 5.5 By End User

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Salesforce, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 SAP SE

- 6.4.4 IBM Corporation

- 6.4.5 Schneider Electric SE

- 6.4.6 ServiceNow, Inc.

- 6.4.7 Accenture plc

- 6.4.8 Oracle Corporation

- 6.4.9 Workiva Inc.

- 6.4.10 Sphera Solutions, Inc.

- 6.4.11 Persefoni AI, Inc.

- 6.4.12 Watershed Technologies, Inc.

- 6.4.13 Plan A Solutions GmbH

- 6.4.14 Sweep SAS

- 6.4.15 Greenly SAS

- 6.4.16 Plan A Solutions GmbH

- 6.4.17 Emitwise Ltd.

- 6.4.18 Enablon SAS

- 6.4.19 EcoVadis SAS

- 6.4.20 Siemens AG

- 6.4.21 Wolters Kluwer N.V.

- 6.4.22 Dakota Software Corporation

- 6.4.23 InnoGreen Technologies

- 6.4.24 Sopra Steria

- 6.4.25 OneStop ESG

- 6.4.26 Tata Consultancy Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment