|

시장보고서

상품코드

2073274

중국의 그린 IT 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

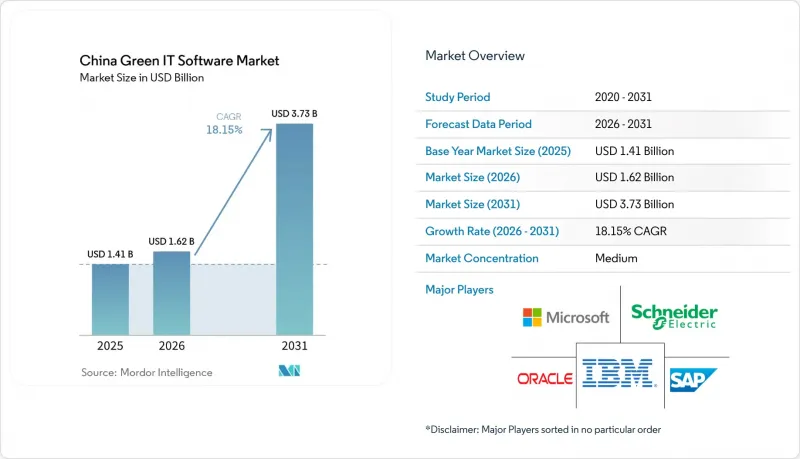

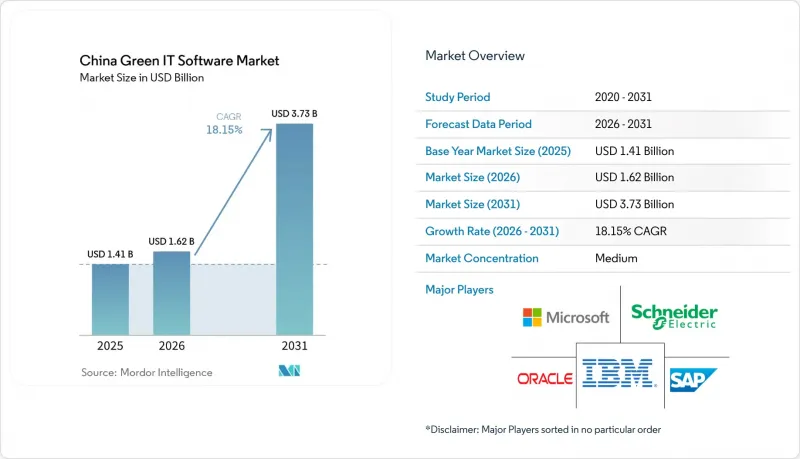

Mordor Intelligence에 의하면, 중국의 그린 IT 소프트웨어 시장 규모는 2025년에 14억 1,000만 달러로 평가되었습니다. 2026년에 16억 2,000만 달러에 달하고, 2031년까지 37억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 18.15%로 성장할 전망입니다.

본 보고서는 제공 형태(소프트웨어 및 서비스), 솔루션 유형(탄소 회계·보고 소프트웨어 등), 도입 형태(클라우드 기반 등), 조직 규모(대기업 및 중소기업), 최종 사용자 산업(정보기술·통신 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 그린 IT 소프트웨어 시장 동향 및 인사이트

'듀얼 카본' 정책의 추진력과 규정 준수의 디지털화

중국의 그린 IT 소프트웨어 시장은 단순히 장기적인 배출 목표를 제시하는 데 그치지 않고, 산업 기업들이 에너지 및 탄소 데이터 시스템을 어떻게 구축해야 하는지를 구체적으로 규정하는 정책 조치로부터 직접적인 지원을 받고 있습니다. 2025년 3월에 발표된 “디지털 에너지·탄소 관리 센터에 관한 지침”이는 산업 기업 및 산업 단지에 대해 보다 명확한 아키텍처 기준을 정하고 있으며, 이에 따라 소프트웨어 공급업체가 조달 과정에서 충족해야 하는 최소 기술 기준이 상향 조정되었습니다. 2025년 1월의 “제품 탄소 발자국 산정 지침”이는 제조업체를 대상으로 공급망 전반에 걸쳐 표준화된 제품 수준의 탄소 관리를 추진함으로써 추가적인 수요를 창출했습니다. 이로 인해 이용 사례는 시설 보고에만 그치지 않고 더욱 광범위한 영역으로 확대되고 있습니다. 이 정책의 추세가 중요한 이유는 소프트웨어 구매가 일회성 규정 준수 프로젝트에서 지속적인 플랫폼 투자로 전환되고 있기 때문입니다. 특히 공장, 산업단지, 기업 그룹이 공통된 데이터 구조를 필요로 하는 상황에서 이러한 경향은 두드러집니다. 중국의 그린 IT 소프트웨어 시장에서 이러한 변화는 기업의 업무 흐름에 부합하면서도 시스템 설계를 국가의 보고 논리에 맞출 수 있는 공급업체를 뒷받침할 것입니다. 또한, 첫 번째 보고 레이어가 도입되면 기업은 일반적으로 제품 데이터, 감사 지원, 공급업체와의 연동을 위한 추가 모듈이 필요하게 되므로, 장기적인 고객 기반 확대의 여지도 생깁니다.

자동화된 탄소 회계에 대한 기업 수요 증가

중국의 그린 IT 소프트웨어 시장은 스프레드시트 기반의 탄소 추적에서 자동화되고 감사 가능한 보고 워크플로로 전환되는 과정에서도 혜택을 보고 있습니다. 현재 기업들은 더욱 강력한 데이터 추적성, 보다 명확한 승인 절차, 그리고 업무 기록과 공개 결과물 간의 보다 직접적인 연계를 필요로 하고 있으며, 이는 재무, ERP, 클라우드 환경에 통합된 플랫폼에 유리하게 작용하고 있습니다. Kingdee의 2025년도 결산에 따르면, 클라우드 구독 매출은 전년 대비 20.9% 증가한 35억 5,600만 위안(4억 8,800만 달러)에 달했으며, 이 회사의 Kingdee AI 플랫폼은 ESG 시나리오를 포함한 다양한 이용 사례에서 20개에 가까운 AI 에이전트를 배포했습니다. 이 결과는 자동화된 ESG 및 탄소 보고 기능이 틈새 시장용 지속가능성 도구에 그치지 않고, 기업의 소프트웨어 지출에서 주류로 자리 잡고 있음을 보여주며, 상업적으로 중요한 의미를 지닙니다. 중국의 그린 IT 소프트웨어 시장에서 이는 기업이 이미 재무 관리 및 업무 관리에 활용하고 있는 시스템 내에서 데이터 수집과 검증을 자동화할 수 있는 공급업체에게 경쟁 우위를 가져다줍니다. 또한, 카본 워크플로가 핵심이 되는 기록 및 승인 프로세스와 연동되면, 기업은 수동 보고나 연동되지 않은 전문 도구로 되돌아가는 것을 주저하게 되므로, 시간이 지남에 따라 전환 비용이 증가하게 됩니다.

분산된 배출 데이터와 취약한 시스템 간의 상호 운용성

데이터 분산은 여전히 중국의 그린 IT 소프트웨어 시장에서 가장 뚜렷한 운영상의 제약 요소 중 하나입니다. 이는 많은 기업이 여전히 생산, 조달, 시설, 물류에 관한 기록을 서로 연동되지 않은 여러 시스템에 걸쳐 관리하고 있기 때문입니다. 중국공정원 전략연구소가 2024년에 발표한 조사 보고서에 따르면, 산업 부문 전반에 걸쳐 신뢰성이 높고 통일된 배출 계수 데이터베이스가 부족하다는 점이 지적되었습니다. 이로 인해 비교 가능하고 감사 가능한 탄소 인벤토리를 작성하기가 어려워지고 있습니다. 이 문제는 단순한 소프트웨어 통합의 문제에 그치지 않습니다. 이는 서로 다른 소스 시스템에서 규제상의 보고 요건과 일치하지 않는 방식으로 경계, 단위, 활동 범주가 정의되는 경우가 많기 때문입니다. 그 때문에 기업에는 소프트웨어 예산이나 보고 의무가 있음에도 불구하고, 외부 심사 담당자가 수작업으로 수정할 필요 없이 대조할 수 있는 기록을 작성하는 데 어려움을 겪는 경우가 있습니다. 중국의 그린 IT 소프트웨어 시장에서는 도입 주기가 지연되면서 서비스 부하가 높은 수준을 유지하고 있습니다. 이는 고객이 플랫폼의 가치를 충분히 체감하기도 전에 공급업체가 데이터 매핑에 막대한 시간을 투자해야 하기 때문입니다. 또한, 통합 계층의 문제가 해결되면 기존 공급업체는 유리한 입지를 유지할 수 있습니다. 왜냐하면 독자적인 데이터 구조나 워크플로가 확립되면 타사 제품으로 전환하기가 어려워지기 때문입니다.

부문별 분석

이 소프트웨어는 계속해서 중국의 그린 IT 소프트웨어 시장을 독점하고 있으며, 2025년에는 67.41%의 점유율을 차지했습니다. 이는 ERP나 클라우드 환경 내의 탄소 회계 및 ESG 공시 시스템과 같은 통합 도구에 대한 기업 수요에 힘입은 것입니다. 기업들은 기록의 일원화, 계산의 자동화, 재사용 가능한 보고서 구조의 구현을 위해 소프트웨어에 대한 의존도를 높이고 있으며, 이를 통해 수작업 개입이 줄어들고 거버넌스와 지속성이 향상되고 있습니다. 조달 전략이 발전함에 따라 구매 담당자들은 통합의 깊이, 확장성, 워크플로우의 추적 가능성을 우선시하며, 단일 대시보드보다 종합적인 엔터프라이즈 솔루션을 제공하는 공급업체를 선호하는 추세입니다. SAP가 2026년 5월에 지속가능성 AI 에이전트를 출시한 것은 시장의 초점이 자동화의 품질과 운영상의 호환성으로 이동하고 있음을 보여주며, 구매 기준이 더욱 엄격해지고 있음에도 불구하고 소프트웨어가 여전히 핵심적인 역할을 수행하고 있음을 입증합니다.

서비스 시장은 2031년까지 연평균 성장률(CAGR) 19.63%를 나타낼 것으로 예측되며, 이는 도입 과정의 복잡성을 해결하는 데 있어 서비스의 전략적 중요성을 반영하고 있습니다. 기업은 특히 여러 거점이나 보고 체계에 걸쳐 사업을 전개할 경우, 플랫폼의 가치를 극대화하기 위해 데이터 준비, 워크플로우 설계, 규정 준수 관리에 대한 지원이 필요합니다. 이러한 추세는 강력한 제품 라인업과 효과적인 도입 서비스를 결합한 공급업체에게 유리하게 작용합니다. 관리형 검증, 자문 지원, 프로세스 재설계는 고객 관계와 계약 갱신율을 향상시키기 때문입니다. 그 결과, 시장은 순수한 라이선스 모델에서 소프트웨어 및 서비스가 하나로 결합되어 가치와 운영상의 통합을 추진하는 혼합형 구조로 전환되고 있습니다.

탄소 회계는 중국의 그린 IT 소프트웨어 시장의 핵심 분야로 자리매김할 것이며, 2025년에는 32.41%의 시장 점유율을 차지했습니다. 이는 배출량 추적, 공개 및 운영 분석을 위한 기반 계층 역할을 하며, 기업이 보다 광범위한 지속가능성 활동을 추진하기 전에 신뢰할 수 있는 기록을 구축할 수 있도록 해줍니다. 일관된 데이터 수집, 빈번한 검토 및 표준화된 보고에 대한 수요가 증가함에 따라, 각 벤더들은 탄소 회계를 재무 및 업무 소프트웨어에 통합하여 워크플로우의 효율성을 높이고 있습니다. 에너지 관리 도구와 지속가능성 성과 솔루션이 주목을 받고 있지만, 기업들은 이를 탄소 회계를 보완하는 수단으로 도입하는 경우가 많으며, 이는 모듈형 성장 접근 방식을 반영하고 있습니다. 이러한 계층적 도입 전략은 다른 솔루션 부문이 확대되고 있음에도 불구하고, 탄소 회계가 여전히 중심적인 위치를 차지하고 있는 이유를 여실히 보여줍니다.

지속가능성 데이터 관리 플랫폼은 2031년까지 연평균 성장률(CAGR)이 21.26%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 부문으로 부상하고 있습니다. 이러한 플랫폼들은 배출량, 에너지, 물 및 사회 관련 데이터를 통합하여 전사적으로 활용할 수 있는 통일된 프레임워크로 정리함으로써, 점점 높아지는 수요에 대응하고 있습니다. 기본적인 탄소 관리 도구만으로는 종합적인 보고 및 모니터링에 필요한 복잡한 데이터 간의 연관성을 관리하기에 부족한 경우가 적지 않습니다. 산재된 기록을 체계적인 보고 기반으로 전환함으로써, 데이터 관리 플랫폼은 운영 데이터에 대한 통합적인 거버넌스를 추구하는 기업에게 필수적인 요소로 자리 잡고 있습니다. 이러한 동향은 중국의 그린 IT 소프트웨어 시장에서 이러한 플랫폼이 보다 광범위한 지속가능성 목표를 뒷받침하는 데 있어 중요한 역할을 하고 있음을 여실히 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the china green IT software market size is projected to be USD 1.41 billion in 2025, USD 1.62 billion in 2026, and reach USD 3.73 billion by 2031, growing at a CAGR of 18.15% from 2026 to 2031.

This report is Segmented by Offering (Software, and Services), Solution Type (Carbon Accounting and Reporting Software, and More), Deployment (Cloud-Based, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Information Technology and Telecommunications, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Green IT Software Market Trends and Insights

Dual-Carbon Policy Momentum and Compliance Digitization

The China green IT software market is gaining direct support from policy measures that now specify how industrial firms should build energy and carbon data systems, rather than only stating long-term emissions goals. The March 2025 guidelines for digital energy-carbon management centers set a clearer architecture baseline for industrial enterprises and parks, which raises the minimum technical standard that software vendors must meet in procurement processes. The January 2025 product carbon footprint accounting guidelines added another layer of demand by pushing manufacturers toward standardized product-level carbon management across supply chains, which broadens the use case beyond facility reporting alone. This policy pattern matters because it shifts software buying from one-time compliance projects toward recurring platform investment, especially where factories, parks, and enterprise groups need common data structures. In the China green IT software market, this change supports vendors that can align system design with national reporting logic while still fitting enterprise workflows. It also creates room for long-term account expansion, because once the first reporting layer is installed, enterprises usually need additional modules for product data, audit support, and supplier engagement.

Rising Enterprise Demand for Automated Carbon Accounting

The China green IT software market is also benefiting from the move away from spreadsheet-based carbon tracking toward automated and auditable reporting workflows. Enterprises now need stronger data traceability, cleaner approval chains, and more direct links between operational records and disclosure outputs, which favors platforms embedded in finance, ERP, and cloud environments. Kingdee's FY2025 results showed that its cloud subscription revenue rose 20.9% year on year to RMB 3,556 million, or USD 488 million, while its Kingdee AI platform deployed nearly 20 AI agents across use cases that included ESG scenarios. That result is commercially important because it shows that automated ESG and carbon reporting functions are moving into mainstream enterprise software spending rather than remaining niche sustainability tools. In the China green IT software market, this gives an advantage to vendors that can automate data collection and validation inside systems enterprises already use for financial and operating control. It also raises switching costs over time, since once carbon workflows are linked to core records and approvals, enterprises are less willing to return to manual reporting or disconnected specialist tools.

Fragmented Emissions Data and Weak System Interoperability

Fragmented data remains one of the clearest operating limits on the China green IT software market, because many enterprises still manage production, procurement, facility, and logistics records across disconnected systems. A 2024 study published by the Strategic Study of the Chinese Academy of Engineering highlighted the lack of a credible and unified emissions factor database across industrial sectors, which makes it harder to produce comparable and auditable carbon inventories. This problem is larger than a basic software integration issue, because different source systems often define boundaries, units, and activity categories in ways that do not match regulatory reporting needs. Enterprises may therefore have the software budget and the reporting obligation, yet still struggle to generate records that external reviewers can reconcile without manual correction. In the China green IT software market, which slows implementation cycles and keeps service intensity high, because vendors often need to spend significant time on data mapping before customers see full platform value. It also protects incumbents once they solve the integration layer, since replacement becomes harder after custom data structures and workflows are in place.

Other drivers and restraints analyzed in the detailed report include:

- AI Enabled Energy Optimization Across Data Centers and Industrial IT

- Expanding ESG Disclosure Requirements Across Export-Oriented Firms

- Limited In-House Sustainability Data Governance in Small and Medium Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software continues to dominate China green IT software market, holding a 67.41% share in 2025, driven by enterprise demand for integrated tools like carbon accounting and ESG disclosure systems within ERP and cloud environments. Businesses increasingly rely on software for centralized records, automated calculations, and reusable reporting structures, reducing manual interventions and enhancing governance and continuity. As procurement strategies evolve, buyers prioritize integration depth, scalability, and workflow traceability, favoring vendors offering comprehensive enterprise solutions over standalone dashboards. SAP's May 2026 launch of sustainability AI agents highlights the market's shift toward automation quality and operational compatibility, reinforcing software's central role despite more stringent buying criteria.

Services are projected to grow at an 19.63% CAGR through 2031, reflecting their strategic importance in addressing the complexities of implementation. Enterprises require support in data preparation, workflow design, and compliance management to maximize platform value, especially when operating across multiple sites or reporting frameworks. This trend benefits vendors combining strong product offerings with effective implementation services, as managed validation, advisory support, and process redesigns enhance customer relationships and renewal rates. Consequently, the market is transitioning from a pure license model to a blended structure where software and services collectively drive value and operational integration.

Carbon accounting remains the backbone of China green IT software market, holding a 32.41% share in 2025. It serves as the foundational layer for emissions tracking, disclosure, and operational analysis, enabling enterprises to establish reliable records before advancing to broader sustainability initiatives. The growing need for consistent data collection, frequent reviews, and standardized reporting has driven vendors to integrate carbon accounting into finance and operations software, enhancing workflow efficiency. While energy management tools and sustainability performance solutions are gaining traction, enterprises often adopt these as complementary layers to carbon accounting, reflecting a modular growth approach. This layered adoption strategy underscores why carbon accounting remains central, even as other solution categories expand.

Sustainability data management platforms are emerging as the fastest-growing segment, with a projected CAGR of 21.26% through 2031. These platforms address the increasing demand for consolidating emissions, energy, water, and social data into a unified framework for enterprise-wide use. Basic carbon tools often fall short in managing complex data relationships required for comprehensive reporting and oversight. By transforming scattered records into a structured reporting backbone, data management platforms are becoming indispensable for enterprises seeking centralized governance of operational data. This trend highlights their critical role in supporting broader sustainability goals within China's green IT software market.

Complete Report Scope:

- By Offering

- Software

- Services

- By Solution Type

- Carbon Accounting and Reporting Software

- Energy Management and Optimization Software

- ESG Data Management Software

- Sustainability Performance Management Software

- Green Data Center Management Software

- By Deployment Mode

- Cloud-Based

- On Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Industry

- IT and Telecommunications

- Manufacturing

- Banking, Financial Services, and Insurance (BFSI)

- Government and Public Sector

- Energy and Utilities

- Healthcare and Life Sciences

- Retail and E-Commerce

- Construction and Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Schneider Electric SE

- Siemens AG

- ABB Ltd.

- Honeywell International Inc.

- Huawei Technologies Co., Ltd.

- Alibaba Group Holding Limited

- Tencent Holdings Limited

- Baidu, Inc.

- Kingdee International Software Group Company Limited

- Yonyou Network Technology Co., Ltd.

- Inspur Group Co., Ltd.

- H3C Technologies Co., Ltd.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Salesforce, Inc.

- ServiceNow, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Dual-Carbon Policy Momentum and Compliance Digitization

- 4.2.2 Rising Enterprise Demand for Automated Carbon Accounting

- 4.2.3 AI Enabled Energy Optimization Across Data Centers and Industrial IT

- 4.2.4 Expanding ESG Disclosure Requirements Across Export Oriented Firms

- 4.2.5 Growth of Cloud Native Sustainability Platforms for Multi Site Operations

- 4.2.6 Integration of Green IT with Enterprise Resource Planning and Operations Systems

- 4.3 Market Restraints

- 4.3.1 Fragmented Emissions Data and Weak System Interoperability

- 4.3.2 Limited In House Sustainability Data Governance in Small and Medium Enterprises

- 4.3.3 High Implementation Friction for Legacy on Premises Environments

- 4.3.4 Shortage of Standardized Verification and Audit Ready Data Workflows

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Solution Type

- 5.2.1 Carbon Accounting and Reporting Software

- 5.2.2 Energy Management and Optimization Software

- 5.2.3 ESG Data Management Software

- 5.2.4 Sustainability Performance Management Software

- 5.2.5 Green Data Center Management Software

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On Premises

- 5.3.3 Hybrid

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 Manufacturing

- 5.5.3 Banking, Financial Services, and Insurance (BFSI)

- 5.5.4 Government and Public Sector

- 5.5.5 Energy and Utilities

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Retail and E-Commerce

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 SAP SE

- 6.4.4 Oracle Corporation

- 6.4.5 Schneider Electric SE

- 6.4.6 Siemens AG

- 6.4.7 ABB Ltd.

- 6.4.8 Honeywell International Inc.

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 Alibaba Group Holding Limited

- 6.4.11 Tencent Holdings Limited

- 6.4.12 Baidu, Inc.

- 6.4.13 Kingdee International Software Group Company Limited

- 6.4.14 Yonyou Network Technology Co., Ltd.

- 6.4.15 Inspur Group Co., Ltd.

- 6.4.16 H3C Technologies Co., Ltd.

- 6.4.17 Dell Technologies Inc.

- 6.4.18 Hewlett Packard Enterprise Company

- 6.4.19 Salesforce, Inc.

- 6.4.20 ServiceNow, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Adoption Barriers by Buyer Segment

- 7.3 Product Innovation Roadmap