|

시장보고서

상품코드

2073216

베트남의 그린 IT 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vietnam Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

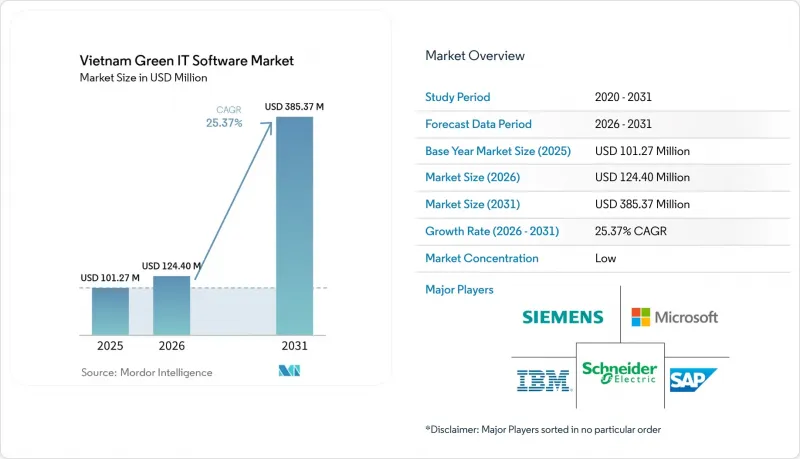

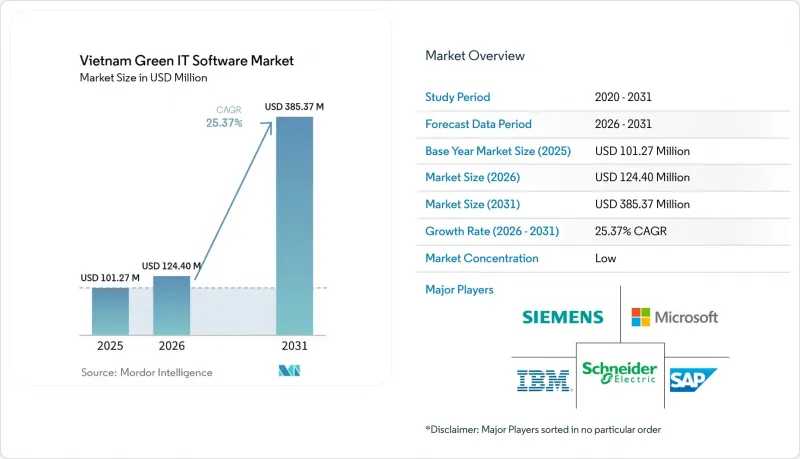

Mordor Intelligence에 의하면, 베트남의 그린 IT 소프트웨어 시장 규모는 2025년에 1억 127만 달러로 평가되었습니다. 2026년 1억 2,440만 달러에서 2031년까지 3억 8,537만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 25.37%를 나타낼 전망입니다.

본 보고서는 제공 형태(소프트웨어 및 서비스), 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 기업 규모(대기업 및 중소기업), 솔루션 유형(탄소 관리·산정 소프트웨어 등), 최종 사용자(정보기술·통신, 제조, 정부 기관 등)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

베트남의 그린 IT 소프트웨어 시장 동향 및 인사이트

탄소 및 에너지 추적성 확보를 위한 규제 추진

베트남의 국내 배출권 거래 제도 시범 사업은 2025년 8월에 시작되었으며, 2026년 1월에는 제29/2026/ND-CP호 정령에 따라 하노이 증권거래소가 운영하는 국내 탄소 거래소가 설립됨에 따라 규제 체계가 더욱 구체화되었습니다. 이어서, 고시 제11/2026/TT-BNNMT호에 따라 국가 탄소 등록부가 설립되었으며, 할당량 및 크레딧의 발행, 이전, 취소에 대한 전자적 추적이 의무화되었습니다. 이로 인해 디지털 기록 관리는 단순한 선택적 행정 도구가 아니라 기능상의 필수 요건이 되었습니다. 베트남의 그린 IT 소프트웨어 시장은 이러한 변화에 대응하고 있습니다. 이는 대상인 110개 시설에서 스프레드시트만으로는 대규모로 쉽게 지원하기 어려운, 감사 가능한 배출 인벤토리와 추적 가능한 워크플로가 필요하기 때문입니다. 완전한 시행은 2029년으로 예상되고 있기 때문에 구매 기업들은 현재의 보고 대응에 그치지 않고, 향후 몇 년 동안 더욱 엄격해질 규정 준수 주기에 대비해 시스템 구축을 추진하고 있습니다. 또한, 레지스트리의 구조상 불충분한 기준 데이터는 비용 증가로 이어집니다. 왜냐하면, 공식적인 감사 추적을 통해 오류가 드러나면 과거 보고 기간과 관련된 위험이 발생할 가능성이 있기 때문입니다. '2026년 기업지배구조 코드'에 따른 기후 거버넌스 요건으로 인해 수요 기반은 더욱 확대되고 있습니다. 현재 상장기업은 환경 모니터링 및 공시 절차와 관련하여 이사회에 더 강력한 설명 책임을 요구받고 있기 때문입니다.

클라우드 전환 및 하이브리드 아키텍처 현대화

베트남에서의 엔터프라이즈 클라우드 도입은 단순히 인프라 비용을 절감하는 데 그치지 않고, ESG 데이터 수집, 워크플로우 통합, 그리고 여러 거점에 걸친 보고를 지원하는 단계에 이르렀습니다. 2026년 아키텍처와 관련된 실무상의 과제는 단순히 ‘"클라우드인가, On-Premise인가"라는 선택이 아니라, 멀티 클라우드의 유연성, 로컬 호스팅, 데이터 상주성 및 시스템 통합을 단일 운영 모델에 어떻게 통합할 것인가 하는 점에 있습니다. 따라서 베트남의 그린 IT 소프트웨어 시장에서는 보고서의 연속성을 해치지 않으면서 ERP 시스템과 연동하고, 규제 대상 데이터의 저장 및 분석 워크로드를 분리할 수 있는 플랫폼에 대한 수요가 높아지고 있습니다. 마이크로소프트가 2026년에 출시한 ‘“지속가능성 관리자”이는 주요 엔터프라이즈 벤더들이 기존 비즈니스 소프트웨어 환경에 지속가능성 기능을 직접 통합함으로써, 이 분야 전반의 자동화 및 통합 수준을 높이고 있음을 보여줍니다. 이는 베트남 구매자들에게 중요한 의미를 지닙니다. 왜냐하면 현지 사이버 보안 의무와 해외 모회사의 보고 요건이 종종 공존하기 때문에 그러한 상황에서는 하이브리드 모델이 가장 현실적인 방안이기 때문입니다. 그 결과, 도입 결정은 더욱 전략적인 성격을 띠게 되었으며, 규정 준수, 상호 운용성, 아키텍처의 유연성을 지원할 수 있는 벤더들이 베트남의 그린 IT 소프트웨어 시장에서 우위를 점하고 있습니다.

클라우드 보안, 데이터 아키텍처 및 탄소 회계 분야의 인력 부족

베트남의 그린 IT 소프트웨어 시장에서 주요 실무적 장벽은 인지도 부족이 아니라, 시스템을 구축하고 데이터 품질을 관리하며 보고 규정을 실용적인 업무 흐름으로 전환할 수 있는 인재의 부족입니다. 베트남은 70만 명의 ICT 전문가를 목표로 삼았으나, 2025년 노동 인구는 55만 명 수준에 그쳤으며, 졸업생 중 기업에서 즉시 업무에 투입될 수 있는 인재로 평가된 비율은 고작 30%에 불과했습니다. 동시에 친환경 인재 채용 경쟁이 치열해지고 있으며, ESG 전문직의 급여는 유사한 IT 직종에 비해 15-25% 높은 수준을 보이고 있습니다. 이러한 인재 문제는 기업의 지속가능성 팀에만 국한되지 않고, 베트남에서는 탄소 크레딧 시장을 뒷받침하기 위해 약 15만 명의 전문 인력이 필요한 것으로 나타나, 제조업, 금융업, 기술 업계의 고용주들이 제한된 인재 풀을 놓고 직접 경쟁하는 상황에 놓여 있습니다. 이러한 인력 부족으로 인해 소프트웨어 구매 후 도입이 지연되고 있습니다. 기업에는 여전히 자산 대장 작성, 데이터 검증, 시스템 연동, 지속적인 보고 주기 관리를 수행할 수 있는 인력이 필요하기 때문입니다. 그 결과, 고객의 도입 의지가 여전히 높은 경우에도 라이선스 이용률, 프로젝트 일정, 그리고 사업 확장에 따른 수익에 부정적인 영향을 미치고 있습니다.

부문별 분석

2025년, 베트남의 그린 IT 소프트웨어 시장에서 소프트웨어가 66.45%의 점유율을 차지했습니다. 이는 초기 투자가 아웃소싱을 통한 제공이 아니라 플랫폼 소유에 중점을 두었음을 보여줍니다. 기업들은 우선 탄소 관리 도구, ESG 보고 시스템, 지속가능성 데이터 플랫폼으로 전환했습니다. 이러한 제품들은 최근의 제출, 감사, 고객 보고와 같은 요구 사항에 가장 부합했기 때문입니다. 이러한 경향은 데이터 입력이나 승인 절차를 직접 관리해야 했던 규제 대상 사업자나 수출 지향 기업에서 특히 두드러졌습니다. 많은 기업이 첫 번째 공식 온실가스 인벤토리 작성이나 내부 거버넌스 체계 구축 단계에 있었기 때문에 라이선스 기반 소프트웨어도 초기 구매 주기에 적합했습니다. 실제로 구매자는 원본 데이터를 수집하고, 감사 추적을 보관하며, 향후 엔터프라이즈 시스템과의 통합을 지원할 수 있는 도구를 원하고 있었습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 26.88%로 확대될 것으로 예상되며, 이는 베트남의 그린 IT 소프트웨어 시장에서 초기 구매 후 도입 지원의 가치가 높아지는 제2단계가 도래할 것임을 시사합니다. 이러한 수요는 사내의 ESG 분석 역량, 탄소 회계 노하우, 기술적 통합 역량에서의 격차에 의해 주도되고 있으며, 많은 기업에게 외부 지원이 필수적입니다. 2026년에 SAP가 선보일 지속가능성 AI 에이전트 역시, 특히 보고서 작성, 시뮬레이션, 규정 준수 문서 작성 분야에서 소프트웨어와 자문 업무의 워크플로가 점차 융합되고 있음을 보여줍니다. 이러한 상황에서 현지 도입 파트너의 중요성은 점점 더 커지고 있으며, ESEC과 IBM Envizi의 제휴는 세계 플랫폼이 베트남 내 현지 도입 역량과 어떻게 결합되고 있는지를 보여주는 대표적인 사례입니다. 즉, 규정 준수 요건이 더욱 세분화됨에 따라, 향후 수익 성장은 도입 프로젝트뿐만 아니라 관리형 보고, 감사 지원, 플랫폼 튜닝 및 지속적인 통합 작업에서도 비롯될 것입니다.

2025년 베트남의 그린 IT 소프트웨어 시장에서 클라우드 기반 솔루션의 도입 비중은 57.81%를 차지했습니다. 이는 여러 시설에서 데이터를 수집하고, 사업 부문 전반에 걸쳐 보고를 통합해야 할 필요성에 기인한 것입니다. 클라우드 모델은 배출량 및 에너지 데이터에 매우 적합합니다. 왜냐하면 기업은 대부분의 경우 각 사업장, 공급업체, 보고 팀 전반에 걸쳐 실시간 또는 준실시간 가시성이 필요하기 때문입니다. 또한, 클라우드 모델은 업데이트 속도 향상, 협업의 용이성 증대, 최신 엔터프라이즈 용도과의 통합성 향상도 지원합니다. 이로 인해, 기존의 로컬 도구를 확장하는 대신 지속가능성 시스템을 처음부터 구축하는 기업들에게 클라우드가 기본적인 선택지가 되고 있습니다. 따라서 베트남의 그린 IT 소프트웨어 시장은 확장성과 원격 접속이 가치 창출의 핵심이 되는 '클라우드 퍼스트'의 설계 쪽으로 기울고 있습니다.

하이브리드 방식은 2031년까지 연평균 성장률(CAGR) 26.33%로 확대될 것으로 예상되며, 세계 보고 기준과 베트남의 데이터 처리 규정을 조화롭게 준수해야 하는 기업들에게 가장 전략적인 아키텍처 선택지로 자리 잡고 있습니다. 로컬 스토리지나 데이터 보관에 관한 규제가 엄격한 경우, 순수한 클라우드 모델에서는 우려가 발생할 수 있습니다. 반면, 완전한 On-Premise 모델의 경우, 공급업체와의 연계나 대규모 분석에 있어 유연성이 떨어질 우려가 있습니다. 하이브리드 아키텍처는 기밀 데이터를 국내에 보관하면서, 분석, 자동화, 워크플로우 조정에는 보다 광범위한 클라우드 리소스를 활용함으로써, 그 중간적인 해결책을 제공합니다. 마이크로소프트의 지속가능성 제품 로드맵과 베트남의 사이버 보안 정책은 모두 이러한 추세를 뒷받침하고 있으며, 구매자들은 기업 및 현지 규정 준수 요건을 모두 충족하는 시스템을 점점 더 많이 요구하고 있습니다. 그 결과, 베트남의 그린 IT 소프트웨어 시장에서의 도입 결정은 더 이상 단순한 IT상의 선호 문제가 아니라, 보다 광범위한 리스크 및 규정 준수 전략의 일부가 되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the vietnam green IT software market size was valued at USD 101.27 million in 2025 and estimated to grow from USD 124.40 million in 2026 to reach USD 385.37 million by 2031, at a CAGR of 25.37% during the forecast period (2026-2031).

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, and More), and End User (Information Technology and Telecom, Manufacturing, Government, and More). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Green IT Software Market Trends and Insights

Regulatory Push for Carbon and Energy Traceability

Vietnam's domestic emissions trading system pilot started in August 2025, and the regulatory framework became much more concrete in January 2026 when Decree No. 29/2026/ND-CP established a domestic carbon exchange operated by the Hanoi Stock Exchange. Circular No. 11/2026/TT-BNNMT then established the national carbon registry and required electronic tracking for the issuance, transfer, and cancellation of quotas and credits, thereby making digital recordkeeping a functional requirement rather than an optional administrative tool. The Vietnam Green IT Software Market is responding to this shift because 110 covered installations now need auditable emissions inventories and traceable workflows that spreadsheets cannot easily support at scale. Full implementation is expected in 2029, so buyers are not only reacting to today's filings but also preparing their systems for a tighter compliance cycle over the next few years. The registry structure also raises the cost of weak baseline data, because errors can become visible across a formal audit trail and create exposure tied to prior reporting periods. Climate governance requirements under the Corporate Governance Code 2026 further broaden the demand base, as listed companies now face stronger board accountability for environmental oversight and disclosure processes.

Cloud Migration and Hybrid Architecture Modernization

Enterprise cloud adoption in Vietnam has reached a point where it supports ESG data collection, workflow integration, and reporting across multiple sites, rather than simply lowering infrastructure costs. The practical architecture question in 2026 is not simply cloud versus on-premise, but how to combine multi-cloud flexibility, local hosting, data residency, and systems integration in a single operating model. That is why the Vietnam Green IT Software Market is seeing a stronger pull for platforms that can connect with ERP systems and separate regulated data storage from analytics workloads without breaking reporting continuity. Microsoft's 2026 Sustainability Manager release shows how large enterprise vendors are building sustainability features directly into existing business software environments, raising the baseline for automation and integration across the category. This matters for buyers in Vietnam because local cybersecurity obligations and global parent reporting requirements often coexist, and a hybrid model is the most workable path in that setting. As a result, deployment decisions are becoming more strategic, and software vendors that can support compliance, interoperability, and architecture flexibility are gaining an advantage in the Vietnam Green IT Software Market.

Talent Shortage in Cloud Security, Data Architecture, and Carbon Accounting

The main practical barrier for the Vietnam Green IT Software Market is not awareness, but the shortage of people who can configure systems, manage data quality, and translate reporting rules into usable workflows. Vietnam targeted 700,000 ICT professionals, but the workforce stood near 550,000 in 2025, and only 30% of graduates were considered immediately ready for enterprise roles. At the same time, green hiring is becoming more competitive, with ESG specialist roles commanding a 15-25% salary premium over similar IT positions. The labor challenge is broader than corporate sustainability teams, as Vietnam also needs around 150,000 specialized workers to support the carbon credit market, placing manufacturing, finance, and technology employers in direct competition for the same small talent pool. That shortage slows deployment after software is purchased, because companies still need staff who can build inventories, validate data, connect systems, and manage ongoing reporting cycles. The result is a drag on license utilization, project timelines, and expansion revenue, even when customer intent to adopt remains strong.

Other drivers and restraints analyzed in the detailed report include:

- Green Data Center and Energy Efficiency Mandates

- Export-Oriented Compliance Pressure from CBAM and ESG Rules

- Data Localization and Compliance Complexity for Foreign Vendors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 66.45% of the Vietnam Green IT Software Market share in 2025, which shows that the first wave of spending centered on platform ownership rather than outsourced delivery. Companies moved first toward carbon management tools, ESG reporting systems, and sustainability data platforms because these products are closest to immediate filing, audit, and customer reporting needs. This pattern was especially clear among regulated operators and export-facing enterprises that needed direct control over data inputs and approval steps. License-based software also fits the early buying cycle because many companies were still establishing their first formal greenhouse gas inventories and internal governance structures. In practice, buyers wanted tools that could capture source data, preserve audit trails, and support future integration with enterprise systems.

Services are projected to expand at a 26.88% CAGR through 2031, indicating a second phase in the Vietnam Green IT Software Market in which implementation support becomes more valuable after the initial purchase. The demand is driven by gaps in internal ESG analytics capacity, carbon accounting know-how, and technical integration skills, making outside help necessary for many companies. SAP's sustainability AI agent rollout in 2026 also shows that software and advisory workflows are converging, especially for reporting preparation, simulation, and compliance documentation. Local delivery partners are becoming increasingly important in this context, and ESEC's IBM Envizi partnership is a strong example of how global platforms are packaged with local implementation capabilities in Vietnam. That means future revenue growth should come not only from setup projects, but also from managed reporting, audit support, platform tuning, and recurring integration work as compliance needs become more detailed.

Cloud-based deployment accounted for 57.81% of the Vietnam Green IT Software Market in 2025, supported by the need to collect data from multiple facilities and consolidate reporting across business units. Cloud models are well-suited to emissions and energy data because companies often need real-time or near-real-time visibility across sites, suppliers, and reporting teams. They also support faster updates, easier collaboration, and better integration with modern enterprise applications. This has made the cloud the default path for companies building sustainability systems from scratch rather than extending older local tools. The Vietnam Green IT Software Market has therefore leaned toward cloud-first designs where scalability and remote access are central to value creation.

Hybrid deployment is projected to expand at a 26.33% CAGR through 2031, making it the most strategic architecture choice for companies balancing global reporting standards with Vietnamese data-handling rules. A pure cloud model can raise concerns when local storage or data residency rules are strict, while a fully on-premises model can reduce flexibility for supplier collaboration and large-scale analytics. Hybrid architecture offers a middle path by keeping sensitive data onshore while still using broader cloud resources for analytics, automation, and workflow coordination. Microsoft's sustainability product roadmap and Vietnam's cybersecurity direction both support this pattern, as buyers increasingly want systems that meet both corporate and local compliance requirements. As a result, deployment choice in the Vietnam Green IT Software Market is no longer a narrow IT preference, but part of a broader risk and compliance strategy.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By End User

- Information Technology and Telecom

- Banking, Financial Services, and Insurance

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Government

- Healthcare and Life Sciences

- Construction and Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- Schneider Electric SE

- Microsoft Corporation

- IBM Corporation

- SAP SE

- Workiva Inc.

- Watershed Technology, Inc.

- Persefoni AI, Inc.

- Sweep SAS

- Normative AB

- EcoVadis SAS

- Diligent Corporation

- Sphera Solutions, Inc.

- Plan A

- Greenly

- Novisto Inc.

- Cority Software Inc.

- Enablon North America Corp.

- Siemens AG

- Honeywell International Inc.

- Johnson Controls International plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Push for Carbon and Energy Traceability

- 4.2.2 Cloud Migration and Hybrid Architecture Modernization

- 4.2.3 Green Data Center and Energy Efficiency Mandates

- 4.2.4 Export-Oriented Compliance Pressure From CBAM and ESG Rules

- 4.2.5 Industrial Park Decarbonization and ESG Digitization

- 4.2.6 AI-Driven Energy Optimization in High-Density Digital Infrastructure

- 4.3 Market Restraints

- 4.3.1 Talent Shortage in Cloud Security, Data Architecture, and Carbon Accounting

- 4.3.2 Data Localization and Compliance Complexity for Foreign Vendors

- 4.3.3 Power Grid and Infrastructure Constraints for Scalable Deployment

- 4.3.4 Budget Sensitivity Among SMEs and Mid-Market Buyers

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management and Accounting Software

- 5.4.2 ESG Reporting and Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy and Resource Optimization Software

- 5.5 By End User

- 5.5.1 Information Technology and Telecom

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare and Life Sciences

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Microsoft Corporation

- 6.4.3 IBM Corporation

- 6.4.4 SAP SE

- 6.4.5 Workiva Inc.

- 6.4.6 Watershed Technology, Inc.

- 6.4.7 Persefoni AI, Inc.

- 6.4.8 Sweep SAS

- 6.4.9 Normative AB

- 6.4.10 EcoVadis SAS

- 6.4.11 Diligent Corporation

- 6.4.12 Sphera Solutions, Inc.

- 6.4.13 Plan A

- 6.4.14 Greenly

- 6.4.15 Novisto Inc.

- 6.4.16 Cority Software Inc.

- 6.4.17 Enablon North America Corp.

- 6.4.18 Siemens AG

- 6.4.19 Honeywell International Inc.

- 6.4.20 Johnson Controls International plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment