|

시장보고서

상품코드

2073271

미국의 그린 IT 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

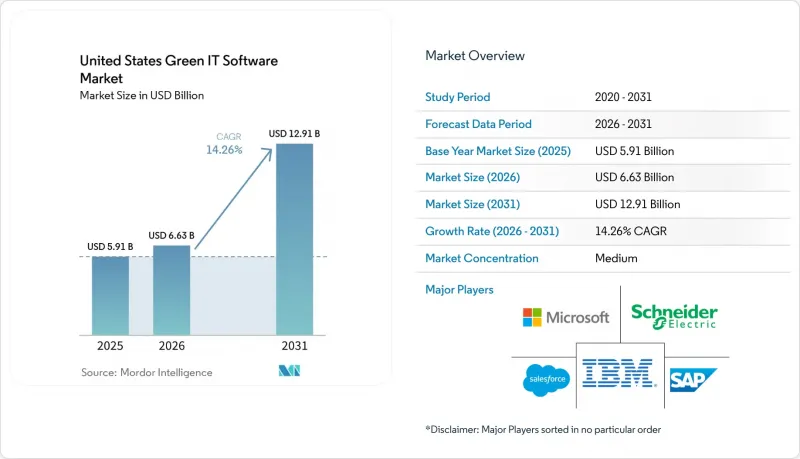

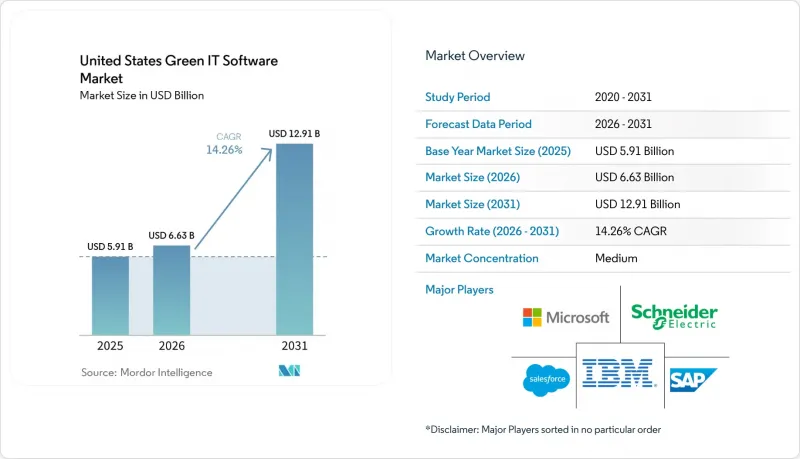

Mordor Intelligence에 의하면, 미국의 그린 IT 소프트웨어 시장 규모는 2025년 59억 1,000만 달러로 평가되었습니다. 2026년에는 66억 3,000만 달러로 확대되어 2031년까지 129억 1,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 14.26%로 성장할 전망입니다.

본 보고서는 제공 형태(소프트웨어 및 서비스), 도입 형태(클라우드 기반 등), 솔루션 유형(탄소 관리·산정 소프트웨어 등), 조직 규모(대기업 및 중소기업), 최종 사용자 산업 분야(정보기술·통신, 제조업 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 그린 IT 소프트웨어 시장 동향 및 인사이트

스코프 1부터 스코프 3에 이르는 보고 자동화에 대한 규제적 압력

캘리포니아주는 미국의 그린 IT 소프트웨어 시장에서 기업의 구매를 촉진하는 가장 뚜렷한 단기적 요인으로 작용하고 있습니다. 이는 캘리포니아주 대기자원국(CARB)이 2026년 2월 26일에 SB 253에 관한 첫 번째 시행 규칙을 채택하고, 해당 주에서 사업을 영위하는 대상 기업에 대해 스코프 1 및 스코프 2 배출량에 대한 첫 번째 공시 기한을 2026년 8월 10일로 정했기 때문입니다. 이 법률의 적용 범위는 캘리포니아주에 본사를 둔 기업에만 국한되지 않습니다. 매출액 기준이 해당 주에서 사업을 영위하는 기업에 적용되므로, 대상 구매자층은 업종이나 사업 지역을 불문하고 확대되고 있습니다. 스코프 3 의무는 2027년부터 발효되므로, 공급업체의 데이터 시스템, 관리 체계 및 내부 심사 프로세스를 감사에 대응할 수 있는 수준으로 구축하고 테스트하는 데 시간이 소요되는 만큼, 많은 구매업체들이 2026년 중에 이미 움직이기 시작했습니다. 이러한 시점에 따라, 배출량 인벤토리, 공급업체로부터 제출된 데이터, 증거 추적 및 프레임워크 준수 결과를 단일 관리 환경에서 관리할 수 있는 소프트웨어에 대한 수요가 증가하고 있습니다. 2026년 5월 SEC가 기후 관련 공시 규정의 철회를 제안했음에도 불구하고, 투자자, 대출 기관, 고객, 이사회로부터 여전히 공시 요구를 받고 있는 대기업들 사이에서는 재현 가능한 보고 시스템에 대한 근본적인 필요성이 해소되지 않고 있습니다. 그 결과, 워크플로우를 일반적으로 인정받는 배출량 산정 관행 및 검증 요건에 부합하도록 조정한 공급업체들이 세를 넓혀가고 있습니다. 이는 구매자가 의무적 보고와 자발적 보고 모두에서 지속적으로 사용할 수 있는 도구를 원하기 때문입니다.

지속 가능한 인텔리전스의 지속적인 활용을 위한 엔터프라이즈 AI의 전환

AI 덕분에 미국의 그린 IT 소프트웨어 시장의 가치는 단순한 데이터 수집에서 벗어나, 지속가능성 정보를 지속적으로 모니터링하고 해석하며 정리할 수 있는 소프트웨어로 전환되고 있습니다. 세일즈포스는 2025년 6월, "Agentforce for Net Zero Cloud"를 출시했습니다. 이 제품에는 공시 컨텐츠 초안 작성, 스코프 1, 스코프 2, 스코프 3 인벤토리 모니터링, 그리고 보고 주기가 끝난 후가 아니라 진행 중에 문제를 파악할 수 있는 AI 에이전트가 탑재되어 있습니다. SAP는 2026년 5월, 자사의 지속가능성 AI 에이전트가 2026년 말까지 일반에 공개될 예정이며, 평균 배출 계수에서 나타나는 변동성을 해결하는 동시에 탈탄소화 시나리오 검토를 지원할 것이라고 발표했습니다. 이로 인해 구매자의 기대는 변화하고 있습니다. 지속가능성 팀은 더 이상 과거 데이터를 단순히 저장하기만 하는 소프트웨어를 원하지 않기 때문입니다. 그들이 원하는 것은 데이터 누락을 지적하고, 시나리오를 비교하며, 보고 기간을 단축하고, 연중 내내 사내 의사결정을 지원할 수 있는 시스템입니다. AI 기능과 거버넌스 관리, 추적성을 비롯해 재무 시스템 및 운영 시스템과의 통합을 결합할 수 있는 벤더가 경쟁 우위를 점하고 있습니다. 이러한 기능 덕분에 감사의 엄격성을 해치지 않으면서도 수작업의 부담을 줄일 수 있기 때문입니다.

기존 ERP 및 시설 관리 시스템과의 통합이 갖는 복잡성

미국의 그린 IT 소프트웨어 시장에서 통합은 여전히 가장 두드러진 운영상의 장벽으로 남아 있습니다. 그 이유는 핵심이 되는 지속가능성 데이터가 배출량 보고를 염두에 두고 설계되지 않은 구식 ERP, 조달, 시설 및 건물 관리 시스템 내에 여전히 존재하기 때문입니다. 많은 구매자들은 실질적인 탄소 배출량을 산출하거나 공개 가능한 기록을 작성하기 전에 여러 거래 시스템을 연동해야 하며, 이러한 작업이 도입 기간을 연장하고 총 비용을 증가시키는 요인이 되고 있습니다. Oracle은 2024년 9월, 기존의 ‘"Fusion Cloud Applications Suite"안에 "Oracle Fusion Cloud Sustainability"를 출시했습니다. 이는 이미 기업의 거래 데이터를 보유하고 있는 소프트웨어 환경 내에 데이터 수집 및 보고 기능을 통합함으로써, 이 과제를 직접 해결하는 것입니다. IBM의 “Envizi Supply Chain Intelligence” 또한, ERP 거래 데이터를 스코프 3 산정에 연동하고, 더 정확한 원본 데이터가 존재하는 경우에는 광범위한 평균값보다 공급업체별 데이터를 우선시함으로써 이 문제를 해결하고자 합니다. 이러한 개선에도 불구하고, 데이터 품질과 시스템 호환성은 도입 기업의 환경에 따라 여전히 크게 다르며, 그 결과 통합 작업의 부담이 도입 속도를 크게 저해하고 있습니다. 도입 기업들은 도입 주기를 단축하고 외부 데이터와의 교환을 줄이기를 원하기 때문에 이러한 제약 조건은 ERP 계층을 관리하는 벤더나 강력한 기성 커넥터를 보유한 벤더에게 지속적인 우위를 가져다줍니다.

부문별 분석

이 서비스 분야는 2031년까지 연평균 성장률(CAGR) 19.26%를 나타낼 것으로 예측되며, 미국의 그린 IT 소프트웨어 시장 내 이 부문에서 가장 빠르게 성장하고 있는 분야입니다. 이러한 성장은 공시 의무가 더욱 상세해짐에 따라 도입 지원, 데이터 아키텍처 구축, 보고서 설계 및 변경 관리에 대한 수요가 증가하고 있음을 반영합니다. 많은 대형 구매 기업들은 소프트웨어를 대규모로 운영할 수 있게 되기 전까지, 배출량 워크플로우를 ERP, 조달 및 시설 데이터와 연동하기 위해 여전히 외부 지원이 필요합니다. 또한, 공급업체 데이터 프로그램, 보증 준비 및 내부 거버넌스 프로세스의 경우, 초기 도입 후에도 지속적인 지원이 필요한 경우가 많기 때문에 서비스 부문의 중요성은 여전히 높습니다. 한편, 2025년에는 소프트웨어가 매출의 46.41%를 차지했으며, 라이선스 기반 플랫폼이 여전히 기업이 지속가능성 데이터 및 보고 프로그램을 관리하는 데 있어 기반이 되고 있음을 보여주고 있습니다.

이 소프트웨어가 도입 기반의 핵심으로 자리 잡고 있는 이유는 제어 계층, 워크플로 로직, 증거 관리의 모든 요소가 컨설팅 업무가 아닌 제품 자체에 내장되어 있기 때문입니다. Workiva는 2025년 9월, 공시 문서 작성, 벤치마킹, 중요도 평가, 동종 업계 기업과의 비교, 규정 준수 워크플로우를 위한 AI 기반 자동화 기능을 갖춘 ‘"Intelligent Finance"“GRC”‘지속가능성’을 발표했습니다. 이는 서비스에 대한 수요가 여전히 견조한 가운데, 공급업체들이 소프트웨어의 가치를 어떻게 확대해 나가고 있는지를 보여줍니다. 자동화가 진행됨에 따라, 서비스에 대한 지출은 반복적인 업무에서 거버넌스 구축, 탈탄소화 계획, 보증 대응 준비와 같은 부가가치가 높은 분야로 전환될 가능성이 있습니다. 이러한 경향은 소프트웨어가 여전히 주요 수익원으로 남아 있는 가운데, 서비스가 급속히 성장하고 있는 이유를 설명하는 요인 중 하나입니다. 따라서 미국의 그린 IT 소프트웨어 업계는 순수한 라이선스만 제공하는 구조가 아니라, 소프트웨어와 제공 서비스를 결합한 모델로 진화하고 있습니다.

2025년에는 클라우드 기반 도입이 매출의 63.94%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 16.12%로 성장할 것으로 전망되어, 미국의 그린 IT 소프트웨어 시장에서 가장 규모가 크고 가장 빠르게 성장하는 도입 모델로 자리매김하고 있습니다. 이러한 이중적 위상은 구매자의 선호도가 초기 전환 단계를 거치지 않고, 클라우드 네이티브 지속가능성 아키텍처로 집중되고 있음을 보여줍니다. 대기업에서는 사업 부문, 지역, 보고 체계를 아우르는 지속적인 조율이 필요하지만, 클라우드 환경은 고립된 On-Premise 시스템보다 이를 실현하기 더 용이하게 해줍니다. 또한, 클라우드 도입은 AI를 활용한 지속가능성 기능이 이상 감지, 시나리오 분석 및 주기 내 검토를 위해 필요로 하는 ‘"상시 가동"의 데이터 피드도 지원합니다. 따라서 현재 클라우드 도입은 호스팅 선택과 마찬가지로 워크플로우 설계 및 시스템 간 상호 운용성과도 밀접하게 연관되어 있습니다.

IBM이 2026년 1월에 출시한 ‘“Envizi 배출량 계산”이 Excel 애드인은 사용자를 다른 작업 환경으로 강제로 전환시키는 것이 아니라, 클라우드 기반의 지속가능성 도구를 기존 사용자 워크플로에 통합하는 방법을 제시합니다. 또한, IBM은 2026년 2월, Envizi Sustainability Reporting Manager 내에 ESRS 옴니버스 프레임워크 구성을 출시했습니다. 이는 기준의 변화에 따라 업데이트가 가능한 관리형 클라우드 프레임워크의 장점을 반영한 것입니다. 데이터의 위치 및 인프라 제어가 여전히 중요하게 여겨지는 규제가 엄격한 환경에서는 On-Premise 구축도 여전히 그 역할을 하고 있습니다. 또한, 기업이 클라우드 분석을 도입하고자 하는 한편, 특정 직원 데이터, 재무 데이터 또는 업무 데이터 세트에 대해 보다 엄격한 통제가 필요한 경우에도 하이브리드 모델이 적합합니다. 규모 측면에서의 직접적인 연관성을 보여주는 한 가지 예로, 2025년 미국의 그린 IT 소프트웨어 시장 규모 중 클라우드 기반 솔루션이 63.94%를 차지했다는 점을 들 수 있습니다. 이는 전개에 대한 주도권이 이미 확장 가능한 호스팅형 모델에 있다는 사실을 뒷받침합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the united states green IT software market size is expected to increase from USD 5.91 billion in 2025 to USD 6.63 billion in 2026 and reach USD 12.91 billion by 2031, growing at a CAGR of 14.26% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, and More), Solution Type (Carbon Management and Accounting Software, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Information Technology and Telecommunications, Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Green IT Software Market Trends and Insights

Regulatory Pressure for Scope 1 To Scope 3 Reporting Automation

California has become the clearest near-term trigger for enterprise buying in the United States green IT software market because CARB adopted initial implementing regulations for SB 253 on February 26, 2026, and set August 10, 2026 as the first disclosure deadline for Scope 1 and Scope 2 emissions for covered companies doing business in the state. The law reaches beyond companies headquartered in California because the revenue threshold applies to firms that do business in the state, which widens the addressable buyer base across sectors and operating regions. Scope 3 obligations will activate from 2027, so many buyers are acting in 2026 because supplier data systems, controls, and internal review processes take time to build and test at audit-ready quality. This timing is lifting demand for software that can manage emissions inventories, supplier submissions, evidence trails, and framework-ready outputs in one controlled environment. The SEC's proposal to rescind its climate-related disclosure rules in May 2026 has not removed the underlying need for repeatable reporting systems among large enterprises that still face disclosure expectations from investors, lenders, customers, and boards. Vendors that align workflows with accepted emissions accounting practices and verification requirements are therefore gaining ground because buyers want tools that remain usable across both mandatory and voluntary reporting settings.

Enterprise AI Shift Toward Continuous Sustainability Intelligence

AI is shifting the value of the United States green IT software market from simple data collection toward software that can monitor, interpret, and organize sustainability information on a continuous basis. Salesforce launched Agentforce for Net Zero Cloud in June 2025 with AI agents that can draft disclosure content, monitor Scope 1, Scope 2, and Scope 3 inventories, and surface issues during the reporting cycle rather than after it closes. SAP stated in May 2026 that its sustainability AI agents will reach general availability by the end of 2026 and will support side-by-side decarbonization scenario work while addressing the variability found in average emissions factors. This changes buyer expectations because sustainability teams no longer want software that only stores past-period data. They want systems that can flag data gaps, compare scenarios, compress reporting timelines, and support internal decision-making during the year. The advantage is moving toward vendors that can combine AI functions with governance controls, traceability, and integration into finance and operating systems, because those features reduce manual effort without weakening audit discipline.

High Integration Complexity With Legacy ERP and Facility Systems

Integration remains the clearest operational barrier in the United States green IT software market because core sustainability data still originates inside older ERP, procurement, facility, and building systems that were not designed for emissions reporting. Many buyers must connect several transactional systems before they can produce usable carbon calculations or disclosure-ready records, and that work can stretch implementations and raise total cost. Oracle launched Oracle Fusion Cloud Sustainability in September 2024 inside its existing Fusion Cloud Applications Suite, which directly addresses this issue by embedding data capture and reporting functions within software environments that already hold enterprise transactions. IBM's Envizi Supply Chain Intelligence also targets this problem by connecting ERP transactions to Scope 3 calculations and by prioritizing supplier-specific data over broad averages where better source data exists. Even with these improvements, data quality and system compatibility still vary widely across buyer environments, which means integration effort remains a real brake on adoption speed. This restraint gives a durable advantage to vendors that control the ERP layer or have strong pre-built connectors, because buyers want shorter implementation cycles and fewer external data handoffs.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Native Carbon and Energy Optimization Adoption in Data Center Workloads

- Procurement Requirements Linking Software Selection to Verified ESG Data

- Weak Supplier Data Quality Slowing Scope 3 Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are projected to grow at a 19.26% CAGR through 2031, which makes them the fastest-expanding part of this segmentation in the United States green IT software market. That growth reflects the need for implementation support, data architecture work, reporting design, and change management as disclosure obligations become more detailed. Many large buyers still need outside help to connect emissions workflows with ERP, procurement, and facility data before the software can operate at scale. Services also remain relevant because supplier-data programs, assurance preparation, and internal governance processes often require sustained support after initial implementation. At the same time, software held 46.41% of revenue in 2025, which shows that licensed platforms still anchor how enterprises govern sustainability data and reporting programs.

Software remains the installed-base core because the control layer, workflow logic, and evidence management all sit inside the product rather than inside a consulting engagement. Workiva introduced Intelligent Finance, GRC, and Sustainability in September 2025 with AI-enabled automation for disclosure drafting, benchmarking, materiality work, peer comparison, and compliance workflows, which shows how vendors are expanding software value even as services demand stays strong. As automation improves, service spend is likely to shift away from repetitive assembly work and toward higher-value areas such as governance setup, decarbonization planning, and assurance readiness. That pattern helps explain why services are growing quickly without displacing software as the larger revenue base. The United States green IT software industry is therefore evolving toward combined software and delivery models rather than a pure license-only structure.

Cloud-based deployment accounted for 63.94% of revenue in 2025 and is projected to grow at a 16.12% CAGR through 2031, which leaves it as both the largest and fastest-growing deployment model in the United States green IT software market. This dual position shows that buyer preference is consolidating around cloud-native sustainability architecture rather than moving through an early transition stage. Large enterprises need continuous synchronization across business units, geographies, and reporting frameworks, and cloud environments make that easier than isolated on-premise systems. Cloud deployment also supports the always-on data feeds that AI-enabled sustainability functions require for anomaly detection, scenario work, and in-cycle review. For that reason, cloud adoption is now tied as much to workflow design and system interoperability as it is to hosting choice.

IBM's January 2026 Excel add-in for Envizi Emissions Calculations shows how cloud-based sustainability tools can be inserted into established user workflows instead of forcing users into a separate operating environment. IBM also released ESRS Omnibus framework configurations in February 2026 inside Envizi Sustainability Reporting Manager, which reflects the advantage of managed cloud frameworks that can be updated as standards evolve. On-premise deployment still has a role in more regulated settings where data residency and infrastructure control remain important. Hybrid models are also relevant where companies want cloud analytics but need tighter control over selected employee, financial, or operational datasets. One sentence with direct scale relevance is that cloud-based deployment held 63.94% of the United States green IT software market size in 2025, which confirms that deployment leadership already sits with scalable hosted models.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Industry

- IT and Telecommunications

- Manufacturing

- Banking, Financial Services, and Insurance (BFSI)

- Government and Public Sector

- Energy and Utilities

- Healthcare and Life Sciences

- Retail and E-Commerce

- Construction and Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- Salesforce, Inc.

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Schneider Electric SE

- Oracle Corporation

- Workiva Inc.

- Diligent Corp.

- Wolters Kluwer N.V.

- Persefoni AI, Inc.

- Watershed Technologies, Inc.

- EcoVadis SAS

- Intelex Technologies ULC

- Sphera Solutions, Inc.

- Benchmark Gensuite LLC

- FigBytes Inc.

- Measurabl, Inc.

- Cority Software Inc.

- Dakota Software Corporation

- EnergyCAP, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Pressure for Scope 1 to Scope 3 Reporting Automation

- 4.2.2 Cloud Native Carbon and Energy Optimization Adoption in Data Center Workloads

- 4.2.3 Enterprise AI Shift Toward Continuous Sustainability Intelligence

- 4.2.4 Procurement Requirements Linking Software Selection to Verified ESG Data

- 4.2.5 Utility Price Volatility Increasing Demand for Consumption Optimization

- 4.2.6 Fragmented Multi-Framework Reporting Burden Across Public and Private Firms

- 4.3 Market Restraints

- 4.3.1 High Integration Complexity With Legacy ERP and Facility Systems

- 4.3.2 Weak Supplier Data Quality Slowing Scope 3 Automation

- 4.3.3 Cybersecurity and Data Residency Concerns for ESG Data Platforms

- 4.3.4 Budget Sensitivity Among Mid-Market Buyers Despite Compliance Need

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Solution Type

- 5.3.1 Carbon Management and Accounting Software

- 5.3.2 ESG Reporting and Compliance Software

- 5.3.3 Sustainability Data Management Platforms

- 5.3.4 Decarbonization Planning Software

- 5.3.5 Energy and Resource Optimization Software

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 Manufacturing

- 5.5.3 Banking, Financial Services, and Insurance (BFSI)

- 5.5.4 Government and Public Sector

- 5.5.5 Energy and Utilities

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Retail and E-Commerce

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Salesforce, Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 SAP SE

- 6.4.5 Schneider Electric SE

- 6.4.6 Oracle Corporation

- 6.4.7 Workiva Inc.

- 6.4.8 Diligent Corp.

- 6.4.9 Wolters Kluwer N.V.

- 6.4.10 Persefoni AI, Inc.

- 6.4.11 Watershed Technologies, Inc.

- 6.4.12 EcoVadis SAS

- 6.4.13 Intelex Technologies ULC

- 6.4.14 Sphera Solutions, Inc.

- 6.4.15 Benchmark Gensuite LLC

- 6.4.16 FigBytes Inc.

- 6.4.17 Measurabl, Inc.

- 6.4.18 Cority Software Inc.

- 6.4.19 Dakota Software Corporation

- 6.4.20 EnergyCAP, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Assessment