|

시장보고서

상품코드

2073231

유럽의 디지털 워크플레이스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

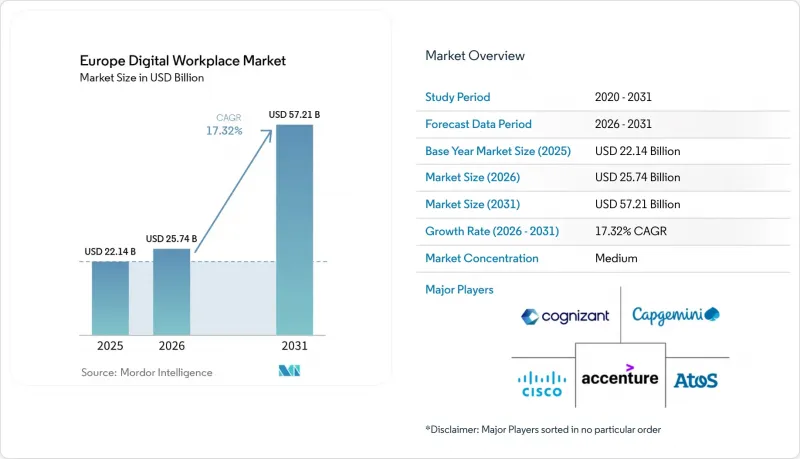

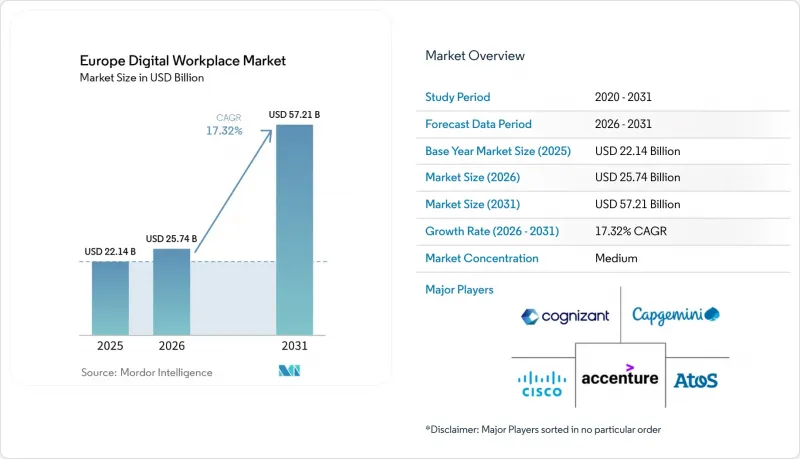

Mordor Intelligence에 의하면, 유럽의 디지털 워크플레이스 시장 규모는 2025년에 221억 4,000만 달러로 평가되었습니다. 2026년에 257억 4,000만 달러에 달하고, 2031년까지 572억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 17.32%로 성장할 전망입니다.

본 보고서는 구성 요소(솔루션 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 조직 규모(대기업 및 중소기업), 최종 사용자 산업 분야(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 의료, 제조, 정부·공공 부문, 교육 등) 및 지역별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 디지털 워크플레이스 시장 동향 및 인사이트

하이브리드 및 원격 근무 모델의 지속적인 도입

하이브리드 근무 방식이 현재 많은 유럽 고용주들의 업무 운영, 팀 협업, 인재 관리 방식에 정착함에 따라, 유럽의 디지털 워크플레이스 시장은 단기적인 사업 지속을 위한 지출이라기보다는 장기적인 업무 환경 재설계와 점점 더 밀접하게 연결되고 있습니다. 이러한 변화로 인해 재택, 사무실, 모바일 환경을 불문하고 일관된 직원 경험을 유지하기 위한 클라우드 협업, 가상 데스크톱 접속, 엔드포인트 제어 및 워크플로우 도구에 대한 수요가 확대되고 있습니다. 또한, 기업의 구매 행동도 변화하고 있습니다. 기업들은 더 이상 단순히 커뮤니케이션 기능만을 요구하지 않고, 분산된 팀 전체에 걸친 액세스 거버넌스, 기기 가시성, 그리고 지원의 질을 더욱 중요하게 여기고 있기 때문입니다. 하이브리드 근무 방식이 정착됨에 따라, 많은 조직은 여러 도구가 뒤죽박죽으로 혼재되어 업무상의 마찰을 야기하고, 정책 이행의 철저함을 약화시키며, 지원 비용을 증가시키고 있다는 사실을 깨닫기 시작했으며, 이는 플랫폼 통합에 대한 새로운 수요를 촉진하고 있습니다. 이러한 경향은 유럽의 디지털 워크플레이스 시장에서 지출이 독립된 단일 제품이 아닌, 보다 광범위한 워크플레이스 제품군으로 이동하고 있는 이유를 설명하는 요인 중 하나입니다. 하이브리드 근무 방식이 일반적인 업무 관행의 일부로 자리 잡을수록, 보안, 모니터링, 사용 편의성을 저해하지 않으면서 유연성을 지원할 수 있는 통합형 디지털 워크플레이스 플랫폼의 필요성은 더욱 커집니다.

기업들의 직원 경험 플랫폼 및 DEX 분석으로의 전환

유럽의 디지털 워크플레이스 시장은 고용주들이 업무 환경 기술의 관리 및 활용을 용이하게 하려는 가운데, 기업들이 직원 경험 플랫폼과 디지털 직원 경험 측정에 더욱 주력하고 있는 점도 성장에 힘을 실어주고 있습니다. 조직은 문제가 발생한 후에야 비로소 IT 팀이 대응하는 사후 대응형 서비스 모델에서 벗어나, 엔드포인트, 워크플로우, 지원 신호를 지속적으로 모니터링하는 환경을 구축해 나가고 있습니다. 이러한 변화가 중요한 이유는 열악한 사용자 경험이 더 이상 IT 부서의 만족도에만 영향을 미치는 것이 아니라, 부서 간 생산성, 인재 유지율, 도구 도입률에도 영향을 미치게 되었기 때문입니다. DEX 플랫폼의 중요성이 커지고 있는 이유는 워크플로우의 병목 현상, 용도의 과도한 사용, 엔드포인트 성능 저하, 지원 미비 등의 문제를 이러한 문제가 더 큰 운영상의 문제로 발전하기 전에 파악하는 데 도움이 되기 때문입니다. 상업적인 영향도 마찬가지로 중요합니다. 왜냐하면, 충분히 활용되지 않는 라이선스나 중복된 도구를 파악할 수 있는 구매자는 벤더를 통합하고, 측정 가능한 성과를 가져다주는 보다 광범위한 제품군에 예산을 재투자하는 경향이 강해지기 때문입니다. 이에 따라 유럽의 디지털 워크플레이스 시장은 분석, 자동화, 서비스 가시성을 개별 레이어로 제공하는 것이 아니라, 이를 통합한 플랫폼으로 나아가고 있습니다.

레거시 용도의 난립과 통합의 복잡성

레거시 용도의 확산은 유럽의 디지털 워크플레이스 시장에서 여전히 가장 뿌리 깊은 운영상의 장벽으로 남아 있습니다. 그 이유는 많은 기업이 단일한 현대적인 직원 환경으로 기능하도록 설계되지 않은 대규모이며 이질적인 소프트웨어 자산을 여전히 관리하고 있기 때문입니다. 이 문제는 단순히 오래된 소프트웨어에 그치지 않고, 상호 연동되지 않는 데이터 모델, 중복된 협업 계층, 파편화된 ID 구조 등도 포함되어 있어, 계약 체결 후의 변화를 지연시키고 있습니다. 조직이 이러한 환경의 현대화를 시도하면 통합 일정이 지연되기 쉬워져, 사용자에게 서비스를 제공하는 시기가 늦어지고, 서비스 비용이 증가하며, 여러 거점이나 부서를 아우르는 지원의 일관성이 훼손됩니다. 이러한 지연은 또 다른 문제를 야기합니다. 즉, 공식적인 전환 작업이 아직 진행 중인 단계에서 사업 부서가 비공식적인 도구를 채택하는 경우가 많아, 다음 통합 단계의 복잡성을 더욱 가중시키게 되는 것입니다. 그 결과, 업무 환경 혁신의 진정한 비용은 대상 플랫폼 자체보다, 레거시 워크플로우, 용도, 데이터 구조를 실용적인 통합체로 만들기 위해 필요한 노력에 따라 좌우되는 경우가 많습니다. 이러한 제약은 엄격한 규제 하에서 방대한 업무를 수행하는 기업들, 특히 업무에 지장을 주지 않으면서도 현대화를 추구하는 유럽의 디지털 워크플레이스 시장에서 특히 중요한 의미를 지닙니다.

부문별 분석

2025년, 솔루션 부문은 전체 시장의 64.58%를 차지하며, 소프트웨어 플랫폼이 유럽의 디지털 워크플레이스 시장 전체에서 여전히 주요 지출 분야임을 보여주었습니다. 이 비율은 통합 커뮤니케이션 및 협업, 통합 엔드포인트 관리, 워크플로 자동화, 지식 관리, 가상 데스크톱 인프라, 그리고 디지털 직원 경험 도구에 대한 지속적인 수요를 반영하고 있습니다. 구매 기업들은 여전히 워크플레이스 스택의 기능 계층을 구축 중이기 때문에 많은 계약에서 소프트웨어에 대한 투자가 제공 및 지원에 대한 투자보다 더 많이 이루어지고 있습니다. 이러한 경향은 장기적인 서비스 체계가 완전히 정착되기 전에, 많은 기업이 플랫폼 차원에서 어떤 업무 공간 기능을 표준화해야 할지 아직 정의하는 단계에 있음을 시사합니다. 단기적으로는 유럽의 디지털 워크플레이스 시장에서 솔루션 분야가 커뮤니케이션, 워크플로우, 지원, 규정 준수에 이르는 광범위한 통합을 요구하는 고용주들로부터 계속해서 혜택을 받을 것으로 보입니다.

서비스는 직접적인 수익 분배 측면에서는 솔루션에 이어 두 번째로 중요한 위치를 차지하고 있지만, 여전히 중요한 역할을 수행하고 있습니다. 왜냐하면 많은 워크플레이스 프로그램에서는 소프트웨어를 실제 비즈니스 환경에서 운영하기 위해 통합, 마이그레이션, 운영 관리, 거버넌스에 대한 지원이 필요하기 때문입니다. 환경이 점점 더 복잡해짐에 따라, 서비스 제공업체는 단순히 라이선스를 배포하는 것뿐만 아니라, 워크플레이스 제품군을 보안 제어, ID 관리 시스템, 레거시 용도과 연동해야 하는 경우가 늘어나고 있습니다. 이에 따라, 특히 고객이 업계 고유의 도입, 주권형 호스팅 설계, 혹은 도입 후 안정적인 운영 지원을 필요로 하는 경우, 서비스 계층은 보다 전략적인 역할을 담당하게 됩니다. 따라서 소프트웨어의 강점과 서비스의 심도 있는 내용이 서로를 보완하는 경향이 강해지고 있기 때문에 유럽의 디지털 워크플레이스 업계는 단순한 제품 중심의 모델로 전환되고 있는 것은 아닙니다. 장기적으로 볼 때, 유럽의 디지털 워크플레이스 시장에서 가장 탄탄한 입지를 확보할 벤더는 핵심 워크플레이스 소프트웨어와 도입 역량, 거버넌스 지원, 라이프사이클 관리를 하나의 통합된 솔루션으로 패키지화할 수 있는 기업이 될 가능성이 높습니다.

클라우드는 2031년까지 연평균 성장률(CAGR) 19.78%를 나타낼 것으로 예측되며, 유럽의 디지털 워크플레이스 시장에서 가장 빠르게 확대되고 있는 도입 형태입니다. 이는 자본 집약적인 On-Premise 환경에서 분산된 전 직원이 더 신속하게 업데이트하고 더 일관성 있게 관리할 수 있는 플랫폼으로의 광범위한 전환이 진행되고 있음을 반영합니다. 또한 기업들은 클라우드를 활용하여 도입 주기를 단축하고, 엔드포인트에 대한 가시성을 높이며, 사무실, 재택, 모바일 등 다양한 근무 환경에서 정책 적용을 일원화하고 있습니다. 많은 구매자에게 있어 클라우드 도입은 이제 규제 대응 계획과 함께 중요한 과제가 되고 있습니다. 이는 데이터 저장 위치, 감사 가능성, 서비스의 내결함성이 인프라의 유연성과 마찬가지로 중요하게 여겨지기 때문입니다. 이러한 요인들로 인해 유럽의 디지털 워크플레이스 시장에서 클라우드는 새로운 업무 환경을 구축하거나 대규모 개편 주기를 진행할 때 주요한 선택지로 자리 잡고 있습니다.

2025년 2월, 마이크로소프트가 'EU 데이터 경계'이를 완성함으로써, 마이크로소프트의 생산성 도구 및 클라우드 환경에 의존하는 규제 대상 고용주들에게 전환의 근거가 더욱 확고해졌습니다. 이는 해당 고객들이 주요 워크플레이스 워크로드에 대해 지역별 처리 경로를 보다 명확히 파악하게 되었기 때문입니다. On-Premise 구축은 국방, 중요 인프라 및 일부 금융 서비스 업무 등 엄격하게 관리되는 환경에서 여전히 그 가치를 인정받고 있습니다. 이러한 환경에서는 격리가 조달 요건으로 남아 있기 때문입니다. 그렇긴 하지만, 그 중간 영역은 특정 워크로드에 대한 로컬 제어와 협업, 분석, 서비스 관리를 위한 클라우드의 확장성을 결합한 하이브리드 구조로 점점 더 전환되고 있습니다. 이로 인해 도입 선택은 단순한 양자택일이 아니라, 규정 준수를 고려한 아키텍처 설계의 과제로 대두되고 있습니다. 이러한 추세가 지속됨에 따라, 주권형 하이브리드 모델을 지원할 수 있는 공급업체는 유럽의 디지털 워크플레이스 시장 전체에서 신규 계약액에서 더 큰 점유율을 확보할 가능성이 높을 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the europe digital workplace market size is projected to be USD 22.14 billion in 2025, USD 25.74 billion in 2026, and reach USD 57.21 billion by 2031, growing at a CAGR of 17.32% from 2026 to 2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Manufacturing, Government and Public Sector, Education, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Europe Digital Workplace Market Trends and Insights

Sustained Adoption of Hybrid and Remote Work Models

Hybrid work is now embedded in how many European employers organize operations, team collaboration, and talent management, so the Europe digital workplace market is increasingly tied to long-term workplace redesign rather than short-term continuity spending. That shift is expanding demand for cloud collaboration, virtual desktop access, endpoint control, and workflow tools that keep employee experience consistent across home, office, and mobile environments. It also changes buying behavior, because companies no longer look only for communication features and now place greater weight on access governance, device visibility, and support quality across distributed teams. As hybrid work matures, many organizations are discovering that a patchwork of tools creates operational friction, weakens policy enforcement, and raises support costs, which is pushing fresh demand for platform consolidation. This pattern helps explain why spending is moving toward broader workplace suites instead of isolated point products in the Europe digital workplace market. The longer hybrid work remains part of normal operating practice, the stronger the case becomes for integrated digital workplace platforms that can support flexibility without losing security, oversight, or usability.

Enterprise Shift to Employee Experience Platforms and DEX Analytics

The Europe digital workplace market is also being driven by a stronger enterprise focus on employee experience platforms and digital employee experience measurement, as employers seek to make workplace technology easier to manage and use. Organizations are moving away from reactive service models in which IT teams respond only after issues arise and instead building environments where endpoints, workflows, and support signals are monitored continuously. That shift matters because poor user experience now affects not only IT satisfaction but also productivity, retention, and tool adoption across departments. DEX platforms are gaining relevance because they help companies identify workflow bottlenecks, application fatigue, poor endpoint performance, and support gaps before those issues grow into larger operational problems. The commercial impact is equally important because buyers who can see underused licenses or overlapping tools are more likely to consolidate vendors and reinvest budgets into broader suites with measurable results. This is pushing the European digital workplace market toward platforms that combine analytics, automation, and service visibility rather than offering those functions as separate layers.

Legacy Application Sprawl and Integration Complexity

Legacy application sprawl remains the most persistent operating barrier in the Europe digital workplace market, because many enterprises still manage large, uneven software estates that were not built to work as one modern employee environment. The problem runs beyond old software alone, since it also includes disconnected data models, duplicated collaboration layers, and fragmented identity structures that slow transformation after contracts are signed. When organizations try to modernize these environments, integration timelines often stretch, delaying user rollouts, increasing service costs, and weakening support consistency across locations and departments. That delay also creates a second problem: business units often adopt unofficial tools while formal migration work is still underway, adding more complexity to the next phase of consolidation. As a result, the true cost of workplace transformation is often shaped less by the target platform itself and more by the effort required to connect legacy workflows, applications, and data structures into a usable whole. This restraint is especially important in the European digital workplace market, where enterprise buyers want modernization without disrupting tightly regulated, high-volume operations.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Migration of Workplace Applications and End-User Computing

- GDPR, Data Sovereignty, and Security by Design Requirements

- Data Residency Constraints Across Cross-Border Workflows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions retained 64.58% of the component segment in 2025, which shows that software platforms remained the main spending center across the Europe digital workplace market. This weight reflects continued demand for unified communication and collaboration, unified endpoint management, workflow automation, knowledge management, virtual desktop infrastructure, and digital employee experience tools. Buyers are still building out the functional layer of the workplace stack, so software receives more direct investment than delivery support in many contracts. That pattern also suggests that many enterprises are still defining which workplace capabilities they want to standardize at the platform level before long-term service structures fully settle. In the near term, the solutions side of the Europe digital workplace market should continue to benefit from employers seeking broader orchestration across communication, workflow, support, and compliance.

Services remain important even though they sit behind solutions in terms of direct revenue share, because many workplace programs depend on integration, migration, managed operations, and governance support to turn software into operational business environments. As estates grow more complex, service providers are increasingly asked to connect workplace suites with security controls, identity systems, and legacy applications rather than simply deploy licenses. This gives the services layer a more strategic role, especially where clients need sector-specific implementation, sovereign hosting design, or steady operational support after rollout. The Europe digital workplace industry is therefore not moving toward a simple product-only model, because software strength and service depth increasingly reinforce each other. Over time, the most resilient vendors in the Europe digital workplace market are likely to be those that can package core workplace software with implementation skill, governance support, and lifecycle management under one coordinated offer.

Cloud is projected to grow at a 19.78% CAGR through 2031, making it the fastest-moving deployment mode within the Europe digital workplace market. This reflects a broad shift away from capital-intensive on-premises environments toward platforms that can be updated more quickly and managed more consistently across dispersed workforces. Enterprises are also using cloud to shorten deployment cycles, improve endpoint visibility, and simplify policy delivery across office, home, and mobile work settings. For many buyers, cloud adoption now sits alongside regulatory planning, because data location, auditability, and service resilience matter as much as infrastructure flexibility. These factors have made the cloud the leading path for new workplace builds and for major refresh cycles in the Europe digital workplace market.

Microsoft's completion of the EU Data Boundary in February 2025 strengthened the migration case for regulated employers that rely on Microsoft productivity and cloud environments, because those customers gained a clearer regional processing path for core workplace workloads. On-premises deployments still hold value in tightly controlled settings such as defense, critical infrastructure, and some financial services operations, where isolation remains a procurement requirement. Even so, the middle ground is increasingly shifting toward hybrid structures that combine local control for selected workloads with cloud elasticity for collaboration, analytics, and service management. This makes deployment choice less of a binary decision and more of a compliance-informed architecture exercise. As that dynamic plays out, providers that can support sovereign hybrid models are likely to capture a larger share of incremental contract value across the Europe digital workplace market.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordics

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- Accenture plc

- Atos SE

- Capgemini SE

- Cisco Systems, Inc.

- Cognizant Technology Solutions Corporation

- Computacenter plc

- DXC Technology Company

- Fujitsu Limited

- Getronics Holding B.V.

- HCL Technologies Limited

- Hewlett Packard Enterprise Company

- IBM Corporation

- Infosys Limited

- Kyndryl Holdings, Inc.

- NTT DATA Group Corporation

- SAP SE

- ServiceNow, Inc.

- SoftwareOne Holding AG

- Tata Consultancy Services Limited

- Telefonica, S.A.

- Wipro Limited

- Zensar Technologies Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustained Adoption of Hybrid and Remote Work Models

- 4.2.2 Enterprise Shift to Employee Experience Platforms and DEX Analytics

- 4.2.3 Cloud Migration of Workplace Applications and End-User Computing

- 4.2.4 GDPR, Data Sovereignty, and Security By Design Requirements

- 4.2.5 EU AI Act and Governance-Ready Workplace Automation

- 4.2.6 Demand for Measurable Productivity, Sentiment, and Experience Telemetry

- 4.3 Market Restraints

- 4.3.1 Legacy Application Sprawl and Integration Complexity

- 4.3.2 Data Residency Constraints Across Cross-Border Workflows

- 4.3.3 High Total Cost of Transformation for Mid-Market Firms

- 4.3.4 User Fatigue From Tool Proliferation and Change Resistance

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Nordics

- 5.5.8 Russia

- 5.5.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Atos SE

- 6.4.3 Capgemini SE

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Cognizant Technology Solutions Corporation

- 6.4.6 Computacenter plc

- 6.4.7 DXC Technology Company

- 6.4.8 Fujitsu Limited

- 6.4.9 Getronics Holding B.V.

- 6.4.10 HCL Technologies Limited

- 6.4.11 Hewlett Packard Enterprise Company

- 6.4.12 IBM Corporation

- 6.4.13 Infosys Limited

- 6.4.14 Kyndryl Holdings, Inc.

- 6.4.15 NTT DATA Group Corporation

- 6.4.16 SAP SE

- 6.4.17 ServiceNow, Inc.

- 6.4.18 SoftwareOne Holding AG

- 6.4.19 Tata Consultancy Services Limited

- 6.4.20 Telefonica, S.A.

- 6.4.21 Wipro Limited

- 6.4.22 Zensar Technologies Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment