|

시장보고서

상품코드

2073266

남미의 디지털 워크플레이스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

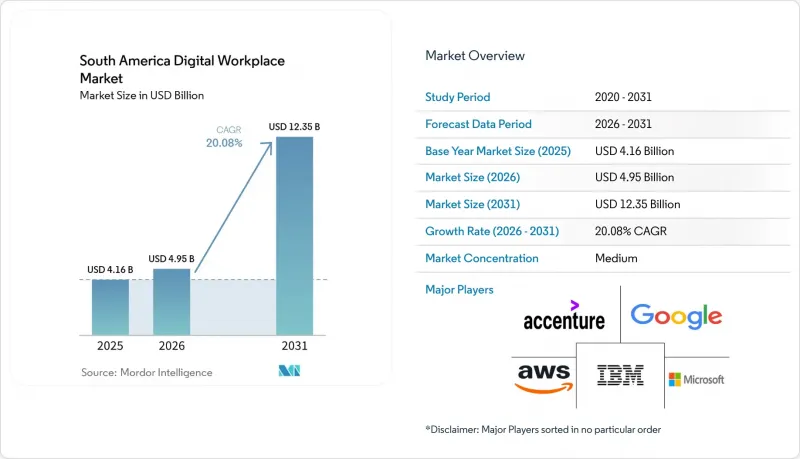

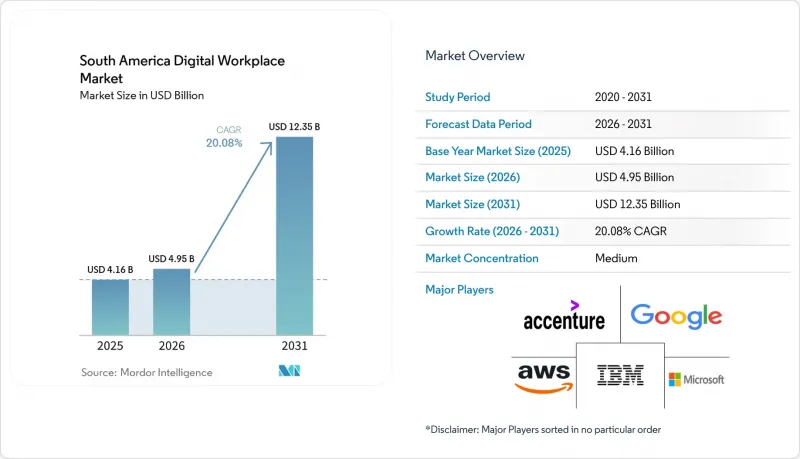

Mordor Intelligence에 의하면, 남미의 디지털 워크플레이스 시장 규모는 2025년에 41억 6,000만 달러로 평가되었습니다. 2026년 49억 5,000만 달러에서 2031년까지 123억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 20.08%를 나타낼 전망입니다.

본 보고서는 구성 요소(솔루션 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 조직 규모(대기업 및 중소기업), 최종 사용자 산업 분야(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 의료, 제조, 소매, 정부·공공 부문 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

남미의 디지털 워크플레이스 시장 동향 및 인사이트

기업 운영에서의 하이브리드 근무 방식 도입 확대

하이브리드 근무 방식은 이 지역의 많은 기업에서 일시적인 조치에서 보다 안정적인 운영 모델로 전환되고 있으며, 남미의 디지털 워크플레이스 시장은 일시적인 긴급 지출이라기보다는 일상적인 업무 흐름에 관한 의사결정과 밀접하게 연관되어 있습니다. 이러한 수요의 영향은 협업 소프트웨어에만 국한되지 않습니다. 이는 고용주가 자택, 지사, 본사 등 다양한 환경 간을 이동하는 직원에 대해 안전한 접근, 관리된 기기, ID 관리, 워크플로우 문서화 및 정책 추적을 필요로 하기 때문입니다. 또한 이 운영 모델은 커뮤니케이션, 파일 액세스, 승인 및 기본적인 직원 지원을 단일 시스템 내에서 통합하는 플랫폼의 중요성을 부각시키고 있으며, 이것이 남미의 디지털 워크플레이스 시장 전반에서 플랫폼 통합이 지속되고 있는 이유 중 하나입니다. 주요 경제권에서 시행되고 있는 공식적인 원격 근무 및 하이브리드 근무 규정 또한 고용주들로 하여금 팀 간 기록, 승인, 거버넌스를 일관되게 지원할 수 있는 시스템을 도입하도록 이끌고 있습니다. 이러한 요건은 특히 고용주가 분산된 직원, 기밀 데이터 및 정기적인 규정 준수 업무를 관리해야 하는 경우, 개별 도구보다 통합형 업무 공간 플랫폼의 가치를 더욱 부각시킵니다. 그 결과, 하이브리드 근무 방식은 남미의 디지털 워크플레이스 시장에서 사용자 수를 늘리고 있을 뿐만 아니라, 구매자들이 각 도입 사례에서 기대하는 기능의 범위도 넓혀가고 있습니다.

협업 및 가상 워크스페이스 스택의 클라우드 전환

협업, 스토리지, ID 관리, 보안 제어가 공유 클라우드 인프라에 배치됨에 따라 워크플레이스 플랫폼의 확장이 용이해지기 때문에 클라우드 전환은 남미의 디지털 워크플레이스 시장에서 여전히 주요 성장 요인으로 자리 잡고 있습니다. 마이크로소프트는 브라질의 클라우드 및 AI 인프라에 3년간 147억 레알(29억 달러)을 투자할 것이라고 발표했습니다. 이는 해당 지역의 기업 수요와 현지 서비스 제공 역량에 대한 장기적인 신뢰를 반영한 것입니다. 이러한 투자가 가져오는 실질적인 효과는 기업이 핵심 업무 공간 기능을 클라우드 환경으로 이전할 때 지연 시간, 내결함성, 데이터 근접성과 관련된 장벽이 줄어든다는 점입니다. 이러한 변화는 남미의 디지털 워크플레이스 시장에서 중요한데, 그 이유는 기반 인프라 문제가 해결되면 구매자들이 협업, 분석, 워크플로우, 직원용 서비스 도구를 동시에 개편하는 경우가 많아지기 때문입니다. 또한, 클라우드 전환은 벤더들의 폭넓은 시장 진입을 촉진합니다. 기업은 단일 On-Premise 아키텍처에만 의존하는 대신, 대규모 플랫폼 제품군과 전문 도구를 조합하여 활용할 수 있게 되기 때문입니다. 향후 몇 년 동안 이러한 추세에 따라, 특히 규제 대상 이용 사례에서 현지 인프라의 신뢰성이 높아지고 있는 국가들에서는 클라우드 중심의 계약이 남미의 디지털 워크플레이스 시장의 중심을 계속 차지할 것입니다.

레거시 애플리케이션 통합의 복잡성

레거시 용도의 통합은 남미의 디지털 워크플레이스 시장에서 여전히 주요 제약 요인 중 하나입니다. 많은 기업이 현대의 클라우드 워크플로우에 맞추어 구축되지 않은 구식 인사, 급여, 문서 관리 및 업무 시스템을 여전히 운영하고 있기 때문입니다. 기업이 새로운 협업 도구, 자동화 도구 또는 직원용 서비스 도구를 도입하고자 할 때, 새로운 플랫폼이 기존 데이터나 승인 절차와 연동되도록 하려면 미들웨어나 맞춤형 인터페이스, 혹은 단계적인 전환 계획이 필요한 경우가 많습니다. 이로 인해 도입이 지연되고 프로젝트 비용이 증가하며, 특히 워크플레이스 프로그램이 직원의 기밀 기록이나 규제 대상 프로세스와 관련된 경우, 구매자는 대규모 도입에 대해 더욱 신중해집니다. 이 문제는 오랜 기간에 걸쳐 여러 시스템이 중첩되어 온 대규모 조직에서 더욱 심각하며, 남미의 디지털 워크플레이스 시장에서 강력한 수요를 실제 도입으로 신속하게 연결하는 데 걸림돌이 되고 있습니다. 또한, 고객이 플랫폼의 가치를 최대한 활용할 수 있도록 하기 위해서는 공급업체가 데이터 매핑, 접근 제어, 프로세스 재설계를 해결해야 하므로, 지출은 장기적인 서비스 계약으로 전환되고 있습니다. 그 결과, 남미의 디지털 워크플레이스 시장은 여전히 강력한 성장세를 보이고 있지만, 통합의 복잡성으로 인해 많은 기업 프로젝트에서 도입 속도와 수익성 달성이 지연되고 있는 것이 현실입니다.

부문별 분석

2025년, 솔루션은 남미의 디지털 워크플레이스 시장의 64.93%를 차지했습니다. 이는 구매자들이 여전히 커뮤니케이션, 파일, 워크플로우 및 직원용 도구를 통합하는 핵심 소프트웨어 플랫폼을 가장 중요하게 여기고 있음을 보여줍니다. 또한 이 리드는 기업 고객들이 현재, 개별 로그인, 지원, 거버넌스 부담을 야기하는 분산된 포인트 도구보다는 소수의 전략적 제품군을 선호하는 경향을 반영하고 있습니다. 남미의 디지털 워크플레이스 시장에서 이러한 추세는 협업, 생산성, 분석, 자동화를 단일 상용 모델로 통합할 수 있는 공급업체들에게 유리하게 작용하고 있습니다. SAP는 2025년에 남미 의사결정권자의 55%가 AI 투자를 늘릴 계획이라고 보고했으며, 이는 AI 기능이 별도의 제품으로 판매되는 것이 아니라 일상 업무에 통합된 보다 종합적인 솔루션 제품군으로의 전환을 뒷받침하는 것입니다.

솔루션 시장은 2031년까지 연평균 성장률(CAGR) 20.48%로 확대될 것으로 예상되며, 이 부문은 남미의 디지털 워크플레이스 시장에서 신규 계약 활동의 중심이 될 것으로 보입니다. 서비스 점유율은 여전히 낮은 수준이지만, 워크플레이스 플랫폼이 더욱 지능화되고 상호 연결성이 강화됨에 따라 고객은 도입, 통합, 변경 관리 및 지속적인 지원이 필요하기 때문에 서비스의 중요성은 계속해서 높아지고 있습니다. Kyndryl사가 2026년 4월에 AI를 활용한 '직장을 위한 디지털 트윈'을 출시한 것은 서비스 지향 기업들이 노동력에 의존하는 제공 방식에서 벗어나, 보다 광범위한 플랫폼 모델의 일환으로 업무 환경의 모니터링, 예측, 운영 개선을 제공하고 있음을 보여줍니다. 이러한 변화는 대규모 계약이 소프트웨어 및 서비스 양쪽에 점점 더 의존하게 됨에 따라, 디지털 워크플레이스 산업이 더 이상 소프트웨어 및 서비스로 명확하게 구분되지 않는다는 점을 시사합니다. 장기적으로는 남미의 디지털 워크플레이스 시장에서 소프트웨어의 심도 있는 전문성과 워크플레이스 환경 전반에 걸친 신뢰할 수 있는 제공 체계, 거버넌스, 운영 지원을 모두 갖춘 벤더가 유력한 입지를 차지하게 될 것입니다.

2025년 기준으로 클라우드는 남미의 디지털 워크플레이스 시장의 58.32%를 차지했으며, 2031년까지 연평균 성장률(CAGR)이 20.64%에 달하고, 가장 빠르게 성장하고 있는 도입 형태이기도 합니다. 이러한 선도적인 위상은 완전히 로컬 환경에 수반되는 막대한 유지보수 부담 없이 분산된 팀, 모바일 사용자, 그리고 증가하는 데이터 수요에 더 쉽게 확장할 수 있는 플랫폼으로 지역 전체에 걸쳐 명확한 전환이 진행되고 있음을 반영합니다. 남미의 디지털 워크플레이스 시장에서 클라우드 도입은 현지 인프라 강화에 힘입어 계속해서 긍정적인 영향을 받고 있습니다. 이는 지연이나 지역적 제약에 대한 우려가 관리하기 쉬워짐에 따라, 구매자들이 기밀성이 높은 협업 및 워크플로 기능을 클라우드 플랫폼에 배치하는 것을 더욱 적극적으로 고려하게 되었기 때문입니다. 마이크로소프트가 브라질에 투자한 147억 레알(29억 달러)은 기업용 클라우드 및 AI 도입을 위한 기반 환경을 강화함으로써 이러한 변화를 뒷받침하고 있습니다.

일부 기업에서는 특정 워크로드를 사내 시스템이나 기밀 데이터의 관리 체계와 가까운 곳에 유지하기 위한 단계적인 전환 경로가 필요하기 때문에 하이브리드 배포는 여전히 남미의 디지털 워크플레이스 시장에서 중요한 위치를 차지하고 있습니다. 이는 특히 신속하게 전환할 수 없는 구형 용도를 운영 중인 조직, 업계 규정이나 사내 정책으로 인해 전환 기간 동안에는 여전히 혼합 아키텍처가 권장되는 경우에 해당합니다. On-Premise 배포의 상대적 비중은 점차 줄어들고 있지만, 일부 정부 기관, 중요 업무 및 디지털 현대화의 초기 단계에 있는 조직에서는 여전히 존재하고 있습니다. 콜롬비아는 해당 지역의 디지털 기업의 12.8%를 차지하고 있으며, 이 또한 클라우드 중심 수요를 뒷받침하고 있습니다. 많은 디지털 네이티브 기업들은 기존 기업에 비해 레거시 시스템으로 인한 마찰이 적고, 최신 협업 도구와 보안 도구를 조기에 도입하는 경향이 있기 때문입니다. 그 결과, 남미의 디지털 워크플레이스 시장 전체에서 클라우드는 여전히 주요 성장 동력으로 자리 잡고 있는 반면, 하이브리드 방식은 단번에가 아니라 단계적으로 현대화를 추진하는 고객들에게 실용적인 가교 역할을 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the south america digital workplace market size was valued at USD 4.16 billion in 2025 and estimated to grow from USD 4.95 billion in 2026 to reach USD 12.35 billion by 2031, at a CAGR of 20.08% during the forecast period (2026-2031).

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Manufacturing, Retail, Government and Public Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America Digital Workplace Market Trends and Insights

Rising Hybrid Work Adoption in Enterprise Operations

Hybrid work has moved from a temporary arrangement to a more stable operating model for many enterprises in the region, keeping the South America digital workplace market closely linked to everyday workflow decisions rather than one-time emergency spending. The demand effect extends beyond collaboration software alone, because employers need secure access, managed devices, identity controls, workflow documentation, and policy tracking for staff who move between home, branch, and central-office settings. This operating model also underscores the importance of platforms that connect communication, file access, approvals, and basic employee support within a single system, which helps explain the continued platform consolidation across the South America digital workplace market. Formal remote and hybrid work rules in major economies are also pushing employers toward systems that can consistently support records, approvals, and governance across teams. That requirement underscores the value of integrated workplace platforms over isolated tools, especially when employers must manage distributed staff, sensitive data, and recurring compliance tasks. As a result, hybrid work is not only expanding seat counts in the South America digital workplace market, but also widening the capabilities buyers expect from each deployment.

Cloud Migration of Collaboration and Virtual Workspace Stacks

Cloud migration remains a central growth force in the South America digital workplace market because workplace platforms are easier to scale when collaboration, storage, identity, and security controls sit on shared cloud infrastructure. Microsoft announced a BRL 14.7 billion (USD 2.9 billion) investment over 3 years in cloud and AI infrastructure in Brazil, reflecting long-term confidence in regional enterprise demand and local service capacity. The practical effect of investments like this is that enterprises face fewer barriers tied to latency, resilience, and data locality when moving core workplace functions into cloud environments. That shift matters in the South America digital workplace market because buyers often refresh collaboration, analytics, workflow, and employee service tools at the same time once the base infrastructure question becomes easier to solve. Cloud migration also supports broader vendor participation, as enterprises can mix large platform suites with specialized tools rather than relying on a single on-premises architecture. Over the next few years, this pattern should keep cloud-led contracts at the center of the South America digital workplace market, especially in countries where local infrastructure has become more credible for regulated use cases.

Legacy Application Integration Complexity

Legacy application integration remains one of the main restraints on the South America digital workplace market because many enterprises still run older HR, payroll, document, and line-of-business systems that were not built for modern cloud workflows. Even when companies want to deploy new collaboration, automation, or employee service tools, they often need middleware, custom interfaces, or phased migration plans before new platforms can work with existing data and approval flows. This slows implementation, raises project costs, and makes buyers more cautious about large-scale rollouts, especially when workplace programs touch sensitive employee records or regulated processes. The problem is more serious in large organizations where several systems have been layered over time, which limits how quickly the South America digital workplace market can convert strong demand into completed deployments. It also shifts spending toward longer service engagements, because vendors must solve data mapping, access control, and process redesign before the customer can use the full platform value. As a result, the South America digital workplace market continues to grow strongly, but integration complexity still delays adoption speed and margin realization across many enterprise projects.

Other drivers and restraints analyzed in the detailed report include:

- AI-Assisted Employee Experience and Workflow Orchestration

- Security-First Endpoint and Identity Management Prioritization

- Skills Shortage in Workplace Digitalization and Endpoint Security

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 64.93% of the South America digital workplace market in 2025, indicating that buyers still place the greatest weight on core software platforms that unify communication, files, workflows, and employee-facing tools. This lead also reflects the way enterprise customers now prefer fewer strategic suites rather than scattered point tools that create separate logins, support, and governance burdens. In the South America digital workplace market, this pattern supports vendors that can combine collaboration, productivity, analytics, and automation within a single commercial model. SAP reported in 2025 that 55% of South American decision-makers planned to increase AI investment, which supports the move toward richer solution suites where AI features are embedded into everyday work rather than sold as separate products.

Solutions are projected to expand at a 20.48% CAGR through 2031, which keeps this category at the center of new contract activity in the South America digital workplace market. Services remain smaller in share, but they continue to grow in importance as customers need implementation, integration, change management, and ongoing support as workplace platforms become more intelligent and connected. Kyndryl's April 2026 launch of its AI-powered Digital Twin for the Workplace shows how service-oriented firms are moving beyond labor-based delivery to offer workplace monitoring, prediction, and operational improvement as part of the wider platform model. That shift suggests the digital workplace industry is no longer splitting neatly between software and services, as large deals increasingly depend on both. Over time, the stronger vendors in the South America digital workplace market are likely to be those that can pair software depth with credible delivery, governance, and operational support across the full workplace environment.

Cloud held 58.32% of the South America digital workplace market share in 2025, and cloud is also the fastest-growing deployment mode with a 20.64% CAGR through 2031. This leadership reflects a clear regional shift toward platforms that can scale more easily across distributed teams, mobile users, and growing data needs without the heavier maintenance burden of fully local environments. The South America digital workplace market for cloud deployment continues to benefit from stronger local infrastructure, as buyers are more willing to place sensitive collaboration and workflow functions on cloud platforms when latency and locality concerns are easier to manage. Microsoft's BRL 14.7 billion (USD 2.9 billion) investment in Brazil supports that change by strengthening the underlying environment for enterprise cloud and AI adoption.

Hybrid deployment still holds an important place in the South America digital workplace market because some enterprises need a staged path that keeps selected workloads closer to internal systems or sensitive data controls. This is especially relevant where organizations run older applications that cannot be moved quickly, or where sector rules and internal policy still favor a mixed architecture during transition. On-premises deployment is losing relative weight, but it remains present in parts of government, critical operations, and organizations that are still early in digital modernization. Colombia's role as host to 12.8% of the region's digital firms also supports cloud-oriented demand, because many digital-native businesses adopt modern collaboration and security tools earlier and with less legacy friction than older enterprises. The result is that cloud remains the main growth engine across the South America digital workplace market, while hybrid serves as a practical bridge for customers modernizing in stages rather than in one step.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility and Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- Hybrid

- On-Premises

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

List of Companies Covered in this Report:

- Microsoft Corporation

- International Business Machines Corporation

- Accenture PLC

- Google LLC

- Amazon Web Services, Inc.

- Cisco Systems, Inc.

- Citrix Systems, Inc.

- Oracle Corporation

- SAP SE

- Hewlett Packard Enterprise Development LP

- DXC Technology Company

- Capgemini SE

- Tata Consultancy Services Limited

- Infosys Limited

- Wipro Limited

- Kyndryl Holdings, Inc.

- Unisys Corporation

- Atos SE

- Cognizant Technology Solutions Corporation

- Globant S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Hybrid Work Adoption in Enterprise Operations

- 4.2.2 Security-First Endpoint and Identity Management Prioritization

- 4.2.3 Cloud Migration of Collaboration and Virtual Workspace Stacks

- 4.2.4 Expansion of Managed Digital Workplace Outsourcing

- 4.2.5 Localization Pressure From Data Residency and Sovereignty Rules

- 4.2.6 AI-Assisted Employee Experience and Workflow Orchestration

- 4.3 Market Restraints

- 4.3.1 Legacy Application Integration Complexity

- 4.3.2 Skills Shortage in Workplace Digitalization and Endpoint Security

- 4.3.3 Fragmented Cross-Border Compliance Requirements

- 4.3.4 Limited Rural Connectivity and Uneven Network Quality

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility and Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 Hybrid

- 5.2.3 On-Premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Chile

- 5.5.4 Colombia

- 5.5.5 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 International Business Machines Corporation

- 6.4.3 Accenture PLC

- 6.4.4 Google LLC

- 6.4.5 Amazon Web Services, Inc.

- 6.4.6 Cisco Systems, Inc.

- 6.4.7 Citrix Systems, Inc.

- 6.4.8 Oracle Corporation

- 6.4.9 SAP SE

- 6.4.10 Hewlett Packard Enterprise Development LP

- 6.4.11 DXC Technology Company

- 6.4.12 Capgemini SE

- 6.4.13 Tata Consultancy Services Limited

- 6.4.14 Infosys Limited

- 6.4.15 Wipro Limited

- 6.4.16 Kyndryl Holdings, Inc.

- 6.4.17 Unisys Corporation

- 6.4.18 Atos SE

- 6.4.19 Cognizant Technology Solutions Corporation

- 6.4.20 Globant S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment