|

시장보고서

상품코드

2073262

디지털 워크플레이스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

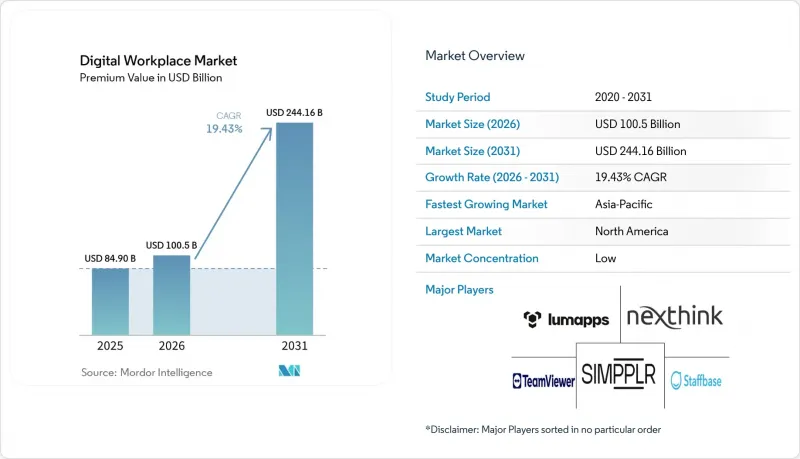

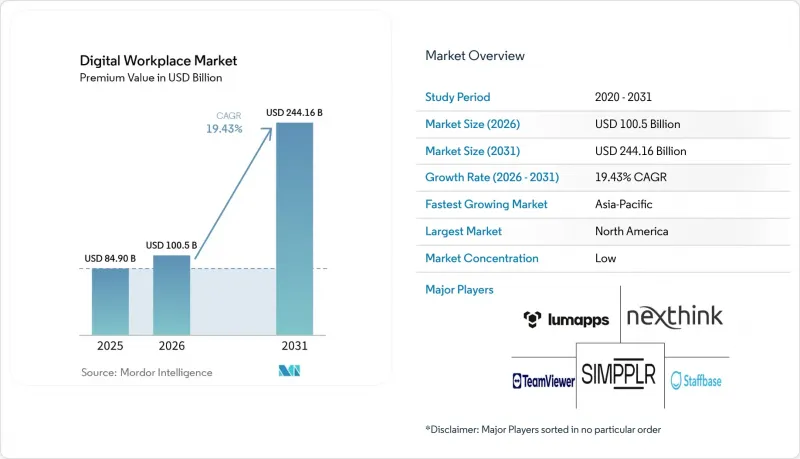

Mordor Intelligence에 의하면, 디지털 워크플레이스 시장 규모는 2025년에 849억 달러, 2026년에 1,005억 달러되어, 2031년까지 2,441억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 19.43%로 성장할 전망입니다.

본 보고서는 구성 요소(솔루션 및 서비스), 배포 방식(클라우드, On-Premise, 하이브리드), 조직 규모(대기업 및 중소기업), 최종 사용자 산업(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 의료, 제조, 소매, 정부·공공 부문, 교육 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 디지털 워크플레이스 시장 동향과 인사이트

AI를 활용한 협업과 워크플로우 자동화가 기업 내 도입을 주도하고 있습니다.

AI를 활용한 협업은 제한적인 시범 운영 단계에서 기업 내 광범위한 활용 단계로 전환되고 있으며, 이러한 변화가 현재 디지털 워크플레이스 시장에서 가장 강력한 수요 견인 요인으로 작용하고 있습니다. Microsoft 365 생태계 내의 활성 AI 에이전트 수는 2025년 3월부터 2026년 3월까지 전년 대비 15배 증가했으며, 대기업의 경우 18배 증가를 기록했습니다. 이는 기존 워크플레이스 플랫폼 내에서 도입이 얼마나 빠르게 확산되고 있는지를 보여줍니다. 또한 마이크로소프트의 조사에 따르면, 2026년 2월에 기록된 10만 건 이상의 Copilot 대화 중 49%가 분석, 문제 해결, 평가, 창의적 사고와 같은 인지적 업무를 지원하는 것으로 나타났습니다. 이는 AI가 단순한 초안 작성뿐만 아니라, 부가가치가 더 높은 업무에 활용되고 있음을 시사합니다. 이는 디지털 워크플레이스 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 구매자들은 협업, 문서, 워크플로 환경에 AI가 처음부터 통합된 플랫폼을 점점 더 많이 선택하고 있기 때문입니다. 이러한 경향은 인간과 AI의 팀워크를 로드맵의 핵심으로 삼고 있는 벤더의 경우, 전환 비용을 높이고 계약 갱신 가능성을 높여줍니다. 또한, 디지털 워크플레이스 시장이 보다 성숙한 도입 단계로 접어들면서, 단순히 제품의 폭이 넓은 것보다 기능의 깊이가 더욱 중요해지고 있습니다.

에이전트형 AI와 엔터프라이즈 검색 커넥터의 확대가 워크플레이스 아키텍처를 재정의하고 있습니다.

에이전트형 AI는 디지털 워크플레이스 시장의 역할을 단순한 생산성 향상 도구의 집합체에서 추론을 수행하고 정보를 검색하며 기업 시스템 전반에 걸쳐 업무를 수행할 수 있는 계층으로 확대되고 있습니다. 마이크로소프트는 2026년 6월 Work IQ API를 정식 출시하며, 에이전트가 컨텍스트에 접근하여 Microsoft 365의 데이터 및 용도 전반에서 작동할 수 있는 공유 인텔리전스 레이어를 구축했습니다. 2026년 1월에 출시된 Nexthink Spark는 IT 문제의 첫 대응 해결률 77%를 달성했으며, 레벨 1 문제를 2분 이내에 자율적으로 해결했습니다. 이는 에이전트 기반 모델이 디지털 워크플레이스 시장에서 서비스 활동의 상당 부분을 이미 처리할 수 있음을 입증하고 있습니다. 그 결과, 엔터프라이즈 검색은 더 이상 단순한 정보 검색 기능에 그치지 않고, 업무, 승인, 지원, 컨텐츠 처리 등의 실행 프로세스의 일부로 자리 잡고 있습니다. ERP, HR, ITSM, 커뮤니케이션 도구를 위한 강력한 커넥터 생태계를 갖추지 못한 벤더는 이 모델이 보급됨에 따라 핵심적인 입지를 유지하기 어려워질 것입니다. 독자적인 커넥터와 더욱 강력한 오케스트레이션 기능을 구축하는 벤더는 예측 기간 동안 디지털 워크플레이스 시장에서 더욱 확고한 입지를 다질 가능성이 높을 것으로 보입니다.

데이터 개인정보 보호, 사이버 보안, 규정 준수 관련 리스크가 조달 주기를 길게 만듭니다.

데이터 개인정보 보호와 사이버 보안은 디지털 워크플레이스 시장에서 여전히 가장 뿌리 깊은 마찰의 원인이 되고 있습니다. 특히, AI 도구가 메시지, 파일, 업무 흐름, 직원 기록에 접근할 수 있게 됨에 따라 이러한 경향은 더욱 두드러지고 있습니다. 시스코는 “2026년 데이터 개인정보 보호 벤치마크 조사”에 따르면, 조직의 56%가 여전히 전담 AI 거버넌스 위원회를 설치하지 않은 것으로 보고되었으며, 워크플레이스 도구의 자율성이 높아짐에 따라 명백한 관리상의 공백이 발생하고 있습니다. 또한, 마이크로소프트는 “2025년 디지털 방어 보고서”에서 AI를 활용한 자동화된 피싱 및 다단계 공격 체인이 원격 액세스 환경에 대한 부담을 가중시키고 있으며, 그 결과 분산형 디지털 워크플레이스 도입에 따른 운영 위험이 증가하고 있다고 지적하고 있습니다. 이러한 문제들은 BFSI(은행 및 금융 및 보험) 및 의료와 같이 규제가 엄격한 분야에서 특히 중요하며, 해당 분야의 구매자들은 계약 체결 전에 SOC 2 Type II, ISO 27001, FedRAMP 및 HIPAA 관련 통제 조치를 요구하는 경우가 많습니다. 그 결과, 디지털 워크플레이스 시장에 진출하는 벤더들에게는 판매 주기의 장기화, 문서화 요건의 강화, 비용 증가와 같은 과제가 대두되고 있습니다. 또한, 성숙한 거버넌스 체계, 감사 대응 능력, 지역별 규정 준수 지원을 입증할 수 있는 공급업체는 조달 과정에서 조기에 우위를 점할 수 있게 됩니다.

부문별 분석

솔루션 부문은 2025년 매출의 63.89%를 차지하고, 2031년까지 연평균 성장률(CAGR) 20.62%로 성장할 것으로 전망됩니다. 이는 해당 솔루션이 디지털 워크플레이스 시장에서 더 큰 점유율을 차지하고 있으며, 시장 전체보다 빠르게 성장하고 있음을 보여줍니다. 이러한 추세는 디지털 워크플레이스 시장의 구매자들이 여전히 서비스 전용 계약보다 소프트웨어 중심의 현대화를 선호하고 있음을 보여줍니다. 협업, 직원 간 커뮤니케이션, 워크플로우 접근, 엔드포인트 제어를 단일 운영 계층으로 통합한 플랫폼에 대한 수요가 가장 높습니다. 디지털 워크플레이스 시장에서는 자동화 기능을 독립적인 애드온으로 판매하는 것이 아니라, AI 기능을 이러한 핵심 모듈에 직접 통합할 수 있는 벤더가 높이 평가받고 있습니다. 이러한 경향은 갱신 시의 경제성도 강화합니다. 왜냐하면 워크플로우의 로직, 권한, 컨텐츠 모델이 한 번 구축되면 시스템을 교체할 때 혼란이 커지기 때문입니다.

또한, 디지털 워크플레이스 업계에서는 조직이 Windows 10으로의 전환이나 클라우드 관리형 엔드포인트의 부상에 대응할 수 있도록 지원하는 솔루션에 대한 관심이 높아지고 있습니다. 마이크로소프트가 2026년 4월에 Windows 365용 Windows 10 갤러리 이미지 제공을 중단함에 따라, 이미 가상 데스크톱 환경을 이용 중인 조직의 경우 Windows 11을 기반으로 한 클라우드 PC 도입 계획을 미루기가 어려워지고 있습니다. 이러한 변화는 디지털 워크플레이스 시장에서 VDI, 클라우드 PC 관리 및 통합 엔드포인트 제어에 대한 수요를 촉진하고 있습니다. 대기업의 경우, 여러 도구에 걸쳐 있는 에이전트형 워크플로우의 설정, 보안 확보, 거버넌스 관리에 외부 지원이 필요한 경우가 많기 때문에 이 서비스는 여전히 중요합니다. 그렇긴 하지만, 디지털 워크플레이스 시장에서 핵심 가치는 협업, 자동화, 엔드포인트 관리를 단일 제품 환경에 통합할 수 있는 벤더에게 있습니다.

클라우드는 2025년에 도입 점유율의 52.38%를 차지하고, 2031년까지 연평균 성장률(CAGR) 20.70%로 확대될 것으로 전망되어, 디지털 워크플레이스 시장에서 주도적인 위치를 차지하고 있으며 여전히 주요 제공 모델임을 입증하고 있습니다. 클라우드 부문이 디지털 워크플레이스 시장을 주도하고 있는 이유는 보다 신속한 프로비저닝, 보다 빈번한 기능 업데이트, 그리고 전체 사용자 그룹에 대한 AI 기능의 보다 간편한 배포를 지원하기 때문입니다. 또한, 벤더는 상호 연결되지 않은 On-Premise 환경에서는 재현하기 어려운 방식으로 분석, 거버넌스 및 지원 기능을 통합할 수 있습니다. 그 결과, 디지털 워크플레이스 시장의 성장은 워크로드의 심층적인 전환 및 기존 계약 범위 내에서의 사용자 수 확대와 점점 더 밀접하게 연결되고 있습니다. 이로 인해 구매자가 클라우드 제품군을 표준화하면, 공급업체와의 관계는 더욱 공고해집니다.

한편, 디지털 워크플레이스 시장은 완전히 획일적인 클라우드 모델로 전환되고 있는 것은 아닙니다. On-Premise 배포는 데이터 저장 장소 및 관리와 관련된 요구 사항이 여전히 엄격한 국방, 정부 기관 및 일부 금융 서비스 환경에서 여전히 중요한 역할을 수행하고 있습니다. 기존의 ERP, 파일 또는 ID 관리 시스템 위에 클라우드 협업 기능을 필요로 하는 기업들에게 있어 하이브리드 아키텍처는 여전히 중요하며, 공급업체가 단일 제어 평면을 통해 양쪽을 모두 관리할 수 있다면 디지털 워크플레이스 시장은 그 혜택을 누릴 수 있을 것입니다. 마이크로소프트는 Windows 11로의 전환, Windows 365 도입, 그리고 기기 보안을 더욱 긴밀하게 연계하여, 단순한 ‘클라우드 전용” 접근 방식이 아니라, 하이브리드 방식의 접근을 지원하고 있습니다. 앞으로 디지털 워크플레이스 시장에서는 최종 사용자와 IT 팀이 하이브리드 환경 관리를 클라우드 환경 관리와 마찬가지로 일관성 있게 느낄 수 있도록 해주는 공급업체가 높이 평가받게 될 것입니다.

지역별 분석

2025년, 북미는 디지털 워크플레이스 시장 점유율의 42.16%를 차지했으며, 공급업체의 높은 밀집도, 기업 내 클라우드 보급률, AI 기반 생산성 도구 도입 속도의 신속함 덕분에 1위 자리를 유지했습니다. 해당 지출의 대부분은 미국이 주도하고 있으며, 2025년 10월 Windows 10 지원 종료를 계기로 기기 교체, 엔드포인트 관리 시스템 업데이트, 클라우드 PC로의 전환이 연쇄적으로 진행되고 있으며, 이러한 추세는 2026년의 조달 동향에도 계속해서 영향을 미치고 있습니다. 캐나다와 멕시코에서는 전문 서비스 및 금융 서비스 등의 분야에서 국경을 초월한 플랫폼의 표준화가 진행되고 있으며, 이는 지역 내 수요를 더욱 부양하고 있습니다. 디지털 워크플레이스 시장은 여전히 북미가 가장 견조한 모습을 보이고 있으며, 이 지역의 기업들은 AI 기능, 거버넌스 관리, 직원 경험에 대한 목표를 보다 광범위한 플랫폼 의사결정에 적극적으로 반영하려는 태도를 보이고 있습니다. 따라서 이 지역은 수익 측면뿐만 아니라, 더 광범위한 디지털 워크플레이스 시장에 영향을 미치는 경우가 많은 제품의 조기 도입 패턴이라는 관점에서도 계속해서 중요한 위치를 차지하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 23.18%를 나타낼 것으로 예측되며, 예측 기간 동안 디지털 워크플레이스 시장에 가장 크게 기여할 것으로 전망됩니다. 이러한 성장은 정부 주도의 디지털화, 중소기업(SME)의 폭넓은 참여, 그리고 선진국과 신흥국 모두에서 나타나는 ‘클라우드 우선”의 워크플레이스 아키텍처의 보급에 힘입어 이루어지고 있습니다. 인도는 대규모 IT 서비스 인프라와, 클라우드를 통해 제공되는 업무용 도구를 대규모로 도입할 수 있게 되어 가는 국내 기업 환경을 통해 시장에 기여하고 있습니다. 일본, 한국, 호주, 뉴질랜드는 기업의 높은 디지털 성숙도를 바탕으로 디지털 워크플레이스 시장을 지탱하고 있는 반면, 동남아시아는 도입 단계가 초기 단계에 머물러 있지만, 현지 운영 상황에 맞춘 모바일 우선 SaaS 모델을 통해 급속히 확대되고 있습니다. 이 지역 전체에서 디지털 워크플레이스 시장은 대규모 현지 인프라를 구축하지 않고도 보다 신속한 도입과 간편한 관리를 원하는 구매자들 덕분에 호황을 누리고 있습니다.

유럽은 수요가 견조하기 때문에 디지털 워크플레이스 시장에 있어 여전히 중요한 지역이지만, 공급업체 선택은 개인정보 보호, 주권, 규정 준수 관련 우려에 의해 더욱 크게 좌우되고 있습니다. 독일은 그 대표적인 예입니다. Bitkom의 보고서에 따르면, 2026년에는 독일 기업의 41%가 AI를 적극적으로 활용할 것으로 예상되며, 이는 2024년의 17%에서 증가한 수치이지만, 여전히 77%가 데이터 보호 요건을 주요 장애물로 꼽고 있습니다. 남미에서는 브라질과 아르헨티나의 금융 서비스, 소매, 기술 분야에 대한 수요를 바탕으로 시장이 발전하고 있지만, 통화 압박과 통신 환경의 격차로 인해 사업 확장 속도가 둔화될 가능성이 있습니다. 중동에서는 사우디아라비아와 아랍에미리트(UAE)에서 진행되고 있는 대규모 공공 및 기업 대상 디지털 프로그램의 혜택을 누리고 있습니다. 한편, 아프리카는 아직 초기 단계이지만, 남아프리카공화국, 나이지리아, 케냐, 이집트 등의 국가에서는 모바일 네이티브 SaaS의 도입과 구조적으로 부합하고 있습니다. 이러한 점들을 종합해 보면, 해당 지역들은 디지털 워크플레이스 시장에 대한 수요가 전 세계적으로 존재하는 한편, 규정 준수, 인프라, 근무 환경이 도입 속도를 좌우하는 측면에서는 여전히 지역별 특성이 존재함을 보여줍니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the digital workplace market size is projected to be USD 84.90 billion in 2025, USD 100.50 billion in 2026, and reach USD 244.16 billion by 2031, growing at a CAGR of 19.43% from 2026 to 2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecom, BFSI, Healthcare, Manufacturing, Retail, Government and Public Sector, Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Workplace Market Trends and Insights

AI-Powered Collaboration and Workflow Automation Drive Enterprise Adoption

AI-powered collaboration has moved from limited pilots to broad enterprise use, and that shift is now the strongest demand driver in the digital workplace market. Active AI agents in the Microsoft 365 ecosystem grew 15x year over year between March 2025 and March 2026, and the increase was 18x among large enterprises, indicating how quickly adoption is deepening within established workplace platforms. Microsoft also found that 49% of more than 100,000 Copilot conversations in February 2026 supported cognitive work such as analysis, problem-solving, evaluation, and creative thinking, suggesting that AI is being used for higher-value work rather than just simple drafting. This matters for the digital workplace market because buyers are increasingly choosing platforms that embed AI into collaboration, document, and workflow environments from the start. That preference raises switching costs and improves renewal potential for vendors whose road maps are centered on human-AI teamwork. It also makes feature depth more important than simple product breadth as the digital workplace market moves into a more mature adoption phase.

Agentic AI and Enterprise Search Connector Expansion Redefine Workplace Architecture

Agentic AI is widening the role of the digital workplace market from a set of productivity tools into a layer that can reason, retrieve information, and complete work across enterprise systems. Microsoft released Work IQ APIs into general availability in June 2026, creating a shared intelligence layer that lets agents access context and act across Microsoft 365 data and applications. Nexthink Spark, launched in January 2026, achieved a 77% first-contact resolution rate for IT issues and resolved Level 1 issues autonomously in under 2 minutes, demonstrating that agent-based models can already handle a meaningful share of service activity in the digital workplace market. The practical result is that enterprise search is no longer just a retrieval feature, because it is becoming part of the execution path for tasks, approvals, support, and content handling. Vendors that lack strong connector ecosystems for ERP, HR, ITSM, and communication tools will find it harder to remain central as this model spreads. Vendors that build proprietary connectors and stronger orchestration capabilities are likely to gain a more durable position in the digital workplace market over the forecast period.

Data Privacy, Cybersecurity, and Compliance Exposure Extend Procurement Cycles

Data privacy and cybersecurity remain the most persistent sources of friction in the digital workplace market, especially as AI tools gain access to messages, files, workflows, and employee records. Cisco reported in its 2026 Data Privacy Benchmark Study that 56% of organizations still lack a dedicated AI governance committee, which leaves a clear control gap as workplace tools become more autonomous. Microsoft also documented in its 2025 Digital Defense Report that AI-automated phishing and multi-stage attack chains are increasing pressure on remote-access environments, thereby raising the operating risk of distributed digital workplace deployments. These issues matter most in regulated fields such as BFSI and healthcare, where buyers often require SOC 2 Type II, ISO 27001, FedRAMP, and HIPAA-related controls before contract award. The result is longer sales cycles, greater documentation requirements, and higher costs for vendors serving the digital workplace market. It also gives providers that can demonstrate mature governance, audit readiness, and regional compliance support an early edge in the buying process.

Other drivers and restraints analyzed in the detailed report include:

- Rising Hybrid and Distributed Work Normalization Creates Platform Replacement Demand

- Cloud and SaaS Workplace Suite Migration Widens the Addressable Market

- Legacy Application and Integration Complexity Limits Deployment Velocity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 63.89% of revenue in 2025 and are projected to grow at a 20.62% CAGR through 2031, indicating they held a larger share of the digital workplace market and are expanding faster than the overall market. This pattern shows that buyers in the digital workplace market still prefer software-led modernization over service-only engagements. Demand is strongest where platforms combine collaboration, employee communication, workflow access, and endpoint control into a single operating layer. The digital workplace market is rewarding vendors that can embed AI capabilities directly into these core modules rather than selling automation as a detached add-on. That preference also strengthens renewal economics, because once workflow logic, permissions, and content models are embedded, replacement becomes more disruptive.

The digital workplace industry is also seeing greater interest in solutions that help organizations navigate the Windows 10 transition and the rise of cloud-managed endpoints. Microsoft retired Windows 10 gallery images for Windows 365 in April 2026, making it harder for organizations already using virtual desktop environments to defer Windows 11-oriented cloud PC planning. That change supports demand for VDI, cloud PC management, and unified endpoint control inside the digital workplace market. Services still matter because large enterprises often need outside help to configure, secure, and govern agentic workflows that span several tools. Even so, the center of value in the digital workplace market remains with solution vendors that can pull collaboration, automation, and endpoint administration into a single product environment.

Cloud held 52.38% of deployments in 2025 and is projected to expand at a 20.70% CAGR through 2031, giving it the leading position in the digital workplace market and confirming that it remains the dominant delivery model. The cloud segment leads the digital workplace market because it supports faster provisioning, more frequent feature updates, and simpler distribution of AI capabilities across user groups. It also allows vendors to unify analytics, governance, and support functions in ways that are harder to replicate across disconnected local installations. As a result, growth in the digital workplace market is increasingly tied to deeper workload migration and wider seat expansion inside existing contracts. This makes vendor relationships more durable once a buyer has standardized on a cloud suite.

At the same time, the digital workplace market is not moving to a fully uniform cloud model. On-premises deployments still serve defense, government, and some financial services environments where residency and control requirements remain strict. Hybrid architectures continue to matter for enterprises that need cloud collaboration on top of legacy ERP, file, or identity systems, and the digital workplace market benefits when vendors can manage both sides through one control plane. Microsoft has linked Windows 11 migration, Windows 365 adoption, and device security more closely, supporting a blended approach rather than a simple cloud-only narrative. Over time, the digital workplace market is likely to reward providers that can make hybrid administration feel as consistent as cloud administration for end users and IT teams.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility and Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

- By End-user Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordics

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Kenya

- Rest of Africa

- North America

Geography Analysis

North America held 42.16% of the digital workplace market share in 2025, maintaining its lead due to its dense vendor base, deep enterprise cloud adoption, and faster adoption of AI-enabled productivity tools. The United States drives most of that spending, and the October 2025 end of support for Windows 10 created a linked cycle of device refreshes, endpoint management renewals, and cloud PC migrations that continues to shape procurement in 2026. Canada and Mexico add to regional demand by standardizing cross-border platforms in sectors such as professional and financial services. The digital workplace market remains strongest in North America, where enterprises are willing to integrate AI features, governance controls, and employee experience goals into broader platform decisions. That keeps the region important not only for revenue, but also for early product adoption patterns that often influence the wider digital workplace market.

Asia-Pacific is projected to expand at a 23.18% CAGR through 2031, making it the fastest-growing regional contributor to the digital workplace market over the forecast period. Growth is supported by government-backed digitalization, broad SME participation, and the spread of cloud-first workplace architectures across both developed and emerging economies. India contributes through a large IT services base and a domestic enterprise environment that is increasingly able to absorb cloud-delivered workplace tools at scale. Japan, South Korea, Australia, and New Zealand support the digital workplace market through strong enterprise digital maturity, while Southeast Asia is earlier in adoption but moving quickly, with mobile-first SaaS models aligning with local operating conditions. Across the region, the digital workplace market benefits from buyers seeking faster deployment and simpler administration without building large local infrastructure stacks.

Europe remains a meaningful region for the digital workplace market because demand is strong, but vendor choice is shaped more heavily by privacy, sovereignty, and compliance concerns. Germany provides a clear example, as Bitkom reported that 41% of German companies actively use AI in 2026, up from 17% in 2024, while 77% still cite data protection requirements as a major hurdle. South America is developing through demand for financial services, retail, and technology in Brazil and Argentina, though currency pressure and connectivity gaps can slow the rollout pace. The Middle East is benefiting from large public and enterprise digital programs in Saudi Arabia and the UAE, while Africa is still early but structurally aligned with mobile-native SaaS adoption in countries such as South Africa, Nigeria, Kenya, and Egypt. Taken together, these regions show that the digital workplace market is global in demand, but still local in how compliance, infrastructure, and workforce conditions shape adoption speed.

- TeamViewer SE

- Nexthink SA

- LumApps SAS

- Staffbase GmbH

- Simpplr Inc.

- Appspace Inc.

- Haiilo GmbH

- Powell Software SAS

- Igloo Software Inc.

- Interact Software Group Limited

- Claromentis Ltd.

- Axero Solutions LLC

- Invotra Limited

- Jostle Corporation

- Passageways, Inc.

- InvolveSoft, Inc.

- Robin Powered, Inc.

- eXo Platform SAS

- Liferay, Inc.

- Lakeside Software, LLC

- ControlUp Technologies Ltd.

- Flexxible Information Technology, S.L.

- Kissflow Inc.

- United Planet GmbH

- Workgrid Software LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Rising Hybrid and Distributed Work Normalization

- 4.3.2 Cloud and SaaS Workplace Suite Migration

- 4.3.3 Growing Investment in Digital Employee Experience

- 4.3.4 AI-Powered Collaboration and Workflow Automation

- 4.3.5 Windows 10 Endpoint Refresh, Windows 11 Adoption, and Cloud PC Migration

- 4.3.6 Agentic AI and Enterprise Search Connector Expansion

- 4.4 Market Restraints

- 4.4.1 Data Privacy, Cybersecurity, and Compliance Exposure

- 4.4.2 Legacy Application and Integration Complexity

- 4.4.3 Tool Sprawl and Digital Friction

- 4.4.4 AI Governance and Workforce Enablement Gaps

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.6.1 Data Protection and Digital Workplace Governance

- 4.6.2 Workplace AI and Employee Monitoring Rules

- 4.7 Technological Outlook

- 4.7.1 GenAI Copilots and Agent Orchestration

- 4.7.2 Unified Endpoint Management and Self-Healing IT

- 4.7.3 Cloud PC, VDI, and Device-as-a-Service

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility and Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-user Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Colombia

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Nordics

- 5.5.3.8 Russia

- 5.5.3.9 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Southeast Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Kenya

- 5.5.6.5 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.2.1 Product Launches and Platform Upgrades

- 6.2.2 Partnerships and Alliances

- 6.2.3 Mergers and Acquisitions

- 6.2.4 Geographic Expansion

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TeamViewer SE

- 6.4.2 Nexthink SA

- 6.4.3 LumApps SAS

- 6.4.4 Staffbase GmbH

- 6.4.5 Simpplr Inc.

- 6.4.6 Appspace Inc.

- 6.4.7 Haiilo GmbH

- 6.4.8 Powell Software SAS

- 6.4.9 Igloo Software Inc.

- 6.4.10 Interact Software Group Limited

- 6.4.11 Claromentis Ltd.

- 6.4.12 Axero Solutions LLC

- 6.4.13 Invotra Limited

- 6.4.14 Jostle Corporation

- 6.4.15 Passageways, Inc.

- 6.4.16 InvolveSoft, Inc.

- 6.4.17 Robin Powered, Inc.

- 6.4.18 eXo Platform SAS

- 6.4.19 Liferay, Inc.

- 6.4.20 Lakeside Software, LLC

- 6.4.21 ControlUp Technologies Ltd.

- 6.4.22 Flexxible Information Technology, S.L.

- 6.4.23 Kissflow Inc.

- 6.4.24 United Planet GmbH

- 6.4.25 Workgrid Software LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment