|

시장보고서

상품코드

2073265

북미의 디지털 워크플레이스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

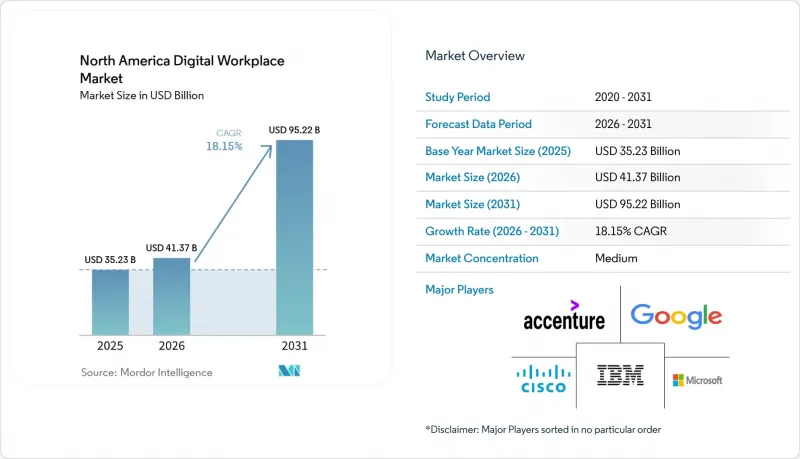

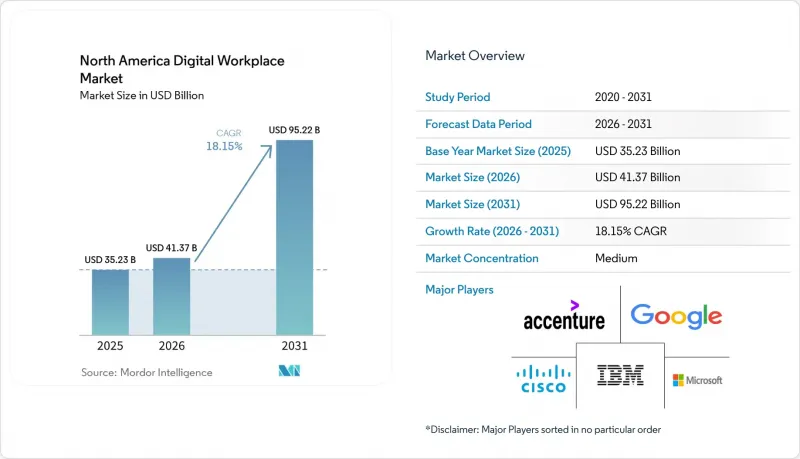

Mordor Intelligence에 의하면, 북미의 디지털 워크플레이스 시장 규모는 2025년 352억 3,000만 달러로 평가되었습니다. 2026년 413억 7,000만 달러에서 2031년까지 952억 2,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 18.15%를 나타낼 전망입니다.

본 보고서는 구성 요소(솔루션 및 서비스), 도입 형태(클라우드, On-Premise 등), 조직 규모(대기업 및 중소기업), 최종 사용자 산업 분야(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 의료, 제조, 소매, 정부·공공 부문 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 디지털 워크플레이스 시장 동향 및 인사이트

하이브리드 근무 및 유연한 근무 방식의 확산

하이브리드 근무 방식은 북미의 디지털 워크플레이스 시장에서 정착된 운영 모델로 자리 잡았으며, 협업 및 직원 지원 플랫폼에 대한 꾸준한 수요를 지속적으로 뒷받침하고 있습니다. 캐나다에서는 2026년 3월 기준으로 전문직 종사자의 56%가 하이브리드 근무를 가장 선호하는 근무 형태로 꼽았으며, 이는 유연성이 일시적인 조치가 아니라 노동력에게 있어 지속적인 기대 사항으로 남아 있음을 보여줍니다. 이러한 추세에 따라, 분산된 팀 전체에서 클라우드 기반 커뮤니케이션 도구, 문서 접근 도구, 디지털 서비스 도구가 계속해서 일상적으로 활용되고 있습니다. 핵심이 되는 하이브리드 인프라가 구축되면, 조직은 플랫폼을 전면적으로 교체하는 것보다 더 원활한 방식으로 스케줄링, 분석, AI 지원 도구를 추가할 수 있습니다. 이러한 움직임은 기존 고객을 대상으로 한 지속적인 플랫폼 확장을 뒷받침하며, 신규 도입과 마찬가지로 업그레이드를 통해 북미의 디지털 워크플레이스 시장의 성장을 가속하고 있습니다.

AI를 활용한 협업 및 자동화 도입

AI를 활용한 협업은 현재 북미의 디지털 워크플레이스 시장에서 가장 강력한 성장 동력 중 하나가 되고 있습니다. 이는 기업이 단순한 시범 운영이 아닌, 실제 업무에 활용하고 있기 때문입니다. 마이크로소프트의 보고서에 따르면, Microsoft 365 생태계 내의 활성 사용자 수는 2025년 3월부터 2026년 3월까지 전년 대비 15배 증가했으며, 북미에서 이루어진 Copilot 대화의 49%가 분석, 문제 해결, 창의적인 작업 등 인지적 업무를 지원하는 데 사용되었습니다. 또한 마이크로소프트는 액센츄어(Accenture plc)가 74만 3,000개 라이선스 규모로 Copilot을 도입한 사례를 강조했습니다. 20만 명의 사용자 데이터에 따르면, 97%의 사용자가 정형화된 업무를 15배 더 빠르게 완료했으며, 53%는 생산성이 크게 향상되었다고 보고했습니다. ServiceNow는 2026년 5월, "자율적인 인력" 을 출범시키고, IT, 인사, CRM, 재무, 법무, 보안 운영에 걸친 거버넌스가 적용된 AI를 약 2억 명의 기업 임직원에게 확대함으로써 이러한 변화를 한층 더 가속화했습니다. 따라서 북미의 디지털 워크플레이스 시장은 AI 오케스트레이션으로 전환되고 있으며, 그 가치는 단편적인 채팅이나 검색 기능이 아니라 시스템 전반에 걸친 거버넌스가 적용된 실행에서 비롯됩니다. 리더십의 방식도 중요합니다. 마이크로소프트의 조사에 따르면, 관리자가 주도하는 AI 도입은 직장에서 에이전트형 AI에 대한 직원들의 신뢰와 그 가치에 대한 인식을 현저히 높이는 것으로 밝혀졌기 때문입니다.

엔드포인트의 확산과 ID의 분산

엔드포인트의 확산과 ID의 분산은 북미의 디지털 워크플레이스 시장에서 여전히 큰 장벽으로 남아 있습니다. 이는 분산형 용도, BYOD 정책 및 AI 에이전트가 거버넌스를 통한 관리보다 더 빠르게 확산되고 있기 때문입니다. Orchid Security의 2026년 조사에 따르면, 기업 용도의 57%가 중앙 ID 제공업체 이외의 곳에서 인증되고 있으며, 기업 계정의 40%는 인사 시스템상에서는 더 이상 활성 상태가 아닌 사용자에게 속하는 것으로 밝혀졌습니다. 해당 보고서에서는 비인간 정체성이 디렉터리의 적용 범위 밖이나 중앙 집중식 관리의 손이 닿지 않는 상태에서 운영되는 경우가 많아, 자율형 도구의 확산에 따른 위험을 높이고 있다는 점도 밝혀졌습니다. NIST의 사이버 보안 프레임워크 업데이트 및 직원 관련 지침은 현재 비인간 신원 및 분산형 인력의 위험을 관리할 필요성을 보다 직접적으로 반영하고 있지만, 복잡한 기업 환경 전반에 걸친 도입은 여전히 더딘 상태입니다. 이로 인해 시정 비용이 증가하고 플랫폼 도입이 지연됨에 따라, 아이덴티티 거버넌스를 독립된 통합 계층으로 남겨두지 않고 워크플레이스 환경에 직접 통합할 수 있는 벤더의 매력이 높아지고 있습니다.

부문별 분석

2025년, 북미의 디지털 워크플레이스 시장에서 디지털 워크플레이스 솔루션이 69.32%를 차지했습니다. 이는 지출이 개별 지원 활동이 아니라 통합형 소프트웨어 플랫폼에 크게 집중되어 있음을 보여줍니다. 또한, 이러한 솔루션은 2031년까지 연평균 성장률(CAGR) 18.56%를 나타낼 것으로 예측되며, 북미의 디지털 워크플레이스 시장에서 가장 빠르게 성장하는 분야로 꼽히고 있습니다. 이러한 추세는 협업, 분석, 워크플로우 자동화, AI 지원을 단일 상용 플랫폼 내에 통합한 환경에 대한 기업 수요를 반영하고 있습니다. Microsoft 365, Google Workspace, ServiceNow는 구매자가 여러 개의 독립적인 도구를 관리할 필요 없이, 이미 도입된 플랫폼 내에서 기능을 확장할 수 있게 해주기 때문에 이러한 변화의 중심적인 역할을 하고 있습니다. 따라서 북미의 디지털 워크플레이스 업계에서는 플랫폼 계층에서 더 많은 가치가 창출되고 있습니다. 이 계층에서는 일회성 소프트웨어 도입 작업보다 지속적인 라이선스 확장이 확장성이 더 뛰어나기 때문입니다.

액센츄어(Accenture plc)가 74만 3,000석 규모로 Microsoft 365 Copilot을 도입한 사례는 이러한 모델을 여실히 보여주고 있습니다. AI 기능을 통해 직원 수를 늘리지 않고도 시트당 수익을 높일 수 있기 때문입니다. 이 서비스는 여전히, 특히 전환, 통합, 거버넌스, 엔드포인트 프로그램 및 변경 지원 분야에서 북미의 디지털 워크플레이스 시장에서 중요한 역할을 수행하고 있습니다. 그러나 일상적인 도입 작업이 표준화되고 플랫폼에 의한 지원이 확대됨에 따라, 서비스 내의 가치 구성은 고부가가치화 방향으로 전환되고 있습니다. AI 거버넌스에 대한 자문, 도입 가속화, 운영 성과 측정이 가능한 공급업체는 범용적인 도입에 중점을 두는 기업보다 유리한 입장에 있습니다. 이 때문에 북미의 디지털 워크플레이스 시장에서는 솔루션 중심의 수익 구조가 형성되어 있지만, 복잡하고 규정 준수를 중시하며 대규모로 직원 체제를 변경하는 경우에는 서비스가 여전히 필수적입니다.

2025년, 클라우드는 북미의 디지털 워크플레이스 시장의 61.18%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 18.78%로 확대될 것으로 전망됩니다. 이러한 성장 속도는 북미의 디지털 워크플레이스 시장 전체의 성장률을 소폭 상회하며, 클라우드가 선호되는 제공 아키텍처로서 주도권을 잡아가고 있음을 뒷받침하고 있습니다. 그 주된 이유는 추상적인 것이 아니라 실용적인 것이며, 주요 벤더들은 현재 최신 협업, 자동화, AI 기능을 우선 클라우드 기반 구독 환경을 통해 제공합니다. 마이크로소프트의 에이전트 생태계 확대와 ServiceNow의 AI 플랫폼 출시는 모두 이러한 방향성을 뒷받침하고 있습니다. 이는 현재 제품 개발이 클라우드 네이티브 제공 방식 및 정기적인 기능 업데이트와 밀접하게 연결되어 있기 때문입니다. 구매자의 입장에서 볼 때, 이를 통해 개별 업그레이드 프로젝트의 필요성이 줄어들고, 분산된 직원 전체에게 보다 일관된 경험을 제공할 수 있게 됩니다.

On-Premise 배포는 정부 기관이나 제조업, 그리고 사이트 수준에서의 엄격한 관리, 레거시 용도에 대한 의존, 또는 업계 고유의 데이터 요구 사항이 있는 기타 환경에서 여전히 중요한 역할을 하고 있습니다. CISA(미국 사이버보안 및 인프라보안국)의 "신뢰할 수 있는 인터넷 연결" 이 아키텍처는 연방 정부의 보안 환경 내에서 클라우드 액세스 및 원격 연결을 구축하는 방식에 계속해서 영향을 미치고 있으며, 이것이 일부 조직이 현대화를 추진하는 와중에도 보다 체계적으로 관리되는 배포 모델을 유지하고 있는 이유 중 하나입니다. 많은 기업이 기존 인프라를 즉시 교체하기보다는 워크로드의 이식성이나 단계적인 전환 경로를 필요로 하기 때문에 하이브리드 배포는 여전히 중요합니다. 그런 의미에서 하이브리드는 일시적인 가교 역할에 그치지 않고, 새로운 클라우드 기능과 기존 운영 시스템 간의 균형을 맞추려는 조직에게 지속 가능한 운영 모델이기도 합니다. 따라서 북미의 디지털 워크플레이스 업계는 클라우드 주도형으로 계속 전환되고 있지만, 리스크, 규정 준수 또는 비즈니스 연속성이 더욱 중요시되는 분야에서는 하이브리드 아키텍처가 여전히 자리를 잡고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the north america digital workplace market size is projected to expand from USD 35.23 billion in 2025 and USD 41.37 billion in 2026 to USD 95.22 billion by 2031, registering a CAGR of 18.15% between 2026 and 2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Manufacturing, Retail, Government and Public Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America Digital Workplace Market Trends and Insights

Rising Hybrid and Flexible Work Mandates

Hybrid work has become a durable operating model in the North America digital workplace market, and it continues to support steady demand for collaboration and employee support platforms. In Canada, 56% of professionals ranked hybrid as their preferred work mode in March 2026, which shows that flexibility remains a standing workforce expectation rather than a short-lived adjustment. This preference keeps cloud-based communication, document access, and digital service tools in regular use across distributed teams. Once the core hybrid infrastructure is in place, organizations can add scheduling, analytics, and AI support tools with less friction than a full platform replacement. That dynamic supports recurring platform expansion inside existing accounts and helps the North America digital workplace market grow through upgrades as much as through first-time deployments.

AI-Enabled Collaboration and Automation Adoption

AI-enabled collaboration is now one of the strongest growth engines in the North America digital workplace market because enterprises are using it for real work rather than limited trials. Microsoft reported that active agents inside the Microsoft 365 ecosystem grew 15 times year over year between March 2025 and March 2026, and 49% of Copilot conversations in North America supported cognitive work such as analysis, problem-solving, and creative tasks. Microsoft also highlighted Accenture plc's 743,000-seat Copilot deployment, where data from 200,000 users showed 97% completed routine tasks 15 times faster and 53% reported significant productivity gains. ServiceNow reinforced this shift in May 2026 when it launched Autonomous Workforce and extended governed AI across IT, HR, CRM, finance, legal, and security operations for nearly 200 million enterprise employees. The North America digital workplace market is therefore moving toward AI orchestration, where value comes from governed execution across systems rather than from isolated chat or search features. Leadership behavior also matters because Microsoft found that manager-led AI adoption materially lifts employee trust and perceived value from agentic AI in the workplace.

Endpoint Sprawl and Identity Fragmentation

Endpoint sprawl and identity fragmentation remain major barriers in the North America digital workplace market because distributed applications, BYOD policies, and AI agents expand faster than governance controls. Orchid Security found in 2026 that 57% of enterprise applications were authenticated outside a central identity provider, while 40% of enterprise accounts belonged to users no longer active in HR systems. The same report also showed that non-human identities often operate without directory coverage or centralized oversight, which raises the risk of scaling autonomous tools. NIST's cybersecurity framework updates and workforce guidance now more directly reflect the need to manage non-human identities and distributed workforce risk, but implementation across complex enterprise environments still lags. This creates added remediation cost, slows platform rollout, and increases the appeal of vendors that can build identity governance directly into workplace environments rather than leaving it as a separate integration layer.

Other drivers and restraints analyzed in the detailed report include:

- Employee Experience-Led Workplace Modernization

- Cloud-First Workplace Standardization

- Integration Complexity Across Legacy Collaboration Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital workplace solutions accounted for 69.32% of the North America digital workplace market in 2025, indicating that spending is heavily centered on integrated software platforms rather than standalone support activities. Solutions are also projected to grow at a 18.56% CAGR through 2031, making them the fastest-growing component of the North America digital workplace market. This pattern reflects enterprise demand for environments that combine collaboration, analytics, workflow automation, and AI support within a single commercial structure. Microsoft 365, Google Workspace, and ServiceNow are central to this shift because they let buyers expand functionality within an installed platform rather than managing multiple separate tools. The North America digital workplace industry is therefore seeing more value captured at the platform layer, where recurring license expansion is easier to scale than one-time software deployment work.

Accenture plc's 743,000-seat Microsoft 365 Copilot rollout illustrates this model, as AI features can increase revenue per seat without requiring growth in the total employee count. Services still retain an important role in the North America digital workplace market, especially for migration, integration, governance, endpoint programs, and change support. However, the value mix inside services is shifting upward as routine implementation work becomes more standardized and more platform-assisted. Providers that can advise on AI governance, accelerate adoption, and measure operational outcomes are better placed than firms focused mainly on commodity implementation. This leaves the North America digital workplace market with a solutions-heavy revenue structure, while services remain essential for complex, compliance-driven, and large-scale workforce change.

Cloud accounted for 61.18% of the North America digital workplace market in 2025 and is forecast to expand at an 18.78% CAGR through 2031. That pace slightly exceeds the broader North America digital workplace market and confirms that cloud is taking the lead as the preferred delivery architecture. The main reason is practical rather than abstract, leading vendors now to deliver their newest collaboration, automation, and AI capabilities first through cloud-based subscription environments. Microsoft's expanding agent ecosystem and ServiceNow's AI platform releases both support that direction, since product development is now closely tied to cloud-native delivery and regular feature updates. For buyers, this reduces the need for separate upgrade projects and supports more consistent experiences across distributed workforces.

On-premises deployment still matters in government, manufacturing, and other settings with strict site-level control, reliance on legacy applications, or sector-specific data requirements. CISA's Trusted Internet Connections architecture continues to shape how secure federal environments structure cloud access and remote connectivity, which helps explain why some organizations maintain more controlled deployment models even as they modernize. Hybrid deployment remains important because many enterprises need workload portability and staged transition paths rather than immediate replacement of existing estates. In that sense, hybrid is not only a temporary bridge but also a durable operating model for organizations balancing new cloud features with older operational systems. The North America digital workplace industry, therefore, continues to move toward cloud leadership, while still leaving room for mixed architectures in sectors where risk, compliance, or operational continuity carry more weight.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility and Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Microsoft Corporation

- IBM Corporation

- Accenture plc

- Cisco Systems, Inc.

- Google LLC

- Citrix Systems, Inc.

- DXC Technology Company

- Cognizant Technology Solutions Corporation

- Hewlett Packard Enterprise Development LP

- NTT DATA Group Corporation

- Tata Consultancy Services Limited

- Wipro Limited

- Atos SE

- Unisys Corporation

- Capgemini SE

- Oracle Corporation

- Salesforce, Inc.

- VMware, Inc.

- ServiceNow, Inc.

- Zoom Communications, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Hybrid and Flexible Work Mandates

- 4.2.2 AI-Enabled Collaboration and Automation Adoption

- 4.2.3 Employee Experience-Led Workplace Modernization

- 4.2.4 Cloud-First Workplace Standardization

- 4.2.5 Security and Compliance Modernization Across Distributed Workforces

- 4.2.6 Cross-Border Managed Workplace Outsourcing in North America

- 4.3 Market Restraints

- 4.3.1 Endpoint Sprawl and Identity Fragmentation

- 4.3.2 Integration Complexity Across Legacy Collaboration Stacks

- 4.3.3 Budget Sensitivity in Small and Medium-Sized Enterprises

- 4.3.4 Change Fatigue and User Adoption Resistance

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility and Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 IBM Corporation

- 6.4.3 Accenture plc

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Google LLC

- 6.4.6 Citrix Systems, Inc.

- 6.4.7 DXC Technology Company

- 6.4.8 Cognizant Technology Solutions Corporation

- 6.4.9 Hewlett Packard Enterprise Development LP

- 6.4.10 NTT DATA Group Corporation

- 6.4.11 Tata Consultancy Services Limited

- 6.4.12 Wipro Limited

- 6.4.13 Atos SE

- 6.4.14 Unisys Corporation

- 6.4.15 Capgemini SE

- 6.4.16 Oracle Corporation

- 6.4.17 Salesforce, Inc.

- 6.4.18 VMware, Inc.

- 6.4.19 ServiceNow, Inc.

- 6.4.20 Zoom Communications, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment