|

시장보고서

상품코드

2073270

에너지 및 유틸리티 분야 디지털 워크플레이스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Digital Workplace In Energy and Utilities - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

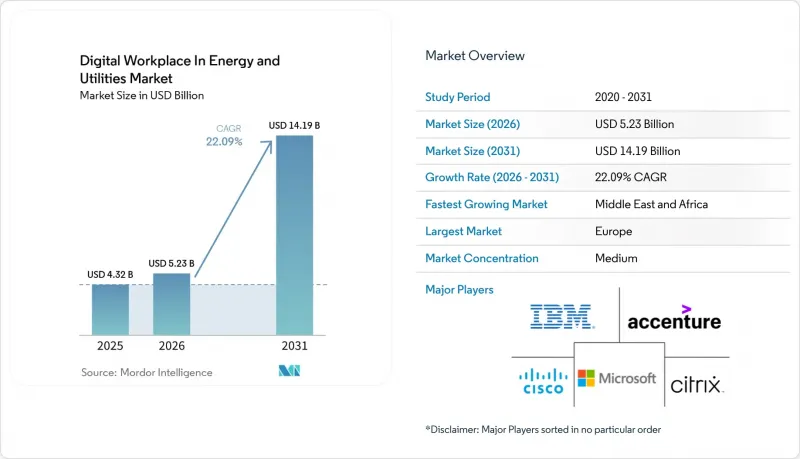

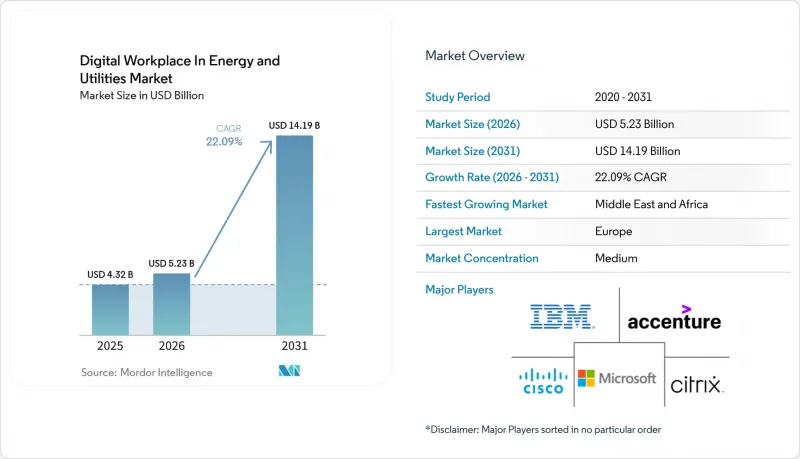

Mordor Intelligence에 의하면, 에너지 및 유틸리티 분야 디지털 워크플레이스 시장 규모는 2025년 43억 2,000만 달러, 2026년 52억 3,000만 달러에서 2031년까지 141억 9,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 22.09%를 나타낼 전망입니다.

본 보고서는 구성 요소별(솔루션(통합 커뮤니케이션 및 협업, 통합 엔드포인트 관리, 엔터프라이즈 모빌리티 관리 등) 및 서비스), 배포 방식별(클라우드, On-Premise 등), 조직 규모별(대기업 및 중소기업), 지역별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러)으로 표시되어 있습니다.

세계 에너지 및 유틸리티 분야 디지털 워크플레이스 시장 동향 및 인사이트

하이브리드 및 분산형 인력의 디지털화

에너지 및 유틸리티 분야 디지털 워크플레이스 시장은 완전 원격 근무가 이전 최고치보다 감소했음에도 불구하고 하이브리드 근무 방식이 정착됨에 따라 지속적인 성장을 이어가고 있습니다. 2026년에는 62%의 조직이 고정된 사무실 출근일을 의무화할 것으로 예상되며, 이는 2025년의 49%에서 증가한 수치입니다. 이는 기업들이 현재 사무실, 현장 및 분산된 팀 전반에 걸쳐 접근, 출석, 일정 관리, 협업을 동시에 지원하는 도구가 필요함을 보여줍니다. 실제 사무실 이용률과 목표 이용률 간의 격차는 2025년 25포인트에서 2026년에는 18포인트로 축소되었으며, 주 3-4일 출근하는 직원의 비율은 19포인트 증가해 55%에 달했습니다. 이는 체계화된 하이브리드 근무 방식이 일시적인 조치가 아니라 운영 모델로 자리 잡아가고 있음을 보여줍니다. 에너지 및 유틸리티 분야 디지털 워크플레이스에서 이 점은 중요합니다. 왜냐하면 유틸리티자, 송전망 운영 사업자 및 에너지 서비스 기업은 단일 거버넌스가 확립된 플랫폼 내에서 사무직 직원, 현장 작업자 및 규제 대상 업무 흐름을 조율해야 하기 때문입니다. 엔드포인트 제어, 협업 및 인력 가시화를 동일한 환경에서 통합할 수 있는 공급업체는 기업으로부터 신규 투자를 유치하는 데 유리한 입장에 있습니다.

AI를 활용한 검색 및 지식 검색

키워드 검색에서 AI 기반 지식 검색으로의 전환은 조직이 디지털 워크플레이스을 구축하는 방식을 변화시키고 있습니다. 아마존 웹 서비스(Amazon Web Services)는 2026년 6월에 “Bedrock Managed Knowledge Base”의 일반 서비스를 시작하여, 기업이 벡터 데이터베이스의 복잡성을 직접 관리할 필요 없이 자사 고유의 데이터에 맞추어 지식 검색 시스템을 도입할 수 있는 방안을 제공했습니다. 에너지 및 유틸리티 분야 디지털 워크플레이스 역시 이와 같은 압박에 직면해 있으며, 이는 현장 및 사무실의 사용자들이 일상적인 업무 흐름에서 기술 문서, 유지보수 기록, 정책 컨텐츠에 대한 권한에 따른 접근을 점점 더 필요로 하고 있기 때문입니다. 경영진은 생성형 AI가 성장을 뒷받침할 것으로 기대하고 있지만, 도입 성숙도는 여전히 낮은 수준이며, 지식 검색과 거버넌스가 여전히 대규모 도입의 걸림돌로 작용하고 있는 것으로 나타났습니다. 그 결과, AI 검색은 더 이상 선택적인 프리미엄 기능으로 취급되지 않게 되었으며, 기업 내 에이전트 활용이 확대됨에 따라 아키텍처 계층에서 지식을 통합하는 플랫폼이 우위를 점하고 있습니다.

사이버 보안 및 데이터 주권에 대한 우려

에너지 및 유틸리티 분야에서 디지털 워크플레이스의 도입 속도를 가로막는 주요 제약 요인으로 사이버 보안과 데이터 주권이 여전히 꼽히고 있습니다. 후지쯔는 2026년 5월, AI 시스템 도입 후 그 학습 방식이나 작동을 제어할 수 있는 조직이 고작 8%에 불과하다고 보고했으며, 이는 워크플레이스의 데이터가 AI 도구에 공급됨에 따라 거버넌스상의 위험이 얼마나 급속히 확대될 수 있는지를 여실히 보여주고 있습니다. 유럽에서는 2026년 8월 2일부터 시행되는 EU AI법에 따라, 직원에게 통지해야 할 의무나 관련 시스템의 로그 보관 의무 등, 직장에서의 AI 관련 의무가 더욱 구체화될 것입니다. 이러한 요건으로 인해 심사 주기가 길어지면서, 구매자들은 보다 강력한 제어 기능, 감사 가능성 및 지역별 호스팅 옵션을 제공하는 플랫폼을 우선적으로 선택하고 있습니다. Orange Business는 2026년 3월, 프랑스의 자체 관리 인프라를 기반으로 ‘Live Collaboration”를 출범시킴으로써 이러한 압력에 대응했습니다. 이는 규정 준수의 복잡성이 제품 설계와 마찬가지로 공급업체의 입지를 형성하고 있음을 보여줍니다.

부문별 분석

2025년에는 솔루션이 매출의 64.38%를 차지하고, 에너지 및 유틸리티 분야 디지털 워크플레이스 부문에서는 2031년까지 연평균 성장률(CAGR) 22.93%로 가장 높은 성장률을 나타낼 것으로 전망됩니다. 이는 커뮤니케이션, 엔드포인트 거버넌스, 모빌리티, 워크플로우 자동화, 지식 접근을 통합한 솔루션 제품군이 단일 기능 도구보다 구매자들에게 더 선호되고 있음을 보여줍니다. 통합 커뮤니케이션 및 협업, 통합 엔드포인트 관리, 엔터프라이즈 모빌리티 관리, 직원 경험 플랫폼, 워크플로우 자동화, 가상 데스크톱 인프라 등은 모두 이 계층에 속하며, 신규 도입 시 주요 투자 대상으로 꼽히고 있습니다. 따라서 에너지 및 유틸리티 분야 디지털 워크플레이스 시장은 도구 기반의 세분화가 아닌 플랫폼 통합으로 나아가고 있습니다.

2025년에는 서비스가 시장의 나머지 부분을 차지하고 있으며, 솔루션 도입에는 거버넌스, 튜닝, 변경 관리 및 관리형 지원이 필요하기 때문에 서비스의 역할은 점점 더 중요해지고 있습니다. 에너지 및 유틸리티 분야 디지털 워크플레이스에서 서비스 수요는 기본적인 도입 작업에서 AI 거버넌스, 워크플로우 최적화, 그리고 직원 경험 관리에 대한 장기적인 지원으로 점차 전환되고 있습니다. 유니리(Unily)가 2026년 6월에 출시한 ‘Indi”는 단일 자연어 프롬프트를 통해 거버넌스가 확보된 인트라넷 환경을 생성하는 것으로, 솔루션 제공업체가 고객이 필요로 하는 도입 후 서비스 및 설정 지원 수준을 얼마나 높이고 있는지를 보여줍니다. 워크플레이스 플랫폼 내에서 자율적인 기능이 확대됨에 따라, 조직은 일회성 설정보다는 지속적인 모니터링이 필요하게 될 것이므로, 서비스의 정착도는 높아질 것입니다. 이러한 변화는 소프트웨어 계층과 그 주변의 운영 모델 모두를 지원할 수 있는 벤더나 파트너에게 유리하게 작용합니다.

지역별 분석

2025년, 유럽은 에너지 및 유틸리티 분야 디지털 워크플레이스 시장 점유율 31.52%를 차지하며, 기준 연도 기준 가장 큰 기여를 한 지역이 되었습니다. 독일, 영국, 프랑스가 여전히 주요 수요 거점으로 자리매김한 반면, 네덜란드와 북유럽 국가들도 디지털 성숙도 향상을 통해 시장을 뒷받침했습니다. Bitkom의 조사에 따르면, 2026년에는 독일 기업의 41%가 비즈니스 프로세스에 AI를 활용하고 있으며, 이는 2025년의 17%에서 증가한 수치로, AI를 도입한 기업의 77%가 경쟁력이 측정 가능할 정도로 향상되었다고 보고하고 있습니다. 아토스(Atos)와 마이크로소프트(Microsoft)는 2026년 6월, 54개국에 걸쳐 있는 아토스 직원 5만 6,000명을 대상으로 보안이 강화된 에이전트형 AI의 도입을 확대했습니다. 이는 규정 준수에 대한 기대가 높아지는 상황에서도 유럽의 대기업들이 대규모 도입을 추진하고 있음을 보여줍니다. EU AI법은 이 지역의 동향에 또 다른 요소를 더하고 있습니다. 직장 내 AI 도입에 있어서는 직원들에게 이를 알리고, 로그를 기록하며, 설명 책임이 있는 거버넌스에 대해 더욱 세심한 배려가 필요해졌기 때문입니다.

북미는 성숙한 클라우드 인프라, 협업 소프트웨어의 높은 보급률, 그리고 AI 관련 기업 지출이 많다는 점 덕분에 에너지 및 유틸리티 분야 디지털 워크플레이스 수요 규모에서 여전히 2위를 유지하고 있습니다. 아시아태평양은 그 뒤를 이어 중국, 일본, 인도, 한국이 주도하고 있습니다. 이 국가들에서는 대규모 산업 및 기술 생태계가 사무실과 현장 모두의 이용 사례에서 워크플레이스의 현대화를 뒷받침하고 있습니다. 인도는 견고한 IT 서비스 기반을 통해 계속해서 중요한 역할을 수행하고 있는 반면, 일본과 한국에서는 생산 및 운영 환경까지 확장 가능한 엔드포인트 및 워크플로우 도구에 대한 수요가 더욱 높아지고 있습니다. 남미는 소규모 기반에서 성장해 왔으며, 클라우드 가격이 저렴해지고 모바일 우선 업무 방식이 보급되면서 대상 고객층이 확대되는 가운데, 브라질과 콜롬비아가 도입을 주도하고 있습니다.

중동 및 아프리카는 2025년 시점에서 시장 규모가 작았으나, 에너지 및 유틸리티 분야 디지털 워크플레이스 부문에서는 2031년까지 연평균 성장률(CAGR) 23.65%라는 가장 높은 성장률을 나타낼 것으로 예측됩니다. 이러한 성장은 정부 주도의 클라우드 투자, 국가 차원의 AI 프로그램, 그리고 대기업과 중소기업 모두에서 디지털 도입이 확대됨에 따라 뒷받침되고 있습니다. 마이크로소프트의 사우디아라비아 Azure 데이터센터 리전은 2026년 1월에 일반 서비스를 시작했습니다. 이를 통해 규제 대상 산업 분야 로컬 데이터 저장 옵션이 확대되었으며, 걸프협력회의(GCC) 전역의 클라우드 도입 환경이 강화되었습니다. 아프리카 전역에서도 정부 주도의 디지털화 프로그램과 모바일 광대역 접속의 확대가 도입을 뒷받침하고 있습니다. 특히 남아프리카공화국, 나이지리아, 케냐, 이집트에서는 현장 업무가 많은 업계가 모바일 우선 워크플레이스 플랫폼의 혜택을 누릴 수 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the digital workplace in energy and utilities market size is projected to expand from USD 4.32 billion in 2025 and USD 5.23 billion in 2026 to USD 14.19 billion by 2031, registering a CAGR of 22.09% between 2026 and 2031.

This report is Segmented by Component [Solutions (Unified Communication and Collaboration, Unified Endpoint Management, Enterprise Mobility Management, and More), and Services], Deployment Mode (Cloud, On-Premise, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Digital Workplace In Energy and Utilities Market Trends and Insights

Hybrid and Distributed Workforce Digitization

The digital workplace in energy and utilities market continues to gain from the normalization of hybrid work, even though fully remote work has fallen from its earlier peak. In 2026, 62% of organizations mandate fixed in-office days, up from 49% in 2025, indicating that enterprises now need tools that support access, presence, scheduling, and collaboration across office, field, and distributed teams simultaneously. The gap between actual and target office utilization narrowed to 18 percentage points in 2026 from 25 in 2025, and employees attending 3-4 days per week rose by 19 percentage points to 55%, indicating that structured hybrid work is becoming an operating model rather than a temporary adjustment. In the digital workplace in energy and utilities market, this matters because utilities, grid operators, and energy service firms must now coordinate office staff, field crews, and regulated workflows within a single, governed platform. Vendors that can combine endpoint control, collaboration, and workforce visibility in the same environment are better placed to win new enterprise spending.

AI-Assisted Search and Knowledge Retrieval

The shift from keyword search to AI-based knowledge retrieval is changing how organizations structure digital work. Amazon Web Services made Bedrock Managed Knowledge Base generally available in June 2026, giving enterprises a way to deploy retrieval systems for their proprietary data without managing the complexity of vector databases themselves. The digital workplace in energy and utilities market is responding to the same pressure, as frontline and office users increasingly need permission-aware access to technical documents, maintenance records, and policy content within daily workflows. Executives expect generative AI to support growth, but deployment maturity remains low, which shows that knowledge retrieval and governance are still limiting scaled adoption. As a result, AI search is no longer treated as an optional premium feature, and the platforms that unify knowledge at the architecture layer are gaining an advantage as enterprise agent use expands.

Cybersecurity and Data Sovereignty Concerns

Cybersecurity and data sovereignty remain major constraints on deployment speed in the digital workplace in energy and utilities market. Fujitsu reported in May 2026 that only 8% of organizations can control how their AI systems learn and behave after deployment, underscoring how quickly governance exposure can widen as workplace data feeds AI tools. In Europe, the EU AI Act will start to make workplace AI obligations more concrete, including worker notification requirements and log retention expectations for relevant systems, effective from August 2, 2026. These requirements lengthen review cycles and push buyers to favor platforms that offer stronger control, auditability, and regional hosting options. Orange Business responded to this pressure in March 2026 with the launch of Live Collaboration on sovereign infrastructure in France, which shows that compliance complexity is now shaping vendor positioning as much as product design.

Other drivers and restraints analyzed in the detailed report include:

- OT and IT Workflow Convergence

- Safety-Critical Knowledge Access Demand

- Legacy Systems and Identity Fragmentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 64.38% of revenue in 2025 and are also projected to record the fastest 22.93% CAGR through 2031 in the digital workplace in energy and utilities market. This shows that buyers are prioritizing integrated suites over narrow point tools as they connect communication, endpoint governance, mobility, workflow automation, and knowledge access. Unified communication and collaboration, unified endpoint management, enterprise mobility management, employee experience platforms, workflow automation, and virtual desktop infrastructure all sit within this layer, making it the core spending destination for new deployments. The digital workplace in energy and utilities market is therefore moving toward platform consolidation rather than a more fragmented tool base.

Services represented the balance of the market in 2025, and their role is becoming more important as solution rollouts now require governance, tuning, change management, and managed support. In the digital workplace of the energy and utilities industry, service demand is shifting away from basic implementation work toward long-term support for AI governance, workflow optimization, and employee experience management. Unily's June 2026 launch of Indi, which generates governed intranet environments from a single natural-language prompt, shows how solution providers are raising the level of post-deployment service and configuration support that customers will need. As autonomous features expand inside workplace platforms, services are likely to become stickier because organizations will need ongoing oversight instead of one-time setup. That shift favors vendors and partners that can support both the software layer and the operational model around it.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordics

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Kenya

- Rest of Africa

- North America

Geography Analysis

Europe held 31.52% of the digital workplace market share in energy and utilities in 2025, making it the largest regional contributor in the base year. Germany, the United Kingdom, and France remained the main demand centers, while the Netherlands and the Nordic countries added support through stronger digital maturity. Bitkom found that 41% of German companies used AI in business processes in 2026, up from 17% in 2025, and that 77% of AI adopters reported a measurable improvement in their competitive position. Atos and Microsoft expanded secure agentic AI deployment to 56,000 Atos employees across 54 countries in June 2026, which shows that large European enterprises are moving ahead with scaled activation even as compliance expectations rise. The EU AI Act is adding another layer to this regional profile, as workplace AI deployment now requires greater attention to worker notification, logging, and accountable governance.

North America remained the second-largest demand pool in the digital workplace in energy and utilities market because of its mature cloud base, strong collaboration software footprint, and high level of AI-related enterprise spending. Asia-Pacific ranked next, led by China, Japan, India, and South Korea, where large industrial and technology ecosystems support workplace modernization across both office and frontline use cases. India continues to matter through its deep IT services base, while Japan and South Korea create additional demand for endpoint and workflow tools that can extend into production and operational settings. South America is growing from a smaller base, with Brazil and Colombia leading adoption as cloud affordability and mobile-first work patterns widen the addressable customer pool.

The Middle East and Africa held a smaller base in 2025, but it is projected to record the fastest 23.65% CAGR through 2031 in the digital workplace in energy and utilities market. Growth is being supported by sovereign cloud investment, national AI programs, and expanding digital adoption among both large enterprises and SMEs. Microsoft's Saudi Arabia Azure datacenter region reached general availability in January 2026, which improved local data residency options for regulated industries and strengthened cloud deployment conditions across the Gulf Cooperation Council. Across Africa, adoption is also gaining support from state-led digitization programs and wider mobile broadband access, especially in South Africa, Nigeria, Kenya, and Egypt, where field-intensive sectors can benefit from mobile-first workplace platforms.

- Microsoft Corporation

- IBM Corporation

- Accenture plc

- Cisco Systems, Inc.

- Omnissa, Inc.

- Citrix Systems, Inc.

- HCL Technologies Limited

- Wipro Limited

- Infosys Limited

- NTT DATA Group Corporation

- Capgemini SE

- DXC Technology Company

- Atos SE

- AvePoint, Inc.

- Unily Group Ltd

- Claromentis Limited

- Workai Sp. z o.o.

- Nutanix, Inc.

- SAP SE

- Oracle Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid and Distributed Workforce Digitization

- 4.2.2 Safety-Critical Knowledge Access Demand

- 4.2.3 OT and IT Workflow Convergence

- 4.2.4 AI Assisted Search and Knowledge Retrieval

- 4.2.5 Mobile First Enablement for Field Personnel

- 4.2.6 Regulatory Pressure for Audit Ready Collaboration

- 4.3 Market Restraints

- 4.3.1 Legacy Systems and Identity Fragmentation

- 4.3.2 Cybersecurity and Data Sovereignty Concerns

- 4.3.3 Low Adoption Among Field and Contractor Users

- 4.3.4 Integration Complexity Across OT and Enterprise Apps

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Colombia

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Netherlands

- 5.4.3.7 Nordics

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Southeast Asia

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Israel

- 5.4.5.5 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Nigeria

- 5.4.6.4 Kenya

- 5.4.6.5 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 IBM Corporation

- 6.4.3 Accenture plc

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Omnissa, Inc.

- 6.4.6 Citrix Systems, Inc.

- 6.4.7 HCL Technologies Limited

- 6.4.8 Wipro Limited

- 6.4.9 Infosys Limited

- 6.4.10 NTT DATA Group Corporation

- 6.4.11 Capgemini SE

- 6.4.12 DXC Technology Company

- 6.4.13 Atos SE

- 6.4.14 AvePoint, Inc.

- 6.4.15 Unily Group Ltd

- 6.4.16 Claromentis Limited

- 6.4.17 Workai Sp. z o.o.

- 6.4.18 Nutanix, Inc.

- 6.4.19 SAP SE

- 6.4.20 Oracle Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment