|

시장보고서

상품코드

2073232

중동 및 아프리카의 디지털 워크플레이스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Middle East and Africa Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

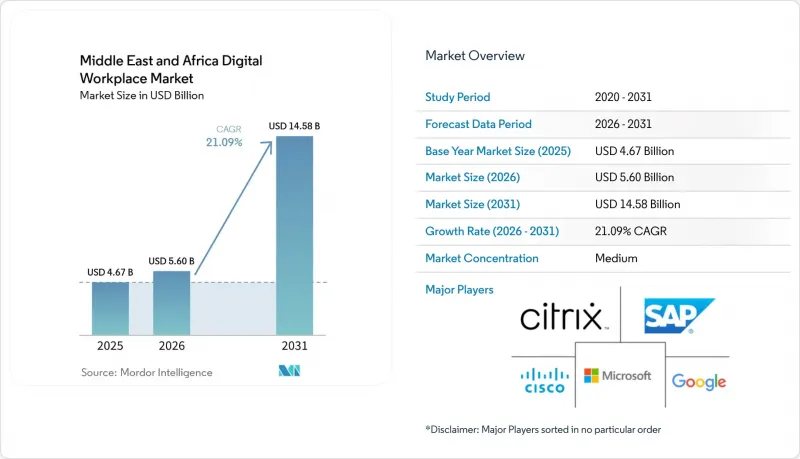

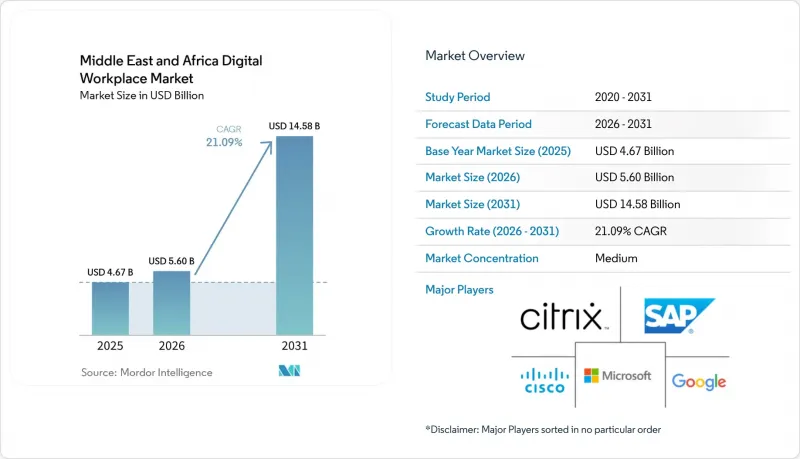

Mordor Intelligence에 의하면, 중동 및 아프리카 디지털 워크플레이스 시장 규모는 2025년 46억 7,000만 달러, 2026년 56억 달러에서 2031년까지 145억 8,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 21.09%를 나타낼 전망입니다.

본 보고서는 구성 요소(솔루션 및 서비스), 배포 방식(클라우드, On-Premise, 하이브리드), 조직 규모(대기업 및 중소기업), 최종 사용자 산업(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 의료, 정부·공공 부문, 교육 등) 및 지역별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동 및 아프리카 디지털 워크플레이스 시장 동향과 인사이트

분산형 기업에서 하이브리드 근무 도입에 대한 수요 증가

이 지역의 하이브리드 근무 방식은 단기적인 근무 형태의 범위를 넘어, 현재 많은 대형 고용주들에게 구조적인 운영 요건으로 자리 잡고 있습니다. 중동 및 아프리카의 디지털 워크플레이스 시장에서 이러한 수요가 가장 높은 곳은 대규모 프로젝트 현장, 여러 사무실, 현장 팀 및 국경을 초월한 사업을 동시에 관리하는 조직입니다. 사우디아라비아에서 진행 중인 메가 프로젝트로 인해, 협업과 기기 관리를 유지하기 위해서는 원격지, 지휘 센터, 본사 간의 지속적인 연계 필요성이 더욱 커지고 있습니다. 2025년 시스코가 사우디아라비아에서 실시한 클라우드 서비스, 데이터센터, 현지 생산 계획, AI 인재 양성 지원 등을 포함한 광범위한 사업 확장은 연결된 업무 환경에 필요한 인프라를 강화했습니다. 남아프리카공화국이나 나이지리아 등 아프리카 시장에서는 조직이 업무 플랫폼(워크플레이스 플랫폼)을 평가할 때, 분산된 사업장 간 직원의 이동성이 재택 원격 근무보다 더 중요하게 여겨지는 경우가 많습니다. 따라서 통신, 엔드포인트 관리, 다국어 지원 및 보안 액세스를 결합한 공급업체는 중동 및 아프리카의 디지털 업무 환경 시장에서 새로운 도입 주기를 확보하는 데 유리한 입장에 있습니다.

워크플레이스 인프라의 클라우드 전환 가속화

중동 및 아프리카의 디지털 워크플레이스 시장에서 클라우드 전환은 단순한 비용 문제가 아니라, 규정 준수 및 운영 모델에 관한 결정 사항으로 점점 더 인식되고 있습니다. 사우디아라비아와 아랍에미리트(UAE)에서는 정부 부처, 은행 및 기타 규제 대상 기관들이 현지 호스팅 증명이나 기밀 데이터에 대한 보다 엄격한 관리를 요구했기 때문에 그동안 일부 기업들의 도입이 더딘 양상을 보였습니다. 마이크로소프트는 사우디아라비아 동부 리전이 2026년 4분기부터 고객의 워크로드를 처리할 수 있게 될 것이라고 확인했습니다. 이를 통해 클라우드 워크로드 및 워크플레이스 용도를 위한 국내 가용성 영역이 추가되어, 이러한 장벽이 완화될 것입니다. e&enterprise의 “OneCloud” 서비스 역시 UAE에서 일어나고 있는 이와 같은 변화를 반영하고 있습니다. 해당 국가에서는 국내 데이터센터 환경 내에서 클라우드 및 AI 워크로드를 지원하기 위해 국가 주도의 하이퍼스케일 인프라가 구축되어 있습니다. 이러한 선택지가 확대됨에 따라, 더 많은 구매자가 데이터 상주 요건을 준수하고 서비스의 연속성을 저해하지 않으면서도 생산성 제품군을 현대화할 수 있게 될 것입니다. 그 결과, 규제상의 이유로 기존 On-Premise 모델에 머물러 있던 조직조차도 클라우드 네이티브 워크플레이스 플랫폼 도입을 정당화하기가 점점 더 쉬워지고 있습니다.

국가마다 차이가 있는 디지털 인프라의 품질

인프라의 품질은 여전히 국가마다 큰 차이를 보이며, 중동 및 아프리카의 디지털 업무 환경 시장에서 준비 상태에 편차가 나타나고 있습니다. 마이크로소프트의 ‘2026년 1분기 전 세계 AI 보급 보고서”에 따르면, 남아프리카공화국의 생산연령 인구 중 생성형 AI 도입률은 23.1%인 반면, 나이지리아는 10.1%에 그치고 있어, 디지털 준비 상태와 안정적인 접속 환경 측면에서 뚜렷한 격차가 드러나고 있습니다. 벤더들이 GCC(걸프협력회의) 회원국 및 남아프리카공화국 이외의 지역으로 사업을 확장함에 따라, 클라우드 우선 아키텍처에서는 저대역폭 지원, 하이브리드 또는 오프라인 지원과 같은 다양한 옵션이 필요한 경우가 많기 때문에 이러한 격차는 업무용 소프트웨어에 직접적인 영향을 미칩니다. 전력 불안정성이나 광대역 품질의 편차는 도입 기간의 장기화, 사용자 경험 저하, 협업이 많이 필요한 워크로드에서 신뢰성 저하를 초래할 가능성이 있습니다. 구매자들은 여전히 최신 도구를 원할지 모르지만, 가동 시간을 유지하기 어려운 시장에서는 실질적인 도입 위험이 여전히 높습니다. 이 때문에 기업 측의 관심이 엿보이는 경우에도 잠재적인 시장 기회는 본래의 잠재력보다 낮은 수준을 벗어나지 못하고 있습니다.

부문별 분석

2025년, 솔루션은 중동 및 아프리카 디지털 워크플레이스 시장 점유율의 69.56%를 차지하며, 해당 지역 전체에서 압도적인 주도적 지위를 확립했습니다. 이러한 위상은 통신, 엔드포인트 관리, 모빌리티, 직원 지원, 워크플로우 도구, 데스크톱 가상화를 단일 관리 환경으로 통합한 통합 제품군에 대한 지속적인 수요를 반영하고 있습니다. 중동 및 아프리카의 디지털 워크플레이스 시장은 조직들이 공급업체 수를 줄이고, 인터페이스를 간소화하며, 분산된 직원 전체에 걸친 거버넌스를 명확히 하기를 요구함에 따라 플랫폼 통합으로 나아가고 있습니다. 또한 구매자들은 업무 환경의 관리 체계를 감사 가능한 상태로 유지해야 한다는 압박에 직면해 있으며, 이는 당연히 개별 제품보다는 종합적인 솔루션 스택을 선호하는 경향으로 이어지고 있습니다. 가상 데스크톱 인프라(VDI)와 클라우드 PC 도구는 정부, 은행, 석유 및 가스 업계에서 주목을 받고 있으며, 현지 호스팅과 중앙 집중식 관리를 통해 데이터 저장 위치 및 접근과 관련된 우려를 완화하는 데 기여하고 있습니다.

마이크로소프트의 사우디아라비아 동부 지역에서는 2026년 4분기 이후, 특히 클라우드 기반 업무 환경을 확대하기 전에 현지에서 서비스가 제공되기를 기다려 온 조직을 중심으로 클라우드 PC 및 관리형 데스크톱의 도입이 더욱 광범위하게 진행될 것으로 예측됩니다. 2025년 시장의 나머지 30.44%는 서비스가 차지하고 있으며, 이는 기업들이 서비스를 도입함에 있어 여전히 구현, 관리형 지원 및 자문 서비스가 필요함을 보여줍니다. 많은 조직에서는 본격적인 도입 규모에 맞추어 정책 계층, 사용자 여정, 통합, 보안 제어를 설정하는 데 필요한 사내 인력이 여전히 부족합니다. 솔루션 제품군이 매출의 대부분을 차지하더라도 서비스가 계속해서 중요하게 여겨지는 이유는 강력한 설치 및 운영 지원이 없다면 소프트웨어 구매만으로는 가치를 창출하기 어렵기 때문입니다. 또한, 아랍에미리트(UAE)에서 해외 매니지드 서비스 제공업체들의 관심이 높아지고 있는 점은 사업 규모와 복잡성이 증가함에 따라 중동 및 아프리카의 디지털 워크플레이스 시장에서 서비스 계층 간의 경쟁이 격화되고 있음을 시사합니다.

2025년에는 클라우드가 시장의 63.19%를 차지하고, 중동 및 아프리카의 디지털 워크플레이스 시장에서 클라우드 도입 규모는 2031년까지 연평균 성장률(CAGR) 22.56%로 확대될 것으로 전망됩니다. 현지 하이퍼스케일 존의 등장으로, 규정 준수 요건과 확장 가능한 클라우드 운영 사이에서 오랫동안 지속되어 온 모순이 해소됨에 따라 성장 전망은 더욱 밝아졌습니다. 많은 구매자, 특히 정부 부처나 규제 대상 부문의 경우, 로컬 호스팅을 이용할 수 있게 됨에 따라 클라우드는 단순한 정책적 문제에서 실용적인 현대화의 길로 변화했습니다. 마이크로소프트의 ‘사우디아라비아 동부”리전은 로컬 데이터 상주성 및 사업 연속성 계획이 필요한 클라우드 기반 업무 환경 도입에 있어 조직에 더 큰 신뢰감을 줄 것입니다.

에어갭 환경이나 시스템 및 데이터에 대해 보다 엄격한 물리적 통제가 필요한 정부 부처, 국방 기관, 석유 및 가스 사업자에게는 On-Premise 구축이 여전히 중요합니다. 이는 보안 체계와 운영 환경이 구매자 유형에 따라 여전히 크게 다르기 때문에 중동 및 아프리카의 디지털 워크플레이스 시장에서 단일 배포 모델이 채택되지는 않을 것임을 의미합니다. 또한, 협업 및 분석을 위해 클라우드 기반 오케스트레이션을 필요로 하면서도, 지연 시간이나 관리상의 이유로 특정 워크로드를 On-Premise에 유지하고자 하는 대기업들 사이에서도 하이브리드 구성이 점차 확산되고 있습니다. 이러한 경향은 운영 기술(OT)과 사무 기술(IT)이 동일한 호스팅 모델을 공유하지 않고 공존해야 하는 경우에 특히 해당됩니다. 인정된 클라우드 보안 기준에서도 감사 가능성, 복원력, 현지 서비스 지원을 입증할 수 있는 공급업체가 계속해서 우대받고 있으며, 이로 인해 중동 및 아프리카의 디지털 워크플레이스 시장에서 만반의 준비를 갖춘 벤더의 입지가 강화되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the middle east and Africa digital workplace market size is projected to expand from USD 4.67 billion in 2025 and USD 5.6 billion in 2026 to USD 14.58 billion by 2031, registering a CAGR of 21.09% between 2026 and 2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Government and Public Sector, Education, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Middle East and Africa Digital Workplace Market Trends and Insights

Rising Demand for Hybrid Work Enablement Across Distributed Enterprises

Hybrid work in the region has moved beyond a short-term work arrangement and now functions as a structural operating requirement for many large employers. In the Middle East and Africa digital workplace market, this demand is strongest among organizations that manage large project sites, multiple offices, field teams, and cross-border operations simultaneously. Mega-project activity in Saudi Arabia has reinforced the need for continuous coordination among remote sites, command centers, and headquarters to sustain collaboration and device management. Cisco's broader Saudi expansion in 2025, including cloud services, data centers, local manufacturing plans, and support for AI talent development, strengthened the infrastructure needed for connected workplace environments. In African markets such as South Africa and Nigeria, workforce mobility across dispersed operating locations often matters more than home-based remote work when organizations evaluate workplace platforms. Vendors that combine communications, endpoint governance, multilingual usability, and secure access are therefore better placed to win new rollout cycles in the Middle East and Africa digital workplace market.

Accelerating Cloud Migration of Workplace Infrastructure

Cloud migration is increasingly being treated as a compliance and operating model decision rather than only a cost discussion across the Middle East and Africa digital workplace market. Saudi Arabia and the UAE had previously slowed some enterprise adoption because ministries, banks, and other regulated organizations needed proof of local hosting and tighter control over sensitive data. Microsoft confirmed that its Saudi Arabia East region will be available for customer workloads from Q4 2026, which reduces this friction by adding in-country availability zones for cloud workloads and workplace applications. e& enterprise's OneCloud offer reflected the same shift in the UAE, where sovereign hyperscale infrastructure has been positioned to support cloud and AI workloads inside local data center environments. As these options expand, more buyers can modernize productivity suites without weakening residency compliance or service continuity. The result is that cloud-native workplace platforms are becoming easier to justify for organizations that had stayed on older on-premises models for regulatory reasons.

Uneven Digital Infrastructure Quality Across Countries

Infrastructure quality still varies widely across countries, creating uneven readiness in the Middle East and Africa digital workplace market. Microsoft's Global AI Diffusion Report for Q1 2026 placed South Africa at 23.1% generative AI adoption among working-age people, while Nigeria stood at 10.1%, highlighting clear differences in digital readiness and reliable access. This gap affects workplace software directly because cloud-first architectures often require low-bandwidth, hybrid, or offline-capable variants as vendors expand beyond the GCC and South Africa. Power instability and uneven broadband quality can lengthen implementation timelines, weaken user experience, and reduce reliability for collaboration-heavy workloads. Buyers may still want modern tools, but practical deployment risk stays higher in markets where uptime is harder to maintain. This keeps the addressable opportunity below its full potential even when enterprise interest is visible.

Other drivers and restraints analyzed in the detailed report include:

- Growing Need for Secure Endpoint and Identity Control

- Increasing Adoption of Employee Experience Platforms and Digital Front Doors

- Budget Constraints and Long Enterprise Sales Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 69.56% of the Middle East and Africa digital workplace market share in 2025, making them the clear lead component across the region. This position reflects sustained demand for integrated suites that combine communications, endpoint management, mobility, employee support, workflow tools, and desktop virtualization in one controlled environment. The Middle East and Africa digital workplace market is moving toward platform consolidation as organizations seek fewer vendors, fewer interfaces, and clearer governance across distributed workforces. Buyers also face growing pressure to keep workplace controls auditable, which naturally favors broader solution stacks over disconnected point products. Virtual desktop infrastructure and cloud PC tools are gaining more attention in government, banking, and oil and gas, where local hosting and centralized control help reduce residency and access concerns.

Microsoft's Saudi Arabia East region is expected to support a broader wave of cloud PC and managed desktop deployments from Q4 2026 onward, especially among organizations that waited for local availability before expanding cloud-based work environments. Services accounted for the remaining 30.44% of the market in 2025, indicating that implementation, managed support, and advisory work remain necessary for enterprise adoption. Many organizations still lack the in-house teams needed to configure policy layers, user journeys, integrations, and security controls at full deployment scale. This is why services continue to matter even when solution suites dominate revenue, because the software purchase alone rarely delivers value without strong setup and operating support. Rising interest from foreign managed service providers in the United Arab Emirates also suggests that the services layer of the Middle East and Africa digital workplace market is becoming more competitive as rollout size and complexity increase.

Cloud accounted for 63.19% of the market in 2025, and the Middle East and Africa digital workplace market size for cloud deployment is projected to expand at a 22.56% CAGR through 2031. The growth case improved as local hyperscale zones reduced the long-standing conflict between compliance needs and scalable cloud operations. For many buyers, especially in ministries and regulated sectors, the availability of local hosting changed cloud from a policy issue into a practical modernization path. Microsoft's Saudi Arabia East region will give organizations more confidence in cloud-based workplace rollouts that need local data residency and continuity planning.

On-premises deployment still matters for ministries, defense entities, and oil and gas operators that require air-gapped environments or tighter physical control over systems and data. This means the Middle East and Africa digital workplace market will not adopt a single deployment model, as security posture and operating context still differ widely by buyer type. Hybrid setups are also gaining ground among large enterprises that want cloud-based orchestration for collaboration and analytics but keep selected workloads on site for latency or control reasons. That pattern is especially relevant where operational technology and office technology need to coexist without sharing the same hosting model. Certified cloud security standards also continue to favor providers that can demonstrate auditability, resilience, and local service support, which strengthens the position of well-prepared vendors in the Middle East and Africa digital workplace market.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Kenya

- Rest of Africa

- Middle East

List of Companies Covered in this Report:

- Microsoft Corporation

- Google LLC

- International Business Machines Corporation

- Cisco Systems, Inc.

- Citrix Systems, Inc.

- SAP SE

- Oracle Corporation

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- Samsung Electronics Co., Ltd.

- Zoho Corporation Pvt. Ltd.

- ServiceNow, Inc.

- Jamf Holding Corp.

- Sophos Group plc

- Fortinet, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Hybrid Work Enablement Across Distributed Enterprises

- 4.2.2 Accelerating Cloud Migration of Workplace Infrastructure

- 4.2.3 Growing Need for Secure Endpoint and Identity Control

- 4.2.4 Increasing Adoption of Employee Experience Platforms and Digital Front Doors

- 4.2.5 Expansion of Workflow Automation and Knowledge Management Use Cases

- 4.2.6 Rising Demand for Virtual Desktop Infrastructure and Cloud PC in Regulated Environments

- 4.3 Market Restraints

- 4.3.1 Uneven Digital Infrastructure Quality Across Countries

- 4.3.2 Budget Constraints and Long Enterprise Sales Cycles

- 4.3.3 Data Sovereignty and Cross-Border Compliance Complexity

- 4.3.4 Fragmented Legacy Application Environments and Integration Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Middle East

- 5.5.1.1 Saudi Arabia

- 5.5.1.2 United Arab Emirates

- 5.5.1.3 Turkey

- 5.5.1.4 Israel

- 5.5.1.5 Rest of Middle East

- 5.5.2 Africa

- 5.5.2.1 South Africa

- 5.5.2.2 Egypt

- 5.5.2.3 Nigeria

- 5.5.2.4 Kenya

- 5.5.2.5 Rest of Africa

- 5.5.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Google LLC

- 6.4.3 International Business Machines Corporation

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Citrix Systems, Inc.

- 6.4.6 SAP SE

- 6.4.7 Oracle Corporation

- 6.4.8 Dell Technologies Inc.

- 6.4.9 HP Inc.

- 6.4.10 Lenovo Group Limited

- 6.4.11 Samsung Electronics Co., Ltd.

- 6.4.12 Zoho Corporation Pvt. Ltd.

- 6.4.13 ServiceNow, Inc.

- 6.4.14 Jamf Holding Corp.

- 6.4.15 Sophos Group plc

- 6.4.16 Fortinet, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment