|

시장보고서

상품코드

2073610

유럽의 미량영양소 비료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Micronutrient Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

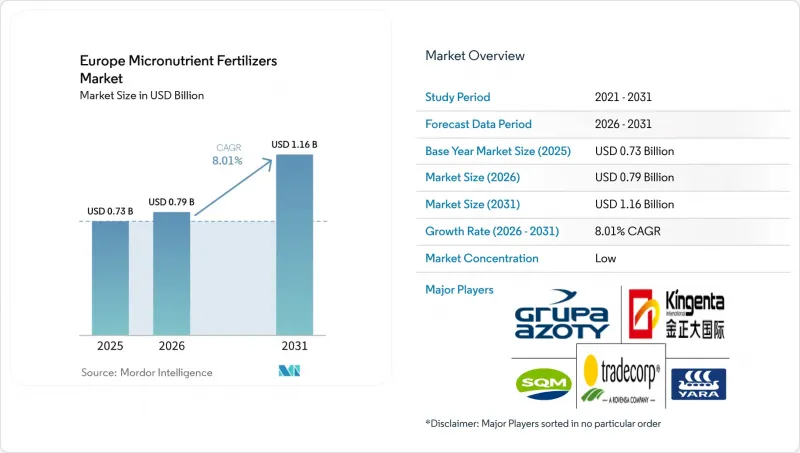

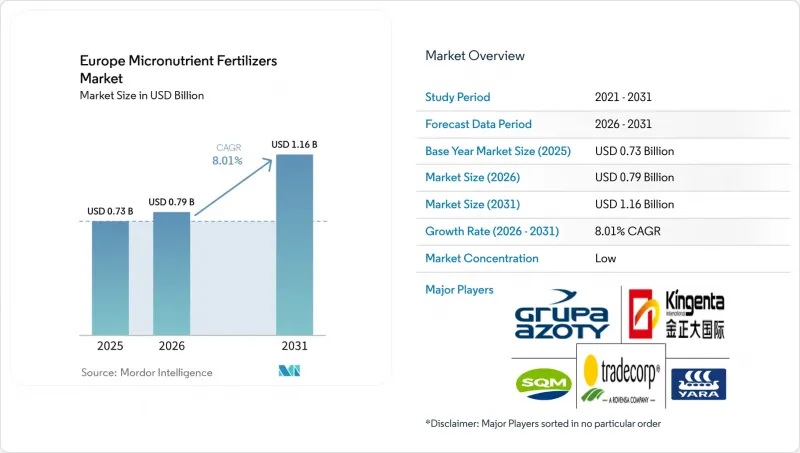

시장 성장 전망은 특수 미량영양소 영향을 더욱 더 강하게 받고 있어 몰리브덴은 2026년부터 2031년까지 CAGR 9.4%를 나타낼 것으로 예측되고 있어 이것은 모든 제품 카테고리 내에서 가장 높은 수치입니다.

Mordor Intelligence에 따르면, 유럽의 미량영양소 비료 시장 규모는 2025년에 7억 3,000만 달러로 평가되었고, 2026년에는 7억 9,000만 달러에 달할 것으로 추정됩니다. 본 보고서는 제품별(붕소, 구리, 철, 망간, 몰리브덴 등), 시용 방법별(비료 관개, 엽면 시비 등), 작물 유형별(밭작물, 원예작물 등), 지역별(프랑스, 독일, 이탈리아, 네덜란드, 러시아, 스페인, 우크라, 영국 등)으로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

유럽 미량영양소 비료 시장 동향과 인사이트

정밀 농업을 통한 토양 미량영양소 매핑

현재 유럽의 대규모 농장에서는 GPS 유도식 시료 채취 장치가 도입되어 있으며, 이를 통해 기존에는 전면 시비로 인해 가려졌던 아연, 철, 망간의 결핍 구역을 특정할 수 있는 상세한 토양 지도가 작성되고 있습니다. 코페르니쿠스 위성 이미지를 통해 계절별 수분량과 식생 지수가 추가됨에 따라, 농업 전문가들은 원격 감지 데이터와 현장 샘플을 대조할 수 있게 되었습니다. 독일의 장비 제조업체는 몇 미터 간격마다 미량영양소의 살포량을 조절할 수 있는 살포기를 상용화했으며, 시범 프로젝트를 통해 과다 시비를 최대 18% 줄이는 데 성공했습니다. 농지 데이터가 풍부해짐에 따라, 생산자들은 알칼리성 토양에서도 효능을 유지하면서 각 구역별 처방 지도에 부합하는 킬레이트화 혼합제 도입을 추진하고 있습니다. 자재 판매업체에 따르면, 농가가 균일한 살포 방식으로 돌아가면 결핍 증상이 재발하기 때문에 가변 시비 프로그램이 재주문으로 이어지고 있다고 합니다. 따라서 이 기술을 통해 미량영양소는 정밀 농업의 한 기법으로 자리 잡았으며, 유럽 전체 미량영양소 비료 시장의 사용량을 끌어올리고 있습니다.

유럽연합(EU)의 공동농업정책(CAP)에 따른 친환경 제도 인센티브

2023년부터 2027년까지의 공동농업정책(CAP)에서는 미량영양소 대차대조표를 포함한 문서화된 영양 관리 계획을 평가하는 생태 보전 지원금으로 480억 유로(520억 달러)가 배정되었습니다. 프랑스와 독일에서는 토양 검사 데이터 및 시비 기록을 통해 미량 원소의 농도가 최적 수준에 있는 것으로 확인될 경우, 생산자에게 헥타르당 60-80유로(헥타르당 65-87달러)가 지급됩니다. 이 자금은 중소규모 농장이 검사 비용, 이동식 센서, 가변 시비 제어기 비용을 충당하는 데 도움이 되고 있습니다. 또한, 사료 작물에서 구리, 아연, 셀레늄이 부족하면 가축의 면역력이 저하될 가능성이 있으므로, 수의위생 기관에서도 균형 잡힌 비료 시비를 권장하고 있습니다. 환경 규제의 준수와 농장 차원의 생산성 향상을 연계함으로써, 이 정책은 과거에는 선택적 관행에 불과했던 것을 주류 농업학적 의무로 전환하고 있습니다. 그 결과, 미량영양소 공급업체들은 상품 가격 변동과 무관하게, 다년간에 걸친 공동농업정책(CAP) 예산과 더욱 일관성을 갖춘 안정적인 미래 수요를 전망할 수 있게 되었습니다.

금속계 원자재 가격 변동

2024년 1월부터 2025년 9월까지 산화아연의 가격은 45% 상승한 반면, 황산구리의 가격은 분기마다 20-30%의 변동을 보였습니다. 이는 광산 공급 부족과 아연 도금 수요의 급증에 기인한 것입니다. 비료 공장은 계약량이 적고 순도 규격도 엄격하기 때문에 에너지 투입재만큼 쉽게 금속 헤지를 할 수 없습니다. 따라서 현물 시장에서의 임베디드이 완제품의 가격 책정에 영향을 미치는 경우가 종종 있습니다. 예측 불가능한 비용에 직면한 유통업체는 재고를 줄이고, 가격 급등분을 생산자에게 직접 전가합니다. 그 결과, 생산자들은 필수 영양소가 아닌 미량영양소의 구매를 미룰 가능성이 있습니다. 일부 제조업체는 제련소와 수년에 걸친 인수 계약을 협상하거나 재활용 금속에 주목하고 있지만, 합금의 제품별 순도는 농업용 순도 기준을 충족하는 경우가 거의 없습니다. 상품 가격이 다시 하락하면, 높은 원가 부담을 안고 있는 생산자는 대폭적인 가격 인하를 할 수밖에 없게 되어 이익률이 압박을 받게 됩니다. 따라서 가격 변동이 지속되면 소매 가격에 리스크 프리미엄이 가산되게 되며, 이는 유럽의 미량영양소 비료 시장에서 단기적인 경기 침체 시 성장을 저해하는 요인이 됩니다.

부문별 분석

2025년, 아연은 유럽 미량영양소 비료 시장 점유율의 31.1%를 차지했습니다. 이는 곡물, 유지종자, 옥수수 생산 시스템에서 아연이 광범위하게 활용된 데 따른 결과입니다. 이러한 생산 시스템에서는 영양분 이용 효율과 수확량의 최적화가 우선시되고 있습니다. 아연에 대한 수요는 중부 및 동유럽 일부 지역에서 아연 결핍 토양이 광범위하게 분포하고 있을 뿐만 아니라, 균형 잡힌 비료 시비 방식의 채택이 확대됨에 따라 더욱 뒷받침되고 있습니다. 또한, 킬레이트화 및 수용성 제제에 대한 수요가 증가함에 따라, 해당 지역 전체의 농업 생산성에 대한 아연의 기여도도 높아지고 있습니다.

콩과 작물 및 고부가가치 원예작물의 재배 확대에 따라, 질소 대사와 작물 생산성에서 중요한 역할을 하는 몰리브덴 수요가 증가하고 있습니다. 한편, 철, 구리, 망간, 붕소는 다양한 작물 재배 체계에서 여전히 중요한 위치를 차지하고 있습니다. 또한, 각 제조업체들은 시비 효율을 높이고 유럽 농업에서 발생하는 토양 영양분 결핍이라는 새로운 과제에 대응하기 위해 다영양소 제품 및 킬레이트 제품의 라인업을 확충하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 개 보고서의 내용

제3장 주요 요약 및 주요 조사 결과

제4장 주요 산업 동향

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 비료 업계 CEO를 향한 중요 전략적 과제

JHS 26.07.09According to Mordor Intelligence, the europe micronutrient fertilizers market size was valued at USD 0.73 billion in 2025 and is estimated to reach USD 0.79 billion in 2026. The market's growth outlook is increasingly influenced by specialty micronutrients, with molybdenum projected to grow at a CAGR of 9.4% during 2026 to 2031, the highest among all product categories.

This report is Segmented by Product (Boron, Copper, Iron, Manganese, Molybdenum, and More), by Application Mode (Fertigation, Foliar, and More), by Crop Type (Field Crops, Horticultural Crops, and More), and by Geography (France, Germany, Italy, Netherlands, Russia, Spain, Ukraine, United Kingdom, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Europe Micronutrient Fertilizers Market Trends and Insights

Precision-Agriculture Led Soil Micronutrient Mapping

Large European farms now operate GPS-guided sampling rigs that generate granular soil maps identifying pockets of zinc, iron, and manganese shortages long masked by blanket fertilization practices. Copernicus imagery adds seasonal moisture and vegetation indices, allowing agronomists to cross-check remote signals with physical samples. German equipment makers have commercialized spreaders that vary micronutrient rates every few meters, trimming over-application by up to 18% in pilot projects. As fields become data-rich, growers turn to chelated blends that stay available in alkaline zones and match prescription maps for each grid. Input distributors report that variable-rate programs convert into repeat orders because deficiencies re-emerge whenever farmers revert to uniform broadcasting. The technology therefore embeds micronutrients into precision-farming playbooks and pushes overall usage higher across the Europe micronutrient fertilizers market.

European Union Common Agricultural Policy Eco-Scheme Incentives

The 2023-2027 CAP earmarks EUR 48 billion (USD 52 billion) for eco-payments that reward documented nutrient-management plans, including micronutrient balance sheets. France and Germany reimburse growers EUR 60-80 per hectare (USD 65-87 per hectare) once soil-test data and application logs show optimum trace-element levels. These funds help small and medium-sized farms absorb the cost of laboratory tests, mobile sensors, and variable-rate controllers. Veterinary health agencies also back balanced fertilization because copper, zinc, and selenium deficiencies in forage crops can weaken livestock immunity. By bundling environmental compliance with farm-level productivity gains, the policy converts what was a voluntary practice into a mainstream agronomic obligation. Consequently, micronutrient suppliers see stable forward demand that is decoupled from commodity-price swings and better aligned with multi-year Common Agricultural Policy (CAP) budgets.

Metal-Based Raw-Material Price Volatility

Between January 2024 and September 2025, zinc oxide prices increased by 45%, while copper sulfate prices fluctuated by 20-30% per quarter, reflecting a tight mining supply and surging galvanizing demand. Fertilizer plants cannot hedge metals as easily as energy inputs because contract volumes are smaller and purity specs stricter, so spot market buying often drives finished-product quotes. Distributors facing unpredictable costs cut inventory and pass price spikes directly to growers, who may postpone non-essential micronutrient purchases. Some manufacturers negotiate multi-year offtake deals with smelters or turn to recycled metals, yet alloy by-product streams rarely meet agricultural purity thresholds. When commodity prices retrace, those producers stuck with high-cost stock must discount aggressively, eroding margins. Persistent volatility, therefore, adds a risk premium to retail prices and caps growth during short economic downturns across the Europe micronutrient fertilizers market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for High-Value Horticulture Crops

- Shift Toward Chelated Liquid and Water-Soluble Formulations

- Stringent European Union Limits on Heavy-Metal Contaminants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc accounted for 31.1% of the European micronutrient fertilizers market share in 2025, driven by its extensive application in cereal, oilseed, and maize production systems. These systems prioritize nutrient-use efficiency and yield optimization. The demand for zinc is further supported by the prevalence of zinc-deficient soils in parts of Central and Eastern Europe, alongside the growing adoption of balanced fertilization practices. Additionally, the increasing preference for chelated and water-soluble formulations is enhancing zinc's contribution to agricultural productivity across the region.

The rising cultivation of legumes and high-value horticultural crops is driving demand for molybdenum due to its critical role in nitrogen metabolism and crop productivity. Meanwhile, iron, copper, manganese, and boron continue to hold significant relevance across various crop systems. Manufacturers are also expanding their multi-nutrient and chelated product portfolios to enhance application efficiency and address evolving soil nutrient deficiencies in European agriculture.

Complete Report Scope:

- Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- By Geography

- France

- Germany

- Italy

- Netherlands

- Russia

- Spain

- Ukraine

- United Kingdom

- Rest of Europe

List of Companies Covered in this Report:

- Yara International ASA

- Compo Expert GmbH (Grupa Azoty S.A.)

- Kingenta Ecological Engineering Group Co., Ltd.

- Sociedad Quimica y Minera de Chile S.A.

- Trade Corporation International (Rovensa Group)

- BASF SE

- Compass Minerals International, Inc.

- Fertiberia, S.A. (Triton Partners)

- Haifa Chemicals Ltd. (Haifa Group)

- ICL Group Ltd.

- K+S Aktiengesellschaft

- Nutrien Ltd.

- Timac Agro SAS (Groupe Roullier)

- Valagro S.p.A. (Syngenta Group Co., Ltd.)

- Verdesian Life Sciences, LLC (AEA Investors)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 Report offers

3 Executive Summary and Key Findings

4 Key Industries Trend

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision-agriculture led soil micronutrient mapping

- 4.6.2 European Union Common Agricultural Policy eco-scheme incentives

- 4.6.3 Rising demand for high-value horticulture crops

- 4.6.4 Shift toward chelated liquid and water-soluble formulations

- 4.6.5 Digital agronomic advisory platforms boosting adoption

- 4.6.6 Post-Brexit fast-track micronutrient registrations in the UK

- 4.7 Market Restraints

- 4.7.1 Metal-based raw-material price volatility

- 4.7.2 Stringent European Union limits on heavy-metal contaminants

- 4.7.3 Bio-fortification policies reducing external application

- 4.7.4 Competition from biological inoculants and biofertilizers

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 By Geography

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Italy

- 5.4.4 Netherlands

- 5.4.5 Russia

- 5.4.6 Spain

- 5.4.7 Ukraine

- 5.4.8 United Kingdom

- 5.4.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 Compo Expert GmbH (Grupa Azoty S.A.)

- 6.4.3 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.4 Sociedad Quimica y Minera de Chile S.A.

- 6.4.5 Trade Corporation International (Rovensa Group)

- 6.4.6 BASF SE

- 6.4.7 Compass Minerals International, Inc.

- 6.4.8 Fertiberia, S.A. (Triton Partners)

- 6.4.9 Haifa Chemicals Ltd. (Haifa Group)

- 6.4.10 ICL Group Ltd.

- 6.4.11 K+S Aktiengesellschaft

- 6.4.12 Nutrien Ltd.

- 6.4.13 Timac Agro SAS (Groupe Roullier)

- 6.4.14 Valagro S.p.A. (Syngenta Group Co., Ltd.)

- 6.4.15 Verdesian Life Sciences, LLC (AEA Investors)