|

시장보고서

상품코드

1636454

북미의 전기자동차용 전지 제조장치 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)North America Electric Vehicle Battery Manufacturing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

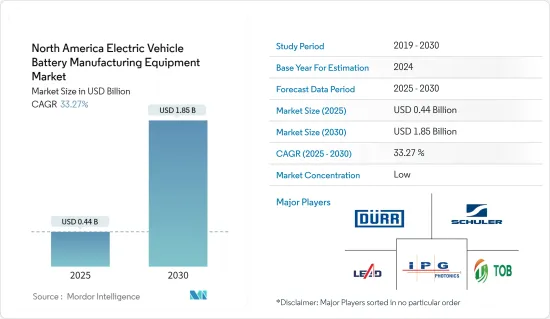

북미의 전기자동차용 전지 제조장치 시장 규모는 2025년에 4억 4,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 33.27%로, 2030년에는 18억 5,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 동지역의 전기자동차 보급 확대나 정부의 지원 시책과 규제 등의 요인이 예측 기간 중 북미 전기자동차 전지 제조장치 시장의 가장 큰 촉진요인 중 하나가 될 것으로 예상됩니다.

- 반면 아시아태평양과 같은 기존 전지 시장과의 경쟁은 예측 기간 동안 북미 전기자동차 전지 제조장치 시장에 위협으로 작용합니다.

- 북미 국가에서 전지 제조 공급망의 현지화에 대한 노력이 지속되면서 향후 시장에 여러가지 기회를 창출할 것으로 예상됩니다.

- 미국은 전지 제조 기반 설립을 위한 정부의 이니셔티브가 활발해지고 있으며 전기자동차 보급이 진행되고 있기 때문에 시장을 독점하고 예측 기간 동안 가장 높은 성장을 기록할 것으로 예상됩니다.

북미 전기자동차 전지 제조장치 시장 동향

슬릿 전극 제조의 대규모 성장

- 북미의 전기자동차용 전지 제조장치 시장에서는 슬릿 전극 제조 부문이 매우 중요한 역할을 하고 있습니다. 이 부문은 특히 전기자동차 수요가 급증하고 있기 때문에 정확성, 효율성 및 적응성이 중요합니다. 이 부문은 코팅 된 전극 재료를 최종 구조로 변환하고 전지 셀에 조립하는 일련의 복잡한 공정을 포함합니다. 전지 셀은 전기자동차 전지의 성능과 신뢰성에 매우 중요합니다.

- 운송 전동화를 추진하는 북미에서는 슬릿 공정으로 대형 롤 형태의 코팅 전극 재료를 폭이 좁은 스트립으로 절단합니다. 이 스트립은 다양한 전지 설계를 위한 정확한 사양을 충족해야 합니다. 양극은 알루미늄, 음극은 구리가 일반적이며, 활성 리튬 화합물이나 집전박 등의 섬세한 재료를 손상시키지 않기 위해서는 이 공정을 높은 정밀도로 실시하는 것이 가장 중요합니다.

- 2024년 1월 현재, National Renewable Energy Laboratory의 데이터에 의하면 북미 전극 및 셀 제조 시장의 큰 잠재력을 확인할 수 있습니다. 미국이 80개 시설과 66개 기업으로 1위이며, 캐나다가 11개 시설과 기업, 북미의 기타 중동 및 아프리카는 4개 시설과 2개 기업을 보유하고 있습니다.

- 이는 북미에서 전기자동차(EV)용 전지 제조 장비 시장의 활발한 성장을 뒷받침합니다. 다수 시설의 존재는 전기자동차 수요 증가에 대응하기 위해 필수 인프라가 확립되었음을 나타냅니다.

- 슬릿 공정 후 전극 제조 공정이 진행되며 여기서는 개별 스트립이 정확한 치수로 절단되어 조립 준비가 이루어집니다. 조립 준비는 전극 성능과 수명을 높이기 위한 탭 추가, 그리고 보호 코팅 및 처치를 포함합니다.

- 게다가 북미 시장에서는 기술 혁신과 지속가능성이 중시되어 슬릿 장치와 전극 제조장치의 진보가 추진되고 있습니다. 제조업체는 폐기물을 최소화하고 재료 재활용성을 높이는 방법을 적극적으로 모색하고 있으며, 수율을 높이면서 스크랩을 줄이고 전극 코팅 및 준비 단계에서 여분의 재료와 용매를 회수하고 재활용하는 시스템을 도입하는 것을 목표로합니다.

- 예를 들어, 2023년 9월, 오크리지 국립 연구소 엔지니어들은 획기적인 건전지 제조 공정을 도입했습니다. 이 기술 혁신은 종종 독성 용매에 의존하는 기존의 습식 슬러리 공정의 문제를 해결합니다. 이러한 의존은 제조 비용을 증가시킬 뿐만 아니라 건강과 환경에 대한 위험을 초래합니다. 오크리지의 무용제 공정은 보다 가볍고 내구성이 우수하며 사용 후에도 높은 에너지 저장 용량을 유지하는 전지를 생산합니다.

- 이러한 진보와 정밀도의 중시를 감안하면, 슬릿 전극 제조 부문은 향후 수년에 크게 성장할 것으로 예상됩니다.

시장을 독점하는 미국

- 미국 내 전기자동차 전지 제조장치 시장은 연방정부의 우대정책, 지방정부의 시책, 민간투자 등 산업의 성장을 뒷받침하는 다양한 요인에 의해 지원되고 있습니다. 예를 들어, 전지 제조에 투자하는 기업에는 다양한 세액 공제와 보조금이 준비되어 있어 신규 진입 장벽을 낮추고 기존 기업의 확대를 지원하고 있습니다.

- 예를 들어, 미국 정부는 2023년부터 인플레이션 감축법을 통해 세액 공제를 제공하고 있으며, 당파를 초월한 인프라법은 에너지 전환을 촉진하기 위해 1조 달러라는 엄청난 금액의 세액 공제를 할당하고 있습니다. 인플레이션 감축법에서는 전지 생산자는 제조 공제를 받을 수 있으며 전지 셀 생산에는 1킬로와트 당 35달러, 전지 모듈은 1킬로와트 당 10달러를 받을 수 있습니다. 또한, 기업은 전극 활성 물질 비용에 대해 10%의 환불을 청구할 수 있습니다. 특히, 기업은 이러한 세액 공제를 다른 납세자에게 양도하거나 판매할 수 있는 유연성이 있습니다.

- 게다가 전기차 공급망을 현지화하려는 강한 움직임으로 인해 자국 내 전지 제조 시설에 대한 투자가 증가하고 있습니다. 이러한 추세는 미국 정부의 엄격한 배기 가스 규제에 의해 더욱 강화되고 있으며, 자동차 제조업체가 보다 지속 가능한 전지 구동 차량으로 전환하도록 촉진하고 있습니다.

- National Renewable Energy Laboratory에 따르면 2024년 1월 현재 미국에는 전지 제조 장비 부문에서 사업을 진행하고 있는 기업이 64개 있으며, 65개 시설이 다양한 지역에 분포하고 있습니다. 이러한 견고한 인프라는 전기자동차 전지 제조 장비 시장의 성장을 뒷받침하고 있습니다.

- 기술 혁신은 미국 시장의 또 다른 기초이며, 많은 기업들이 전지 효율 개선, 비용 절감, 전지 생산 지속가능성 향상을 위한 선구적인 노력을 하고 있습니다. 연구 초점은 리튬 이온 기술의 진보뿐만 아니라 더 높은 에너지 밀도와 안전성 프로파일 개선을 보장하는 고체 전지와 같은 대체 화학 및 솔루션의 탐구에도 맞춰져있습니다.

- 따라서 미국은 예측 기간 동안 큰 성장을 이룰 것으로 예상됩니다.

북미 전기자동차 전지 제조장치 산업 개요

북미의 전기자동차 전지 제조 장비 시장은 양분화되어 있습니다. 동시장의 주요 기업(순서부동)은 Duerr AG, Schuler AG, IPG Photonics Corporation, Wuxi Lead Intelligent Equipment, Xiamen TOB New Energy Technology입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 촉진요인

- 전기자동차 보급 확대

- 정부의 지원성 규제와 시책

- 억제요인

- 기존 시장과의 경쟁

- 촉진요인

- 공급망 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협 제품 및 서비스

- 경쟁 기업간 경쟁 관계

- 투자 분석

제5장 시장 세분화

- 프로세스

- 혼합

- 코팅

- 캘린더링

- 슬릿 전극 가공

- 기타

- 전지

- 리튬 이온

- 납축전지

- 니켈 수소 전지

- 기타 전지

- 지역

- 미국

- 캐나다

- 기타 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Duerr AG

- Schuler AG

- Hitachi Ltd.

- Xiamen Tmax Battery Equipments Limited

- ACEY New Energy Technology

- IPG Photonics Corporation

- Wuxi Lead Intelligent Equipment Co Ltd

- ACEY New Energy Technology

- Xiamen Lith Machine Limited

- Xiamen TOB New Energy Technology Co., Ltd.

- 기타 유력 기업 목록

- 시장 순위/점유율(%) 분석

제7장 시장 기회와 앞으로의 동향

- 공급망 현지화

The North America Electric Vehicle Battery Manufacturing Equipment Market size is estimated at USD 0.44 billion in 2025, and is expected to reach USD 1.85 billion by 2030, at a CAGR of 33.27% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing adoption of electric vehicles in the region coupled with supportive government policies and regulations are expected to be among the most significant drivers for the North American Electric Vehicle Battery Manufacturing Equipment Market during the forecast period.

- On the other hand, established battery markets such as Asia Pacific are competing. This poses a threat to the North American Electric Vehicle Battery Manufacturing Equipment Market during the forecast period.

- Nevertheless, continued efforts to localize battery manufacturing supply chains in North American countries are expected to create several opportunities for the market in the future.

- United States is expected to dominate the market and will likely register the highest growth during the forecast period due to the government's rising efforts to establish battery manufacturing and the growing adoption of electric vehicles.

North America Electric Vehicle Battery Manufacturing Equipment Market Trends

Slitting and Electrode Making to Witness Significant Growth

- The slitting and electrode-making segment plays a pivotal role in North America's electric vehicle battery manufacturing equipment market. This segment underscores the importance of precision, efficiency, and adaptability, especially given the surging demand for electric vehicles. It involves a series of intricate processes that convert coated electrode materials into final structures, primed for assembly into battery cells. These cells are crucial for the performance and reliability of electric vehicle batteries.

- In North America, where the drive towards transport electrification is gaining momentum, the slitting process cuts large rolls of coated electrode material into narrower strips. These strips must meet precise specifications for various battery designs. Executing this process with high precision is paramount to avoid damaging delicate materials, including active lithium compounds and current collector foils, which are typically aluminum for cathodes and copper for anodes.

- As of January 2024, data from the National Renewable Energy Laboratory reveals a significant presence in North America's electrode and cell manufacturing landscape. The U.S. leads with 80 facilities and 66 companies, followed by Canada with 11 facilities and companies, and the rest of North America with four facilities and two companies.

- This underscores the vigorous growth of the electric vehicle (EV) battery manufacturing equipment market in North America. The multitude of facilities indicates a well-established infrastructure, crucial for meeting the rising demand for electric vehicles.

- After slitting, the electrode-making process commences. Here, individual strips are cut to precise dimensions and readied for assembly. This preparation may involve adding tabs and applying protective coatings or treatments to boost the electrode's performance and longevity.

- Furthermore, the North American market emphasizes innovation and sustainability, propelling advancements in slitting and electrode-making equipment. Manufacturers are actively seeking methods to minimize waste and bolster material recyclability. Innovations aim to enhance yield, reduce scrap, and implement systems for recovering and recycling excess materials or solvents from the electrode coating and preparation stages.

- For example, in September 2023, engineers at Oak Ridge National Laboratory introduced a groundbreaking dry battery manufacturing process. This innovation tackles the challenges of the traditional wet slurry method, which often depends on toxic solvents. Such reliance not only escalates manufacturing costs but also poses health and environmental risks. Oak Ridge's solvent-free process yields a battery that's lighter, more durable, and maintains a high energy storage capacity even after use.

- Given these advancements and the emphasis on precision, the slitting and electrode-making segment is poised for significant growth in the coming years.

United States to Dominate the Market

- In the United States, the electric vehicle battery manufacturing equipment market is supported by a confluence of factors, including federal incentives, local government policies, and private investments that collectively enhance the industry's growth. For example, various tax credits and grants are available to companies that invest in battery manufacturing, which lowers the entry barrier for new players and supports the expansion of existing companies.

- For instance, starting in 2023, the United States government is offering Tax Credits via the Inflation Reduction Act, and Bipartisan Infrastructure Law laws have allocated a staggering USD 1 trillion in tax credits to facilitate the energy transition. Under the Inflation Reduction Act, battery producers benefit from manufacturing credits, receiving USD 35 per kilowatt-hour for battery cell production and USD 10 per kilowatt-hour for battery modules. Additionally, companies can claim a 10% reimbursement on costs for electrode-active materials. Notably, businesses have the flexibility to transfer or sell these tax credits to other taxpayers.

- Additionally, there is a strong push towards localizing the electric vehicle supply chain, which has led to increased investments in battery manufacturing facilities across the country. This trend is further bolstered by the United States government's stringent emissions regulations, which encourage automotive manufacturers to shift towards more sustainable, battery-powered vehicles.

- According to the National Renewable Energy Laboratory, as of January 2024, the United States boasted 64 companies operating in the battery manufacturing equipment sector, with 65 facilities spread across various regions. This robust infrastructure drives the growth of the Electric Vehicle Battery Manufacturing Equipment Market.

- Technological innovation is another cornerstone of the United States market, with numerous companies engaged in pioneering work to improve battery efficiency, reduce costs, and enhance the sustainability of battery production. The focus is not only on advancing lithium-ion technology but also on exploring alternative chemistries and solutions, such as solid-state batteries, which promise higher energy densities and improved safety profiles.

- Therefore, the United States is expected to witness significant growth during the forecast period, as mentioned above.

North America Electric Vehicle Battery Manufacturing Equipment Industry Overview

The North America Electric Vehicle Battery Manufacturing Equipment Market is semi-fragmented. Some of the key players in this market (in no particular order) are Duerr AG, Schuler AG, IPG Photonics Corporation, Wuxi Lead Intelligent Equipment Co. Ltd., and Xiamen TOB New Energy Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Supportive Government Regulations and Policies

- 4.5.2 Restraints

- 4.5.2.1 Competition From Established Markets

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Process

- 5.1.1 Mixing

- 5.1.2 Coating

- 5.1.3 Calendaring

- 5.1.4 Slitting and Electrode Making

- 5.1.5 Other Process

- 5.2 Battery

- 5.2.1 Lithium-ion

- 5.2.2 Lead-Acid

- 5.2.3 Nickel Metal Hydride Battery

- 5.2.4 Other Batteries

- 5.3 Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Duerr AG

- 6.3.2 Schuler AG

- 6.3.3 Hitachi Ltd.

- 6.3.4 Xiamen Tmax Battery Equipments Limited

- 6.3.5 ACEY New Energy Technology

- 6.3.6 IPG Photonics Corporation

- 6.3.7 Wuxi Lead Intelligent Equipment Co Ltd

- 6.3.8 ACEY New Energy Technology

- 6.3.9 Xiamen Lith Machine Limited

- 6.3.10 Xiamen TOB New Energy Technology Co., Ltd.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Localization of Supply Chains