|

시장보고서

상품코드

1636482

미국의 전기자동차용 전지 제조장치 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)United States Electric Vehicle Battery Manufacturing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

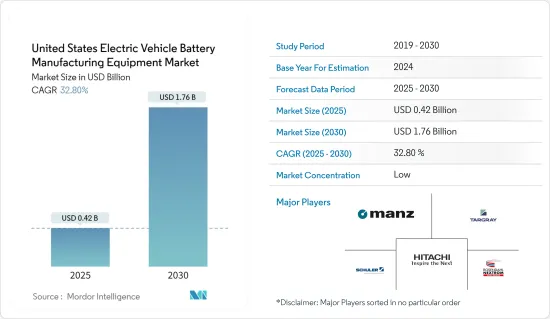

미국의 전기자동차용 전지 제조장치 시장 규모는 2025년에 4억 2,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 32.8%로, 2030년에는 17억 6,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 전지 제조를 위한 정부의 시책과 투자, 전지 원료(특히 리튬 이온)의 비용 저하가 예측 기간 시장을 견인할 것으로 보입니다.

- 반면 아시아태평양의 다른 기존 시장과의 경쟁이 향후 시장의 걸림돌이 될 것으로 예상됩니다.

- 미국의 전기자동차에 대한 장기적인 목표는 예측 기간 동안 큰 기회를 창출할 것으로 예상됩니다.

미국 전기자동차 전지 제조장치 시장 동향

리튬 이온 전지가 큰 점유율을 차지할 전망

- 리튬 이온 전지 제조장치는 리튬 이온 전지 제조에 특화된 전용 기계 및 공구로 구성됩니다. 미국에서 리튬 이온 전지 제조장치는 전지 셀, 모듈, 팩 생산에 필수적인 장비입니다. 미국은 전기자동차(EV) 시장과 에너지 저장 솔루션의 강화를 목표로 하여 전지의 자국 내 생산에 주력하고 있습니다.

- 게다가 자국 내 제조 장비 시장의 진보는 미국의 리튬 이온 전지 가격을 크게 낮추고 있습니다. 전기자동차 수요가 급증함에 따라 규모의 경제는 생산 비용 절감으로 이어졌습니다. 그 결과, 리튬 이온 전지 가격이 하락함에 따라 기업은 전기자동차 전지 제조에 대한 투자를 확대하고 있으며, 미국에서 리튬 이온 전지 제조 장비 수요를 더욱 촉진하고 있습니다.

- 2023년에는 리튬 이온 전지 팩의 가격은 전년보다 14% 하락해 139달러/kWh에 안정되었습니다. 이러한 가격 우위성뿐만 아니라 현재 진행중인 연구개발은 전기자동차용으로 보다 효과적인 리튬 전지 재료 개발을 목표로 하고 있으며, 이는 선진적 전지 제조장치의 필요성이 높아지고 있음을 시사하고 있습니다.

- 게다가 미국 내에서 리튬 광석이 새롭게 발견됨에 따라 전지 제조업체는 전기자동차용 리튬 전지의 생산 확대에 박차를 가하고 있습니다. 이러한 추세는 예측 가능한 미래에 전지 제조 장비 수요가 급증할 것을 시사합니다.

- 예를 들어, 2024년 6월, ExxonMobil과 세계 유수의 전기자동차 전지 개발 기업인 SK On이 양해각서를 체결했습니다. 이를 통해 ExxonMobil은 아칸소의 첫 프로젝트에서 최대 100,000톤의 MobilTM 리튬을 얻을 수 있습니다. 게다가 ExxonMobil은 이 리튬을 2030년까지 연간 약 100만대의 EV용 전지 생산에 사용하는 것을 목표로 하고 있습니다.

- 게다가 미국 정부는 2023년 11월 당파를 초월한 인프라법에 근거하여 첨단 전지와 재료의 생산 강화를 위해 약 35억 달러의 투자를 약속했습니다. 이러한 노력으로 자국 내 리튬 이온 전지 생산이 강화되어 향후 수년간 장비 시장에 혜택을 줄 것으로 보입니다.

- 이러한 개발로 인해 전지 부문은 조사 대상 시장에서 큰 점유율을 차지할 것으로 예상됩니다.

전지 제조를 위한 정부의 시책과 투자가 시장을 견인하는 전망

- 정부의 조치와 전지 제조에 대한 투자는 미국 EV 전지 제조 장비 시장의 중요한 촉진요인입니다. 조성금, 보조금, 세제 우대 정책 등 연방 및 주 정부의 이니셔티브는 전지 제조 설비의 개발과 확대를 장려하고 있습니다.

- 예를 들어, 미국 에너지부는 2024년 1월 EV 전지와 충전 시스템 연구개발을 추진하는 프로젝트에 대해 1억 3,100만 달러의 자금 제공을 발표했습니다. 이 자금 지원을 통해 EV 생태계는 기술 비용 절감, 전지 차량 주행 거리 연장, 안전하고 지속 가능한 자국 내 전지 공급망 구축을 실현합니다.

- 이러한 재정 지원은 첨단 설비에 투자하는 기업의 초기 비용을 낮추고 생산 확립과 규모 확대를 보다 현실화합니다. 에너지부(DOE)로부터의 자금제공 등 연구개발을 촉진하는 이러한 시책은 전지기술과 제조 공정의 혁신을 촉진합니다.

- 미국 내 전기자동차 판매량이 증가함에 따라 정부가 미국 내 전지 제조 장비에 대한 수요를 촉진하기 위한 조치를 추가로 내릴 것을 촉구할 것으로 예상됩니다. 국제에너지기구(International Energy Agency)에 따르면 2023년 미국의 EV차 총 판매량은 139만대로 2022년 99만대에서 증가하였습니다.

- 게다가 정부의 지원을 받아 전지 제조 기업은 새로운 EV 제조 공장의 개발에 투자하고 있으며, 이는 미국 내 EV 전지 제조장치 수요를 급증할 것으로 예상됩니다.

- 예를 들어 2023년 5월 SK와 현대차그룹은 조지아주 합작사업 계획을 승인했으며 SK가 미국 자동차 기술의 미래 형성에 깊이 관여하고 있음을 보여주었습니다. 50억 달러에 달하는 이번 투자로 조지아 주 바토 카운티에 EV용 전지 공장을 설립할 예정입니다.

- 이와 같이 최근 동향과 EV 판매 증가로 인한 정부의 시책과 전지 제조에 대한 투자가 시장을 견인할 것으로 예상됩니다.

미국 전기자동차 전지 제조 장비 산업 개요

미국의 전기자동차 전지 제조장치 시장은 양분화되어 있습니다. 동시장의 주요 기업(순서부동)에는 Manz AG, Schuler AG, Hitachi, Rosendahl Nextrom GmbH, Targray Technology International Inc 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 촉진요인

- 전지 제조를 위한 정부의 시책과 투자

- 전지 원료 비용 저하

- 억제요인

- 기존 시장과의 경쟁

- 촉진요인

- 공급망 분석

- PESTLE 분석

- 투자분석

제5장 시장 세분화

- 프로세스

- 혼합

- 코팅

- 캘린더링

- 슬릿 전극 가공

- 기타

- 전지

- 리튬 이온

- 납축전지

- 니켈 수소 전지

- 기타

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Manz AG

- Rosendahl Nextrom GmbH

- Schuler AG

- Hitachi Ltd

- Targray Technology International Inc

- Targray Technology International Inc

- Xiamen TOB New Energy Technology Co.,Ltd.

- DAIICHI JITSUGYO(AMERICA), INC.

- Sovema Group

- 기타 유력 기업 일람

- 시장 순위 분석

제7장 시장 기회와 앞으로의 동향

- 전기차의 장기 목표

The United States Electric Vehicle Battery Manufacturing Equipment Market size is estimated at USD 0.42 billion in 2025, and is expected to reach USD 1.76 billion by 2030, at a CAGR of 32.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, government policies and investments towards battery manufacturing, and a decline in the cost of battery raw materials, especially lithium-ion, are expected to drive the market in the forecast period.

- On the other hand, competition from other established markets in Asia-Pacific region is expected to hamper the market in the future.

- Nevertheless, long-term ambitious targets for electric vehicles in the United States are expected to create a significant opportunity in the forecast period.

United States Electric Vehicle Battery Manufacturing Equipment Market Trends

Lithium-ion Battery is Expected to Have a Major Share

- Lithium-ion battery manufacturing equipment comprises specialized machines and tools tailored for lithium-ion battery production. In the United States, this equipment is pivotal for producing battery cells, modules, and packs. The United States is intensifying its focus on domestic battery production, aiming to bolster the electric vehicle (EV) market and energy storage solutions.

- Moreover, advancements in the domestic manufacturing equipment market are significantly driving down lithium-ion battery prices in the United States. As the demand for electric vehicles surges, achieving economies of scale has led to reduced production costs. Consequently, with decreasing lithium-ion battery prices, companies are ramping up investments in EV battery manufacturing, further fueling the demand for lithium-ion battery manufacturing equipment in the United States.

- In 2023, lithium-ion battery pack prices dropped by 14% from the previous year, settling at USD139/kWh. Beyond these price advantages, ongoing research and development efforts aim to create more effective lithium battery materials for electric vehicles, underscoring the growing need for advanced battery manufacturing equipment.

- Furthermore, fresh discoveries of lithium ore within the United States are spurring battery manufacturers to ramp up production of lithium batteries for electric vehicles. Such ambitions signal a burgeoning demand for battery manufacturing equipment in the foreseeable future.

- For example, in June 2024, ExxonMobil and SK On, a leading global electric vehicle battery developer, signed a non-binding memorandum of understanding. This sets the stage for a potential multiyear offtake agreement, enabling ExxonMobil to acquire up to 100,000 metric tons of MobilTM Lithium from its debut project in Arkansas. Moreover, ExxonMobil targets this lithium for the production of approximately 1 million EV batteries annually by 2030.

- Additionally, in November 2023, the United States government, under the Bipartisan Infrastructure Law, committed an investment of around USD 3.5 billion to enhance the production of advanced batteries and their materials. Such initiatives are poised to bolster domestic lithium-ion battery production, subsequently benefiting the equipment market in the coming years.

- Given these developments, the segment is anticipated to command a substantial share in the market under study.

Government Policies and Investments Towards Battery Manufacturing is Expected to Drive the Market

- Government policy and investment in battery production are critical drivers of the U.S. EV battery manufacturing equipment market. Federal and state initiatives, such as grants, subsidies, and tax incentives, encourage the development and expansion of battery manufacturing facilities.

- For instance, in January 2024, the U.S. Department of Energy announced USD 131 million in funding for projects to advance research and development in EV batteries and charging systems. The funding will empower the EV ecosystem to lower technology costs, extend the driving range of battery vehicles, and establish a secure and sustainable domestic battery supply chain.

- These financial supports lower the initial costs for companies investing in advanced equipment, making it more feasible to establish and scale up production. Such policies promoting research and development, such as funding from the Department of Energy (DOE), spur innovation in battery technologies and manufacturing processes.

- Increasing electric vehicle sales in the country is expected to encourage the government to launch more policies that drive the demand for battery manufacturing equipment in the country. According to the International Energy Agency, in 2023, total EV car sales in the United States accounted for 1.39 million units, up from 0.99 million units in 2022.

- Further, with government support, battery manufacturing companies are investing in developing new EV manufacturing plants, which is expected to surge the demand for EV battery manufacturing equipment in the country.

- For instance, in May 2023, SK and Hyundai Motor Group greenlit plans for a joint venture in Georgia, signaling SK's deepening involvement in shaping the future of U.S. automotive technology. The venture, set to invest USD 5 billion, will establish an EV battery cell plant in Bartow County, Georgia.

- Thus, owing to the recent developments and increasing EV sales, government policies and investments in battery manufacturing are expected to drive the Market.

United States Electric Vehicle Battery Manufacturing Equipment Industry Overview

The United States electric vehicle battery manufacturing equipment market is semi-fragmented. Some of the major players in the market (in no particular order) include Manz AG, Schuler AG, Hitachi Ltd, Rosendahl Nextrom GmbH, and Targray Technology International Inc, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments Towards Battery Manufacturing

- 4.5.1.2 Decline in Cost of Battery Raw Materials

- 4.5.2 Restraints

- 4.5.2.1 Competition from Established Market

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Process

- 5.1.1 Mixing

- 5.1.2 Coating

- 5.1.3 Calendering

- 5.1.4 Slitting and Electrode Making

- 5.1.5 Other Process

- 5.2 Battery

- 5.2.1 Lithium-ion

- 5.2.2 Lead-Acid

- 5.2.3 Nickel Metal Hydride Battery

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1

Manz AG

- 6.3.2 Rosendahl Nextrom GmbH

- 6.3.3 Schuler AG

- 6.3.4 Hitachi Ltd

- 6.3.5 Targray Technology International Inc

- 6.3.6 Xiamen Acey New Energy Technology Co

.,Ltd

- 6.3.7 Xiamen TOB New Energy Technology Co.,Ltd.

- 6.3.8 DAIICHI JITSUGYO (AMERICA), INC.

- 6.3.9 Sovema Group

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term Ambitious Targets for Electric Vehicles