|

시장보고서

상품코드

1636471

아시아태평양의 전기자동차 배터리 제조 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Asia Pacific Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

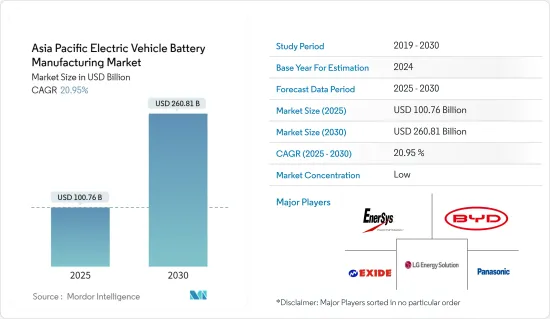

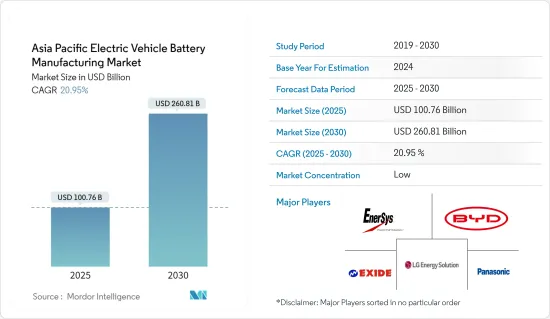

아시아태평양의 전기자동차 배터리 제조 시장 규모는 2025년 1,007억 6,000만 달러, 2030년 2,608억 1,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 20.95%에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 전지 생산 능력 증대를 위한 투자 증가와 전지 원료 비용의 저하가 예측 기간 동안 전기자동차용 전지 제조 수요를 견인할 것으로 예상됩니다.

- 한편, 신뢰성이 높기 때문에 기존 자동차의 판매가 증가하고 있으며 예측 기간 동안 전기자동차 배터리 시장에 부정적인 영향을 미칠 것으로 예상됩니다.

- 그럼에도 불구하고 생산 능력 확대, 기술 진보 강화, 비용 절감 등 전기자동차에 대한 장기적인 야심적 목표는 가까운 미래에 전기자동차 배터리 제조 시장에 큰 기회를 가져올 것으로 예상됩니다.

- 예측기간 동안 아시아태평양의 전기자동차 배터리 제조시장에서는 전기차 보급 대수 증가로 인도가 가장 급성장하고 있는 지역입니다.

아시아태평양의 전기자동차 배터리 제조 시장 동향

리튬 이온 배터리 유형이 시장을 독점

- 리튬이온(Li-ion) 배터리는 전기자동차(EV) 시장에 혁명을 일으켜 배터리 제조 기술 혁신을 촉진했습니다. 고에너지 밀도, 긴 사이클 수명, 급속 충전 등 리튬 이온 배터리의 주요 특성으로 오늘날의 EV에는 리튬 이온 배터리가 선택되고 있습니다.

- 또한, 리튬 이온 이차 전지는 용량 중량비가 우수하기 때문에 다른 기술을 능가하고 있습니다. 리튬이온 이차전지는 대체품보다 비싼 경향이 있지만, 시장의 대기업은 R&D 투자를 늘리고 생산을 확대하고 있기 때문에 경쟁이 격화되고 가격 인하로 이어지고 있습니다.

- EV와 배터리 에너지 저장 시스템(BESS)용 배터리 팩의 평균 가격이 상승하고 있음에도 불구하고 2023년 배터리 가격은 139달러/kWh로 13%의 대폭 하락을 보였습니다. 예측에 따르면 이 하락 기조는 향후에도 계속되어 2025년에는 113달러/kWh에 달하고, 2030년에는 80달러/kWh까지 하락할 것으로 예상됩니다.

- 아시아태평양에서는 각국 정부가 전기자동차(EV)의 보급을 촉진하고 리튬 이온 배터리의 생산 확대를 촉진하기 위한 정책과 인센티브를 실시했습니다. 이들 정부는 연구개발을 우선으로 하여 코발트와 같은 고가이고 희귀한 재료의 대용품으로서 비용효과가 높고 입수가능한 재료를 확인하려고 하고 있습니다. 이 전략은 제조 비용을 줄일 뿐만 아니라 보다 지속 가능한 공급망을 보장합니다.

- 예를 들어 중국은 2024년 5월 하이브리드 모델을 포함한 전기자동차(EV)용 차세대 배터리 기술 개척에 약 60억 위안(8억 4,500만 달러)을 투자하게 되었습니다. 최첨단 기술인 ASSB는 기존의 리튬 이온 배터리(LIB)를 고체 부품으로 강화합니다. 기존 배터리에 비해 발화나 폭발의 위험성이 낮고 에너지 밀도도 우수합니다. 이러한 기술 혁신은 앞으로 수년간 선진적인 리튬이온전지 수요를 끌어올려 이 지역의 EV용 전지 제조에 긍정적인 영향을 미칠 전망입니다.

- 게다가 리튬 이온 배터리 수요 급증은 기가팩토리라고 불리는 대규모 생산 시설의 설립을 뒷받침하고 있습니다. 이 전문 시설은 배터리 셀을 대량 생산하도록 설계되었으며 전기자동차(EV) 증가하는 수요를 확실하게 충족시킬 수 있습니다. 이 지역의 주요 기업은 리튬 이온 배터리의 제조를 강화하기 위해 여러 프로젝트를 시작하고 있습니다.

- 예를 들어 BMW는 2024년 2월 태국 라용에 새로운 배터리 공장을 건설할 계획을 발표했습니다. 동사는 태국을 아시아태평양의 EV용 배터리의 주요 수출 거점으로 삼아 이 지역의 리튬 이온 배터리 공급을 더욱 강화할 계획입니다. 이와 같은 대처에 의해 이 나라의 전지 생산은 향후 수년에 가속하게 됩니다.

- 그 결과 이러한 노력이 리튬 이온 전지의 생산을 확대하고 예측 기간 중에 EV용 전지의 생산 능력을 대폭 높일 수 있습니다.

현저한 성장을 이루는 인도

- 인도의 전기자동차(EV) 배터리 제조 시장은 이 나라가 보다 친환경적인 이동성 솔루션을 채택함에 따라 빠르게 확대되고 있습니다. 이 성장의 원동력이 되고 있는 것은 정부의 이니셔티브, 전기차에 대한 수요의 급증, 국내외 기업에 의한 다액의 투자입니다.

- 인도가 청정 에너지로 중심을 옮기는 동안 전기자동차에 대한 중점 투자는 많은 기업들에게 가장 중요한 과제가 되고 있습니다. 이 지역에서 EV 판매가 급증하고 있습니다. 예를 들어 국제에너지기구(IEA)의 보고에 따르면 2023년 전기차 판매량은 8만 2,000대에 달하고, 2022년부터 70.8% 증가, 2019년부터는 119배라는 경이적인 성장을 보였습니다. 정부가 최근 여러 프로젝트와 이니셔티브를 시작함으로써 EV 판매는 더욱 크게 성장하는 태세가 갖추어지고 있습니다.

- 인도에서는 국내 기업과 국제 기업 모두에서 전기자동차 배터리 제조에 대한 투자가 잇따르고 있습니다. 이러한 투자는 국가의 전기자동차 인프라를 강화하고 화석연료에 대한 의존도를 줄이고 지속가능한 운송을 지지하는 것을 목표로 합니다. 정부의 지원 정책과 장려책에 힘입어 인도는 세계 EV 시장에서 뛰어난 지위를 구축하고 있습니다.

- 예를 들어, 2024년 7월, Ola Electric은 인도의 타밀 나두에 있는 기가팩토리의 첫 번째 단계에 1억 달러를 투자할 것이라고 발표했습니다. 이 시설에서는 국산 리튬 이온 배터리를 생산합니다. 이 회사는 내년 초까지 전기자동차 배터리 셀을 현재 한국과 중국에서 수입에서 자체 제조로 전환할 계획입니다. 이러한 움직임은 향후 몇 년동안 전국적으로 배터리 생산을 강화할 것입니다.

- 또한 인도 정부는 전기자동차(EV)의 보급을 촉진하고 현지에서 배터리 제조를 활성화하기 위한 이니셔티브를 전개하고 있습니다. 이러한 조치에는 EV 구매자에 대한 보조금, 제조업체에 대한 감세, 충전 인프라에 대한 투자 강화 등이 포함됩니다.

- 그 일례로 인도 정부는 2023년에 2030년까지 자가용차 판매의 30%, 상용차의 70%, 이륜차와 삼륜차의 80%를 EV로 바꾸는 야심적인 목표를 내걸었습니다. 또한 정부는 1kWh 당 10,000 인도루피(120달러)부터 15,000 인도루피(180미국달러)까지 보조금 우대조치를 제공합니다. 이러한 대처는 EV의 생산과 수요를 끌어올릴 뿐만 아니라 예측기간 동안 이 지역에서의 배터리 제조의 필요성을 높입니다.

- 그 결과, 이러한 프로젝트와 이니셔티브는 EV 수요를 강화하고 향후 수년간 전기자동차 배터리 제조의 요구를 크게 높일 것입니다.

아시아태평양의 전기자동차 배터리 제조 업계 개요

아시아태평양의 전기자동차 배터리 제조 시장은 반 파편화되었습니다. 주요 기업(순부동)에는 BYD Company Ltd, LG Energy Solution, Exide Industries Ltd, EnerSys, Panasonic Holdings Corporation 등이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모 및 수요 예측(단위: 달러)

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 배터리 생산 능력 증강을 위한 투자

- 전지 원재료 비용의 저하

- 억제요인

- 기존 자동차의 높은 신뢰성

- 성장 촉진요인

- 공급망 분석

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협 제품 및 서비스

- 경쟁 기업간 경쟁 관계

- 투자분석

제5장 시장 세분화

- 배터리별

- 리튬 이온

- 납축

- 니켈 수소

- 기타

- 전지 형상별

- 각형

- 가방형

- 원통형

- 차량별

- 승용차

- 상용차

- 기타

- 추진별

- 배터리 전기자동차

- 하이브리드 전기자동차

- 플러그인 하이브리드 전기자동차

- 지역별

- 중국

- 인도

- 호주

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- BYD Co. Ltd

- Panasonic Corporation

- LG Energy Solution

- EnerSys

- Exide Industries

- Contemporary Amperex Technology Co. Limited

- Tianjin Lishen Battery Joint-Stock Co., Ltd.

- Samsung SDI

- SK Innovation Co., Ltd.

- Envision AESC

- Gotion High tech Co Ltd

- 기타 유명 기업 일람

- 시장 랭킹 분석

제7장 시장 기회와 앞으로의 동향

- 전기자동차의 장기적인 야심적 목표

The Asia Pacific Electric Vehicle Battery Manufacturing Market size is estimated at USD 100.76 billion in 2025, and is expected to reach USD 260.81 billion by 2030, at a CAGR of 20.95% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, rising investments to enhance the battery production capacity and the decline in the cost of battery raw materials are expected to drive the demand for electric vehicle battery manufacturing during the forecast period.

- On the other hand, increasing sales of conventional vehicles due to their high reliability is expected to have a negative impact on the EV battery market during the forecast period.

- Nevertheless, the long-term ambitious targets for electric vehicles, such as scaling up production capacity, enhancing technological advancements, and reducing costs, are expected to create significant opportunities for the electric vehicle battery manufacturing market in the near future.

- India is the fastest-growing region in Asia Pacific's electric vehicle battery manufacturing market during the forecast period due to the rising electric vehicle adoption.

Asia Pacific Electric Vehicle Battery Manufacturing Market Trends

Lithium-Ion Battery Type Dominate the Market

- Lithium-ion (Li-ion) batteries have revolutionized the electric vehicle (EV) market, driving innovations in battery production. Their key attributes, such as high energy density, long cycle life, and swift charging, make them the preferred choice for today's EVs.

- Moreover, lithium-ion rechargeable batteries surpass other technologies due to their excellent capacity-to-weight ratio. Although they tend to be more expensive than alternatives, major players in the market are boosting R&D investments and ramping up production, heightening competition and leading to price reductions.

- Despite rising average battery pack prices for EVs and battery energy storage systems (BESS), 2023 witnessed a significant drop in battery prices to USD 139/kWh, a 13% decline. Projections suggest this downward trajectory will persist, with prices anticipated to reach USD 113/kWh by 2025 and further plummet to USD 80/kWh by 2030, driven by relentless technological and manufacturing progress.

- In the Asia Pacific region, governments are implementing policies and incentives to promote electric vehicle (EV) adoption and stimulate Lithium-ion battery production growth. By prioritizing research and development, these governments seek to pinpoint cost-effective and readily available materials as substitutes for more expensive and scarce ones, such as cobalt. This strategy not only curtails manufacturing costs but also ensures a more sustainable supply chain.

- For example, in May 2024, China is set to invest approximately 6 billion yuan (USD 845 million) into pioneering next-generation battery technology for electric vehicles (EVs), encompassing hybrid models. ASSBs, a cutting-edge technology, enhance traditional lithium-ion batteries (LIBs) with solid components. They boast a reduced risk of fire or explosion compared to conventional batteries and offer superior energy density. Such innovations are poised to boost the demand for advanced lithium-ion batteries in the coming years, positively influencing EV battery manufacturing in the region.

- Furthermore, the surging demand for Li-ion batteries has catalyzed the establishment of large-scale production facilities, dubbed Gigafactories. These specialized facilities are engineered to produce battery cells en masse, ensuring they meet the escalating demand from electric vehicles (EVs). Major companies in the region are launching multiple projects to strengthen their lithium-ion battery manufacturing, anticipating a notable uptick in EV battery demand soon.

- For instance, in February 2024, BMW unveiled plans for a new battery factory in Rayong, Thailand, aiming to bolster the nation's battery supply chains. The company envisions Thailand as its primary export hub for EV batteries throughout the Asia Pacific, further strengthening the region's lithium-ion battery supply. Such initiatives are set to accelerate the country's battery production in the upcoming years.

- Consequently, these endeavors are poised to amplify lithium-ion battery production and substantially boost EV battery manufacturing capacity in the forecast period.

India to Witness Significant Growth

- India's electric vehicle (EV) battery manufacturing market is rapidly expanding as the nation embraces greener mobility solutions. This growth is fueled by government initiatives, a surging demand for electric vehicles, and substantial investments from both domestic and international players.

- As India pivots towards clean energy, the emphasis on electric vehicles has become paramount for numerous companies. EV sales in the region have skyrocketed. For instance, the International Energy Agency (IEA) reported that in 2023, electric vehicle sales reached 82,000 units, marking a 70.8% increase from 2022 and a staggering 119-fold jump since 2019. With the government recently launching multiple projects and initiatives, EV sales are poised for further significant growth.

- India has seen a wave of investments in EV battery manufacturing, both from domestic entities and international firms. These investments aim to strengthen the nation's electric vehicle infrastructure, lessen reliance on fossil fuels, and champion sustainable transportation. Bolstered by supportive government policies and incentives, India is carving out a prominent position in the global EV landscape.

- For example, in July 2024, Ola Electric unveiled a USD 100 million investment for the first phase of its gigafactory in Tamil Nadu, India. This facility will produce indigenous lithium-ion batteries. The company plans to transition to its battery cells for its electric vehicles by early next year, moving away from current imports from Korea and China. Such moves are set to ramp up battery production nationwide in the coming years.

- Additionally, the Indian government has rolled out initiatives to promote electric vehicle (EV) adoption and stimulate local battery manufacturing. These measures encompass subsidies for EV purchasers, tax breaks for manufacturers, and bolstered investments in charging infrastructure.

- As an illustration, the Indian government, in 2023, set ambitious targets: by 2030, they aim for EVs to constitute 30% of private car sales, 70% of commercial vehicles, and 80% of two and three-wheelers. Furthermore, the government is offering subsidy incentives ranging from INR 10,000 per kWh (USD 120) to INR 15,000 per kWh (USD 180). Such initiatives are poised to not only boost EV production and demand but also amplify the need for battery manufacturing in the region during the forecast period.

- Consequently, these projects and initiatives are set to bolster EV demand and, in turn, significantly elevate the need for EV battery manufacturing in the coming years.

Asia Pacific Electric Vehicle Battery Manufacturing Industry Overview

Asia Pacific's electric vehicle battery manufacturing market is semi-fragmented. Some of the key players (not in particular order) are BYD Company Ltd, LG Energy Solution, Exide Industries Ltd, EnerSys, and Panasonic Holdings Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Investments to Enhance the battery production capacity

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 High reliability on Conventional Vehicle

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

- 5.5 Geography

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Australia

- 5.5.4 Malaysia

- 5.5.5 Thailand

- 5.5.6 Indonesia

- 5.5.7 Vietnam

- 5.5.8 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Panasonic Corporation

- 6.3.3 LG Energy Solution

- 6.3.4 EnerSys

- 6.3.5 Exide Industries

- 6.3.6 Contemporary Amperex Technology Co. Limited

- 6.3.7 Tianjin Lishen Battery Joint-Stock Co., Ltd.

- 6.3.8 Samsung SDI

- 6.3.9 SK Innovation Co., Ltd.

- 6.3.10 Envision AESC

- 6.3.11 Gotion High tech Co Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles