|

시장보고서

상품코드

2063350

중국의 화학제품 창고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

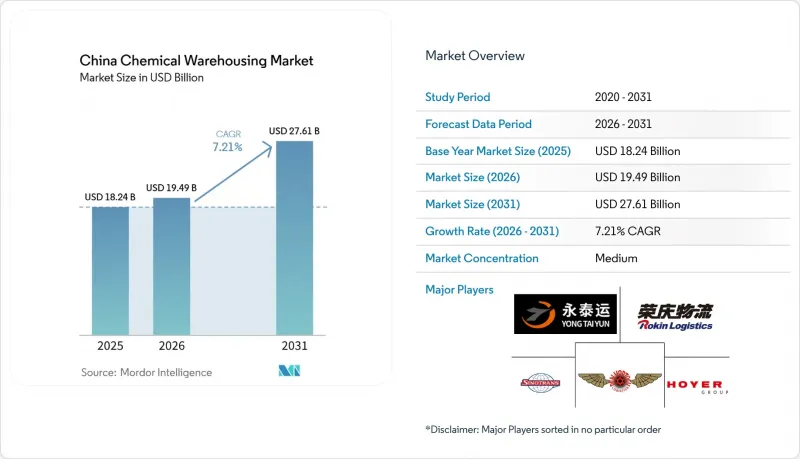

Mordor Intelligence에 의하면, 중국의 화학제품 창고 시장 규모는 2025년에 182억 4,000만 달러로 평가되었고, 2026년에 194억 9,000만 달러로 추정되고, 2031년까지 276억 1,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 7.21%로 성장할 전망입니다.

본 보고서는 창고 유형별(일반 창고, 특수 화학제품 창고, 위험물(HAZMAT) 창고 등), 화학 물질 유형별(인화성 액체, 부식성 물질, 독성 물질 등), 그리고 최종 사용자 산업별(기초 화학제품 제조, 특수 화학제품 제조 등)로 분류되어 있습니다. 시장 전망은 금액 기준(10억 달러)으로 제시되어 있습니다.

중국의 화학제품 창고 시장 동향 및 인사이트

화학 생산 거점의 급속한 확대

중국의 석유화학 및 화학 부문은 2025-2026년 안정적 성장 계획에 따라, 고부가가치 폴리올레핀, 전자 화학제품, 신에너지 원료에 중점을 두고 2026년까지 연평균 5%를 상회하는 부가가치 성장을 달성할 전망입니다. 대규모 프로젝트를 통해 생산 능력이 지속적으로 확대됨에 따라, 더 엄격한 보관 요건을 갖춘 가연성 및 유독 물질 전용 창고가 유치되고 있습니다. 4억 7,500만 달러 규모의 우시 거점을 포함한 생명과학 및 특수 화학 플랫폼에 대한 외국인 직접 투자는 GDP 기준에 부합하는 보관 및 유통 사업에 더욱 탄력을 불어넣고 있습니다. 비활성 분위기 하에서 오염 없는 보관이 필요한 전자 등급 용매 및 엔지니어링 소재의 취급량이 증가함에 따라, 중국의 화학제품 창고 시장이 그 혜택을 누리고 있습니다. 이러한 업스트림 공정으로의 전환을 통해 체류 시간이 단축되고 자동화의 가치가 높아짐에 따라, 인증 사업자의 가동률이 향상되고 이익률이 안정화되고 있습니다.

엄격한 화학물질 안전 규제

2026년 5월 1일부터 시행되는 '위험화학물질안전법'은 127개 조항으로 구성된 체계를 마련하여, 고독성 물질 및 중대 위험 물질에 대해 2인 이상으로 구성된 인원이 수령 및 보관하도록 의무화하고, 관련 기록을 최소 3년간 보관하도록 규정하고 있습니다. 2025년 11월 1일에 시행된 GB 45673-2025는 고위험 공정에서 전 공정의 자동화를 의무화하고, 지속적인 모니터링 및 안전 계장 시스템의 업그레이드를 규정하고 있습니다. 창고에서는 인가 취득 및 감사 통과를 위해 IoT 센서, 규제 준수 스프링클러, 정부 기관과 연동되는 제어 시스템을 도입하고 있습니다. 개보수 자금이 부족한 소규모 시설들은 통합하거나 철수하는 것 중 하나를 선택하고 있으며, 이로 인해 규정 준수 체계가 완벽한 인증 공원이나 통합 플랫폼에 대한 수요가 증가하고 있습니다. 2026년에 규제 집행이 강화됨에 따라, 중국의 화학물질 창고 시장은 규모는 줄어들겠지만, 더욱 자동화되고 추적 가능한 시설로 전환되고 있습니다.

유해 물질에 대한 제한적인 토지 이용 정책

'위험화학물질안전법'은 유해물질의 저장 시설과 영향을 받기 쉬운 수용지 사이에 소정의 안전 거리를 의무화하고 있으며, 신규 프로젝트를 정기적인 심사를 받는 인가된 화학 공단 내로 유도하고 있습니다. 새로운 오염 물질과 관련된 환경 영향 규제로 인해 심사가 강화되었으며, 생태학적 구역 설정 및 산업단지 차원의 환경영향 평가(EIA)와의 일관성이 요구되고 있습니다. 이러한 규제로 인해 적합한 토지가 줄어들고 승인까지 걸리는 기간이 길어지면서, 프로젝트는 해안 허브에 비해 교통 및 응급 서비스가 부족한 지역으로 밀려나고 있습니다. 중국의 화학제품 창고 시장에서는 2026년에 입지 제약과 완충 구역이 확대됨에 따라 톤당 자본 집약도가 높아지고 있습니다. 개발업체들은 승인 절차가 보다 예측 가능하고, 안전 대책 및 비상 대응 인프라가 갖춰진 지정 공단을 우선적으로 선정함으로써 이러한 과제에 대처하고 있습니다.

부문별 분석

2025년, 중국의 화학제품 창고 시장에서 특수 화학제품 창고가 36.42%라는 가장 높은 시장 점유율을 차지했습니다. 이는 고객들이 분리 보관 및 오염 관리가 필요한 정밀 화학제품이나 전자 화학제품으로 전환했기 때문입니다. 이러한 시설에서는 산소에 민감한 화합물에 대해 불활성 가스를 이용한 대기 제어, 흡습성 물질에 대한 습도 관리, 그리고 반도체 및 바이오의약품의 보관 이력 관리 요건을 충족하기 위해 RFID를 활용한 로트 추적이 이루어지고 있습니다. 온도 관리형 화학제품 창고 시장은 가장 빠르게 성장하고 있으며, 더욱 엄격해진 GDP(보관 및 배송 기준) 규제와 API(원료의약품) 및 특수 중간체의 콜드체인 물류 증가를 배경으로, 2031년까지 연평균 성장률(CAGR)이 8.62%를 나타낼 것으로 전망됩니다. 이를 통해 규정 준수 중심의 차별화가 강화되고 있습니다. 일반 화학제품 창고는 무결성 위험이 적은 안정적인 벌크 제품을 계속 취급하고 있지만, 화주들이 민감한 품목에 대해서는 책임 보호를 우선시하는 경향이 있어 이익률에 대한 압박이 커지고 있습니다. 중국의 화학제품 창고 시장에서는 규제 강화 속에서 특수 인프라와 디지털 통합을 결합하여 자산 회전율과 서비스 품질을 향상시키는 사업자들이 우위를 점하고 있습니다.

이 부문의 성장은 2026년의 기술 도입 및 규제 대응 진척 상황에 따라 달라집니다. 가연성, 부식성, 독성 물질을 취급하는 위험물 창고에서는 GB 규격 및 '2인 관리'와 '실시간 추적'에 관한 법적 요건을 준수하는 방폭 시스템 및 자동 소화 시스템으로의 업그레이드가 진행되고 있습니다. 사업자들은 슬롯 배정과 노동 효율을 개선하기 위해 디지털 트윈과 AI를 활용한 스케줄링 시스템을 시범 도입하고 있으며, 규정 준수 비용 증가에도 불구하고 생산성 향상으로 인해 이익률을 유지하고 있는 것으로 보고되고 있습니다. 중국의 화학제품 창고 업계는 2026년을 목표로 인가 확보 및 정부 플랫폼과의 상호 운용성을 실현하기 위해 표준화된 자동화와 통합 모니터링으로 전환하고 있습니다. 중국의 화학제품 창고 시장은 전문 분야에 대한 대응 능력, GDP(적정 보관 기준) 준수 현황, 그리고 고객의 위험을 줄여주는 신속한 감사 측면에서 계속해서 차별화를 꾀하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the china chemical warehousing market size is projected to be USD 18.24 billion in 2025, USD 19.49 billion in 2026, and reach USD 27.61 billion by 2031, growing at a CAGR of 7.21% from 2026 to 2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and More), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, and More), and by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

China Chemical Warehousing Market Trends and Insights

Rapid Expansion of Chemical Manufacturing Base

China's petrochemical and chemical sector is set to deliver value-added growth above 5% annually through 2026, with emphasis on high-end polyolefins, electronic chemicals, and new-energy feedstocks under the 2025 to 2026 stable growth plan. Large-scale programs continue to add capacity and draw in specialized warehousing for flammable and toxic materials with tighter custody needs. Foreign direct investment in life sciences and specialty platforms, including the USD 475 million Wuxi site, adds momentum to GDP-compliant storage and distribution. The China chemical warehousing market benefits as throughput rises for electronic-grade solvents and engineered materials that require inert-atmosphere, contamination-free storage. This upstream shift compresses dwell times and raises the value of automation, raising utilization and stabilizing margins for certified operators.

Stringent Chemical Safety Regulations

The Dangerous Chemicals Safety Law, effective May 1, 2026, sets a 127-article framework that enforces dual-person receipt and dual-person custody for highly toxic and major-hazard materials, with records kept for at least three years. The GB 45673-2025, which took effect on November 1, 2025, mandates full-process automation for high-risk processes and upgrades continuous monitoring and safety instrumentation. Warehouses are adding IoT sensors, compliant sprinklers, and government-interconnected control systems to meet approvals and pass audits. Smaller facilities without the capital to retrofit are either consolidating or exiting, which tilts demand to certified parks and integrated platforms with high compliance readiness. The Chinese chemical warehousing market shifts toward fewer but more automated and traceable sites as enforcement intensifies in 2026.

Restrictive Land Use Policies for Hazardous Materials

The Dangerous Chemicals Safety Law requires prescribed safety distances between hazardous storage and sensitive receptors and pushes new projects into approved chemical parks that undergo periodic reviews. Environmental impact rules linked to new pollutants strengthen screening and alignment with ecological zoning and park-level EIAs. These layers reduce eligible land and prolong approvals, sending projects to zones where transport and emergency services lag coastal hubs. The Chinese chemical warehousing market sees higher capital intensity per tonne as siting constraints and buffer areas expand in 2026. Developers navigate this by prioritizing designated parks with built-in safety and response infrastructure where approvals are more predictable.

Other drivers and restraints analyzed in the detailed report include:

- Belt and Road Initiative (BRI) Logistics Growth

- Growth in the Specialty and Fine Chemicals Sector

- High Compliance and Infrastructure Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty chemical warehouses held the largest market share of 36.42% of the China chemical warehousing market in 2025, as customers shifted to fine and electronic chemicals that require segregation and contamination control. These sites use inert-gas blanketing for oxygen-sensitive compounds, controlled humidity for hygroscopic materials, and batch genealogy tracked with RFID to meet chain-of-custody needs in semiconductors and biologics. Temperature-controlled chemical warehouses are growing the fastest, with a CAGR of 8.62% through 2031 under stricter GDP rules and rising cold-chain flows of APIs and specialty intermediates, which strengthens compliance-led differentiation. General chemical warehouses continue to serve stable bulk products with fewer integrity risks, although margin pressure is rising as shippers prioritize liability protection in sensitive categories. The Chinese chemical warehousing market favors operators that blend specialty infrastructure and digital orchestration to raise asset turns and service quality under tighter enforcement.

Growth within this segmentation tracks technology deployment and regulatory readiness in 2026. HAZMAT warehouses that manage flammables, corrosives, and toxics are upgrading to explosion-proof systems and automated suppression aligned to GB and legal requirements on dual-person custody and real-time tracking. Operators are piloting digital twins and AI-driven scheduling to improve slotting and labor efficiency, reporting productivity gains that defend margins despite higher compliance costs. The Chinese chemical warehousing industry is moving to standardized automation and integrated monitoring to ensure approvals and to interoperate with government platforms in 2026. The Chinese chemical warehousing market continues to differentiate on specialty readiness, GDP performance, and audit velocity that reduces customer risk.

List of Companies Covered in this Report:

- Sinotrans Ltd.

- Yongtaiyun Chemical Logistics

- Rokin Logistics

- Den Hartogh Logistics

- Hoyer Group

- Milkyway Intelligent Supply Chain

- COSCO Shipping Group (COSCO Shipping Chemical)

- Sumisho Global Logistics (China) Co.,Ltd

- Bertschi

- Sunward logistics co. ltd

- SF Express

- Kerry Logistics Network

- BDP International

- Rhenus Logistics

- DHL Group

- CEVA Logistics

- Broekman Logistics

- Yusen Logistics

- Odyssey Logistics and Technology Corporation

- DSV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Chemical Manufacturing Base

- 4.2.2 Stringent Chemical Safety Regulations

- 4.2.3 Belt and Road Initiative (BRI) Logistics Growth

- 4.2.4 Growth in Specialty and Fine Chemicals Sector

- 4.2.5 Yangtze River Economic Belt Development

- 4.2.6 Smart Warehousing Technology Integration

- 4.3 Market Restraints

- 4.3.1 Restrictive Land Use Policies for Hazardous Materials

- 4.3.2 High Compliance and Infrastructure Costs

- 4.3.3 Frequent Regulatory Changes and Enforcement

- 4.3.4 Chemical Industry Relocation Pressures

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals and Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings and Adhesives

- 5.3.6 Food and Feed Additives

- 5.3.7 Oil and Gas / Petrochemicals

- 5.3.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Sinotrans Ltd.

- 6.4.2 Yongtaiyun Chemical Logistics

- 6.4.3 Rokin Logistics

- 6.4.4 Den Hartogh Logistics

- 6.4.5 Hoyer Group

- 6.4.6 Milkyway Intelligent Supply Chain

- 6.4.7 COSCO Shipping Group (COSCO Shipping Chemical)

- 6.4.8 Sumisho Global Logistics (China) Co.,Ltd

- 6.4.9 Bertschi

- 6.4.10 Sunward logistics co. ltd

- 6.4.11 SF Express

- 6.4.12 Kerry Logistics Network

- 6.4.13 BDP International

- 6.4.14 Rhenus Logistics

- 6.4.15 DHL Group

- 6.4.16 CEVA Logistics

- 6.4.17 Broekman Logistics

- 6.4.18 Yusen Logistics

- 6.4.19 Odyssey Logistics and Technology Corporation

- 6.4.20 DSV

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment