|

시장보고서

상품코드

2063354

인도의 화학제품 창고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

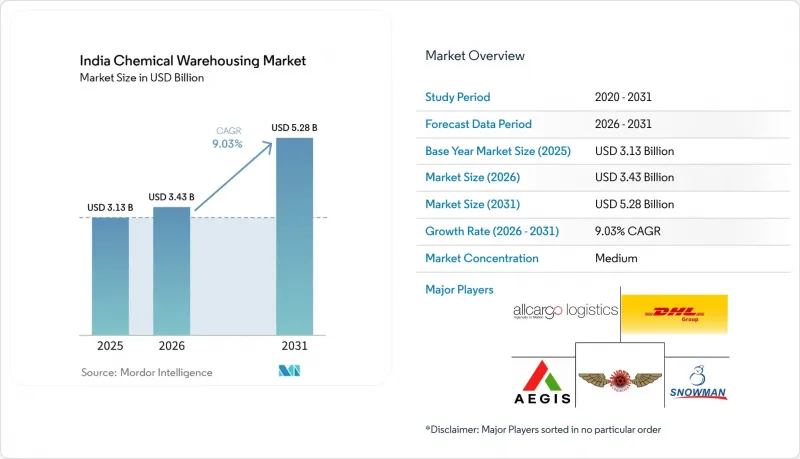

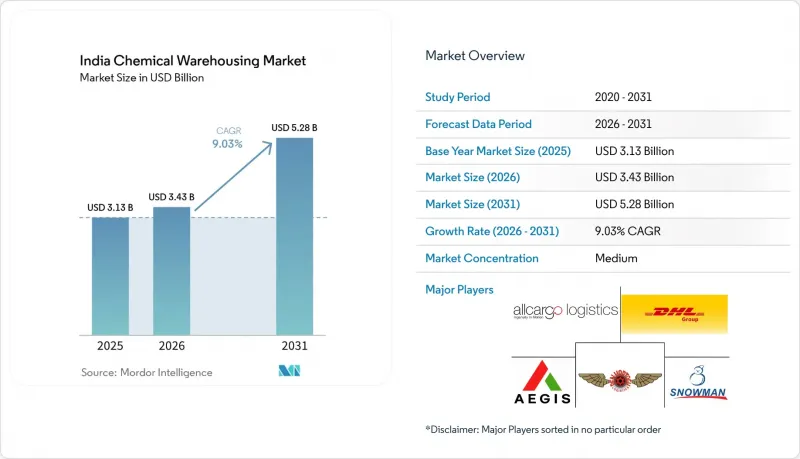

Mordor Intelligence에 의하면, 인도의 화학제품 창고 시장 규모는 2025년 31억 3,000만 달러로 평가되었고, 2026년에는 34억 3,000만 달러로 추정되고, 2031년까지 52억 8,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 9.03%로 성장할 전망입니다.

재고 증가는 200억 달러 규모의 특수 화학제품에 대한 설비 투자 열풍, 국가 물류 정책의 비용 절감 목표, 그리고 항구에서 내륙으로의 운송 시간을 단축하는 전용 화물 회랑에 힘입어 가속화되고 있습니다. 본 보고서는 창고 유형별(일반 창고, 특수 화학제품 창고, 위험물 창고, 온도 관리형 화학제품 창고), 화학제품 유형별(가연성 액체, 부식성 물질, 독성 물질, 산화제, 기타), 그리고 최종 사용자 산업별(기초 화학제품 제조업 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

인도의 화학제품 창고 시장 동향 및 인사이트

200억 달러 규모의 특수 화학제품 설비 투자 열풍(2024-2028년)

생산자들이 업스트림 공정으로의 통합을 추진하며 수출 성장을 도모하는 가운데, 수년에 걸친 투자 급증이 지역 내 창고 수요를 재편하고 있습니다. 예를 들어, 고드레지 인더스트리즈는 발리아 공장에 5,950만 달러를 투자하여 연간 생산 능력을 27만 5,000톤으로 확대하고 특수 알코올 생산 라인을 추가하고 있습니다. 타밀나두주의 탐팍과 라마나타푸람에 대한 타타 케미컬스의 유사한 투자는 신공장을 항만 중심의 물류 회랑에 위치시키는 것입니다. 이러한 확장에 따라 인도의 화학제품 창고 시장은 하지라, 다헤지, 카다롤로 점차 집중되고 있습니다. 이 지역에서는 철도 전용선과 연안 운송을 통해 체류 시간이 단축되고 있습니다. 한편, 사업자들은 원자재 가격 변동과 관세 변경 가능성에 직면해 있어, 단계적이고 신중한 투자를 할 수밖에 없는 상황입니다. 인도 화학 산업이 2028년까지 3,000억 달러 규모에 달할 것이라는 업계 전망은 위험물(HAZMAT) 보관 능력 확충에 대한 장기적인 근거를 더욱 확고히 하고 있습니다.

국가 물류 정책 : A등급 위험물 시설에 대한 세제 혜택

주 차원의 산업 정책에서는 국가건축기준법의 방화 안전 규정 및 PESO(위험물 면허)를 준수하는 A급 창고에 대해 실질적인 자본 비용을 절감할 수 있는 세제 혜택이 제공되고 있습니다. 연방 차원에서는 통합 물류 인터페이스 플랫폼(Unified Logistics Interface Platform)이 현재 36개의 정부 시스템을 연계하여 항만 서류 처리 주기를 대폭 단축하고 체류 시간을 줄이고 있습니다. 인도 창고 협회(Warehousing Association of India)가 발행한 새로운 전자 핸드북은 각종 규정과 기준을 통합하여 개발자의 정보 검색 비용을 절감하고 있습니다. Allcargo와 같은 사업자들은 랙 내 스프링클러 및 거품 소화 설비를 갖춘 다중 위험물 대응 복합 시설을 구축하여 이에 대응하고 있으며, 한편 연방 정부가 자금을 지원하는 3개의 벌크 의약품 공단에서는 규정 준수 부담의 일부가 사회화되어 있습니다. 반면, 2025년 말로 예정된 20건의 화학제품 품질 관리 명령 철폐로 인해 인증에 소요되는 간접비가 줄어들면서, 소규모 3PL 제공업체의 영업이익률이 일시적으로 확대되고 있습니다.

대량 화학제품에 대한 해상화물보험의 할증료 인상

2025년, 홍해 및 페르시아만 항로의 전쟁 위험 보험료는 15-30% 상승하여 수입 용제의 도착 비용을 끌어올렸을 뿐만 아니라, 신용장(L/C)의 담보 요건도 강화되었습니다. 현재 595만 달러 규모의 화물 1건당 총 보험료로 약 7,800달러가 지급되고 있으며, 이는 수출입 흐름에 의존하는 인도의 화학제품 창고 시장 사업자들에게 취급 마진을 압박하는 요인이 되고 있습니다. Aegis사는 장기 용선 계약을 통해 이러한 위험의 일부를 헤지하고 있지만, 소규모 3PL 기업들은 운전자금 부족에 직면해 있어 사업 확장이 지연될 가능성이 있습니다. 바다반 항구와 같은 심수항 프로젝트는 2029년 이후에 일부 완화 효과를 가져올 것으로 기대되지만, 그 전까지는 보험료 변동이 자본 배분에 걸림돌이 될 것입니다.

부문별 분석

2025년 기준으로 인도 화학제품 창고 시장 중 일반 창고가 37.47%를 차지했으며, 상온 보관만으로 충분한 벌크 상품의 유통을 담당하고 있습니다. 이러한 선두 주자에도 불구하고, 바이오의약품, 원료의약품, 온도에 민감한 촉매 등에 대한 수요로 인해, 온도 관리형 화학제품 창고 시장은 2031년까지 연평균 성장률(CAGR) 12.11%라는 견실한 성장세를 보일 것으로 전망됩니다. 각 사업체는 적정 유통 기준(GDP) 요건을 충족하기 위해 전용 냉장실, 글리콜 칠러, 단열 도크 도어의 도입을 추진하고 있습니다. 올카고(All Cargo)사의 16만 평방피트 규모 우라늄 거점은 이러한 추세를 여실히 보여주고 있으며, 25℃ 미만의 보관실과 방폭 조명을 결합하여 70개 이상의 기업에 서비스를 제공하는 전국적인 네트워크의 일환입니다.

불활성 가스 충전, HEPA 필터, ISO 9001 워크플로우를 지원하는 특수 화학제품 창고는 시장 가치가 이동하는 분야로 부상하고 있습니다. 하지라와 다헤지 인근 토지는 현재 상당한 프리미엄이 붙어 있으며, 개발업체들이 '서부 전용 화물 회랑(Western Dedicated Freight Corridor)'과 직접 연결되는 철도 부설선이 있는 부지를 확보하기 위해 경쟁하고 있습니다. 셀시우스 로지스틱스가 2025년에 시작할 의약품용 GDP 준수 크로스독 네트워크는 콜드체인과 위험물(HAZMAT)의 융합을 상징합니다. 한편, 인증된 방화 시스템을 도입하면 보험료가 15-30% 절감된다는 점은 등급 B 창고에서 등급 A 시설로 전환하는 데 있어 추가적인 유인책이 되고 있습니다. 이러한 요인들이 복합적으로 작용하여 인도 화학제품 창고 시장의 장기적인 성장 전략의 기반을 마련하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 10억 루피)

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the india chemical warehousing market size is expected to increase from USD 3.13 billion in 2025 to USD 3.43 billion in 2026 and reach USD 5.28 billion by 2031, growing at a CAGR of 9.03% over 2026-2031.

Inventory expansion is being fueled by a USD 20 billion specialty-chemical capital-expenditure wave, the National Logistics Policy's cost-reduction targets, and Dedicated Freight Corridors that shorten port-to-hinterland transit. This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials Warehouses, Temperature-Controlled Chemical Warehouses), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, Others), and by End-User Industry (Basic Chemicals Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Chemical Warehousing Market Trends and Insights

USD 20 Billion Specialty-Chemical CAPEX Wave (2024-28)

A multi-year investment surge is reshaping regional warehouse demand as producers back-integrate and chase export growth Godrej Industries, for example, is injecting USD 59.5 million into its Valia plant to lift capacity to 275,000 tons per year and add specialty alcohol lines. Similar outlays by Tanfac in Tamil Nadu and Tata Chemicals in Ramanathapuram are aligning new plants with port-centric logistics corridors. These expansions draw the India chemical warehousing market toward Hazira, Dahej, and Cuddalore, where rail sidings and coastal shipping compress dwell times. Operators are simultaneously exposed to raw-material volatility and possible tariff shifts, prompting cautious phase-wise spending. Industry forecasts that India's chemicals sector could touch USD 300 billion by 2028 bolster the long-term case for additional HAZMAT capacity.

National Logistics Policy Tax Holidays for Grade A HAZMAT Facilities

State-level industrial policies are offering tax incentives that cut the effective cost of capital for Grade A warehouses that comply with the National Building Code fire-safety schedule and PESO licensing. At the federal level, the Unified Logistics Interface Platform now links 36 government systems to significantly shrink port document cycles and reduce dwell times.A new e-Handbook from the Warehousing Association of India has consolidated codes and standards, lowering search costs for developers. Operators such as Allcargo have responded by rolling out multi-hazard complexes with in-rack sprinklers and foam suppression, while three federally funded Bulk Drug Parks socialize part of the compliance burden.Conversely, the late-2025 rollback of 20 Chemical Quality-Control Orders has lightened certification overhead, temporarily widening operating margins for smaller 3PL providers.

Rising Marine-Cargo Insurance Surcharges on Bulk Chemicals

War-risk premiums on Red Sea and Persian Gulf routes climbed 15-30% in 2025, lifting the landed cost of imported solvents and raising collateral requirements for letters of credit.A single USD 5.95 million cargo now pays nearly USD 7,800 in total cover, eroding throughput margins for India chemical warehousing market operators that rely on import-export flows. Aegis has hedged part of this exposure via long-term charter-party deals, but smaller 3PLs face working-capital squeezes that could delay expansion. Deep-draft projects such as Vadhavan Port promise partial relief post-2029, yet until then, premium volatility remains a drag on capital deployment.

Other drivers and restraints analyzed in the detailed report include:

- Bharatmala Freight-Corridor Rail Sidings Unlocking Bulk-Chemical Reach

- Lithium-Ion Battery Raw-Material Imports Spurring Class 3 & 8 Storage Demand

- Mandatory BIS Quality-Control Orders Raising Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General warehousing captured 37.47% of the India chemical warehousing market in 2025, serving bulk commodity flows that need only ambient storage. Despite this lead, temperature-controlled chemical warehouses will register a brisk 12.11% CAGR through 2031 due to biologics, active pharmaceutical ingredients, and temperature-sensitive catalysts. Operators are adding dedicated cold rooms, glycol chillers, and insulated dock doors to meet Good Distribution Practice requirements. Allcargo's 160,000-square-foot Uran site illustrates the trend, blending sub-25 °C chambers with explosion-proof lighting as part of a broader national network that serves more than 70 companies.

Specialty chemical warehouses configured for inert-gas blanketing, HEPA filtration, and ISO 9001 workflows have emerged as the market's value-migration zone. Land near Hazira and Dahej now commands significant price premiums as developers bid for rail-siding parcels that link directly to the Western Dedicated Freight Corridor. Celcius Logistics' 2025 launch of a GDP-compliant cross-dock network for pharma exemplifies convergence between cold chain and HAZMAT, while insurer premium reductions of 15-30% for certified fire systems create an added incentive to shift from Grade B sheds to Grade A facilities. Collectively, these factors anchor the long-term expansion strategy of the India chemical warehousing market.

List of Companies Covered in this Report:

- Aegis Logistics Ltd

- Allcargo Logistics

- DHL Group

- Den Hartogh Logistics

- Snowman Logistics Ltd

- Adani Logistics Ltd

- BEST Roadways Ltd.

- Swift Cargo

- IMC Logistics

- Tankstore Ltd

- Noatum Logistics

- Vopak India

- Mahindra Logistics

- Kiran Group

- Apollo Supply Chain

- Seashell Logistics

- DSV

- BDP International

- Yusen Logistics

- Rhenus Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 USD 20 Billion Specialty-Chemical CAPEX Wave (2024-28)

- 4.2.2 National Logistics Policy Tax Holidays for Grade-A Hazmat Facilities

- 4.2.3 Bharatmala Freight-Corridor Rail Sidings Unlocking Bulk-Chemical Hinterland Reach

- 4.2.4 Lithium-Ion Battery Raw-Material Imports Spurring Class 3 & 8 Storage Demand

- 4.2.5 Agro-Pesticide Production-Linked Incentive Scheme Amplifying Regional Warehouse Needs

- 4.2.6 QR-Based Hazardous-Waste E-Tracking (NHWIS-2025) Accelerating Digital WMS Adoption

- 4.3 Market Restraints

- 4.3.1 Rising Marine-Cargo Insurance Surcharges on Bulk Chemicals

- 4.3.2 Mandatory BIS Quality-Control Orders Raising Compliance Costs for 3PL Operators

- 4.3.3 Short Supply of PFAS-Free Fire-Suppression Systems Delaying Warehouse Retrofits

- 4.3.4 Variable Inland-Waterway Draft Hindering Barge Logistics for Liquid Chemicals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, INR Bn)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals and Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings and Adhesives

- 5.3.6 Food and Feed Additives

- 5.3.7 Oil and Gas / Petrochemicals

- 5.3.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Aegis Logistics Ltd

- 6.4.2 Allcargo Logistics

- 6.4.3 DHL Group

- 6.4.4 Den Hartogh Logistics

- 6.4.5 Snowman Logistics Ltd

- 6.4.6 Adani Logistics Ltd

- 6.4.7 BEST Roadways Ltd.

- 6.4.8 Swift Cargo

- 6.4.9 IMC Logistics

- 6.4.10 Tankstore Ltd

- 6.4.11 Noatum Logistics

- 6.4.12 Vopak India

- 6.4.13 Mahindra Logistics

- 6.4.14 Kiran Group

- 6.4.15 Apollo Supply Chain

- 6.4.16 Seashell Logistics

- 6.4.17 DSV

- 6.4.18 BDP International

- 6.4.19 Yusen Logistics

- 6.4.20 Rhenus Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment