|

시장보고서

상품코드

2063336

영국의 화학제품 창고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United Kingdom Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

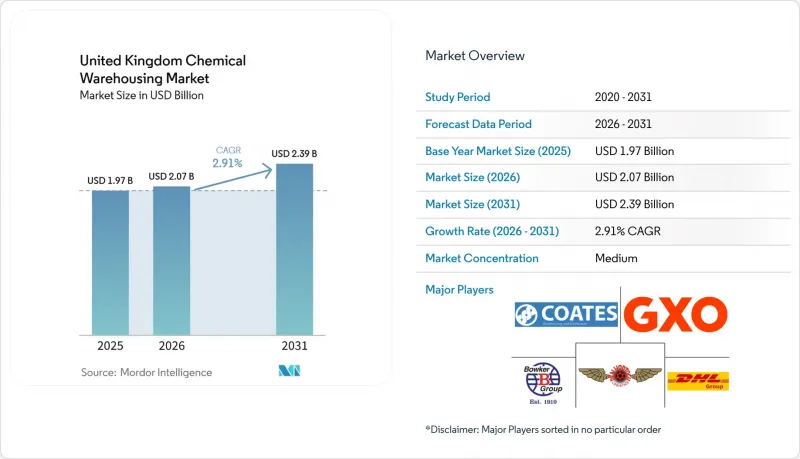

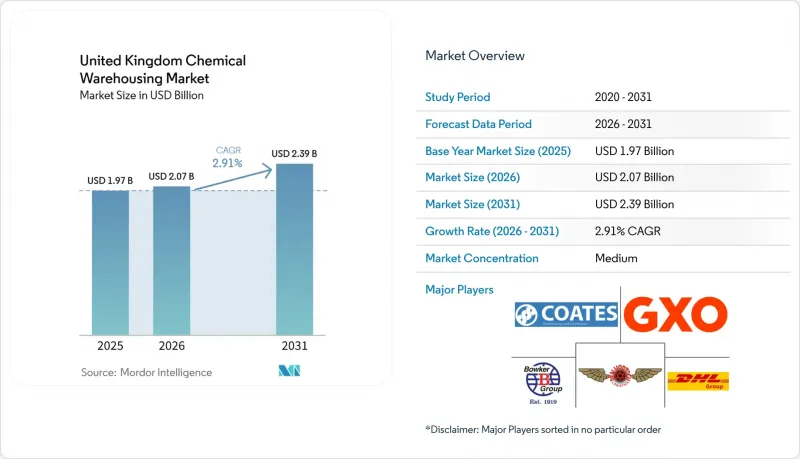

Mordor Intelligence에 의하면, 영국의 화학제품 창고 시장 규모는 2025년 19억 7,000만 달러로 평가되었고, 2026년에는 20억 7,000만 달러로 추정되고, 2031년까지 23억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 2.91%로 성장할 전망입니다.

본 보고서는 창고 유형별(일반 창고, 특수 화학제품 창고, 위험물(HAZMAT) 창고 등), 화학 물질 유형별(인화성 액체, 부식성 물질 등), 그리고 최종 사용자 산업별(기초 화학제품 제조, 특수 화학제품 제조, 농약 등)로 분류되어 있습니다. 시장 전망은 금액 기준(10억 달러)으로 제시되어 있습니다.

영국의 화학제품 창고 시장 동향 및 인사이트

의약품 및 생명과학 제조 분야의 강점

영국의 의약품 생산량은 2025년까지 증가세 이어갔으며, 2월에는 4.4% 증가했고, 12월까지의 3개월간에는 전분기 대비 9.3% 증가를 기록했습니다. 이에 따라 제조 및 연구 거점과 가까운 곳에 위치한 GDP 기준 및 콜드체인 대응 보관 공간에 대한 수요가 증가하고 있습니다. 정부의 생명과학 경쟁 지표에 따르면, 영국은 2024년까지 더 많은 외국인 직접 투자와 주식 자금을 유치하고 있으며, 이로 인해 전문적인 창고 보관 및 유통 솔루션이 필요한 규제 대상 제품의 파이프라인이 강화되고 있습니다. '생명과학 부문 계획'에는 최대 6억 파운드(8억 946만 달러) 규모의 지원이 수반되는 AI 기반 의료 데이터 서비스도 개요로 제시되어 있으며, 이러한 움직임은 임상 개발을 가속화하고 임상시험용 의약품의 단기 보관 프로세스를 확대할 가능성이 있습니다. 극저온에서의 취급과 엄격한 관리 체계(체인 오브 커스터디)가 필요한 첨단 의료용 의약품은 2024년 영국에서 뚜렷한 임상시험 실적을 거두었으며, 바이오의약품 공급망을 뒷받침하는 시설에 대한 사양 요건을 지속적으로 강화해 나갈 것으로 보입니다. 템즈 밸리 지역의 생물학적 제제 생산 능력 확대 계획은 인접한 무균 보관 및 온도 관리 물류에 대한 장기적인 수요를 시사하고 있습니다. 이러한 모든 요인이 복합적으로 작용하여, 생명과학 업계가 제조, 임상 업무 및 콜드체인 네트워크를 확장함에 따라 영국 화학제품 창고 시장의 꾸준한 성장을 뒷받침하고 있습니다.

브렉시트 이후의 세관 및 보세 창고

영국 국세청(HM Revenue & Customs)의 보고서에 따르면, 승인된 통관 창고의 총 용량은 매우 크며, 가동률은 평균 약 87%이고 피크 시에는 90%에 달하고, 수입 완충 기능이나 관세 납부 유예 측면에서 보세 시설에 대한 구조적인 의존도가 두드러지게 나타나고 있습니다. 일반 창고에 비해 통관 창고 재고에서 위험물이 차지하는 비중이 현저히 높은데, 이는 보세 업무에서 위험 분리형 보관 및 누출 방지 시스템의 중요성을 반영하고 있습니다. EU-영국 무역협력협정 및 영국 REACH 규정의 지속적인 시행으로 인해, 서류 작성 및 원산지 규정이 규정 준수(컴플라이언스)의 핵심이 되었으며, 상품이 자유 유통 단계에 진입할 때까지 관세 및 부가가치세(VAT) 납부를 유예할 수 있는 보세 보관 모델에 대한 수요가 지속되고 있습니다. 간소화된 통관 절차와 향후 10년간의 세제 혜택 연장을 특징으로 하는 영국의 프보고서 프로그램은 화학제품 무역 흐름을 뒷받침하는 지정 구역 내에 통관 창고를 설치하는 이점을 한층 더 강화하고 있습니다. 더 친환경적인 선단을 위한 민관 공동 항만 투자와 선석 및 철도 운송 능력 확충을 통해, 위험물 운송의 적시성(JIT)과 예측 가능성이 향상되고 있습니다. 그 결과, 브렉시트 이후 영국의 화학제품 창고 시장에서 세관 및 보세 시설은 여전히 전략적 수단으로 자리 잡고 있습니다.

심각한 창고 공간 부족

규제 준수 요건으로 인한 공간 부족 현상은 지속되고 있으며, 세관 승인 수용 능력은 가동률이 높아 여유 공간이 제한적이기 때문에 새로운 화학물질의 유입이나 계절적 수요 급증에 대응할 수 있는 유연성이 제약을 받고 있습니다. 이용률의 중앙값이 87%이고, 피크 시간대의 가동률이 90%에 육박한다는 사실은 특히 위험물 분야에서 여력이 제한적임을 보여줍니다. 위험물의 경우, 일반 창고보다 세관 창고에서의 재고 비중이 더 높습니다. COMAH(중대 위험 물질 관리법)에 따른 감독 또한 추가적인 제약 요인으로 작용하고 있으며, 우선 대상 시설에서는 기후 위험 평가 및 홍수 대책 프로토콜이 요구되어, 이로 인해 용량 변경 일정이 지연될 가능성이 있습니다. 규정 준수 부담은 리스크 관리 측면에서 타당하지만, 대규모 개보수 없이 특정 위험물 등급을 수용할 수 있는 상위 등급 시설의 부족 문제를 더욱 심화시키고 있습니다. 영국의 화학제품 창고 시장에서 이는 입지 선정 시 항만이나 클러스터와의 근접성과, 적절한 부지 및 허가 취득의 제한된 공급량 사이에서 균형을 맞추어야 함을 의미합니다. 단기적인 영향으로는 전환 비용 증가와 전문적인 보관 역량 도입에 소요되는 리드타임의 장기화를 들 수 있습니다.

부문별 분석

2025년에는 자산 소유자들이 유해 물질 취급 기준을 준수하는 격리 시설, 인공 환기 시스템, 첨단 소화 설비를 우선적으로 도입한 결과, 특수 화학 물질 창고가 40.64%라는 가장 높은 점유율을 차지했습니다. 부식성, 가연성, 산화성 물질에 대한 규제 강화는 자본 측면에서의 진입 장벽이 되어, 영국 화학물질 창고 시장에서 서비스 프리미엄을 유지하게 하고 공급의 탄력성을 저하시키고 있습니다. 영국의 우선 COAH(중대 위험 시설) 부지는 기후 위험 평가 및 홍수 대책 계획을 포함한 강화된 감독 하에 운영되고 있으며, 이에 따라 저장 시설의 설계 및 입지 선정은 관련 규제와 밀접하게 연계되어 있습니다. 이러한 규제로 인해 일상적인 운영 관리에서 안전 시나리오, 비상 계획, 지역 사회와의 협력의 중요성이 커지고 있습니다. 그 결과, 영국의 화학제품 창고 업계는 위험 관리와 복합 운송 접근성을 모두 충족시키는 항만이나 산업 집적지와 가까운 전문적인 입지를 선호하는 경향이 있습니다.

바이오의약품과 첨단 치료제가 엄격한 GDP 및 GMP 요건 하에 임상 및 상업적 생산을 확대함에 따라, 온도 관리 시설 부문이 5.78%로 가장 빠르게 성장하고 있습니다. 바이오의약품이나 세포 치료제를 위한 2-8℃의 냉장 보관, 혹은 그보다 더 낮은 온도의 보관 구역을 갖춘 시설은 더 엄격한 사양 기준이 요구되며, 제조 거점이나 공항 인근에 입지하는 것이 더욱 중요시될 것입니다. 2025년까지 의약품 생산량이 증가함에 따라, 이러한 시설에서의 종단간 추적성 및 빈번한 품질 감사의 필요성이 더욱 커지고 있습니다. 영국의 화학제품 창고 시장 규모는 연평균 성장률(CAGR) 2.91%를 기록하며 2031년까지 23억 9,000만 달러에 달할 것으로 전망됨에 따라, 업체들은 사이언스 파크나 국제 관문과 가까운 지역에 고사양 창고를 집중 배치할 수 있도록 시설 규모를 조정하고 있습니다. 이러한 구성을 통해 상온 및 저위험 화물의 수용 능력을 확보하는 동시에, 관리 환경에 대한 수요 증가에도 대응하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the united kingdom chemical warehousing market size is expected to increase from USD 1.97 billion in 2025 to USD 2.07 billion in 2026 and reach USD 2.39 billion by 2031, growing at a CAGR of 2.91% over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), and by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Agrochemicals, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

United Kingdom Chemical Warehousing Market Trends and Insights

Pharmaceutical and Life Sciences Manufacturing Strength

Pharmaceutical output in the United Kingdom expanded through 2025, with a 4.4% rise in February and a 9.3% three month on three-month pace by December, which is lifting storage needs for GDP-compliant and cold chain space close to manufacturing and research centers. Government life sciences competitiveness indicators show the United Kingdom attracted stronger foreign direct investment and equity finance into 2024, reinforcing the pipeline of regulated products that require specialized warehousing and distribution solutions. The Life Sciences Sector Plan also outlines an AI-ready health data service with up to GBP 600 million (USD 809.46 million) of support, a move that can accelerate clinical development and expand short-cycle storage flows for investigational products. Advanced therapy medicinal products, which require cryogenic handling and strict chain of custody controls, had a notable United Kingdom trial footprint in 2024 and will continue to push specification requirements for facilities that serve biopharma supply chains. Planned expansion of biologics manufacturing capacity in the Thames Valley region signals long-term demand for adjacent sterile storage and temperature-managed logistics. All together, these forces support steady expansion in the United Kingdom chemical warehousing market as life sciences scale manufacturing, clinical operations, and cold chain networks.

Post-Brexit Customs and Bonded Warehousing

HM Revenue & Customs reported large installed customs authorized capacity with utilization rates near 87% on average and 90% at peaks, highlighting the structural reliance on bonded facilities for import buffers and duty deferment. Hazardous goods comprised a materially higher share of customs warehouse inventory relative to general stores, which reflects the importance of risk-segregated storage and spill prevention systems in bonded operations. Ongoing implementation of the EU-UK Trade and Cooperation Agreement and UK REACH places documentation and origin rules at the core of compliance, sustaining demand for bonded storage models that defer duty and VAT until goods enter free circulation. The United Kingdom Freeports program, with simplified customs processes and extended tax relief windows through the next decade, strengthens the case for locating customs warehousing within designated zones that serve chemicals trade flows. Complementary public and private port investments in cleaner fleets and added berth and rail capacity improve predictability for just-in-time hazardous shipments. As a result, customs and bonded facilities remain a strategic lever in the United Kingdom chemical warehousing market in the post-Brexit context.

Severe Warehouse Space Shortage

Structural tightness persists for compliant space, and customs-authorized capacity has shown high utilization with limited free space, which constrains flexibility for new chemical flows and seasonal peaks. Median utilization at 87% and peak occupancy near 90% indicate limited headroom, especially for dangerous goods, where inventory shares are higher in customs warehouses than in general sites. COMAH oversight adds further constraints, as priority establishments require climate risk assessments and flood preparedness protocols that can extend timelines for capacity changes. The compliance burden is appropriate for risk management, but reinforces the scarcity of upper-tier sites that can accept certain hazard classes without extensive modification. For the United Kingdom chemical warehousing market, this means location decisions must balance proximity to ports and clusters with the limited availability of suitable lots and permits. The shorter effect is higher switching costs and longer commissioning lead times for specialized capacity.

Other drivers and restraints analyzed in the detailed report include:

- Specialty Chemicals and Advanced Materials Growth

- Port Infrastructure Modernization

- High Energy and Occupancy Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty chemical warehouses held the largest share of 40.64% in 2025 as asset owners prioritized segregation, engineered ventilation, and advanced fire suppression that align with hazardous substance handling standards. Enhanced controls for corrosive, flammable, and oxidizing substances create capital barriers that sustain service premiums and reduce supply elasticity in the United Kingdom chemical warehousing market. Priority COMAH sites in England operate under intensified oversight with climate risk assessments and flood planning, which keeps storage design and location choices tightly linked to regulation. These controls elevate the role of safety cases, emergency planning, and community liaison in day-to-day operational management. As a result, the United Kingdom chemical warehousing industry leans toward specialized footprints near ports and clusters that pair hazard control with multimodal access.

Temperature-controlled sites are the fastest growing of 5.78% as biopharma and advanced therapies expand clinical and commercial output with stringent GDP and GMP requirements. Facilities that support 2-8°C refrigerated storage or colder zones for biologics and cell-based therapies will command higher specification standards and closer siting to manufacturing and airports. Rising pharmaceutical production through 2025 strengthens the case for end-to-end traceability and frequent quality audits in these buildings. As the United Kingdom chemical warehousing market size advances to USD 2.39 billion by 2031 at a 2.91% CAGR, operators are calibrating footprints to concentrate higher spec units close to science parks and international gateways. This setup balances capacity for ambient and low-hazard goods while meeting rising demand for controlled environments.

List of Companies Covered in this Report:

- H.W. Coates

- Bowker Transport

- Den Hartogh Logistics

- GXO Logistics

- DHL Group

- Edge Worldwide

- Rhenus Logistics

- HOYER Group

- DSV

- CEVA Logistics

- Brenntag

- Bertschi

- Yusen Logistics

- Kuehne + Nagel

- Noatum Logistics

- Clarion Shipping Services L.L.C

- BDP International

- DACHSER

- Streamline Shipping Group Ltd.

- C.H Robinson

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pharmaceutical and Life Sciences Manufacturing Strength

- 4.2.2 Post-Brexit Customs and Bonded Warehousing

- 4.2.3 Specialty Chemicals and Advanced Materials Growth

- 4.2.4 Port Infrastructure Modernization

- 4.2.5 Net Zero Carbon Commitments

- 4.2.6 COMAH Safety Regulation Enforcement

- 4.3 Market Restraints

- 4.3.1 Severe Warehouse Space Shortage

- 4.3.2 High Energy and Occupancy Costs

- 4.3.3 HGV Driver Shortage Crisis

- 4.3.4 Brexit-Related Regulatory Uncertainty

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Geopolitical Events on the Market

- 4.9 Circular Economy Chemical Recycling

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 H.W. Coates

- 6.4.2 Bowker Transport

- 6.4.3 Den Hartogh Logistics

- 6.4.4 GXO Logistics

- 6.4.5 DHL Group

- 6.4.6 Edge Worldwide

- 6.4.7 Rhenus Logistics

- 6.4.8 HOYER Group

- 6.4.9 DSV

- 6.4.10 CEVA Logistics

- 6.4.11 Brenntag

- 6.4.12 Bertschi

- 6.4.13 Yusen Logistics

- 6.4.14 Kuehne + Nagel

- 6.4.15 Noatum Logistics

- 6.4.16 Clarion Shipping Services L.L.C

- 6.4.17 BDP International

- 6.4.18 DACHSER

- 6.4.19 Streamline Shipping Group Ltd.

- 6.4.20 C.H Robinson

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment