|

시장보고서

상품코드

2063324

유럽의 화학제품 창고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

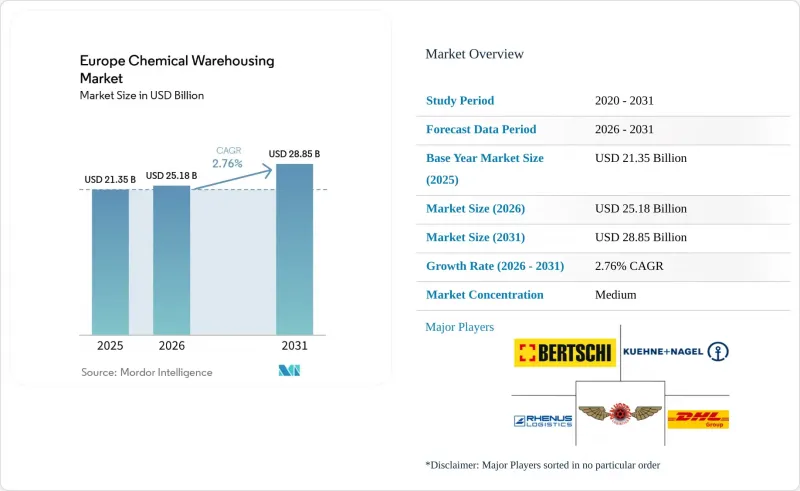

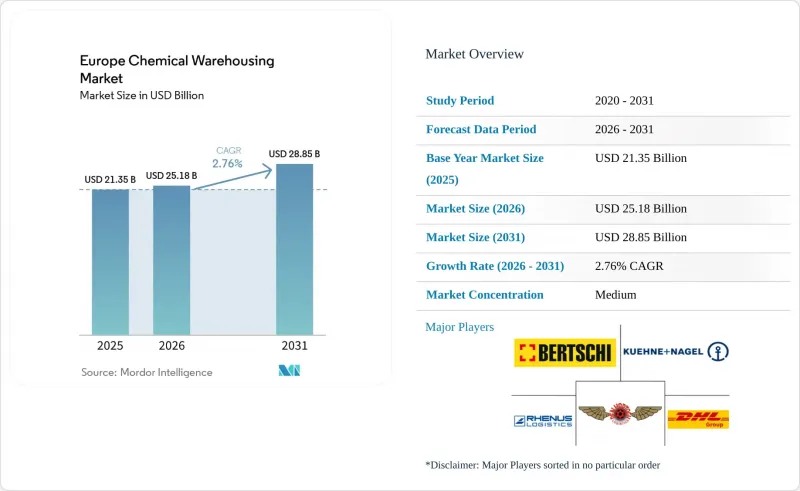

Mordor Intelligence에 의하면, 유럽의 화학제품 창고 시장 규모는 2025년 213억 5,000만 달러로 평가되었습니다. 2026년에는 251억 8,000만 달러, 2031년까지 288억 5,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR은 2.76%를 나타낼 것으로 예측됩니다.

본 보고서는 창고 유형(일반 창고, 특수 화학물질 창고, 위험물(HAZMAT) 창고, 기타), 화학물질 유형(인화성 액체, 기타), 최종 사용자 산업(기초 화학물질 제조, 특수 화학물질 제조, 기타), 국가(독일, 스페인, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 화학제품 창고 시장 동향 및 인사이트

기가팩토리에서의 배터리 등급 화학물질 생산 확대가 ADR 규제 대상 물질의 보관 수요를 끌어올리고 있습니다.

유럽의 배터리 셀 생산이 급속히 확대됨에 따라, ADR 클래스 8 규제의 적용을 받는 수산화 리튬, NMP 용매, PVDF 바인더에 대한 수요가 집중되고 있습니다. Northvolt의 Ett 사업장에서 2026년까지 60GWh로 확장할 계획만으로도 반경 50km 이내 지역에 새로운 온도 제어형 보관 시설이 필요하게 되며, 이에 따라 2028년까지 해당 지역의 보관 용량은 50만 m²를 넘어설 것으로 전망됩니다. 소화 설비의 업그레이드, 위험물 전용 구역 설치, ±2℃의 온도 관리가 필요하기 때문에 시설에 대한 투자 비용은 표준 부지보다 30-45% 더 높아집니다. 공간 부족이 가장 심각한 곳은 독일 동부, 스웨덴 북부, 헝가리의 자동차 산업 회랑이며, SEVESO III 규정에 따른 허가를 신속하게 취득하고 모듈식 창고를 구축할 수 있는 사업자가 유리한 입장에 서게 됩니다.

EU의 CBAM과 관련된 기초 화학물질의 국내 회귀가 버퍼 재고 창고에 대한 수요를 창출하고 있습니다.

수입 암모니아와 메탄올에 부과된 탄소 관세로 인해, EU 역내 생산이 20년 만에 수익성을 회복하게 되었으며, 이는 BASF와 Yara가 유럽 내 생산 능력 재개를 계획하는 계기가 되었습니다. 각 제조업체들은 현재 공급 리스크를 헤지하기 위해 2023년 기준치의 2배에 해당하는 30-45일 분량의 원자재를 보유하고 있으며, 루트비히스하펜, 안트베르펜, 지중해 연안 항만 주변에서 창고 면적이 확대되고 있습니다. 규모보다 유연성이 더 중요시됨에 따라, 민첩한 WMS를 갖춘 다품목 창고가 단일 상품용 탱크를 대체하며 시장 점유율을 확대되고 있습니다. 북아프리카산 그린 수소 수입이 비용 면에서 우위를 점하고 있어, 이탈리아와 스페인은 CBAM의 혜택을 특히 많이 누리고 있으며, 부두 인근의 저장 수요가 급증하고 있습니다.

항만 혼잡과 홍해를 경유하는 우회로 인해 체류 시간과 재고 리스크가 확대됨

2025년, 희망봉을 경유하는 항로로 인해 아시아에서 EU까지의 항해 일수가 최대 14일 연장되었습니다. 로테르담에서 컨테이너의 평균 체류 기간이 4일에서 10일로 늘어남에 따라, 수입업체들은 안전 재고를 두 배로 늘리고 더 높은 선박 체류료를 지불할 수밖에 없게 되었습니다. 대체 공급업체가 없는 특수 품목의 수입업체는 15-20%의 물류비 상승을 감수할 수밖에 없어, 이익률이 축소됨에 따라 조달처를 국내로 복귀한 생산 능력으로 전환하는 경향을 보이고 있습니다.

부문별 분석

온도 관리형 화학물질 창고는 2031년까지 유럽 화학물질 창고 시장 점유율 성장 추이의 5.62%를 차지했습니다. 이는 ±2℃라는 좁은 온도 범위만을 허용하는 바이오의약품이나 배터리용 전해액 수요가 급증한 것을 반영한 것입니다. 이러한 고사양 시설과 관련된 유럽의 화학물질 창고 시장 규모는 확대되고 있습니다. 이는 사업자가 기존 창고를 개조하고, 멀티존 공조 시스템, 습도 조절 장치, 불활성 가스 소화 시스템을 도입함으로써 단일 시설 내에서 GDP(우수 제조 기준) 및 ADR(위험물 운송 규정)의 요건을 충족시키려 하기 때문입니다. 제곱미터당 1,200-1,800유로(1,411-2,117달러)에 달하는 높은 건설 비용은 바이오시밀러 파이프라인을 위한 최대 5년에 달하는 계약 기간을 통해 상쇄되는 경향이 강해지고 있으며, 이로 인해 부동산 소유주는 더 높은 수익률을 확보하고, 부채 상환 일정을 앞당길 수 있게 되었습니다.

2025년에도 특수 화학제품 창고는 유럽의 화학제품 창고 시장 규모의 38.58%를 계속 차지했으며, 그 중심에는 격리된 베이, 전도성 바닥 코팅, ISO 클린룸 부대 시설이 필요한 마이크로 배치 전자 화학제품 및 기능성 첨가제가 있습니다. 주로 대량 상품용 창고로 구성된 일반 창고는 고객들이 업그레이드된 특수 시설 내에서 제공되는 부가가치가 높은 혼합 및 사전 희석 서비스로 전환함에 따라 가격 결정력을 점차 상실하고 있습니다. 위험물 전용 빌딩은 여전히 석유화학제품 유통에 있어 필수적이지만, PFAS 오염에 대한 우려로 인해 보험료가 상승하면서 이익률 압박에 직면해 있습니다. 이에 따라 소규모 사업자들은 ‘디지털 유럽’ 보조금을 통해 자금을 지원받아, 공동 사업을 통해 소화용수 저장 설비를 현대화해 나가고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the europe chemical warehousing market size is projected to expand from USD 21.35 billion in 2025 USD 25.18 billion in 2026 to USD 28.85 billion by 2031, growing at a CAGR of 2.76% over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and More), by Chemical Type (Flammable Liquids, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Country (Germany, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Chemical Warehousing Market Trends and Insights

Gigafactory Battery-Grade Chemical Buildouts Elevating ADR Storage Demand

Europe's rapid battery-cell scale-up drives clustered demand for lithium hydroxide, NMP solvents, and PVDF binders that fall under ADR Class 8 regulations. Northvolt's Ett expansion to 60 GWh by 2026 alone requires new temperature-controlled storage within a 50 km radius, pushing regional capacity past 500,000 m2 by 2028. Facility investments are 30-45% costlier than standard sites because of fire-suppression upgrades, segregated hazmat bays, and +-2 °C climate control. Spatial pressure is most acute in eastern Germany, northern Sweden, and Hungary's automotive corridor, favoring operators that can fast-track SEVESO-III permits and deploy modular warehouses.

EU CBAM-Linked Reshoring of Basic Chemicals Creating Buffer-Stock Warehousing

Carbon tariffs on imported ammonia and methanol make EU production financially viable for the first time in two decades, prompting BASF and Yara to plan continental capacity restarts. Manufacturers now hold 30-45 days of feedstock double the 2023 norm to hedge supply risks, swelling warehousing footprints around Ludwigshafen, Antwerp, and Mediterranean ports. Flexibility trumps scale, so multi-product warehouses with agile WMS gain share over single-commodity tanks. Italy and Spain stand out as CBAM beneficiaries because green-hydrogen imports from North Africa offer cost advantages, sending berth-proximate storage demand surging.

Port Congestion and Red-Sea Rerouting Inflating Dwell-Time and Inventory Risk

Cape-of-Good-Hope routing lengthened Asian-to-EU voyages by up to 14 days in 2025. Rotterdam's average container dwell stretched from 4 days to 10 days, forcing importers to double safety stocks and pay higher demurrage fees. Specialty importers lacking secondary suppliers must absorb 15-20% logistics-cost inflation, shrinking margins, and nudging procurement toward reshored capacity.

Other drivers and restraints analyzed in the detailed report include:

- Offshore-Wind Resin and Hardener Volume Surge Near North Sea Ports

- EU Digital Europe Subsidies Accelerating Warehouse Robotics and Autonomy Adoption

- PFAS Phase-Out Liabilities Requiring Costly Decontamination Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Temperature-controlled chemical warehouses captured 5.62% of the Europe chemical warehousing market share growth trajectory through 2031, reflecting surging biologics and battery-grade electrolyte demand that tolerates temperature windows of only +-2 °C. The Europe chemical warehousing market size linked to these high-specification sites is climbing as operators retrofit legacy rooms with multi-zone HVAC, humidity scrubbers, and inert-gas fire suppression to satisfy GDP and ADR rules in a single footprint. Premium build costs of EUR 1,200-1,800 (USD 1411-2117) per m2 are increasingly offset by contract lengths stretching to five years for biosimilar pipelines, enabling landlords to lock in higher yields and speed debt pay-down schedules.

Specialty chemical warehouses still controlled 38.58% of the Europe chemical warehousing market size in 2025, anchored by micro-batch electronic chemicals and performance additives that demand segregated bays, conductive-floor coatings, and ISO Clean Room annexes. General warehouses, largely bulk commodity halls, are losing pricing power as clients gravitate toward value-added blending or pre-dilution services now offered inside upgraded specialty facilities. Hazmat-only buildings remain a staple for petrochemical flows but face margin squeeze from mounting insurance premiums after PFAS contamination scares, pushing small operators toward joint-venture fire-water containment upgrades funded under Digital Europe grants.

List of Companies Covered in this Report:

- DHL Group

- Kuehne + Nagel

- Rhenus Logistics

- Bertschi AG

- Den Hartogh Logistics

- Talke Logistics

- HOYER Group

- Broekman Logistics

- Odyssey Logistics & Technology Corporation

- Mainfreight

- NTG Nordic Transport Group A/S

- H.W. Coates

- TIBA Group

- H.Essers

- DSV A/S

- CMA CGM Group (Including CEVA Logistics)

- BDP International

- GEODIS

- C.H. Robinson

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Gigafactory Battery-Grade Chemical Buildouts Elevating ADR Storage Demand

- 4.2.2 EU CBAM-Linked Reshoring of Basic Chemicals Creating Buffer-Stock Warehousing

- 4.2.3 EU Digital Europe Subsidies Accelerating Warehouse Robotics and Autonomy Adoption

- 4.2.4 Offshore-Wind Resin and Hardener Volume Surge Near North Sea Ports

- 4.2.5 Mandatory QR-Traceability under EU Chemicals Strategy Boosting WMS Upgrades

- 4.2.6 Rise of Contract Synthesis Start-Ups Needing Flexible Multi-Tenant Hazmat Space

- 4.3 Market Restraints

- 4.3.1 PFAs Phase-Out Liabilities Requiring Costly Decontamination Capacity

- 4.3.2 Green-Finance Taxonomy and Higher Rates Raising Retrofit Hurdle Costs

- 4.3.3 Port Congestion and Red-Sea Rerouting Inflating Dwell-Time and Inventory Risk

- 4.3.4 Extreme-Weather Resilience Mandates Driving Unplanned Capex on Sites

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals and Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings and Adhesives

- 5.3.6 Food and Feed Additives

- 5.3.7 Oil and Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 Russia

- 5.4.4 Italy

- 5.4.5 Netherlands

- 5.4.6 Spain

- 5.4.7 Poland

- 5.4.8 France

- 5.4.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Kuehne + Nagel

- 6.4.3 Rhenus Logistics

- 6.4.4 Bertschi AG

- 6.4.5 Den Hartogh Logistics

- 6.4.6 Talke Logistics

- 6.4.7 HOYER Group

- 6.4.8 Broekman Logistics

- 6.4.9 Odyssey Logistics & Technology Corporation

- 6.4.10 Mainfreight

- 6.4.11 NTG Nordic Transport Group A/S

- 6.4.12 H.W. Coates

- 6.4.13 TIBA Group

- 6.4.14 H.Essers

- 6.4.15 DSV A/S

- 6.4.16 CMA CGM Group (Including CEVA Logistics)

- 6.4.17 BDP International

- 6.4.18 GEODIS

- 6.4.19 C.H. Robinson

- 6.4.20 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment