|

시장보고서

상품코드

2063327

중동의 화학제품 창고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Middle East Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

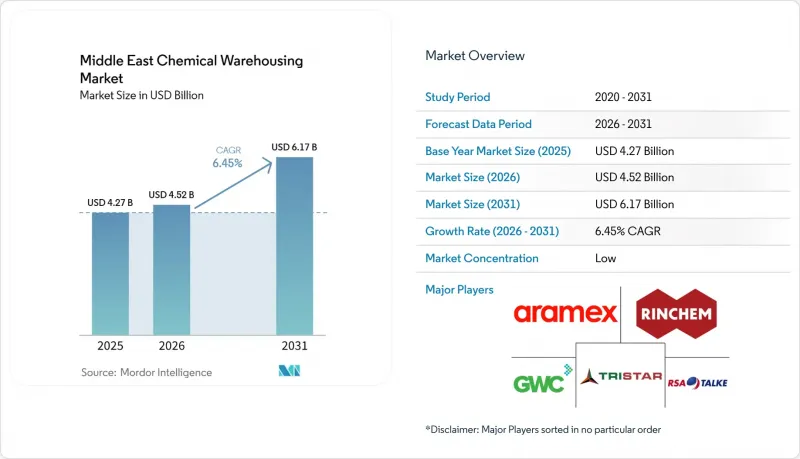

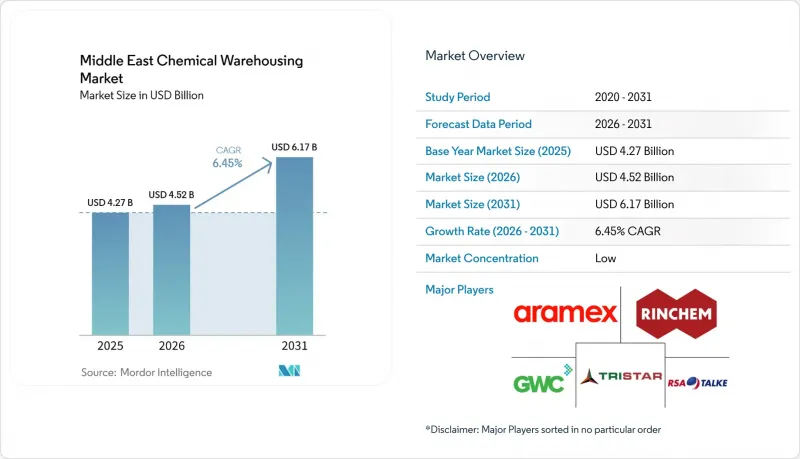

Mordor Intelligence에 의하면, 중동의 화학제품 창고 시장 규모는 2025년 42억 7,000만 달러로 평가되었고, 2026년에는 45억 2,000만 달러로 추정되고, 2031년까지 61억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 6.45%로 성장할 전망입니다.

본 보고서는 창고 유형별(일반 창고, 특수 화학물질 창고 등), 화학제품 유형별(인화성 액체, 부식성 물질 등), 최종 사용자 산업별(기초 화학제품 제조 등), 지역별(사우디아라비아, 아랍에미리트, 카타르, 오만, 쿠웨이트, 바레인, 기타 중동 국가)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동의 화학제품 창고 시장 동향 및 분석

석유화학 산업의 주도력이 전문적인 보관 수요를 견인하고 있습니다.

만안 지역 전체에서 가동을 시작한 대규모 통합 복합 시설은 원료 및 폴리머의 지속적인 처리량 증가로 이어지고 있으며, 이에 따라 규정을 준수하는 대량 및 포장 화학제품의 보관 수요가 증가하고 있습니다. 사우디아라비아에서는 합작 투자를 통해 건설된 새로운 혼합 원료 분해 및 하류 설비가 대규모 에틸렌 및 폴리에틸렌 생산 능력을 가동할 예정이며, 이에 따라 항만 및 철도망 인근으로 위험물 및 별도 보관이 필요한 가연성 액체와 완제품 수지의 안정적인 물류가 창출될 것입니다. 카타르에서는 라스 라판 석유화학 프로젝트가 수출 시장을 대상으로 에틸렌 및 폴리에틸렌을 공급하게 되며, 이에 따라 위험물 분류 기준을 충족하는 탱크 설비, 컨테이너용 수지 보관 시설 및 하역 구역이 필요하게 됩니다. 중동의 화학제품 창고 시장은 플랜트와 항구 간의 양방향 물류 수요에 대응하기 위해, 소화 설비의 밀도 향상, 증기 관리, 그리고 도로 및 철도 연결망의 개선을 통해 이에 대응하고 있습니다. 또한, 제3자 보관 업체들도 수출 서류 및 세계 각국 고객의 사양에 부합하는 수지 포장(봉지 또는 드럼)을 지원하기 위해 보세 구역과 포장 라인을 확충하고 있습니다. 이러한 노력을 통해 중동 화학제품 창고 시장은 해당 지역의 주요 석유화학 투자 주기와 계속해서 발맞추어 나갈 수 있을 것입니다.

자유무역지대 및 경제도시 개발이 인프라 구축을 가속화

물류 전용 구역은 이미 구축된 기반 시설, 간소화된 인허가 절차, 부두 및 야드 공간에 대한 직접적인 접근성을 제공함으로써 신규 보관 시설의 프로젝트 일정을 단축하고 있습니다. 사우디아라비아에서는 NEOM의 Oxagon이 포워딩, 창고 보관, 풀필먼트 서비스를 자동화 운송 및 디지털 가시화 기술과 결합한 통합 밸류체인 플랫폼을 구축하고 있으며, 이를 통해 화학제품 화물 흐름에서 발생하는 인터페이스상의 마찰이 완화될 것입니다. 2026년 가동을 예정하고 있는 NEOM 항구의 T1 터미널에는 자동 크레인과 온도 조절이 가능한 보관 구역이 도입되어, 안정적인 환경과 신속한 게이트 이동이 필요한 고부가가치 및 민감한 화물을 위한 핵심 거점이 조성될 예정입니다. 카타르에서는 자유무역지대 당국이 라스 부폰타스에 전 세계 화물 통합 업체들을 유치함으로써 물류 생태계를 확대했습니다. 이로 인해 국경을 넘는 네트워크와 시간 엄수 화물에 대해 신뢰할 수 있는 항공기 화물칸 공간을 필요로 하는 화학제품 취급 업체들에게 이용 가능한 선택지가 늘어나고 있습니다. 이러한 노력은 자유무역지구 내에서의 혼합, 재포장 및 시험 기능의 집적을 촉진하고 있으며, 이는 중동 화학제품 창고 시장에 유리한 환경을 조성하고 있습니다.

극단적인 기후 조건이 보관 상태를 악화시키고 냉각 비용을 증가시킵니다.

2025년, 해당 지역 전체에서 폭염과 가뭄이 복합적으로 심화되면서 과거 기준치를 웃도는 이상 기후와 강수량 부족이 동시에 발생해 냉각 시스템과 전력망에 부담이 가중되었습니다. 창고 운영자에게 있어 지속적인 고온은 가연성 액체의 증기압 위험을 높이고 저장 탱크의 부식을 가속화하기 때문에 점검 빈도와 유지보수 범위가 확대됩니다. 의약품 중간체 및 특수 농약용 온도 관리실은 엄격한 온도 범위를 유지해야 하므로, 이로 인해 에너지 소비량이 증가하게 되며, 수요가 정점에 달하는 달을 대비한 예비 용량 계획이 필요합니다. 위험 관리 분야에서는 현재 단열, 증기 관리, 그리고 위험물 구역 전체에 걸친 가스 감지를 위한 능동적 모니터링이 더욱 중요시되고 있습니다. 연료 및 전력 공급에 차질을 빚게 하는 지정학적 사태는 기후로 인한 부담을 더욱 가중시킵니다. 2026년 3월 오만에서 발생한 사건은 터미널 운영이 축소되어 화물을 우회 운송할 수밖에 없었던 사례 중 하나입니다. 이러한 상황은 안전성이 극히 중요한 보관 시설의 운영 기준을 강화시키고 있으며, 중동의 화학제품 창고 시장에서 장애 내성이 높은 냉각 및 보호 시스템에 대한 투자를 촉진하고 있습니다.

부문별 분석

2025년에는 위험물 시설이 시장 점유율의 39.41%를 차지했습니다. 이는 해당 지역의 제품 구성을 특징짓는 가연성 물질, 부식성 물질, 산화제 및 유독 물질에 대한 안전 요건에 근거한 것입니다. 이 부문에서 중동 화학제품 창고 시장의 온도 관리 시설 시장 규모는 해당 지역의 생명과학 및 특수 원료 수요 증가에 힘입어 2026-2031년 연평균 성장률(CAGR) 7.14%로 성장할 것으로 전망됩니다. 새로운 컨테이너 터미널에는 대규모 온도 관리 구역, 전기 설비 및 육상 전원이 도입되어, 이를 통해 배출량을 줄이면서 민감한 화물을 처리할 수 있게 되었습니다. 제3자 물류 업체들은 의약품 중간체 및 고순도 화학 물질의 감사 추적 요건을 충족하기 위해 보세 냉장 창고와 적합성 평가 프로토콜을 도입하고 있습니다. 위험물 취급 시설에서는 인화 및 노출 위험에 대한 규정 준수를 유지하기 위해, 거품 소화 시스템, 가스 감지 장치 및 격리형 봉쇄 설비에 대한 투자가 계속되고 있습니다. 이러한 업그레이드는 중동 화학제품 창고 시장의 프리미엄 서비스 부문을 강화하고, 고위험 구역에서의 사고 발생 가능성을 낮춥니다.

일반 화학제품 창고는 벌크 형태의 비위험 화학제품, 포장 자재 및 저위험 혼합물을 취급하는 반면, 특수 화학제품 시설은 오염 관리 및 추적 관리 시스템이 갖춰진 코팅제, 접착제 및 전자 등급 용제를 취급합니다. 온도 관리 사업을 영위하는 업체들은 구역 전체에 걸쳐 좁은 온도 범위를 유지하기 위해 매핑, 검증 및 경보 관리 시스템을 확대되고 있습니다. 항만 및 자유무역지대 주변에 모여 있는 다국적 제조업체들에게 있어, 냉장실, 플라스틱 포장 설비, 품질 검사실을 갖춘 통합형 위험물(HAZMAT) 단지는 공장에서 수출 경로로 이어지는 물류 흐름을 개선해 줍니다. 이 통합 시설은 사우디아라비아와 카타르의 새로운 생산 체계와 부합하며, 해당 지역에서는 에틸렌 및 폴리에틸렌 제품이 수출 전에 규정을 준수하는 보관 거점을 경유하게 됩니다. 제품 포트폴리오가 고부가가치이며 안전성이 극히 중요한 중간체로 다양화되는 가운데, 위험물 부문은 앞으로도 중동 화학제품 창고 시장의 핵심으로 자리매김할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the middle east chemical warehousing market size is expected to increase from USD 4.27 billion in 2025 to USD 4.52 billion in 2026 and reach USD 6.17 billion by 2031, growing at a CAGR of 6.45% over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing, and Specialty Chemical Warehouse and More), by Chemical Type (Flammable Liquids, Corrosives and More), by End-User Industry (Basic Chemicals Manufacturing, and More), and by Geography (Saudi Arabia, United Arab Emirates, Qatar, Oman, Kuwait, Bahrain, Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).

Middle East Chemical Warehousing Market Trends and Insights

Petrochemical Industry Leadership Drives Specialized Storage Demand

Large integrated complexes commissioning across the Gulf are translating into sustained throughput of feedstocks and polymers, which lifts demand for compliant bulk and packaged chemical storage. In Saudi Arabia, new mixed feed cracking and downstream units under joint ventures are scheduled to bring high volume ethylene and polyethylene capacity online, which adds steady flows of flammable liquids and finished resins that need hazardous and segregated warehousing near port and rail links. In Qatar, the Ras Laffan petrochemicals project will supply ethylene and polyethylene volumes to export markets, which creates a requirement for tankage, containerized resin storage, and handling areas that meet hazardous classification standards. The Middle East chemical warehousing market is responding with higher fire suppression densities, vapor control, and road rail interface upgrades to handle two way flows between plants and ports. Third party storage providers are also adding bonded zones and packaging lines to support resin bagging and drumming that align with export documentation and global customer specs. These actions ensure the Middle East chemical warehousing market stays synchronized with the region's core petrochemical investment cycle.

Free Zone and Economic City Development Accelerates Infrastructure Build Out

Purpose-built logistics precincts are compressing project timelines for new storage capacity by providing ready utilities, simplified licensing, and direct access to berth and yard space. In Saudi Arabia, Oxagon at NEOM is building a unified supply chain platform that combines forwarding, warehousing, and fulfillment with automated handling and digital visibility, which reduces interface friction for chemical cargo flows. The Port of NEOM's T1 terminal, targeted for 2026, will introduce automated cranes and temperature-controlled storage areas, creating an anchor node for high-value and sensitive shipments that need stable conditions and fast gate moves. In Qatar, the free zones authority has expanded its logistics ecosystem by onboarding global freight integrators to Ras Bufontas, which raises the available options for chemical handlers seeking cross-border reach and reliable belly capacity for time-sensitive consignments. These initiatives encourage the co-location of blending, repacking, and testing capabilities inside free zones, which is a favorable setup for the Middle East chemical warehousing market.

Extreme Climate Conditions Compromise Storage Integrity and Escalate Cooling Costs

Compound heat and dryness events intensified across the region in 2025, with anomalies above historical baselines and concurrent precipitation deficits that stressed cooling systems and power grids. For warehouse operators, persistent heat increases vapor pressure risks for flammable liquids and accelerates corrosion in storage vessels, which raises inspection frequency and maintenance scope. Temperature-controlled rooms for pharmaceutical intermediates and specialty agrochemicals must hold tight bands, which lift energy draw and require redundancy planning for peak months. Risk controls now place greater emphasis on insulation, vapor management, and active monitoring for gas detection across HAZMAT zones. Geopolitical events that disrupt fuel and power supply compound climate stress, as seen with the March 2026 incident in Oman that reduced terminal operations and rerouted cargo. These dynamics increase the operating baseline for safety critical storage and push the Middle East chemical warehousing market to invest in resilient cooling and protection systems.

Other drivers and restraints analyzed in the detailed report include:

- Downstream Chemical Integration Creates Captive Warehousing Demand

- Vision 2030 Economic Diversification Underpins Long Term Policy Support

- Water Scarcity and Desalination Dependency Inflate Industrial Operating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hazardous materials facilities commanded 39.41% in 2025, supported by safety requirements for flammables, corrosives, oxidizers, and toxic substances that define the region's product mix. Within this category, the Middle East chemical warehousing market size for temperature-controlled facilities is projected to expand at a 7.14% CAGR between 2026 and 2031 as life sciences and specialty inputs scale in the region. New container terminals are incorporating large temperature-controlled zones, electric equipment, and shore power, which supports the handling of sensitive cargo with lower emissions. Third-party logistics providers are adding bonded cold rooms and qualification protocols to meet audit trails for pharmaceutical intermediates and high-purity chemicals. HAZMAT sites continue to invest in foam-based fire suppression, gas detection, and segregated containment to maintain compliance against ignition and exposure risks. These upgrades reinforce premium service tiers in the Middle East chemical warehousing market and reduce incident probability in high-hazard zones.

General chemical warehouses serve bulk non-hazardous chemicals, packaging inputs, and lower-risk formulations, while specialty chemical facilities cater to coatings, adhesives, and electronic-grade solvents with contamination controls and traceability. Operators pursuing temperature-controlled business are expanding mapping, validation, and alarm management to sustain narrow bands across zones. For multinational producers that cluster near ports and free zones, integrated HAZMAT campuses with cold rooms, resin bagging, and quality labs improve flow from plant to export channels. This integrated setup aligns with new production in Saudi Arabia and Qatar, where ethylene and polyethylene output will move through compliant storage nodes before export. The hazardous materials segment will remain the anchor of the Middle East chemical warehousing market as product portfolios diversify into higher value, safety-critical intermediates.

List of Companies Covered in this Report:

- RSA TALKE

- Tristar Group

- Gulf Warehousing Company (GWC)

- Rinchem Company

- Aramex

- BDP International Logistic Services

- HOYER Group

- DHL Group

- Bertschi AG

- TLM International Freight Services LLC

- Kuehne + Nagel

- CEVA Logistics

- DSV

- Den Hartogh Logistics

- Noatum Holdings

- Azka Logistics

- Clarion Shipping

- Kanoo Logistics

- Geodis

- C.H. Robinson

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Petrochemical Capacity Build-Outs Across GCC

- 4.2.2 Vision 2030 Mega-Project Demand for Construction Chemicals

- 4.2.3 Tightening ADR/IMO-Aligned Hazmat Compliance Audits

- 4.2.4 E-Commerce Growth in Specialty Chemical Distribution

- 4.2.5 Green-Hydrogen and Ammonia Pilot Plants Needing Dedicated Storage

- 4.2.6 Duty-Free Free-Zone Cold Chains for Cell & Gene Therapies

- 4.3 Market Restraints

- 4.3.1 High Capex for Fluorine-Free Fire-Suppression Retrofits

- 4.3.2 Shortage of DG-Certified Warehouse Labor

- 4.3.3 Sand-Storm Corrosion Risk Raising Insurance Deductibles

- 4.3.4 Limited Regional Supply of OFAS-Free Foam Concentrates

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Country

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Oman

- 5.4.5 Kuwait

- 5.4.6 Bahrain

- 5.4.7 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 RSA TALKE

- 6.4.2 Tristar Group

- 6.4.3 Gulf Warehousing Company (GWC)

- 6.4.4 Rinchem Company

- 6.4.5 Aramex

- 6.4.6 BDP International Logistic Services

- 6.4.7 HOYER Group

- 6.4.8 DHL Group

- 6.4.9 Bertschi AG

- 6.4.10 TLM International Freight Services LLC

- 6.4.11 Kuehne + Nagel

- 6.4.12 CEVA Logistics

- 6.4.13 DSV

- 6.4.14 Den Hartogh Logistics

- 6.4.15 Noatum Holdings

- 6.4.16 Azka Logistics

- 6.4.17 Clarion Shipping

- 6.4.18 Kanoo Logistics

- 6.4.19 Geodis

- 6.4.20 C.H. Robinson

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment