|

시장보고서

상품코드

2063694

AI 데이터센터용 GPU : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

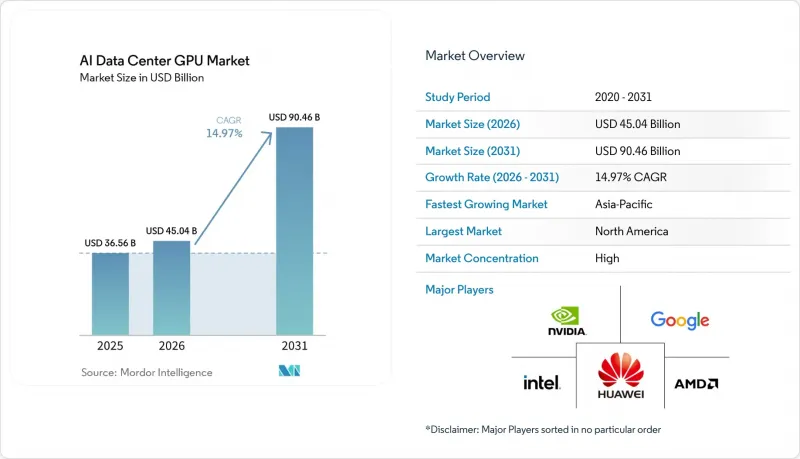

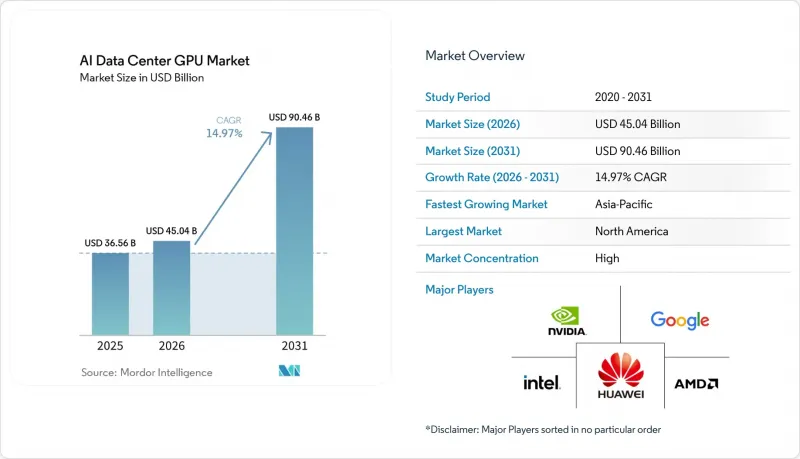

Mordor Intelligence에 의하면, AI 데이터센터용 GPU 시장 규모는 2025년 365억 6,000만 달러로 평가되었습니다. 2026년에는 450억 4,000만 달러로 확대되어 2026-2031년 CAGR은 14.97%를 나타내, 2031년까지 904억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 도입 형태(클라우드 데이터센터, 기업 및 프라이빗 데이터센터 등), GPU 유형(훈련용 GPU, 추론용 GPU), 상호 연결(PCIe 기반 GPU, 고대역폭 상호 연결 GPU), 최종 사용자(하이퍼스케일러 및 클라우드 서비스 제공업체, 기업, 정부 및 연구 기관), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 AI 데이터센터용 GPU 시장 동향 및 인사이트

생성형 AI 모델 규모의 폭발적인 확대

대규모 언어 모델이나 멀티모달 모델은 매개변수 수가 1조 개를 넘으며, 인간의 피드백을 활용한 강화 학습, 합성 데이터 확장, 장문 문맥 추론과 같은 훈련 후 확장 단계에서는 초기 사전 훈련 실행 시보다 최대 30배에 달하는 연산 자원을 소비하게 되었습니다. 따라서 운영자는 패키지에 방대한 메모리를 탑재한 GPU를 우선적으로 선택하고 있습니다. AMD의 MI325X는 288GB의 HBM3e를 탑재하고 있어, 단일 서버에서 1조 파라미터 규모의 모델을 호스팅할 수 있으며, 노드 간 샤딩으로 인한 지연을 해소합니다. NVIDIA의 Blackwell 아키텍처는 100만 토큰당 비용을 15배 개선하여 약 0.02달러까지 낮췄습니다. 이를 통해 엔터프라이즈 규모의 종량제 API의 경제성을 실현할 수 있게 되었습니다. 각 하이퍼스케일러 기업들은 사상 최대 규모의 설비 투자를 통해 이에 대응하고 있으며, 선불 계약을 통해 웨이퍼 생산 개시와 첨단 패키징 물량을 확보하고 있습니다. 이로 인해 수요가 앞당겨지면서, AI 데이터센터용 GPU 시장의 성장세가 더욱 확고해지고 있습니다.

GPU 가속 클라우드 서비스의 급속한 보급

생성형 AI를 생산성 소프트웨어에 직접 통합하면 사용자 유지율이 높고 수익성도 높다는 사실이 입증됨에 따라, 클라우드 제공업체들은 전례 없는 규모의 GPU를 확보하고 있습니다. 마이크로소프트는 4개월 동안 800만 개 이상의 유료 Gemini Enterprise 라이선스를 판매한 반면, 구글 클라우드의 매출은 2,800개 기업 고객사에 Gemini가 도입된 것을 배경으로 2025년 4분기에 전년 동기 대비 48% 급증했습니다. 이러한 워크로드는 2년 이내에 GPU 플릿에 대한 투자 비용을 회수할 수 있기 때문에 적극적인 도입을 촉진하고 있습니다. 마이크로소프트가 노르웨이의 230메가와트 규모 시설을 위해 Nscale에 3만 대의 GPU를 발주한 것과 같은 수년에 걸친 병행 공급 계약은 AI 데이터센터용 GPU 시장을 지탱하는 현금 흐름에 대한 확신을 여실히 보여주고 있습니다.

첨단 패키징 분야의 수급 불균형이 지속되고 있습니다.

고대역폭 메모리(HBM) 스택과 CoWoS 인터포저는 여전히 만성적인 공급 부족이 지속되고 있습니다. HBM의 다이 면적은 기존 DRAM의 약 2.5배이며, TSV의 복잡성으로 인해 결함률이 상승하고 있기 때문에 공급업체는 수율 저하에 대비해 웨이퍼 면적을 확보할 수밖에 없습니다. 마이크론의 2026년 HBM 생산량은 이미 매진된 상태이며, 삼성은 HBM 매출을 3배로 확대하고 있음에도 불구하고, 여전히 10%대 후반의 가격 인상을 단행하고 있으며, TSMC의 9.5 리트리 리미트 확장도 2027년까지는 CoWoS 생산 능력을 대폭 늘리지 않을 것입니다. 공급 부족으로 인해 Rubin 및 MI400의 양산이 지연되고 있으며, 공급업체는 초기 물량을 수익성이 높은 구매자에게 배정할 수밖에 없어, 중소규모의 클라우드 및 기업 사용자에 대한 공급이 늦어질 가능성이 있습니다.

부문별 분석

2025년에는 클라우드 시설이 매출의 66.38%를 차지했습니다. 이는 각각 10만 대 이상의 GPU를 수용하는 수냉식 랙 포드를 통합한, 수 기가와트 규모의 캠퍼스가 주도하고 있습니다. 기업들은 이러한 집중형 용량을 활용하여 수천 개의 테넌트 간에 컴퓨팅 비용을 분산시키고 있지만, 아웃바운드 데이터 통신 요금의 급등과 개인정보 보호 규제의 강화로 인해 일부 워크로드는 On-Premise나 국내 데이터센터로 되돌아가고 있습니다. 엣지 데이터센터는 여전히 틈새 시장으로 남아 있지만, 자율주행차, 로봇 셀, 실시간 산업용 검사 분야에서 10밀리초 미만의 왕복 지연 시간이 요구됨에 따라 2031년까지 연평균 성장률(CAGR) 15.57%를 나타낼 것으로 전망됩니다.

각 벤더사는 서로 다른 환경 간에 원활한 모델 이전을 가능하게 하기 위해 소프트웨어 재설계를 가속화하고 있습니다. 예를 들어, NVIDIA의 BlueField-4 데이터 처리 유닛(DPU) 계층은 키-값 캐시를 코어에서 에지로 터널링하여 전송함으로써 매우 중요한 역할을 수행하고 있습니다. 이러한 접근 방식을 통해 GPU 메모리의 중복 할당이 대폭 줄어들고, 리소스 활용도가 최적화됩니다. 이러한 발전들이 맞물리면서, AI 데이터센터용 GPU 시장은 두 가지 축을 중심으로 성장 궤도를 타고 있습니다. 한편 하이퍼스케일 허브가 눈부신 성장을 이루고 있는 반면, 페더레이티드 마이크로사이트 역시 기반 수준은 크게 다르지만 계속해서 확대되고 있습니다. 이러한 동향은 AI 워크로드의 진화하는 수요에 부응하기 위해 채택되고 있는 다양한 전략을 여실히 보여주고 있습니다.

추론 가속기는 2025년 매출의 54.23%를 차지했으며, 견고한 토큰 기반 수익화 모델 덕분에 훈련용 GPU를 능가하는 연평균 성장률(CAGR) 15.37%를 나타낼 전망입니다. 파인 튜닝, 리트리벌 확장 생성, 실시간 개인화가 지속적인 추론 주기를 주도하고 있으며, 이 세 가지가 현재 2026년 컴퓨팅 지출의 약 3분의 2를 차지하고 있습니다. 훈련용 GPU는 최첨단 모델 개발에 필수적이지만, 매개변수를 조금만 늘려도 성능 향상이 둔화되기 때문에 그 점유율은 감소하고 있습니다.

하드웨어 벤더들은 혼합 정밀도 파이프라인을 통해 이에 대응하고 있으며, NVIDIA Rubin은 3세대 Transformer Engine을 탑재했고, AMD MI325X는 HBM 용량을 두 배로 늘려 단일 보드에 1조 매개변수의 인터프리터를 탑재하고 있습니다. 이것들은 모두 경제성을 더욱 추론 쪽으로 기울게 하는 혁신입니다. 그 결과, 각 하이퍼스케일러 기업들은 자사의 GPU 플릿을 점점 더 양분화하고 있습니다. 최신 고성능 인터커넥트 GPU는 대규모 배치 훈련용으로 확보하고, 한편 추론 클러스터에는 토큰당 비용에 최적화된 고메모리 밀도 카드를 배치하고 있습니다.

지역별 분석

북미는 2025년 매출의 37.50%를 차지했으며, 주요 클라우드 제공업체의 본사와의 근접성은 물론 텍사스주, 중서부, 태평양 연안 북서부 지역의 풍부한 전력 공급 능력에 힘입었습니다. 미국의 정책은 여전히 국내 배분을 우선시하고 있으며, 2026년 1월 수출 규제 개정으로 인해 해외로 출하되는 특정 고성능 GPU에 25%의 관세가 부과됨에 따라, 사실상 국내 공급이 확보되었습니다. Applied Digital이 Delta Forge 1에서 체결한 300메가와트 규모의 계약과 같은 대규모 임대 계약은 미국 내 건설 사업의 장기적인 성장 잠재력을 여실히 보여주고 있습니다. 유럽은 집중적이면서도 전략적인 성장세를 보이고 있습니다. 노르웨이 나르비크에서 마이크로소프트가 체결한 3만 대 규모의 루빈(Rubin) GPU 계약은 증가하는 탄소세를 완화하기 위해 추운 지역에서 재생 에너지를 활용하는 캠퍼스에 대한 수요가 있음을 보여주고 있습니다. 영국은 5억 파운드(6억 3,000만 달러)를 ‘소버린 AI 유닛’에 투자하고, 스타트업 1곳당 100만 GPU 시간의 보조금을 지원하며, 인프라 오케스트레이션 기업에 대한 직접 투자를 약속했습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.97%를 기록하며, 지역별로는 가장 빠른 성장세를 보일 것으로 전망됩니다. 가고시마에 건설될 일본 정부의 120억 달러 규모 GMI Cloud 소버린 사이트는 1기가와트의 용량을 목표로 하고 있으며, 로봇 공학, 자율주행차, 중공업용 AI 워크로드를 위한 국내 제조 거점으로서의 입지를 확립하고자 합니다. 중국은 NVIDIA H200 칩 수입에 대한 미국의 수출 규제 강화와 통관상의 장벽에 직면해 있으며, 화웨이, 캄브리콘, 비렌을 통해 국산 가속기로의 전환을 추진하고 있습니다. 다만, 수율이나 소프트웨어 성숙도 면에서의 격차로 인해 단기적으로는 성능 면에서 뒤처질 것으로 보입니다. 한편, 인도에서는 수 메가와트 규모의 캠퍼스 승인 절차가 가속화되고 있으며, 한국의 삼성과 SK하이닉스는 GPU 밸류체인의 업스트림 단계에서 가치를 창출하기 위해 HBM4 생산 라인 확충을 추진하고 있습니다.

남미, 중동 및 아프리카는 시장 점유율은 작지만, 저비용 재생에너지 분야에서 ‘빠른 추격자’로서의 역할을 수행하고 있습니다. 2025년 5월의 정책 전환에 따라 사우디아라비아와 UAE는 ‘Validated End User(검증된 최종 사용자)’ 체제 하에서 첨단 GPU 수입을 허용했으며, 풍부한 천연가스와 태양광 자산을 활용하여 경쟁력 있는 전력 구매 계약을 체결하고 있습니다. 이 지역들은 절대적인 규모 면에서 북미나 아시아·태평양 지역과 비교할 수는 없지만, AI 데이터센터용 GPU 시장에 진출하는 업체들에게는 추가적인 성장 여지와 지리적 위험 분산 효과를 가져다줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the aI data center GPU market size is expected to grow from USD 36.56 billion in 2025 to USD 45.04 billion in 2026 and is forecast to reach USD 90.46 billion by 2031 at a 14.97% CAGR over 2026-2031.

This report is Segmented by Deployment Mode (Cloud Data Centers, Enterprise and Private Data Centers, and More), GPU Type (Training GPUs, and Inference GPUs), Interconnect (PCIe-Based GPUs, and High-Bandwidth Interconnect GPUs), End-User (Hyperscalers and Cloud Service Providers, Enterprises, and Government and Research Institutions), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI Data Center GPU Market Trends and Insights

Explosive Growth in Generative AI Model Size

Large language and multimodal models are ballooning past the trillion-parameter mark, and post-training scaling steps such as reinforcement learning from human feedback, synthetic data expansion, and long-context reasoning now consume up to 30 times the compute of the original pre-training run. Operators therefore prioritize GPUs with enormous on-package memory; AMD's MI325X offers 288 GB of HBM3e, enabling a single server to host a 1-trillion-parameter model and eliminating cross-node sharding delays. NVIDIA's Blackwell architecture improves cost per million tokens by 15-fold, down to roughly USD 0.02 per million tokens, making pay-as-you-go API economics viable at enterprise scale. Hyperscalers are responding with record capex, and prepayment contracts are locking in both wafer starts and advanced packaging slots, effectively pulling demand forward and solidifying the AI data center GPU market's growth trajectory.

Rapid Adoption of GPU-Accelerated Cloud Services

Embedding generative AI directly into productivity software is proving sticky and high-margin, prompting cloud providers to reserve unprecedented quantities of GPUs. Microsoft sold more than 8 million paid Gemini Enterprise seats within four months, while Google Cloud revenue surged 48% year-over-year in Q4 2025 on the back of Gemini roll-outs across 2,800 corporate customers. These workloads amortize GPU fleets in under two years, reinforcing aggressive procurement. Parallel multiyear supply contracts, such as Microsoft's 30,000-GPU order from Nscale for a 230-megawatt site in Norway, highlight the cash-flow confidence underpinning the AI data center GPU market.

Persistent Supply-Demand Imbalance for Advanced Packaging

High-bandwidth memory (HBM) stacks and CoWoS interposers remain in chronic shortage. HBM die areas are roughly 2.5 times those of conventional DRAM, and TSV complexity raises defect rates, forcing suppliers to reserve wafer area for yield loss. Micron's 2026 HBM output is already presold, Samsung is tripling HBM revenue yet still hiking prices by high-teens percentages, and TSMC's 9.5-reticle-limit expansion will not meaningfully lift CoWoS capacity until 2027. Scarcity slows Rubin and MI400 volume ramps and may compel vendors to allocate early lots to the highest-margin buyers, delaying access for smaller cloud and enterprise users.

Other drivers and restraints analyzed in the detailed report include:

- Data-Center-Scale GPU Clusters Crossing the 100 K-GPU Threshold

- Rise of Sovereign AI Initiatives in Smaller Economies

- Growing Preference for Custom AI Accelerators Over GPUs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud facilities accounted for 66.38% revenue in 2025, anchored by multi-gigawatt campuses that integrate liquid-cooled rack pods housing more than 100,000 GPUs each. Enterprises rely on this centralized capacity to amortize compute across thousands of tenants, but rising outbound data fees and privacy mandates are nudging some workloads back on-prem or toward sovereign centers. Edge data centers, though still niche, are forecast to expand at a 15.57% CAGR through 2031 as autonomous vehicles, robotic cells, and real-time industrial inspection demand sub-10-millisecond round-trip latency.

Vendors are increasingly re-architecting software to facilitate seamless model migration across different environments. For instance, NVIDIA's BlueField-4 Data Processing Unit (DPU) layer plays a pivotal role by tunneling key-value caches from the core to the edge. This approach significantly reduces redundant GPU memory allocations, thereby optimizing resource utilization. Collectively, these advancements are driving the AI data center GPU market along a dual-track scaling trajectory. On one hand, hyperscale hubs are witnessing substantial growth, while on the other, federated micro-sites are also expanding, albeit starting from vastly different foundational levels. These developments highlight the diverse strategies being adopted to meet the evolving demands of AI workloads.

Inference accelerators accounted for 54.23% of 2025 revenue and will grow faster than training GPUs, with a 15.37% CAGR, thanks to steady, token-based monetization models. Fine-tuning, retrieval-augmented generation, and real-time personalization drive continuous inference cycles that now represent roughly two-thirds of 2026 compute spend. Training GPUs remain indispensable for frontier model creation, but their share erodes as marginal parameter increases yield diminishing performance gains.

Hardware vendors are responding with mixed-precision pipelines, NVIDIA Rubin packs a third-generation Transformer Engine, and AMD MI325X doubles HBM capacity to squeeze trillion-parameter interpreters onto a single board, both innovations that tilt economics further toward inference. As a result, hyperscalers increasingly bifurcate their fleets, reserving the newest interconnect-rich GPUs for large-batch training while backfilling inference clusters with memory-dense cards optimized for cost per token.

Geography Analysis

North America retained 37.50% of 2025 revenue, buoyed by the proximity of top cloud providers' headquarters and abundant power capacity in Texas, the Midwest, and the Pacific Northwest. U.S. policy continues to favor domestic allocation: January 2026 export-control revisions imposed a 25% tariff on certain high-end GPUs shipped abroad, effectively preserving local supply. Mega-leases such as Applied Digital's 300-megawatt deal at Delta Forge 1 underscore the long-term runway for U.S.-based construction. Europe follows with concentrated but strategic growth; Microsoft's 30,000-Rubin-GPU contract in Narvik, Norway, reveals appetite for cold-climate, renewable-powered campuses that mitigate rising carbon taxes. The United Kingdom is channeling GBP 500 million (USD 630 million) into its Sovereign AI Unit, pledging one-million-GPU-hour grants per startup and direct equity stakes in infrastructure orchestration firms.

Asia-Pacific is projected to log the fastest regional expansion at a 15.97% CAGR through 2031. Japan's USD 12 billion GMI Cloud sovereign site in Kagoshima aims for 1 gigawatt of capacity, positioning the country as a domestic manufacturing hub for robotics, autonomous vehicles, and heavy-industry AI workloads. China, facing tightened U.S. export rules and customs hurdles on imports of NVIDIA H200 chips, is pivoting toward homegrown accelerators from Huawei, Cambricon, and Biren, even though yield and software maturity gaps suggest short-term performance lags. Elsewhere, India accelerates approvals for multi-megawatt campuses, while Samsung and SK Hynix in South Korea ramp HBM4 lines to capture value upstream in the GPU supply chain.

South America, the Middle East, and Africa hold smaller shares but serve as fast-follower destinations for low-cost renewable energy. Policy shifts in May 2025 opened Saudi Arabia and the UAE to advanced GPU imports under a Validated End User framework, leveraging their vast natural gas and solar assets to deliver competitive power purchase agreements. Although these regions will not challenge the scale of North America or Asia-Pacific in absolute dollars, they offer incremental upside and geographic risk diversification for vendors marketing into the AI data center GPU market.

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Google LLC

- Amazon Web Services, Inc.

- Microsoft Corporation

- Alibaba Group Holding Limited

- Baidu, Inc.

- Huawei Technologies Co., Ltd.

- Graphcore Ltd.

- SambaNova Systems, Inc.

- Cerebras Systems Inc.

- Tenstorrent Inc.

- Qualcomm Technologies, Inc.

- IBM Corporation

- Giga Computing Technology Co., Ltd.

- Super Micro Computer, Inc.

- ASUStek Computer Inc.

- Dell Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Growth in Generative AI Model Size

- 4.2.2 Rapid Adoption of GPU-Accelerated Cloud Services

- 4.2.3 Data-Center-Scale GPU Clusters Crossing the 100K-GPU Threshold

- 4.2.4 Standardization of MLPerf Benchmarks in Procurement

- 4.2.5 Rise of Sovereign AI Initiatives in Smaller Economies

- 4.2.6 Liquid-Cooling Retrofits Driving Refresh Sales

- 4.3 Market Restraints

- 4.3.1 Persistent Supply-Demand Imbalance for Advanced Packaging

- 4.3.2 Escalating Total Cost of Ownership for Air-Cooled Racks

- 4.3.3 Export Control Restrictions on High-End GPUs

- 4.3.4 Growing Preference for Custom AI Accelerators Over GPUs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise and Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By End-User

- 5.4.1 Hyperscalers and Cloud Service Providers

- 5.4.2 Enterprises

- 5.4.3 Government and Research Institutions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Google LLC

- 6.4.5 Amazon Web Services, Inc.

- 6.4.6 Microsoft Corporation

- 6.4.7 Alibaba Group Holding Limited

- 6.4.8 Baidu, Inc.

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 Graphcore Ltd.

- 6.4.11 SambaNova Systems, Inc.

- 6.4.12 Cerebras Systems Inc.

- 6.4.13 Tenstorrent Inc.

- 6.4.14 Qualcomm Technologies, Inc.

- 6.4.15 IBM Corporation

- 6.4.16 Giga Computing Technology Co., Ltd.

- 6.4.17 Super Micro Computer, Inc.

- 6.4.18 ASUStek Computer Inc.

- 6.4.19 Dell Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment