|

시장보고서

상품코드

2065487

아시아태평양의 데이터센터 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

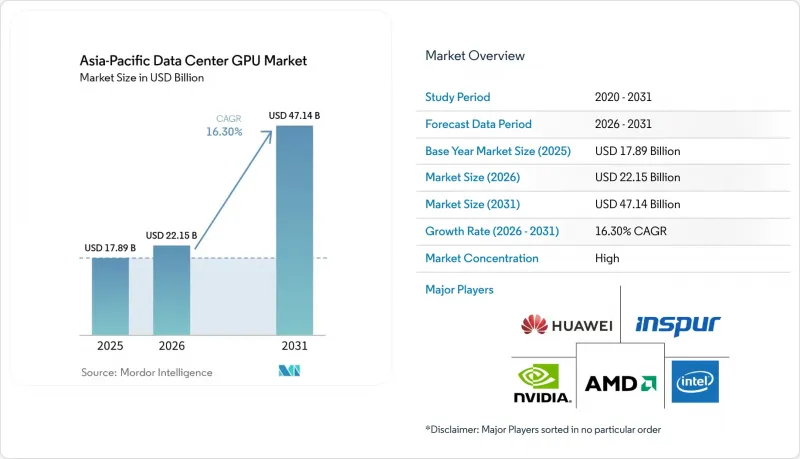

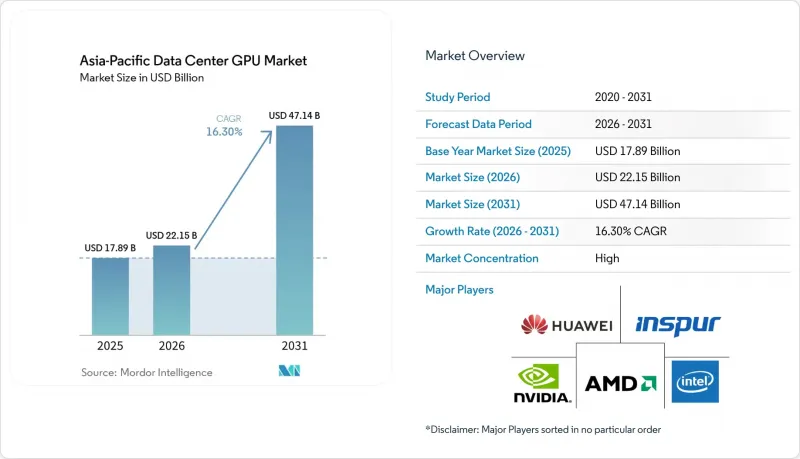

Mordor Intelligence에 의하면, 아시아태평양의 데이터센터 GPU 시장 규모는 2025년 178억 9,000만 달러로 평가되었고, 2026년 221억 5,000만 달러로 추정되고, 2031년까지 471억 4,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 16.3%를 나타낼 것으로 예측됩니다.

본 보고서는 도입 형태별(클라우드 데이터센터 등), GPU 유형별(훈련용 GPU 및 추론용 GPU), 상호 연결 방식별(PCIe 기반 GPU 및 고대역폭 상호 연결 GPU), 워크로드 유형별(AI 및 ML, HPC, 기타), 최종 사용자별(하이퍼스케일러/CSP, 기업, 기타), 국가별(중국, 일본, 한국, 인도, 기타)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

아시아태평양의 데이터센터 GPU 시장 동향 및 인사이트

하이퍼스케일 클라우드 데이터센터에서 AI 훈련 워크로드의 급증

각 하이퍼스케일 제공업체들은 1조 파라미터 규모의 모델 훈련을 지원하기 위해 10만 대 이상의 가속기를 갖춘 클러스터를 구축하고 있습니다. 마이크로소프트와 OpenAI가 추진하는 획기적인 1,000억 달러 규모의 ‘Stargate’ 프로젝트는 미국을 거점으로 하고 있지만, 동등한 규모 달성을 목표로 하는 지역 기업들에게 새로운 기준을 제시했습니다. 텐센트 클라우드는 국내 LLM 개발자들의 급증하는 수요에 대응하기 위해 2025년에 인프라를 확장할 예정이며, 바이두의 ‘Wenxin’ 플랫폼은 하루 2억 명의 사용자에게 1초 미만의 응답 속도를 유지하기 위해 H100 카드를 지속적으로 추가하고 있습니다. 클라우드 사업자들이 아시아태평양을 세계 최대의 AI 컴퓨팅 허브로 자리매김하는 가운데, 2026년에는 이 지역의 설비 투자액이 전 세계 하이퍼스케일러 예산 5,270억 달러 중 상당한 비중을 차지할 것으로 예측됩니다. 클라우드를 통해 제공되는 GPU-as-a-Service(GPUaaS) 제품은 출시 주기를 단축하는 한편, 가격 결정권을 소수공급업체에 집중시켜 대규모 계약을 확보하지 못하는 중소 경쟁사들에게 압박을 가하고 있습니다.

‘소버린 AI 클라우드’의 부상으로 인해, 지역 내 GPU 클러스터에 대한 수요가 증가하고 있습니다.

현재 각국 정부는 기밀성이 높은 AI 워크로드를 국내 인프라에서 실행할 것을 요구하고 있습니다. 일본 디지털청은 후지쯔 및 마이크로소프트와 협력하여 2024년에 1조 6,000억 엔(103억 달러)을 투자해 주권형 클라우드 존 구축에 착수했습니다. 인도의 ‘반도체 미션 2.0’ 역시 같은 해 108억 달러를 배정하여, 2030년까지 수입 GPU에 대한 의존도를 40% 줄이는 것을 목표로 하고 있습니다. 중국은 2025년에, 2027년까지 정부의 AI 추론 처리를 Ascend GPU로 전환하도록 의무화하는 지침을 발표했으며, 연간 수천 대 규모의 국내 출하를 보장했습니다. 이러한 병렬 아키텍처에서는 공급자가 주권형 테넌트와 상용 테넌트를 위해 각각 전용 풀을 유지해야 하기 때문에 인프라에 대한 지출이 두 배로 늘어나고 규모의 경제 효과가 약화됩니다.

최신 GPU에 대한 접근을 제한하는 수출 규제

2023년 10월 워싱턴이 발표한 규제에 따라 H200급 GPU의 중국 내 판매가 금지되었으며, 성능 상한선은 H100 수준으로 제한되고 있습니다. 2025년에 부과된 25%의 관세로 인해 구매 가격은 더욱 치솟고 있습니다. 이에 반해, ByteDance와 Alibaba는 2025년을 목표로 Huawei Ascend 910C 60만 대를 발주했으나, 각 칩의 처리량은 H100 트랜스포머의 60-70% 수준에 그치기 때문에 과잉 조달을 피할 수 없는 상황입니다. 라이선싱 절차에 6-12개월의 지연이 발생함에 따라, 대학 및 연구 기관의 계획에 대한 불확실성이 더욱 커지고 있습니다.

부문별 분석

2025년, 아시아태평양의 데이터센터 GPU 시장 점유율 중 63.45%를 클라우드 시설이 차지했습니다. 이는 하이퍼스케일러의 타의 추종을 불허하는 구매력과 멀티테넌트의 경제성을 반영한 것입니다. 한편, 엣지 사이트는 10밀리초 미만의 응답 루프가 필요한 5G의 밀집화에 힘입어 2031년까지 연평균 성장률(CAGR) 17.88%로 성장을 지속하고, 있습니다. 또한, 은행이나 제약 기업들이 데이터 상주 요건을 충족하기 위해 추론 처리를 사내에서 수행하려는 움직임에 따라, 민간 기업의 데이터센터와 관련된 아시아태평양의 데이터센터 GPU 시장 규모도 확대되고 있습니다.

집중형 클라우드 클러스터의 이용률은 85% 이상에 달하고, 가격 면에서 우위를 점하고 있는 반면, 엣지 환경에서는 AR 내비게이션이나 스마트 팩토리 제어 등 지연 시간에 민감한 새로운 서비스를 통한 수익화가 진행되고 있습니다. 기업은 정책 관리를 완벽하게 유지하면서 온프레미스 클러스터의 규모를 최소화할 수 있으며, 이는 기밀성이 높은 워크로드나 더 엄격한 개인정보 보호법이 적용되는 지역에 있어 매력적인 선택지가 됩니다.

추론 가속기는 2025년에 아시아태평양 데이터센터 GPU 시장 점유율의 58.77%를 차지한 것으로 평가되었으며, 워크로드가 모델 연구 단계에서 운영 환경으로 전환됨에 따라 2031년까지 연평균 성장률(CAGR) 17.24%로 성장할 전망입니다. 훈련용 GPU는 최첨단 모델에 있어 여전히 필수적이지만, 훈련이 완료된 모델 하나가 수백만 건의 추론 호출을 처리하게 되므로 그 비중은 줄어들고 있습니다.

NVIDIA의 L4 및 L40S, AMD의 MI300X, 화웨이의 Ascend 310은 H100 훈련용 칩에 비해 전력 소비량과 가격이 낮습니다. INT8 및 INT4 양자화 기술 덕분에 아시아태평양의 데이터센터용 추론용 GPU 시장은 지속적인 성장을 보이고 있으며, 이를 통해 구형 보드도 경쟁력을 유지하면서 토큰당 전력 소비를 줄일 수 있게 되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the asia-Pacific data center GPU market size is projected to expand from USD 17.89 billion in 2025 and USD 22.15 billion in 2026 to USD 47.14 billion by 2031, registering a 16.3% CAGR between 2026 and 2031.

This report is Segmented by Deployment Type (Cloud Data Centers, and More), GPU Type (Training GPUs and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), End-User (Hyperscalers/CSPs, Enterprises, and More), and by Country (China, Japan, South Korea, India, and More). The Market Forecasts are Provided in Value (USD).

Asia-Pacific Data Center GPU Market Trends and Insights

Surge in AI Training Workloads in Hyperscale Cloud Data Centers

Hyperscale providers are rolling out clusters with more than 100,000 accelerators to support trillion-parameter model training. Microsoft and OpenAI's landmark USD 100 billion Stargate project, though U.S.-based, set the bar for regional players racing to reach comparable scale. Tencent Cloud expanded its fleet in 2025 to meet skyrocketing demand from domestic LLM developers, and Baidu's Wenxin platform added continuous batches of H100 cards to keep sub-second response for 200 million daily users. Regional capital-expenditure outlays are on pace to claim a significant share of the global USD 527 billion hyperscaler budget in 2026 as cloud operators position Asia-Pacific as the world's largest AI compute hub. Cloud-delivered GPU-as-a-Service products shorten launch cycles but concentrate pricing power in a handful of vendors, pressuring smaller rivals unable to secure volume contracts.

Rise of Sovereign AI Clouds Demanding In-Region GPU Clusters

Governments now require sensitive AI workloads to run on domestic infrastructure. Japan's Digital Agency, working with Fujitsu and Microsoft, committed JPY 1.6 trillion (USD 10.3 billion) in 2024 to build sovereign cloud zones. India's Semiconductor Mission 2.0 allocated USD 10.8 billion the same year, aiming to reduce reliance on imported GPUs by 40% before 2030. China issued directives in 2025 mandating that government AI inference migrate to Ascend GPUs by 2027, guaranteeing thousands of annual domestic shipments. Such parallel architectures double infrastructure outlays because providers must maintain dedicated pools for sovereign and commercial tenants, diluting economies of scale.

Export Control Regulations Limiting Access to Latest GPUs

Washington's October 2023 rules block H200-class GPU sales to China, capping performance ceilings at H100 equivalents. Tariffs of 25% imposed in 2025 further inflate acquisition prices. ByteDance and Alibaba responded by booking 600,000 Huawei Ascend 910C units for 2025, yet each chip delivers only 60-70% of the H100 transformer's throughput, prompting over-provisioning. License processing delays of six to twelve months amplify planning uncertainty for universities and research labs.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Domestic AI Semiconductor Manufacturing in the Asia-Pacific

- Expansion of Edge Data Centers for 5G and IoT Traffic

- High Capital Expenditure for GPU-Based Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud venues accounted for 63.45% of the Asia-Pacific data center GPU market share in 2025, reflecting hyperscalers' unmatched buying power and multitenancy economics. Edge sites, however, post a 17.88% CAGR through 2031, spurred by 5G densification that requires sub-10-millisecond response loops. The Asia-Pacific data center GPU market size tied to private enterprise data centers also expands, as banks and pharmaceutical firms internalize inference to meet data residency.

Centralized cloud clusters reach utilization above 85%, enabling price leadership, while edge rollouts monetize new latency-sensitive services such as AR wayfinding and smart-factory controls. Enterprises can keep on-prem clusters smaller while maintaining full policy control, an attractive option for confidential workloads and regions subject to stricter privacy laws.

Inference accelerators captured 58.77% of the Asia-Pacific data center GPU market share in 2025 and will grow at a 17.24% CAGR through 2031 as workloads migrate from model research to production. Training GPUs remain indispensable for frontier models, yet their share declines as every trained model fuels millions of inference calls.

NVIDIA's L4 and L40S, AMD's MI300X, and Huawei's Ascend 310 offer lower power draw and price points than H100 training silicon. The Asia-Pacific data center GPU market for inference continues to grow, thanks to INT8 and INT4 quantization, enabling older boards to remain competitive while driving down watts per token.

List of Companies Covered in this Report:

- Nvidia Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Huawei Technologies Co. Ltd.

- Tencent Cloud

- Baidu Inc.

- Amazon Web Services Inc.

- Microsoft Corporation

- Google LLC

- Samsung Electronics Co. Ltd.

- Inspur Group

- Giga Computing Technology Co. Ltd.

- Super Micro Computer Inc.

- Lenovo Group Limited

- NEC Corporation

- H3C Technologies Co. Ltd.

- Fujitsu Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in AI Training Workloads in Hyperscale Cloud Data Centers

- 4.2.2 Expansion of Edge Data Centers for 5G and IoT Traffic

- 4.2.3 Government Incentives for Domestic AI Semiconductor Manufacturing in Asia-Pacific

- 4.2.4 Adoption of Liquid Cooling Enabling Higher GPU Rack Density

- 4.2.5 Rise of Sovereign AI Clouds Demanding In-Region GPU Clusters

- 4.2.6 Corporate Sustainability Targets Driving GPU Consolidation for Energy Efficiency

- 4.3 Market Restraints

- 4.3.1 Ongoing Supply Chain Constraints for Advanced GPU Packaging

- 4.3.2 High Capital Expenditure for GPU-Based Infrastructure

- 4.3.3 Export Control Regulations Limiting Access to Latest GPUs

- 4.3.4 Skill Gap in Optimizing GPU Workloads Among Enterprise IT Teams

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

- 5.6 By Country

- 5.6.1 China

- 5.6.2 Japan

- 5.6.3 South Korea

- 5.6.4 India

- 5.6.5 Southeast Asia

- 5.6.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nvidia Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Huawei Technologies Co. Ltd.

- 6.4.5 Tencent Cloud

- 6.4.6 Baidu Inc.

- 6.4.7 Amazon Web Services Inc.

- 6.4.8 Microsoft Corporation

- 6.4.9 Google LLC

- 6.4.10 Samsung Electronics Co. Ltd.

- 6.4.11 Inspur Group

- 6.4.12 Giga Computing Technology Co. Ltd.

- 6.4.13 Super Micro Computer Inc.

- 6.4.14 Lenovo Group Limited

- 6.4.15 NEC Corporation

- 6.4.16 H3C Technologies Co. Ltd.

- 6.4.17 Fujitsu Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment