|

시장보고서

상품코드

2065489

유럽의 데이터센터 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

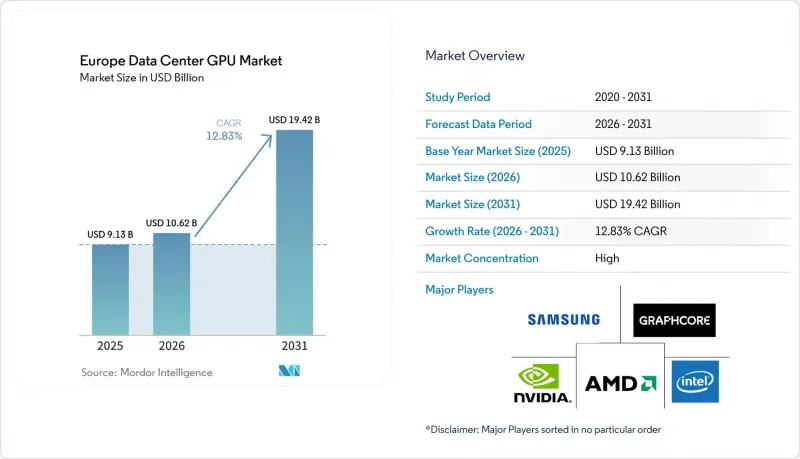

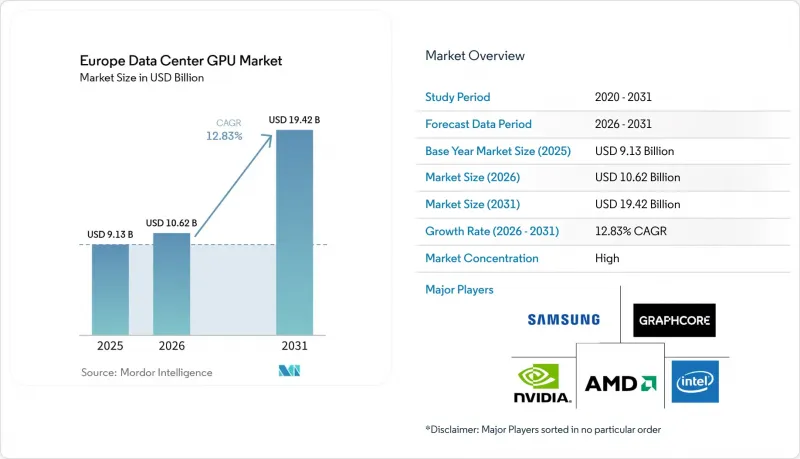

Mordor Intelligence에 의하면, 유럽의 데이터센터 GPU 시장은 2026년 106억 2,000만 달러로 추정되고, 2031년까지 194억 2,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 12.83%를 나타낼 것으로 예측됩니다.

본 보고서는 도입 형태별(클라우드 데이터센터 등), GPU 유형별(훈련용 GPU 및 추론용 GPU), 상호 연결 방식별(PCIe 기반 GPU 및 고대역폭 상호 연결 GPU), 워크로드 유형별(AI 및 ML, HPC, 기타), 최종 사용자별(하이퍼스케일러/CSP, 기업, 기타), 국가별(독일, 영국, 프랑스, 이탈리아, 기타)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

유럽의 데이터센터 GPU 시장 동향 및 인사이트

유럽 전역의 하이퍼스케일 캠퍼스에서 AI 모델 학습 능력에 대한 수요가 가속화되고 있습니다.

하이퍼스케일 사업자들은 파운데이션 모델(Foundation Model) 훈련에 수반되는 높은 계산 부하를 감당하기 위해 1만 대 이상의 가속기를 갖춘 GPU 클러스터를 가동하고 있으며, 뮌헨, 파리 및 북유럽 국가들에 이를 도입함으로써 지역별 엑사스케일 수준이 향상되고 있습니다. 유연한 전력 계약과 저탄소 전력망이 북유럽으로의 자본 유치를 촉진하는 한편, 독일과 프랑스의 주권 클라우드 규제로 인해 이 용량의 상당 부분이 국내 관리 하에 남게 될 것이 보장됩니다. 이러한 클러스터의 규모를 구현하기 위해서는 NVLink 6과 같은 고대역폭 패브릭이 필수적이며, 이를 통해 올 리듀스(all-reduce)의 지연 시간이 단축되고 GPU 활용도가 90% 이상으로 유지됩니다. 이러한 투자들이 맞물리면서, 상호 보완적인 상호 연결 기술, 냉각 시스템, 온프레미스 AI 서비스의 대상 시장이 확대되어 유럽 데이터센터 GPU 시장을 견인하고 있습니다. 그러나 한편으로는 첨단 패키징 과정에서 병목 현상에 노출될 위험도 커지고 있어, 사업자들은 공급 리스크를 헤지하기 위해 여러 공급업체와 계약을 체결할 수밖에 없는 실정입니다.

금융 서비스 및 통신 분야에서 GPU 기반 분석 플랫폼의 도입 확대

은행과 통신 사업자들은 부정 감지, 리스크 모델링, 네트워크 최적화 파이프라인에 GPU를 도입하여 추론 시간을 수 분에서 밀리초 단위로 단축하고 있습니다. 도이치은행, ING, 보다폰, 오렌지 등 각사는 분석 워크로드를 GPU 클러스터로 이전한 후 지연 시간이 두 자릿수만큼 개선되었다고 보고하며, 가속기 업그레이드에 대한 투자 대비 효과를 입증하고 있습니다. 유럽 네트워크를 통해 전송되는 트랜잭션 데이터와 텔레메트리 데이터가 급증함에 따라 실시간 처리가 필수적이 되었으나, CPU만으로 구성된 플랫폼으로는 이를 비용 효율적으로 유지할 수 없습니다. 그 결과, 유럽의 데이터센터 GPU 시장은 정기적인 하드웨어 업데이트 주기, 소프트웨어 스택의 통합, 그리고 규제 산업에 맞춤화된 관리형 서비스 제공의 혜택을 누리고 있습니다. 오픈소스 프레임워크에 대한 벤더의 지원 덕분에 도입 장벽이 더욱 낮아져, 소규모 기관에서도 독점 기술에 얽매이지 않고 GPU 가속을 활용할 수 있게 되었습니다.

대만 및 한국의 첨단 패키징 분야 공급망 집중 위험

CoWoS 및 HBM3e의 생산 능력 제약으로 인해 주력 GPU의 납기 기간이 50주 이상으로 길어지면서, 유럽의 클라우드 및 조사 프로젝트 추진 일정에 차질이 빚어지고 있습니다. Samsung Electronics와 SK하이닉스가 북미의 대규모 계약을 우선시하고 있기 때문에 EU의 사업자들은 대체 공급업체나 구형 GPU SKU를 고려할 수밖에 없는 상황입니다. 이러한 공급 부족으로 인해 현물 시장 가격이 상승하면서, 유럽 데이터센터 GPU 시장 전반에서 프로젝트 이익률이 압박을 받고 있으며, 수익 인식이 지연되고 있습니다. 듀얼 소싱 전략이나 재고 완충량 확보와 같은 긴급 대책을 통해 위험은 부분적으로 완화되지만, 운전 자금 부담이 증가하고 있습니다.

부문별 분석

엣지 시설은 2025년 매출에서 차지한 비중은 미미했으나, 연평균 성장률(CAGR) 14.66%를 기록하며 유럽 데이터센터 GPU 시장 평균을 상회하는 성장이 예상됩니다. 이러한 급속한 보급의 배경에는 자율주행차의 텔레메트리, 산업용 IoT의 센서 융합, 증강현실(AR) 스트리밍 등이 있으며, 이들 모두 왕복 지연 시간이 10밀리초 미만이어야 합니다. 클라우드 캠퍼스는 2025년 매출의 55.67%를 차지하며, 이는 독일과 프랑스에 기반을 둔 하이퍼스케일 훈련 클러스터 및 멀티테넌트형 추론 팜을 반영한 것입니다. 나머지 부분은 기밀성이 높은 금융 데이터나 의료 데이터에 대해 온프레미스 GPU 사용을 권장하는 규정 준수 요건의 영향으로, 기업 및 프라이빗 클라우드가 차지하고 있습니다.

엣지 배포에서는 마이크로 모듈식 설계, 팬리스 수냉식 냉각, 그리고 추론을 가입자에게 더 가깝게 제공하는 실시간 오케스트레이션 스택이 활용되고 있습니다. 통신 사업자들은 5G 기지국에 GPU가 탑재된 노드를 도입해 대역폭을 동적으로 분할하는 한편, 소매 체인들은 쇼핑객 분석을 강화하기 위해 매장 내 컴퓨터 비전 시스템의 시범 운영을 진행하고 있습니다. 이에 대응하여 클라우드 제공업체는 분산형 추론 서비스를 제공함으로써, 중앙 캠퍼스와 지역 집약 지점을 아우르는 하이브리드 아키텍처를 구축하고 있습니다. 이러한 분산형 패턴은 유럽 데이터센터 GPU 시장의 잠재적 시장을 대도시권 허브를 넘어 확장시키고 있으며, 전문 통합업체와 통신사 중립적 교환 플랫폼에 새로운 기회를 제공합니다.

2025년 매출액 중 훈련용 GPU가 59.87%를 차지한 것으로 평가되었습니다. 이는 멀티랙 클러스터가 기반 모델 개발을 주도하고 있기 때문이지만, 기업들이 예산을 생산 환경 도입으로 전환함에 따라 추론 가속기의 연평균 성장률(CAGR)은 14.78%를 나타낼 것으로 예측됩니다. NVIDIA의 L40S 및 L4는 챗봇 및 사기 감지 분야에서 와트당 고성능을 추구하는 엣지 및 엔터프라이즈 시장의 구매자들을 사로잡고 있습니다. AMD의 MI300X는 프랑크푸르트와 파리에 위치한 CoreWeave 및 Lambda Labs의 거점에서 훈련과 추론 모두에 대해 비용 효율적인 대안을 제공합니다.

은행은 현재 증분 설비 투자의 대부분을 추론에 할당하고 있으며, 클라우드 캠퍼스로의 네트워크 왕복 통신 없이도 초당 수백만 건의 트랜잭션을 처리할 수 있는 대용량 메모리가 탑재된 GPU를 배정하고 있습니다. 통신 사업자들은 지연 시간과 에너지 효율을 우선시하며, PCIe의 오버헤드를 최소화하기 위해 패키지 내 네트워크 기능을 갖춘 가속기를 선택하고 있습니다. 훈련은 하이퍼스케일러와 연구 기관에 있어 여전히 매우 중요하지만, 성숙한 모델이 추론 중심의 라이프사이클 단계로 전환됨에 따라 그 비중은 줄어들고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the europe data center GPU market is expected to grow from USD 10.62 billion in 2026 to USD 19.42 billion by 2031, at a 12.83% CAGR over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, and More), GPU Type (Training GPUs and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), End-User (Hyperscalers/CSPs, Enterprises, and More), and by Country (Germany, United Kingdom, France, Italy, and More). The Market Forecasts are Provided in Value (USD).

Europe Data Center GPU Market Trends and Insights

Accelerating Demand for AI Model Training Capacity Across European Hyperscale Campuses

Hyperscale operators are commissioning GPU clusters with more than 10,000 accelerators to meet the compute intensity of foundation-model training, with deployments in Munich, Paris, and the Nordic states pushing regional exascale thresholds. Flexible power contracts and low-carbon grids attract capital to Northern Europe, while sovereign-cloud rules in Germany and France ensure that a sizeable share of this capacity remains domestically controlled. The scale of these clusters necessitates high-bandwidth fabrics such as NVLink 6, which reduces all-reduce latency and keeps GPU utilization above 90%. Collectively, these investments expand the addressable market for complementary interconnects, cooling systems, and on-premises AI services, boosting the European data center GPU market. However, they also magnify exposure to advanced packaging bottlenecks, compelling operators to secure multi-vendor contracts to hedge supply risk.

Growing Adoption of GPU-Powered Analytics Platforms in Financial Services and Telecom Sectors

Banks and carriers are embedding GPUs into fraud-detection, risk-modeling, and network-optimization pipelines, trimming inference times from minutes to milliseconds. Deutsche Bank, ING, Vodafone, and Orange each reported double-digit latency improvements after migrating analytical workloads to GPU clusters, validating the return on investment for accelerator upgrades. The surge of transactional and telemetry data streaming through European networks necessitates real-time processing, which CPU-only platforms cannot sustain cost-effectively. As a result, the Europe data center GPU market benefits from recurring hardware refresh cycles, software stack integrations, and managed service offerings tailored to regulated industries. Vendor support for open-source frameworks further lowers adoption barriers, allowing smaller institutions to harness GPU acceleration without proprietary lock-in.

Supply Chain Concentration Risk Around Advanced Packaging in Taiwan and South Korea

CoWoS and HBM3e capacity constraints extend delivery lead times for flagship GPUs beyond 50 weeks, disrupting rollout schedules for European cloud and research projects. Samsung and SK hynix prioritize larger North American contracts, compelling EU operators to consider alternative vendors or older GPU SKUs. The shortage inflates spot-market pricing, narrowing project margins and delaying revenue recognition across the Europe data center GPU market. Contingency actions, such as dual-sourcing strategies and inventory buffers, partially mitigate risk but add working-capital burdens.

Other drivers and restraints analyzed in the detailed report include:

- EU Green Deal Incentives Pushing Energy-Efficient GPU Upgrades in Data Centers

- Rising Uptake of Sovereign Cloud Initiatives Requiring On-Prem GPU Clusters

- High Electricity Prices in Key European Colocation Hubs Denting TCO Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge facilities contributed a modest slice of 2025 revenue, yet are projected to outpace the Europe data center GPU market average with a 14.66% CAGR. Rapid adoption stems from autonomous-vehicle telemetry, industrial IoT sensor fusion, and augmented-reality streaming, all of which require under 10 ms round-trip latency. Cloud campuses retained 55.67% of turnover in 2025, reflecting hyperscale training clusters and multi-tenant inference farms anchored in Germany and France. Enterprises and private clouds fill the remainder, driven by compliance mandates favoring on-prem GPUs for sensitive financial and healthcare data.

Edge deployments benefit from micro-modular designs, fanless liquid cooling, and real-time orchestration stacks that push inference closer to subscribers. Telcos deploy GPU-enabled nodes at 5G base stations to dynamically slice bandwidth, while retail chains pilot in-store computer vision systems to enhance shopper analytics. Cloud providers respond by offering distributed inference services, creating hybrid architectures that span central campuses and regional aggregation points. This decentralized pattern expands the addressable market for Europe data center GPU markets beyond metropolitan hubs, unlocking opportunities for specialized integrators and carrier-neutral exchanges.

Training GPUs accounted for 59.87% of 2025 sales because multi-rack clusters powered foundation-model development, but inference accelerators are forecast to post a 14.78% CAGR as enterprises shift budgets toward production deployment. NVIDIA's L40S and L4 attract edge and enterprise buyers seeking high performance per watt for chatbots and fraud detection. AMD's MI300X provides a lower-cost path for both training and inference at CoreWeave and Lambda Labs sites in Frankfurt and Paris.

Banks now channel most incremental capex toward inference, allocating memory-rich GPUs that handle millions of transactions per second without network round-trips to cloud campuses. Telecom operators prioritize latency and energy efficiency, selecting accelerators with on-package networking to minimize PCIe overhead. Training remains mission-critical for hyperscalers and research institutes, but its proportional share declines as mature models age into inference-heavy life-cycle phases.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Samsung Electronics Co. Ltd.

- International Business Machines Corporation

- Atos SE

- Inspur Group Co. Ltd.

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Lenovo Group Limited

- Giga Computing Technology Co. Ltd.

- Graphcore Ltd.

- OVH Groupe SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating demand for AI model training capacity across European hyperscale campuses

- 4.2.2 Growing adoption of GPU-powered analytics platforms in financial services and telecom sectors

- 4.2.3 EU Green Deal incentives pushing energy-efficient GPU upgrades in data centers

- 4.2.4 Rising uptake of sovereign cloud initiatives requiring on-prem GPU clusters

- 4.2.5 Emergence of liquid-cooling retrofits enabling higher GPU rack densities

- 4.2.6 Proliferation of synthetic data generation startups driving burst GPU leasing

- 4.3 Market Restraints

- 4.3.1 Supply chain concentration risk around advanced packaging in Taiwan and South Korea

- 4.3.2 High electricity prices in key European colocation hubs denting TCO economics

- 4.3.3 Emerging EU chip-sovereignty rules complicating cross-border GPU fleet sharing

- 4.3.4 Growing scrutiny over water usage for liquid-cooled GPU farms in drought-prone regions

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Samsung Electronics Co. Ltd.

- 6.4.5 International Business Machines Corporation

- 6.4.6 Atos SE

- 6.4.7 Inspur Group Co. Ltd.

- 6.4.8 Hewlett Packard Enterprise Company

- 6.4.9 Dell Technologies Inc.

- 6.4.10 Lenovo Group Limited

- 6.4.11 Giga Computing Technology Co. Ltd.

- 6.4.12 Graphcore Ltd.

- 6.4.13 OVH Groupe SAS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment