|

시장보고서

상품코드

2065499

영국의 데이터센터 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United Kingdom Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

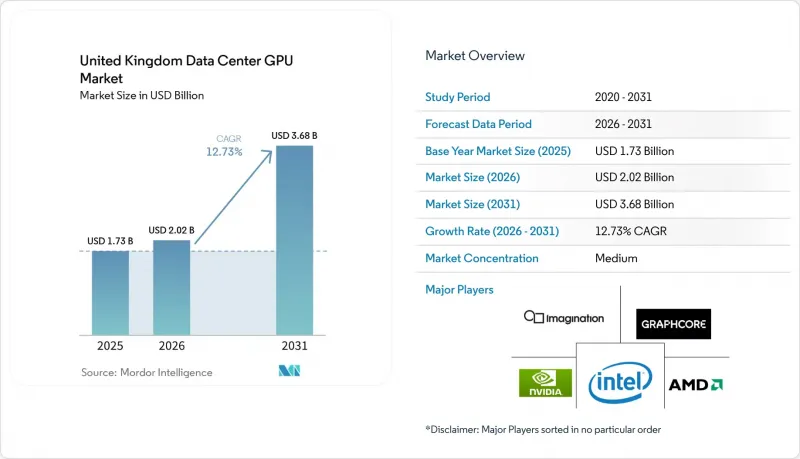

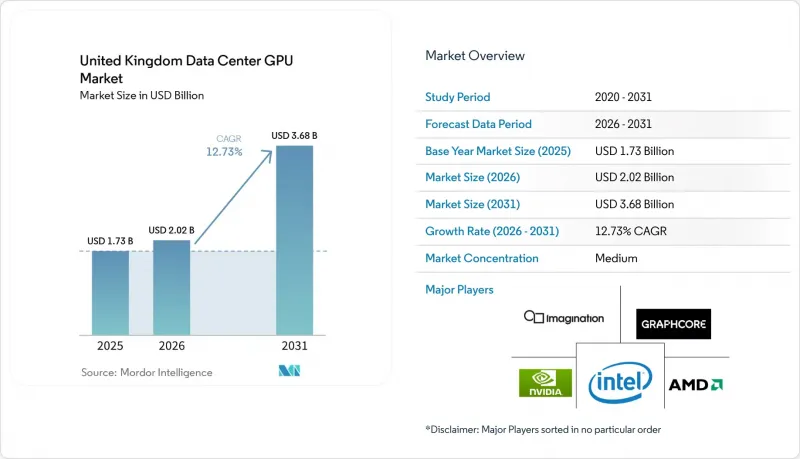

Mordor Intelligence에 의하면, 영국의 데이터센터 GPU 시장 규모는 2025년에 17억 3,000만 달러로 평가되었고, 2026년 20억 2,000만 달러로 추정되고, 2031년까지 36억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 12.73%를 나타낼 전망입니다.

본 보고서는 도입 형태별(클라우드 데이터센터, 엔터프라이즈 및 프라이빗 데이터센터 등), GPU 유형별(훈련용 GPU 및 추론용 GPU), 상호 연결 방식별(PCIe 기반 GPU 및 고대역폭 상호 연결 GPU), 워크로드 유형별(AI 및 ML, HPC, 데이터 분석 등), 그리고 최종 사용자별(하이퍼스케일러/CSP, 기업 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

영국의 데이터센터 GPU 시장 동향 및 인사이트

영국 기업들의 AI 워크로드 도입 가속화

기업들은 고객을 대상으로 운영 중인 애플리케이션을 퍼블릭 클라우드에서 지연 시간, 규정 준수 및 예측 가능한 비용을 보장하는 전용 스택으로 이전하고 있습니다. 현지 통합 업체가 제공하는 프라이빗 AI 플랫폼은 스토리지, 네트워크 및 관리형 소프트웨어가 번들로 구성된 턴키형 클러스터를 제공하여, 도입 주기를 수개월에서 수주일로 단축하고 있습니다. 규제가 엄격한 업계, 은행, 의료, 중요 인프라 분야에서는 클라우드 본연의 확장성보다 온프레미스 환경에서의 제어 가능성과 감사 가능성이 더 중요시되기 때문에 수요가 특히 높아지고 있습니다. 하드웨어 공급업체들은 기존 전력 한도 내에서 작동하는 소형 고효율 GPU SKU를 제공함으로써 이에 대응하고 있으며, 이를 통해 처음부터 새로 구축하는 것이 아니라 단계적인 업그레이드가 가능하도록 하고 있습니다.

영국 가용성 영역 내 하이퍼스케일러의 확장

AWS, 마이크로소프트, 구글은 AI 성장 구역의 계획 개편에 새로운 가용성 구역을 추가하며, 수년에 걸친 건설 프로그램을 전개하고 있습니다. 용도지역 지정 승인에 소요되는 기간이 기존 18개월에서 약 12개월로 단축됨에 따라, 건설 리드타임도 단축되었습니다. 하이퍼스케일러는 우선적인 전력망 접속권을 확보하는 한편, 지방 자치단체는 25년에 걸쳐 사업세를 전액 징수할 수 있기 때문에 세수와 인프라 확장이 서로를 강화하는 선순환이 형성되고 있습니다. 이러한 하이퍼스케일러의 각 캠퍼스에서는 재생에너지 발전 및 전용 회선을 통한 전력 도입 계약을 위해 부지를 확보하고 있으며, 이를 통해 추가되는 발전 용량이 국가의 탄소 예산을 초과하지 않도록 보장하고 있습니다. 또한, 하이퍼스케일러들의 토지 확보는 광섬유 백본, 데이터센터 시설 및 관련 공급업체들을 인근 지역으로 유치함으로써, 소규모 코로케이션 사업자들에게 경쟁 장벽을 더욱 높이고 있습니다.

고성능 GPU 공급망상의 제약

CoWoS 패키징의 병목 현상과 HBM3e 공급 부족으로 인해 납기 기간이 50주 이상으로 늘어났으며, 중견 기업들은 하이퍼스케일러에 이어 2순위 할당 대상으로 밀려나고 있습니다. 현물 가격의 급등으로 인해 CFO들은 시간당 75-95파운드(101.93-129.11달러)의 GPU 임대 비용과, 예산 주기 전체에 걸쳐 납품되지 않을 가능성이 있는 자본 구매 중 어느 쪽을 선택할지 신중하게 검토할 수밖에 없게 되었습니다. 이러한 부족으로 인해 ASIC에 대한 관심이 급속히 높아지고 있으며, 소프트웨어 팀은 기존 하드웨어를 최대한 활용하기 위해 모델 압축에 주력하고 있습니다.

부문별 분석

엣지 시설은 2025년 영국 데이터센터 GPU 시장 규모에서 차지한 점유율은 작았으나, 제조업체들이 10밀리초 미만의 추론 처리를 요구하는 가운데 2031년까지 연평균 성장률(CAGR) 13.77%로 급성장하고 있습니다. 스톡턴온티즈에는 40곳의 뉴럴 엣지 사이트 중 첫 번째 사이트가 설치될 예정입니다. 각 사이트는 소형 165W RTX PRO GPU에 최적화되어 있어, 공장은 프레임을 런던으로 보내 처리할 필요 없이 시각 검사 라인을 가동할 수 있게 됩니다.

지연 시간의 경제성이 네트워크 토폴로지를 형성하고 있습니다. 각 하이퍼스케일러 기업들은 이에 대응하여 캐리어 호텔 내에 마이크로 리전을 구축하는 한편, 에지 노드를 자사의 주요 캠퍼스에 연결하기 위한 프라이빗 트랜짓 링을 구축하고 있습니다. 많은 중견 기업에서는 하이브리드 방식이 주류를 이루고 있습니다. 대량의 훈련 작업은 비용이 저렴한 스코틀랜드 지역에서 수행되며, 고객을 위한 추론은 메트로 지역에 인접한 에지 노드에서 수행됩니다. 이러한 연동을 통해 사업자는 전력 가격 차익 거래와 규정 준수에 기반한 데이터 지역성의 균형을 맞출 수 있으며, 대규모 배치 작업에서는 클라우드의 우위를 유지하면서 엣지 확장을 촉진하고 있습니다.

2025년에는 추론용 실리콘이 영국 데이터센터 GPU 시장 점유율의 55.66%를 차지했으며, 훈련용 GPU를 앞질렀습니다. 실시간 고객 대응이 핵심 워크로드로 자리 잡으면서, 훈련용 GPU의 연평균 성장률(CAGR)은 2031년까지 14.11%를 기록했습니다.

훈련은 여전히 기반 모델 제공업체에게 있어 핵심적인 과제이지만, 현재 대부분의 기업이 처음부터 훈련을 진행하는 대신 미세 조정을 수행하고 있기 때문에 최상위급 HBM 메모리에 대한 전반적인 수요는 줄어들고 있습니다. 각 벤더사는 이러한 추세에 발맞추어 제품 라인업을 세분화하고 있습니다. 듀얼 슬롯 250W 추론 보드가 보급되는 한편, 하이퍼스케일 사이트에서는 초고밀도 NVLink 트레이가 클러스터로 구성되고 있습니다. 이러한 양극화로 인해 운영사는 도입 규모를 최적화하고 칩 조달처를 다각화할 수 있게 되어, 향후 공급 차질에 대한 위험을 헤지할 수 있게 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSHAccording to Mordor Intelligence, the united kingdom data center GPU market size was valued at USD 1.73 billion in 2025 and is estimated to grow from USD 2.02 billion in 2026 to reach USD 3.68 billion by 2031, at a CAGR of 12.73% during the forecast period (2026-2031).

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise / Private Data Centers, and More), GPU Type (Training GPUs and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and More), and End-User (Hyperscalers/CSPs, Enterprises, and More). The Market Forecasts are Provided in Value (USD).

United Kingdom Data Center GPU Market Trends and Insights

Accelerated Adoption of AI Workloads by United Kingdom Enterprises

Enterprises are migrating live customer-facing applications from the public cloud to dedicated stacks that guarantee latency, compliance, and predictable costs. Private AI platforms offered by local integrators deliver turnkey clusters bundled with storage, networking, and managed software, compressing deployment cycles from months to weeks. Demand is especially strong in regulated verticals, banking, healthcare, and critical infrastructure, where on-premises control and auditability outweigh raw cloud elasticity. Hardware vendors respond with smaller, energy-efficient GPU SKUs that fit within existing power envelopes, enabling phased upgrades rather than greenfield builds.

Hyperscaler Expansion of United Kingdom Availability Zones

AWS, Microsoft, and Google are rolling out multi-year build programs that layer new availability zones on top of AI Growth Zone planning reforms. Construction lead times are shrinking because zoning approvals now take roughly 12 months, down from 18 previously. Hyperscalers gain priority grid connections, while local authorities retain all business rates for a quarter-century, creating a self-reinforcing loop of tax revenue and infrastructure expansion. Each of these hyperscale campuses reserves parcel space for renewable generation or private-wire import agreements, ensuring that incremental megawatts do not breach national carbon budgets. The hyperscaler land grabs, in turn, pull optical fiber backbones, data center housing, and tertiary suppliers into adjacent districts, raising the competitive bar for smaller colocations.

Supply Chain Constraints for Advanced GPUs

CoWoS packaging bottlenecks and tight HBM3e supply push delivery windows beyond 50 weeks, relegating mid-tier enterprises to secondary allocation after hyperscalers. Spot pricing spikes force CFOs to weigh GPU rental at GBP 75-95 (USD 101.93 - 129.11) per hour against capital purchases that may not arrive for an entire budget cycle. The shortage is accelerating interest in ASICs and pushing software teams toward model compression to stretch existing hardware.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Digital Infrastructure and AI Research

- Growing Demand for Sovereign Cloud GPU Instances

- Rising Energy Costs and Carbon Targets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge facilities captured a smaller share of the United Kingdom data center GPU market size in 2025, but are accelerating at a 13.77% CAGR through 2031 as manufacturers demand sub-10 millisecond inference. Stockton-on-Tees will host the first of 40 neural-edge sites, each optimized for compact 165 W RTX PRO GPUs, allowing factories to run visual inspection lines without shipping frames to London for processing.

Latency economics shape network topology. Hyperscalers respond by seeding micro-regions within carrier hotels and creating private transit rings to connect edge nodes back to their flagship campuses. For many mid-market enterprises, a hybrid approach dominates: bulk training jobs run in low-cost Scottish zones, while customer-facing inference runs on a metro-adjacent edge node. This choreography lets operators balance power-price arbitrage against compliance-driven data locality, sustaining cloud dominance for large-scale batch jobs while still rewarding edge expansion.

Inference silicon accounted for 55.66% of the United Kingdom data center GPU market share in 2025, outpacing training GPUs, which posted a 14.11% CAGR through 2031 as real-time customer interactions become the core workload.

Training remains mission-critical for foundation-model providers, but most enterprises now fine-tune rather than train from scratch, shrinking overall demand for top-bin HBM memory footprints. Vendors segment their catalog accordingly: dual-slot, 250 W inference boards proliferate, while ultra-dense NVLink trays cluster at hyperscale sites. This bifurcation allows operators to right-size deployments and diversify chip sourcing, a hedge against future supply disruptions.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Graphcore Ltd.

- Imagination Technologies Ltd.

- Arm Ltd.

- Amazon Web Services, Inc.

- Microsoft Corporation

- Dell Technologies Inc.

- Lenovo Group Limited

- Super Micro Computer, Inc.

- Fujitsu Limited

- Penguin Solutions, Inc.

- OCF Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of AI Workloads by UK Enterprises

- 4.2.2 Hyperscaler Expansion of UK Availability Zones

- 4.2.3 Government Incentives for Digital Infrastructure and AI Research

- 4.2.4 Growing Demand for Sovereign Cloud GPU Instances

- 4.2.5 Convergence of Edge Computing in Smart Manufacturing Corridors

- 4.2.6 Rise of Liquid-Cooled GPU Servers to Meet Sustainability Mandates

- 4.3 Market Restraints

- 4.3.1 Supply Chain Constraints for Advanced GPUs

- 4.3.2 Rising Energy Costs and Carbon Targets

- 4.3.3 Limited High-Bandwidth Interconnect Expertise Among UK Integrators

- 4.3.4 Competition from ASIC Accelerators for Inference Workloads

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Graphcore Ltd.

- 6.4.5 Imagination Technologies Ltd.

- 6.4.6 Arm Ltd.

- 6.4.7 Amazon Web Services, Inc.

- 6.4.8 Microsoft Corporation

- 6.4.9 Dell Technologies Inc.

- 6.4.10 Lenovo Group Limited

- 6.4.11 Super Micro Computer, Inc.

- 6.4.12 Fujitsu Limited

- 6.4.13 Penguin Solutions, Inc.

- 6.4.14 OCF Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment