|

시장보고서

상품코드

2065508

중국의 데이터센터 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

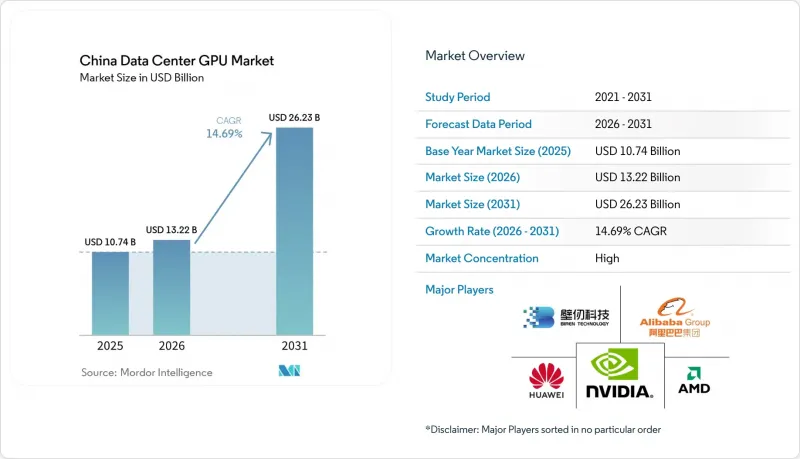

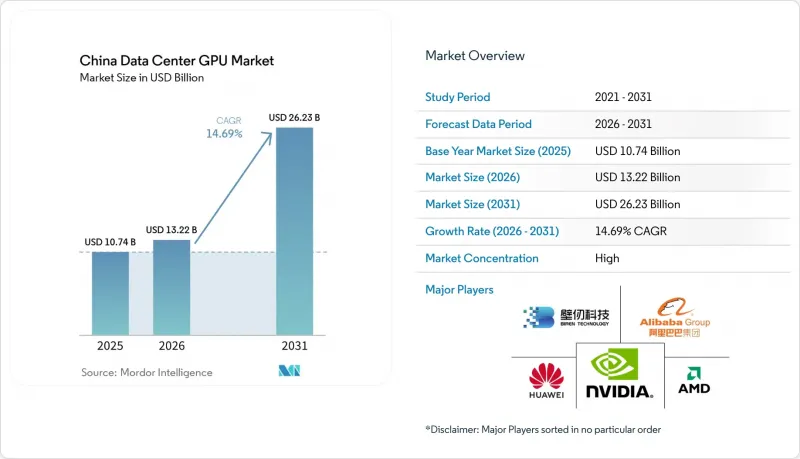

Mordor Intelligence에 의하면, 중국의 데이터센터 GPU 시장 규모는 2025년에 107억 4,000만 달러로 평가되었고, 2026년에 132억 2,000만 달러로 추정되고, 2031년까지 262억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 14.69%로 성장할 전망입니다.

본 보고서는 도입 형태별(클라우드 데이터센터, 엔터프라이즈 및 프라이빗 데이터센터, 엣지 데이터센터), GPU 유형별(훈련용 GPU, 추론용 GPU), 상호 연결 방식별(PCIe 기반 GPU, 고대역폭 상호 연결 GPU), 워크로드 유형별(AI 및 ML, HPC 등), 최종 사용자별(하이퍼스케일러 및 CSP, 기업, 정부 및 연구 기관)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 데이터센터 GPU 시장 동향 및 인사이트

AI 클러스터를 위한 하이퍼스케일러의 설비 투자 증가

바이트댄스는 2026년 설비 투자로 1,600억 위안(230억 달러)을 확보했으며, 그 절반을 GPU 구매에 할당했습니다. 한편, 알리바바는 3년 동안 인프라 투자를 4,800억 위안까지 늘리는 방안을 검토하고 있습니다. 텐센트는 2026년 연간 AI 예산을 약 50억 달러로 두 배로 늘렸으나, 이전 공급 부족으로 인해 2025년 지출은 792억 위안 수준에 그쳤습니다. 항저우시가 마련한 37억 달러 규모의 자금 조달 패키지는 기업의 지출을 시너지 효과를 통해 증대시키는 지자체 주도 공동 투자의 한 예입니다. 미국의 수출 허가에 따라 25%의 관세와 50%의 수량 제한을 조건으로 H200의 제한적인 수입이 허용됨에 따라, 각 하이퍼스케일러 기업들은 화웨이의 Ascend를 대체할 대안을 모색하기 시작했습니다. 활동은 양쯔강 삼각주와 광둥·홍콩·마카오 대만구를 중심으로 전개되고 있으며, 이 지역에서는 10밀리초 미만의 지연 시간과 랙당 300와트의 전력 여유 덕분에 멀티카드 클러스터 운영이 가능합니다.

수출 규제로 인한 현지 생산 GPU로의 대체

2025년 중반 이후, NVIDIA 및 AMD의 첨단 가속기에 대한 수출 규제가 강화됨에 따라 화웨이의 출하가 촉진되어, 2025년 말까지 ‘Ascend 910B’가 5만 대를 돌파하였고, 2026년에는 ‘Ascend 950PR’ 칩 75만 대 출하가 계획되어 있습니다. 910C 및 950PR은 H100의 처리량의 60-80%를 달성하며, SMIC의 N+3 공정을 채택함으로써 TSMC의 패키징 능력에 대한 의존도를 낮추고 있습니다. Cambricon의 2024년 매출액은 67.4% 증가한 12억 8,000만 위안으로 급증했으며, 투자은행들은 2027년까지 국내 자급률이 50%를 나타낼 것으로 전망하고 있습니다. 국산 기술을 우선시하는 정책에 따라 공공 부문과 군사 분야에서의 도입이 가속화되고 있습니다. 민간 하이퍼스케일러조차도 라이선스 리스크를 헤지하기 위해 국산 그래픽 카드를 채택하고 있습니다.

첨단 패키징(CoWoS/HBM) 생산 능력의 병목 현상

TSMC는 2026년 초까지 CoWoS 생산량을 4배로 늘려 월간 약 12만 장의 웨이퍼에 도달했으나, 그 할당량의 60% 가까이를 NVIDIA가 확보하고 있습니다. HBM3e는 SK하이닉스와 삼성의 생산 확대 이후에도 전 세계적으로 30% 공급 부족이 지속되고 있어, 여전히 공급이 부족한 상황입니다. 국내 공급업체들은 대기 현상을 피하기 위해 LPDDR 메모리를 탑재한 7나노미터 공정을 채택하고 있지만, 하이엔드 훈련용 칩에는 여전히 CoWoS가 필요하며, 납기일이 50주 이상 지연되고 있습니다. 이러한 병목 현상으로 인해 중국 바이어들은 교육 일정을 연장하거나 희소성 있는 수입품에 대해 추가 비용을 지불할 수밖에 없게 되어, 중국 데이터센터 GPU 시장의 단기적인 성장 여지가 제한되고 있습니다.

부문별 분석

2025년, 중국 데이터센터 GPU 시장에서 엣지 시설이 가장 빠르게 성장한 부문으로, 2031년까지 연평균 성장률(CAGR) 20.3%를 나타낼 것으로 전망됩니다. 클라우드 데이터센터는 10만 개의 GPU 클러스터를 운영하며 규모의 경제를 실현하는 하이퍼스케일러의 존재 덕분에, 2025년 기준 중국 데이터센터 GPU 시장 점유율의 62.84%를 차지하며 여전히 지배적인 위치를 유지하고 있습니다.

차이나모바일과 차이나유니콤은 클라우드 게임 및 실시간 동영상 스트리밍에 GPU를 활용하는 5G MEC 시범 프로젝트를 실시하여, 연산 처리가 도심에 배치된 경우 왕복 지연 시간 15밀리초 미만을 실현할 수 있음을 입증했습니다. 리스 가격 하락으로 인해 소규모 프라이빗 데이터센터의 사업 타당성이 약화되면서, 많은 중견 기업들은 워크로드를 퍼블릭 클라우드로 분산시키는 한편, 기밀 데이터는 온프레미스 엣지 노드에 보관하고 있습니다. ZTE에서 출하되는 수냉식 마이크로 모듈은 소매점이나 공장 환경에서 발생하는 공간 및 전력 제약을 해결하는 데 도움이 되고 있습니다.

추론 가속기는 2025년 중국 데이터센터 GPU 시장 규모의 59.21%를 차지한 것으로 평가되었으며, 연평균 성장률(CAGR) 16.8%로 성장할 것으로 전망되어 가장 규모가 크고 성장 속도가 가장 빠른 부문으로 자리매김하고 있습니다. 훈련용 GPU는 새로운 기반 모델에 필수적이지만, 주요 클러스터가 이미 존재하고 단기 수익을 주도하는 것은 추론이기 때문에 그 확대 속도는 완만합니다.

Alibaba Cloud의 TensorRT-LLM 및 vLLM 서비스는 LPDDR 메모리를 탑재한 중급 GPU에서 하루에 수십억 건의 쿼리를 처리할 수 있으며, HBM 기반 대체 제품에 비해 칩 비용을 30-40% 절감합니다. ByteDance에 매각된 화웨이의 950PR은 FP16의 최고 성능이 아닌, 1.56 PFLOPS의 FP4 기반 추론 처리량에 중점을 두고 있습니다. 국내 설계자들은 CoWoS의 대기열을 피하기 위해 6나노미터 또는 7나노미터 노드를 선택하고 있으며, 이는 가격에 민감한 추론 도입 요구와 부합합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the china data center GPU market size is projected to be USD 10.74 billion in 2025, USD 13.22 billion in 2026, and reach USD 26.23 billion by 2031, growing at a CAGR of 14.69% from 2026 to 2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), and End-User (Hyperscalers/CSPs, Enterprises, Government and Research Institutions). Market Forecasts are Provided in Terms of Value (USD).

China Data Center GPU Market Trends and Insights

Rising Hyperscaler Capex for AI Clusters

ByteDance set aside CNY 160 billion (USD 23 billion) for 2026 capital expenditure and devoted half of that sum to GPU purchases, while Alibaba discussed raising infrastructure investment to RMB 480 billion over three years.Tencent doubled its annual AI budget to roughly USD 5 billion in 2026, although earlier supply tightness kept its 2025 spending to RMB 79.2 billion. Hangzhou's USD 3.7 billion procurement package illustrates municipal co-investment that compounds corporate outlays. United States export licenses allowed limited H200 imports with a 25% tariff and 50% volume cap, nudging hyperscalers toward Huawei Ascend alternatives. Activity centers on the Yangtze River Delta and the Greater Bay Area, where sub-10-millisecond latency and 300 watts per rack of power headroom accommodate multi-card clusters.

Export-Control-Driven Substitution Toward Local GPUs

The block on advanced NVIDIA and AMD accelerators since mid-2025 stimulated Huawei shipments that topped 50,000 Ascend 910B units by year-end 2025 and planned 750,000 Ascend 950PR chips for 2026. The 910C and 950PR deliver 60-80% of H100 throughput and ride SMIC's N+3 process, shrinking reliance on TSMC packaging capacity. Cambricon's 2024 revenue surged 67.4% to RMB 1.28 billion, and investment banks see domestic self-sufficiency reaching 50% by 2027. Mandates favoring indigenous tech speed adoption in public-sector and military workloads. Even private hyperscalers add domestic cards to hedge license risk.

Advanced Packaging (CoWoS/HBM) Capacity Bottlenecks

TSMC quadrupled CoWoS output to about 120,000 wafers per month by early 2026, yet NVIDIA locks down close to 60% of that allocation. HBM3e remains tight with a 30% global shortfall even after SK Hynix and Samsung expansions. Domestic vendors tap 7-nanometer nodes with LPDDR memory to avoid the queue, but high-end training chips still need CoWoS, delaying deliveries by more than 50 weeks. The bottleneck forces Chinese buyers to stretch training schedules or pay premiums for scarce imports, clipping near-term upside for the China data center GPU market.

Other drivers and restraints analyzed in the detailed report include:

- Government Vouchers Incentivizing Domestic AI Compute

- Liquid-Cooling Adoption Enabling 80 kW+ Racks

- Rapid Price Declines in GPU Cloud Leasing

- Persistent Software Ecosystem Gap vs CUDA

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge facilities represented the fastest-growing slice of the China data center GPU market during 2025 and are forecast to post a 20.3% CAGR through 2031. Cloud data centers still dominate with 62.84% of China's data center GPU market share in 2025, thanks to hyperscalers that run 100,000-GPU clusters to achieve economies of scale.

China Mobile and China Unicom staged 5G MEC pilots that use GPUs for cloud gaming and real-time video, proving that sub-15-millisecond round-trip is achievable when compute sits within the city core. Lower leasing prices weaken the business case for small private halls, so many mid-sized firms burst workloads into public cloud but keep sensitive data on on-premise edge nodes. Liquid-cooled micro-modules shipping from ZTE help solve space and power limitations in retail and factory environments.

Inference accelerators held 59.21% of the China data center GPU market size in 2025 and are projected to grow at a 16.8% CAGR, making them both the largest and fastest segment. Training GPUs, while indispensable for new foundation models, expand more slowly as major clusters already exist and inference drives near-term revenue.

Alibaba Cloud's TensorRT-LLM and vLLM services can answer billions of daily calls on mid-tier GPUs paired with LPDDR memory, cutting chip costs by 30-40% against HBM-based alternatives. Huawei's 950PR sold to ByteDance focuses on inference throughput with 1.56 PFLOPS FP4 rather than peak FP16 performance. Domestic designers choose 6- or 7-nanometer nodes to dodge CoWoS queues, aligning with price-sensitive inference deployments.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Huawei Technologies Co., Ltd.

- Alibaba Group Holding Limited (Alibaba Cloud)

- Baidu, Inc.

- Tencent Holdings Ltd.

- Inspur Electronic Information Industry Co., Ltd.

- Lenovo Group Limited

- Intel Corporation

- Biren Technology Co., Ltd.

- Moore Threads Technology Co., Ltd.

- Cambricon Technologies Corp. Ltd.

- Hygon Information Technology Co., Ltd.

- Dawning Information Industry Co., Ltd. (Sugon)

- Enflame Technology Co., Ltd.

- MetaX Technology Inc.

- Iluvatar CoreX (Shanghai) Inc.

- JINGJIA Microelectronics Co., Ltd.

- China Telecom Corporation Limited

- ByteDance Ltd. (Volcengine)

- Shanghai Zhaoxin Semiconductor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Hyperscaler Capex for AI Clusters

- 4.2.2 Government Vouchers Incentivizing Domestic AI Compute

- 4.2.3 Export-Control-Driven Substitution Toward Local GPUs

- 4.2.4 Rapid Price Declines in GPU Cloud Leasing

- 4.2.5 Liquid-Cooling Adoption Enabling 80 kW+ Racks

- 4.2.6 East-Data West-Compute Policy Unlocking Low-Cost Power

- 4.3 Market Restraints

- 4.3.1 Advanced Packaging (CoWoS/HBM) Capacity Bottlenecks

- 4.3.2 Persistent Software Ecosystem Gap vs CUDA

- 4.3.3 Low Utilization Rates in Newly Built AI Centers

- 4.3.4 Grid-Connection Delays in Remote Western Hubs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Alibaba Group Holding Limited (Alibaba Cloud)

- 6.4.5 Baidu, Inc.

- 6.4.6 Tencent Holdings Ltd.

- 6.4.7 Inspur Electronic Information Industry Co., Ltd.

- 6.4.8 Lenovo Group Limited

- 6.4.9 Intel Corporation

- 6.4.10 Biren Technology Co., Ltd.

- 6.4.11 Moore Threads Technology Co., Ltd.

- 6.4.12 Cambricon Technologies Corp. Ltd.

- 6.4.13 Hygon Information Technology Co., Ltd.

- 6.4.14 Dawning Information Industry Co., Ltd. (Sugon)

- 6.4.15 Enflame Technology Co., Ltd.

- 6.4.16 MetaX Technology Inc.

- 6.4.17 Iluvatar CoreX (Shanghai) Inc.

- 6.4.18 JINGJIA Microelectronics Co., Ltd.

- 6.4.19 China Telecom Corporation Limited

- 6.4.20 ByteDance Ltd. (Volcengine)

- 6.4.21 Shanghai Zhaoxin Semiconductor Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment