|

시장보고서

상품코드

2066771

북미의 전기자동차 배터리 제조 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2006-2031년)North America Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

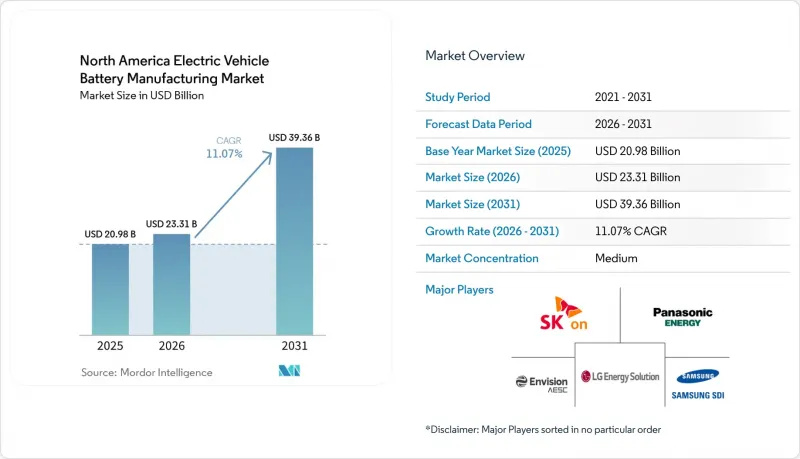

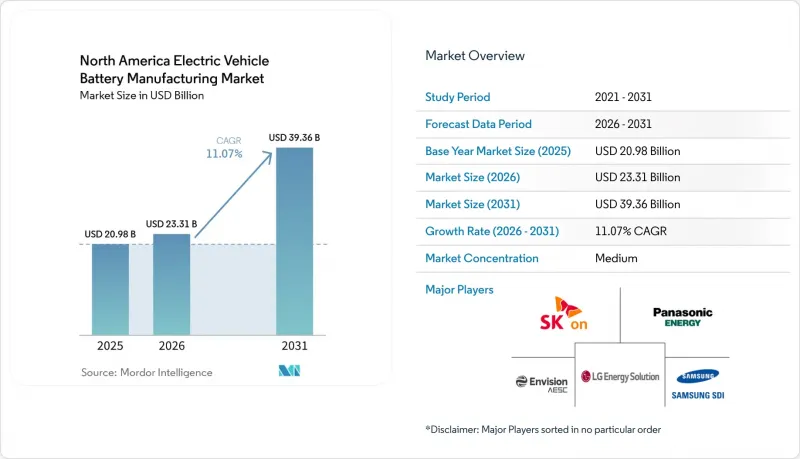

Mordor Intelligence에 의하면, 북미의 전기자동차 배터리 제조 시장 규모는 2025년 209억 8,000만 달러로 평가되었고, 2026년에는 233억 1,000만 달러로 추정되고, 2026-2031년 CAGR 11.07%로 성장을 지속할 전망이며, 2031년까지 393억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 배터리의 화학적 조성별(리튬 이온, 신기술, 납산, 니켈 금속 수소 전지), 셀 형태별(원통형, 각형, 파우치형), 동력원별(배터리 전기차 등), 차종별(승용차, 소형 상용차, 중형·대형 트럭, 버스·장거리 버스 등), 지역별(미국, 캐나다, 멕시코)로 분류되어 있습니다.

북미의 전기자동차용 배터리 제조 시장 동향 및 인사이트

IRA(인플레이션 억제법)에 힘입어 기가팩토리 건설 확대

연방 정부의 생산세액 공제 정책으로 인해 북미의 전기자동차 배터리 제조 시장에 진출한 기업들은 수입 중심 공급 체제에서 국내 생산 라인으로의 전환을 강요받고 있으며, 2024년에는 미국에서 13개의 신규 공장이 에너지부로부터 대출 제안을 받았습니다. 각 개발사는 2032년 이후 보조금이 단계적으로 삭감되기 전에 유리한 단위 경제성을 확보하기 위해 시설 가동을 서두르고 있습니다. 아시아산 수입에 계속 의존하는 자동차 제조업체는 소비자 대상 세제 혜택에서 제외될 위험이 있으며, 그 결과 북미산 배터리를 탑재한 모델에 비해 차량 가격이 7,500달러 더 비싸지게 됩니다. 그 결과 발생한 현지화 경쟁으로 인해 중서부 및 남동부의 산업단지는 기가팩토리의 집적지로 변모했으며, 이는 지역 건설업체와 금형 공급업체에 눈에 띄는 단기적인 수요 증가를 가져왔습니다.

OEM을 통한 수직 통합 경쟁

Ultium Cells와 BlueOval SK를 비롯한 자사 계열 합작 사업은 기존 OEM 각사가 조달 전략을 어떻게 재편하고 있는지를 여실히 보여주고 있습니다. 제너럴 모터스(GM)와 LG 에너지 솔루션은 이미 총 140GWh의 생산 능력을 갖춘 3개의 합작 공장을 운영하고 있으며, 배터리 셀 비용을 시장 가격이 아닌 장부 가격으로 계상함으로써 변동이 심한 리튬 및 니켈의 벤치마크 가격에 대한 노출을 완화하고 있습니다. 테슬라의 건식 전극 관련 특허는 조립 공정과 핵심 지적 재산권(IP)을 모두 자사 내부에 확보하겠다는 야심을 보여주고 있습니다. 수직 통합은 현물 시장의 원자재 가격이 급격히 변동할 때 매출총이익률을 지키기 위한 안전장치로 간주됩니다. 또한, 양극재 공급업체와의 협상에서 협상상의 우위를 점할 수 있게 해줍니다.

원자재 가격의 급격한 변동

리튬 탄산염은 2022년 톤당 8만 5,000달러에서 2023년에는 1만 3,000달러로 급락했으나, 2024년에는 6개월도 채 되지 않아 가격이 두 배로 치솟았습니다. 니켈의 경우, 인도네시아의 수출 규제와 러시아에 대한 제재로 인해 공급이 부족해진 결과, 가격이 35% 변동했습니다. 장기 오프테이크 계약 대신 분기별 재협상이 이루어지게 되면서, 과거 20% 전후로 유지되던 셀 제조업체의 매출총이익률 여력이 줄어들고 있습니다. IRA(인플레이션 억제법)의 국내 조달 요건으로 인해 조달의 유연성이 제한되어, 전 세계 현물 가격 기준이 더 저렴한 경우에도 제조업체는 비용이 높은 지역산 원료에 얽매이게 됩니다.

부문별 분석

리튬 이온 배터리는 95% 이상의 높은 수율과 250-300 Wh/kg의 에너지 밀도를 바탕으로, 2025년 북미 전기차용 배터리 제조 시장 점유율의 90.85%를 유지했습니다. 고체 전지, 리튬-황 전지, 나트륨 이온 전지 등 각 제품 라인은 OEM 업체들의 시범 생산이 소량 양산 단계로 전환됨에 따라 2031년까지 연평균 성장률(CAGR) 34.08%를 나타낼 것으로 전망됩니다. NMC는 300마일을 넘는 프리미엄 주행거리 차량에서 여전히 선호되는 화학 조성물이지만, 코발트 가격 변동이 심화됨에 따라 코발트 함유량이 불과 10%에 불과한 고니켈 NMC 811 블렌드로의 전환이 가속화되고 있습니다. LFP 배터리는 에너지 밀도가 낮지만, 코발트를 포함하지 않는 설계 덕분에 부품 원가 리스크를 줄일 수 있어 북미 시장에서 회복세를 보이고 있습니다.

북미의 신흥 화학 성분 전기자동차 배터리 제조 시장 규모 확대는 두 가지 전제에 기반을 두고 있습니다. 즉, 2028년까지 전고체 배터리의 수율이 기존 생산 라인과의 격차를 좁히고, 자동화를 통해 GWh당 설비 투자액이 절반으로 줄어드는 것입니다. 나트륨 이온 배터리는 에너지 밀도가 낮기 때문에 고정형 에너지 저장이나 도시 지역의 통근용 모델로만 제한되지만, 원료가 풍부하다는 점에서 리튬 부족에 대한 대비책이 됩니다. 리튬-황 전지에 대한 조사 결과, 사이클 수명은 150회를 넘어서는 추세이지만, 실용화에 대해서는 여전히 불투명합니다. 전반적으로, 새로운 화학 조성은 공급 리스크를 분산시켜, 2030년까지 리튬 이온 배터리를 완전히 대체하지는 않더라도 지역별 기술 곡선을 확대하는 결과를 가져올 것입니다.

2025년 수요 중 원통형 셀이 51.90%를 차지했습니다. 이는 테슬라가 초기 단계에서 노트북을 참고한 설계를 채택한 점과 고속 권선 라인이 성숙 단계에 접어들었음을 반영한 것입니다. 프리즘형 배터리는 자동차 제조업체들이 20% 향상된 부피 효율과 간소화된 팩 조립 방식을 선호함에 따라, 2031년까지 연평균 성장률(CAGR) 25.32%로 성장할 전망입니다. 파우치형은 10%대 중반의 틈새 시장을 유지하고 있지만, 팽창 사고로 인한 리콜은 대규모 생산에서 품질 관리의 과제를 여실히 드러내고 있습니다.

프리즘형 배터리의 성장은 북미 전기차용 배터리 제조 시장 규모를 확대되고 있습니다. 이 지역에서는 새로운 생산 라인에서 셀을 팩에 직접 조립하는 방식을 채택하고 있으며, 모듈 하우징을 생략함으로써 kW시당 5-8달러의 비용 절감을 실현하고 있습니다. 테슬라의 4,680 원통형 배터리 전략은 여전히 탭이 없는 전극을 통해 50%의 비용 절감을 목표로 하고 있지만, 오스틴 공장의 수율이 80% 미만에 그치고 있어 이 공정의 양산화가 쉽지 않다는 점이 드러나고 있습니다. BYD와 CATL은 팩 수준에서 160 Wh/kg을 달성하고, 못 관통 시험을 통해 충돌 안전성을 입증한 블레이드형 프리즘 팩으로 업계의 벤치마크를 확립했습니다. 각 자동차 제조업체들은 체적 효율 향상과 익숙하지 않은 생산 설비로 전환함에 따른 위험 사이의 균형을 맞추려고 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the north america electric vehicle battery manufacturing market size is expected to grow from USD 20.98 billion in 2025 to USD 23.31 billion in 2026 and is forecast to reach USD 39.36 billion by 2031 at 11.07% CAGR over 2026-2031.

This report is Segmented by Battery Chemistry (Lithium-Ion, Emerging, Lead-Acid, and Nickel-Metal-Hydride), Cell Format (Cylindrical, Prismatic, and Pouch), Propulsion (Battery Electric Vehicle, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium and Heavy Trucks, Buses and Coaches, and More), and Geography (United States, Canada, and Mexico).

North America Electric Vehicle Battery Manufacturing Market Trends and Insights

IRA-Fuelled Giga-Factory Build-Out

Federal production credits have pushed North America's electric vehicle battery manufacturing market participants to shift from import-led supply toward domestic lines, with 13 new U.S. plants securing Department of Energy loan offers in 2024. Developers are racing to commission facilities before subsidies taper after 2032, locking in advantageous unit economics. Automakers that continue to rely on Asian imports risk forfeiting consumer tax incentives, effectively pricing their vehicles USD 7,500 above models with North American batteries. The resulting localization sprint has converted Midwest and Southeast industrial parks into giga-factory corridors and supplied a visible near-term lift to regional construction and tooling suppliers.

OEM Vertical-Integration Race

Ultium Cells, BlueOval SK, and other captive ventures illustrate how legacy OEMs are rewriting procurement doctrine. General Motors and LG Energy Solution already run three joint plants totaling 140 GWh of capacity, embedding cell cost at book value instead of market value and moderating exposure to volatile lithium and nickel benchmarks. Tesla's dry-electrode patents show an ambition to internalize both assembly and core IP. Vertical integration is viewed as insurance that protects gross margins when spot raw-material contracts swing widely; it also provides bargaining leverage in negotiations with cathode suppliers.

Raw-Material Price Whiplash

Lithium carbonate plunged from USD 85,000 per tonne in 2022 to USD 13,000 per tonne in 2023, then doubled inside six months in 2024. Nickel saw a 35% swing after Indonesian export curbs and Russian sanctions tightened supply. Quarterly renegotiations have replaced long-term offtake contracts, shrinking the gross-margin buffer for cell producers that once hovered near 20%. IRA domestic-content rules restrict sourcing flexibility and lock manufacturers into higher-cost regional feedstock even when global spot benchmarks are cheaper.

Other drivers and restraints analyzed in the detailed report include:

- Regionalisation of Cathode & Anode Supply

- Solid-State Pilot-Line Breakthroughs

- Grid-Capacity & Permitting Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion retained 90.85% of the 2025 North America electric vehicle battery manufacturing market share thanks to mature yields exceeding 95% and energy densities between 250 and 300 Wh/kg. Solid-state, lithium-sulfur, and sodium-ion lines will grow at a 34.08% CAGR through 2031 as OEM pilots graduate to low-volume series production. NMC remains the preferred chemistry for premium ranges above 300 miles, but cobalt cost volatility is accelerating the pivot toward high-nickel NMC 811 blends with just 10% cobalt content. LFP packs are rebounding in North America because their cobalt-free design reduces bill-of-materials risk despite lower energy density.

The North America electric vehicle battery manufacturing market size expansion for emerging chemistries rests on two assumptions: solid-state yields close the gap with conventional lines by 2028, and capex per GWh falls by half through automation. Sodium-ion's lower density constrains it to stationary storage and urban commuter models, yet its abundant raw material offers a hedge against lithium scarcity. Lithium-sulfur research pushes cycle life beyond 150, though deployment remains speculative. Collectively, new chemistries diversify supply risk and extend the regional technology curve without displacing lithium-ion before 2030.

Cylindrical cells held 51.90% of 2025 demand, reflecting Tesla's early laptop-derived designs and mature high-speed winding lines. Prismatic alternatives will move ahead with a 25.32% CAGR through 2031 as automakers favor 20% better volumetric efficiency and simplified pack assembly. Pouch formats keep a mid-teens niche, but recalls tied to swelling episodes highlight quality-control hurdles at scale.

Prismatic growth boosts the North America electric vehicle battery manufacturing market size, where new lines integrate cells directly into the pack, cutting module housings and saving USD 5-8 per kilowatt-hour. Tesla's 4680 cylindrical strategy still aims for a 50% cost cut through tab-less electrodes, though yields under 80% in Austin show the difficulty of scaling the process. BYD and CATL have set a benchmark with blade-style prismatic packs that reach 160 Wh/kg at the pack level and demonstrate crash safety during nail-penetration tests. Automakers are balancing volumetric gains with the risk of shifting to less familiar production tooling.

List of Companies Covered in this Report:

- LG Energy Solution

- Panasonic Energy (w/ Tesla)

- SK On

- Samsung SDI

- AESC Envision

- Ultium Cells (GM + LG)

- CATL USA

- FREYR Battery

- BYD Motors NA

- Contemporary Amperex Technology Ltd.

- American Battery Solutions

- EnerSys

- GS Yuasa Corp

- Exide Industries NA

- Sionic Energy

- Clarios LLC

- Redwood Materials

- Li-Cycle Holdings

- QuantumScape

- Solid Power

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IRA-fuelled giga-factory build-out

- 4.2.2 OEM vertical-integration race

- 4.2.3 Regionalisation of cathode & anode supply

- 4.2.4 Solid-state pilot-line breakthroughs

- 4.2.5 Second-life & recycling credit markets

- 4.2.6 North-American critical-minerals pacts

- 4.3 Market Restraints

- 4.3.1 Raw-material price whiplash

- 4.3.2 Grid-capacity & permitting bottlenecks

- 4.3.3 Skilled-labour shortfall for giga-scale

- 4.3.4 Persisting EV-demand cyclicality

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (NMC, LFP, NCA)

- 5.1.2 Emerging (Solid-state, Li-S, Na-ion)

- 5.1.3 Lead-acid

- 5.1.4 Nickel-metal-hydride

- 5.2 By Cell Format

- 5.2.1 Cylindrical

- 5.2.2 Prismatic

- 5.2.3 Pouch

- 5.3 By Propulsion

- 5.3.1 Battery Electric Vehicle (BEV)

- 5.3.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.3.3 Hybrid Electric Vehicle (HEV)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Trucks

- 5.4.4 Buses and Coaches

- 5.4.5 Two and Three-wheelers

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 LG Energy Solution

- 6.4.2 Panasonic Energy (w/ Tesla)

- 6.4.3 SK On

- 6.4.4 Samsung SDI

- 6.4.5 AESC Envision

- 6.4.6 Ultium Cells (GM + LG)

- 6.4.7 CATL USA

- 6.4.8 FREYR Battery

- 6.4.9 BYD Motors NA

- 6.4.10 Contemporary Amperex Technology Ltd.

- 6.4.11 American Battery Solutions

- 6.4.12 EnerSys

- 6.4.13 GS Yuasa Corp

- 6.4.14 Exide Industries NA

- 6.4.15 Sionic Energy

- 6.4.16 Clarios LLC

- 6.4.17 Redwood Materials

- 6.4.18 Li-Cycle Holdings

- 6.4.19 QuantumScape

- 6.4.20 Solid Power

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment