|

시장보고서

상품코드

2072554

동남아시아의 NOR 플래시 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South East Asia NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

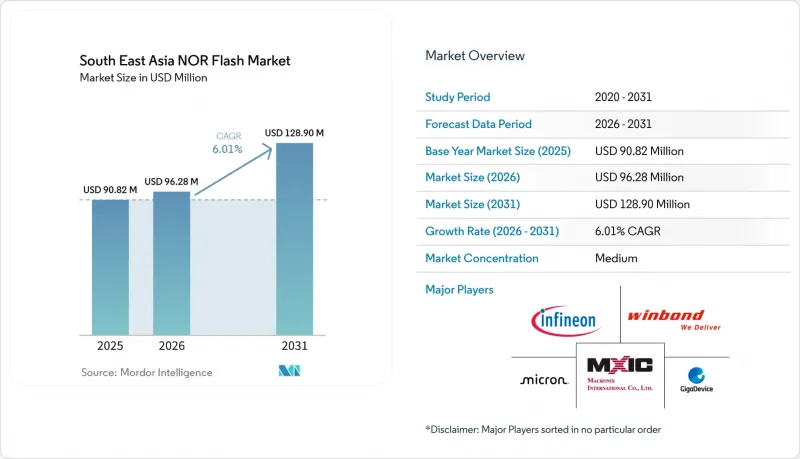

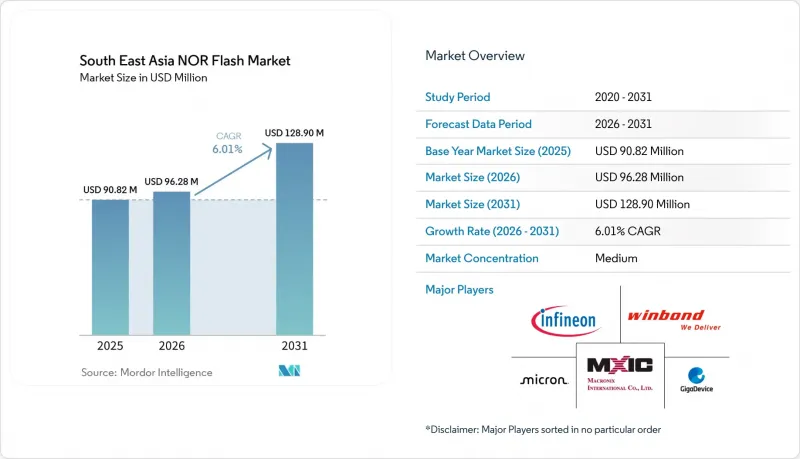

Mordor Intelligence에 의하면, 동남아시아의 NOR 플래시 시장 규모는 2025년 9,082만 달러로 평가되었습니다. 2026년에는 9,628만 달러로 확대되어 2026-2031년에 걸쳐 CAGR 6.01%로 성장을 지속하여, 2031년에는 1억 2,890만 달러에 이를 것으로 예측됩니다.

본 보고서는 NOR 플래시 유형(직렬, 병렬), 인터페이스(SPI 싱글/듀얼, 기타), 용량(2메가비트 이하, 기타), 전압(3V급, 1.8V, 기타), 최종 사용자용도(통신, 기타), 공정 기술 노드(65nm, 45nm, 기타), 패키징 유형(WLCSP/CSP, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러)과 수량(개)으로 제시되어 있습니다.

동남아시아의 NOR 플래시 시장 동향 및 인사이트

정부 주도의 인센티브가 전자제품 제조 확대를 견인하고 있습니다.

정부의 정책은 동남아시아의 NOR 플래시 메모리 시장에 있어 단기적인 수요를 뒷받침하는 가장 확실한 요인 중 하나입니다. 이는 인센티브 프로그램을 통해 해당 지역에 조립, 패키징, 전자기기 제조 프로젝트가 더욱 많이 유치되고 있기 때문입니다. 베트남 고시 제33/2025/TT-BKHCN호에서는 전자기기 제조업체에 대한 세제 우대 조치 적용 요건으로, 베트남에서 설계 또는 제조된 반도체의 사용, 공급망 내 국내 조달 비율이 30% 이상이어야 한다는 등 4가지 기준이 정해져 있으며, 이를 통해 칩 기반 제품의 현지 조달 부품 비율 확대가 촉진되고 있습니다. 2025년 1월에 출범한 조호르-싱가포르 특별경제구역에서는 요건을 충족하는 전자기기 및 반도체 사업에 대해 최장 15년 동안 5%의 법인세율을 적용하고 있어, OEM의 설계·조립 거점 근처에 거점을 마련하고자 하는 공급업체들에게 그 매력이 더욱 커지고 있습니다. 태국의 국가 반도체 로드맵은 25년 동안 23만 명 이상의 고숙련 인재를 양성하는 것을 목표로 하고 있으며, 이를 통해 태국이 반도체 역량을 단기적인 정책 과제가 아닌 장기적인 산업 우선 과제로 삼고 있음을 알 수 있습니다. 말레이시아의 ‘'새로운 인센티브 체계'는 2026년 3월 1일에 발효되어, 전자, 반도체 패키징, 정밀 공학을 중심으로 한 제조 지원 체제를 재구축했습니다. 이로 인해 코드 저장 공간과 부트 메모리를 소모하는 공장의 기반이 확대되고 있습니다. 이러한 프레임워크 덕분에 Tier 1 OEM의 입지 결정 기간이 단축되는 한편, NOR 플래시에 대한 직접적이고 지속적인 수요를 창출하는 전자제품 생산 라인의 도입 기반이 확대되고 있습니다.

해당 지역 내 자동차용 전자기기 클러스터의 형성 및 성장

스마트 콕핏, ADAS, 전기차(EV) 전력 관리, OTA 소프트웨어 등 모든 분야의 발전이 신뢰성이 높은 펌웨어 저장 장치에 대한 수요를 높임에 따라, 자동차용 전자 계기판이 동남아시아의 NOR 플래시 메모리 시장의 성장을 주도하고 있습니다. 멀티코드 일렉트로닉스(MCE)와 혜주 포유 제너럴 일렉트로닉스는 2025년 9월, 아세안 전역에서 콕핏 도메인 컨트롤러 및 커넥티드카 기술의 현지화를 위한 제조·개발 계약을 체결했습니다. 이에 따라 MCE는 페로두아의 생산 기지 인근에 1억 5,000만-2억 링깃(3,400만-4,500만 달러)을 투자할 예정입니다. VinFast는 2025년에 전기차(EV)의 현지화율을 60% 이상 달성하고, 2026년까지 84%를 목표로 하고 있으며, 이는 ECU 및 배터리 관리 시스템용 자동차 등급 메모리의 조달 증가를 의미합니다. 말레이시아에는 말레이시아 자동차·로봇 IoT 연구소(MARI)가 지원하는 국가 정책에 따라 반도체 수출 기반과 자동차 개발 노력이 융합되고 있다는 구조적 우위도 있습니다. 실제로 이는 해당 지역의 많은 자동차 프로젝트가 기본적인 메모리 수요에서 벗어나, 더 높은 신뢰성과 보존 성능이 요구되는 안전 규격 준수 디바이스로 전환되고 있음을 의미합니다. 이러한 변화는 진입 장벽을 높이고, 인증 공급업체 목록을 축소하며, 동남아시아의 NOR 플래시 메모리 시장에서 고부가가치 컨텐츠의 확대를 뒷받침하고 있습니다.

동남아시아 지역 외부에 위치한 파운드리 업체에 대한 과도한 의존

동남아시아의 NOR 플래시 메모리 시장에서 가장 큰 구조적 제약은 해당 지역이 대량의 NOR 플래시를 소비하고 있음에도 불구하고 이를 생산하는 웨이퍼 제조 거점을 확보하지 못하고 있다는 점에 있습니다. 동남아시아는 여전히 뿌리 깊은 팹 갭에 직면해 있으며, 이 지역이 보다 심층적인 반도체 생태계 구축을 시도하고 있음에도 불구하고 칩 생산은 중국과 대만에 집중되어 있습니다. 중국에서 성숙한 로직 노드의 확대로 자원이 조기에 재배분됨에 따라, 이미 NOR 플래시 생산에 압박이 가해지고 있으며, 베트남이나 말레이시아 등지의 조립업체에 대한 공급이 부족해지고 있습니다. 2026년 1월에 발표된 미국과 대만의 무역·투자 관련 합의에 따라, 대만의 반도체 투자 중 2,500억 달러가 미국에 투입될 예정이며, 이에 따라 새로운 업스트림 공정 팹 생산 능력이 동남아시아로 대규모로 이전되지 않을 것이라는 전망이 강해지고 있습니다. NOR 플래시의 인증 공급업체 기반이 제한적이기 때문에 할당량이 부족한 상황에서는 현지 제조업체가 조달처를 쉽게 다각화할 수 없습니다. 따라서 예측 기간의 대부분 동안 동남아시아의 NOR 플래시 메모리 시장은 지정학적 충격이나 공급업체의 우선순위 결정에 영향을 받기 쉬운 상황에 놓이게 될 것입니다.

부문별 분석

시리얼 NOR 플래시는 2025년 매출의 62.1%를 차지했으며, 같은 해 동남아시아의 NOR 플래시 시장 점유율의 62.1%를 차지했습니다. 또한, 2026년부터 2031년에 걸쳐 유형별 부문 중 가장 높은 연평균 성장률(CAGR) 7.5%로 성장을 지속하고, 있으며, 이는 해당 분야의 주도적 지위가 약화되기는커녕 오히려 강화되고 있음을 보여줍니다. 이 부문은 지역 제조 거점과 긴밀히 협력하고 있습니다. SPI 연결, 핀 수 감소, 소형 기판 요구 사항이 가전제품, 통신 기기, 다양한 산업용 제품에 사용되는 마이크로컨트롤러를 많이 활용한 설계에 부합하기 때문입니다. 또한, 인플레이스 실행 기능 덕분에 섀도 RAM의 필요성이 줄어들어, 비용 관리가 제품 아키텍처에 큰 영향을 미치는 이 지역에서 BOM(부품표) 비용 부담을 완화하고 있습니다. 2026년, 윈본드는 이러한 수요 패턴에 부응하는 고속 인터페이스와 저전력 폼 팩터를 갖춘 고밀도 직렬 NOR 및 자동차용 등급 제품의 로드맵을 지속적으로 확대해 나갈 것입니다.

그 결과, 동남아시아의 NOR 플래시 메모리 시장에서 시리얼 NOR는 대대적인 설계 변경을 강요하지 않으면서도 대량 생산되는 소비자용 플랫폼과 새로운 엣지 디바이스 모두에 활용되고 있습니다. 웨어러블 기기, Wi-Fi 모듈, IoT 엔드포인트, 스마트 가전 등은 모두 이 부문이 제공하는 공간 효율성과 표준화된 컨트롤러의 호환성이라는 이점을 누리고 있습니다. 따라서 동남아시아의 NOR 플래시 메모리 산업에서는 특정 대역폭이나 레거시 시스템의 조건에 따라 다른 방향성이 요구되는 경우를 제외하고, 대부분의 신규 설계에서 시리얼 NOR를 기본 선택지로 계속 채택하고 있습니다. 병렬 NOR 플래시에도 여전히 그 역할이 있지만, 그 용도는 주로 더 넓은 버스가 운영상 여전히 유용한 구형 산업용 컨트롤러, 자동차용 디스플레이, 부팅 처리가 빈번하게 이루어지는 시스템으로 한정되어 있습니다. 인피니언(Infineon)과 윈본드(Winbond)가 제공하는 자동차 등급 병렬 제품은 2024년에도 여전히 해당 아키텍처를 필요로 하는 ECU 및 인포테인먼트 플랫폼을 위해 확고한 틈새 시장을 유지했습니다. 동남아시아의 NOR 플래시 메모리 시장의 장기적인 방향성은 여전히 시리얼 제품에 명확히 중점을 두고 있습니다. 이는 해당 지역의 신규 조립 프로그램 대부분이 콤팩트한 레이아웃, 핀 수 감소, 플랫폼 재사용의 용이성을 우선시하고 있기 때문입니다.

2025년에는 쿼드 SPI가 44.8%로 인터페이스 매출 점유율에서 가장 큰 비중을 차지했으며, 이는 주류 전자기기 조립 부문에서 이 기술이 광범위하게 도입된 실적을 반영한 것입니다. 옥탈과 xSPI는 2026년부터 2031년까지 7.7%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측되며, 이는 프로세서 및 자동차 시스템이 더 높은 읽기 대역폭을 요구함에 따라 성능 요구 사항이 꾸준히 변화하고 있음을 보여줍니다. 이러한 세부 내역은 동남아시아의 NOR 플래시 시장의 현황을 여실히 보여주고 있으며, 기존 방식의 대량 생산과 미래를 내다본 신규 설계 프로젝트가 각각 다른 속도로 진행되고 있습니다. 쿼드 SPI는 많은 기존 마이크로컨트롤러 플랫폼이 이미 이를 지원하고 있으며, 통신 모듈이나 소비자용 제품에서의 도입 기반도 넓기 때문에 여전히 깊이 자리 잡고 있습니다. 그 때문에 엔지니어링 팀이 더 빠른 규격에 대응할 준비를 하고 있는 와중에도, 쿼드 SPI는 계속해서 견조한 판매량을 유지하고 있습니다.

동남아시아의 NOR 플래시 메모리 시장에서는 자동차용 프로세서, AI 지원 컨트롤러, 고성능 임베디드 시스템에서 실시간 코드 실행이 보편화됨에 따라 옥탈 SPI와 xSPI의 입지가 확대되고 있습니다. 인피니언의 SEMPER 포트폴리오는 산업용 및 자동차용에 최적화된 내구성과 유지 특성을 갖춘 옥탈 SPI 및 HYPERBUS를 지원하며, 이는 인터페이스 업그레이드가 이미 까다로운 용도의 요구 사항을 충족하고 있음을 보여줍니다. STMicroelectronics 역시 최신 STM32N 시리즈 디바이스에서 XSPI의 8비트 및 16비트 구성을 지원하고 있으며, 이는 컨트롤러 생태계가 XSPI 지원을 염두에 두고 구축되고 있음을 뒷받침합니다. 싱글 및 듀얼 SPI 채널은 저가형 블루투스 모듈, IoT 센서, 보급형 웨어러블 기기에서 특히 베트남이나 인도네시아와 같이 가격을 중시하는 시장에서 여전히 중요합니다. 그러나 플랫폼 설계의 방향성은 명확하며, 동남아시아의 NOR 플래시 메모리 시장에서는 대규모 Quad SPI 기반은 물론, 옥탈 및 xSPI로의 전환 경로를 모두 지원할 수 있는 공급업체가 점점 더 높은 평가를 받게 될 것으로 보입니다.

32-64메가비트 범주는 2025년에 매출의 27.7%를 차지하며, 지역 시장에서 가장 큰 용량 구간을 형성했습니다. 이 대역은 주류 Wi-Fi 칩, 블루투스 SoC, 스마트 미터, 그리고 많은 저가-중가형 웨어러블 기기의 펌웨어 요구 사항과 밀접하게 부합하며, 이것이 주요 조립 거점에서의 수량 면에서의 우위를 설명해 줍니다. 또한, 폭넓은 제품 라인업과 조달 리드타임 단축이라는 장점도 있는데, 이는 재고를 최소한으로 유지하며 운영 중인 제조업체에게 중요한 요소입니다. 그런 의미에서 이 부문은 소비자용 및 통신 부문 수요 주기를 통해 동남아시아의 NOR 플래시 메모리 시장을 안정화해 온 설치 기반의 대부분을 차지하고 있습니다. 이는 특수한 최종 용도라기보다는 일상적인 전자기기 생산과 가장 밀접하게 관련된 단계입니다.

최상위 부문인 256메가비트 초과 부문은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.3%를 나타낼 것으로 예측되며, 이는 성장률이 가장 높은 용량 대역이 될 것입니다. 그 주된 원인은 AI 기반 서버 수요입니다. GB200 베이스 랙은 기존 랙보다 훨씬 더 많은 NOR 플래시 디바이스가 필요하기 때문에 자원을 대용량 부품으로 재분배하기 시작했습니다. 마크로닉스사는 3D NOR 플래시 디바이스의 샘플 제공을 2026년 하반기로 예정하고 있으며, 2027년 양산 개시를 목표로 하고 있다고 발표했습니다. 이는 기존 2D NOR 구조의 용량 한계에 대한 업계의 직접적인 대응을 보여줍니다. 8메가비트에서 32메가비트에 이르는 중간 용량 대역은 IoT 및 휴대용 진단 기기에 있어 여전히 중요하며, 한편 128메가비트에서 256메가비트에 이르는 용량 대역은 네트워크 장비, 보안 액세스 장치, 자동차용 서브시스템을 뒷받침하고 있습니다. 이로 인해 동남아시아의 NOR 플래시 메모리 시장에서는 단일 용량 제품군만으로는 모든 성장 부문을 충족시킬 수 없는 다층적인 수요 패턴이 나타나고 있습니다. 또한, 이는 소비자의 구매 주기, 인프라 확충, AI 주도의 할당 압력 등의 요인으로 인해 수요가 변동하는 상황에서 주류 노드와 대용량 노드를 모두 아우르는 공급업체가 수요를 포착하는 데 있어 유리한 입장에 있다는 것을 의미합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the south east asia NOR flash market size is expected to grow from USD 90.82 million in 2025 to USD 96.28 million in 2026 and is forecast to reach USD 128.90 million by 2031 at 6.01% CAGR over 2026-2031.

This report is Segmented by NOR Flash Type (Serial, and Parallel), Interface (SPI Single/Dual, and More), Density (2 Megabit and Less, and More), Voltage (3V Class, 1. 8V, and More), End-User Application (Communication, and More), Process Technology Node (65 Nm, 45 Nm, and More), and Packaging Type (WLCSP/CSP, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

South East Asia NOR Flash Market Trends and Insights

Government-Led Incentives Driving Expansion In Electronics Manufacturing

Government policy has become one of the clearest near-term demand supports for the Southeast Asia NOR Flash Memory market because incentive programs are drawing more assembly, packaging, and electronics manufacturing projects into the region. Vietnam's Circular 33/2025/TT-BKHCN set four eligibility criteria for tax relief for electronics manufacturers, including the use of Vietnam-designed or manufactured semiconductors and at least 30% domestic supply-chain participation, which encourages more localized component sourcing around chip-based products. The Johor-Singapore Special Economic Zone launched in January 2025 and offers a 5% corporate tax rate for qualifying electronics and semiconductor operations for up to 15 years, which improves the case for suppliers that want to stay close to OEM design and assembly centers. Thailand's national semiconductor roadmap targets more than 230,000 highly skilled personnel over a 25-year period, showing that the country is treating semiconductor capability as a long-cycle industrial priority rather than a short policy window. Malaysia's New Incentive Framework became operational on March 1, 2026, and reshaped manufacturing support around electronics, semiconductor packaging, and precision engineering, which broadens the base of plants that consume code storage and boot memory. As these frameworks shorten location decisions for Tier-1 OEMs, they increase the installed base of electronics production lines that generate direct and repeat NOR Flash demand.

Formation And Growth Of Automotive Electronics Clusters In The Region

Automotive electronics clusters are driving the Southeast Asia NOR Flash Memory market higher, as every move toward smart cockpits, ADAS, EV power management, and OTA software increases demand for reliable firmware storage. Multi-Code Electronics and Huizhou Foryou General Electronics signed a manufacturing and development agreement in September 2025 to localize cockpit domain controllers and connected-vehicle technology across ASEAN, with MCE investing RM150 million to RM200 million (USD 34 million to USD 45 million) near Perodua's manufacturing hub. VinFast reached more than 60% EV localization in 2025 and is targeting 84% by 2026, implying increased procurement of automotive-grade memory for ECUs and battery management systems. Malaysia also has a structural advantage because its semiconductor export base and automotive development agenda are converging under national policies supported by the Malaysia Automotive, Robotics and IoT Institute. In practice, this means more vehicle programs in the region are moving from basic memory needs toward safety-qualified devices with stronger reliability and retention requirements. That shift raises entry barriers, concentrates approved vendor lists, and supports higher-value content in the Southeast Asia NOR Flash Memory market.

Heavy Dependence On Foundries Located Outside South East Asia

The biggest structural constraint on the South East Asia NOR Flash Memory market is that the region consumes large volumes of NOR Flash but does not control the wafer fabrication base that produces it. South East Asia still faces a persistent fab gap, with chipmaking concentrated in China and Taiwan even as the region tries to build a deeper semiconductor ecosystem. Earlier allocation shifts in China toward mature logic node expansion have already put pressure on NOR Flash output, tightening supply for assemblers in countries such as Vietnam and Malaysia. U.S.-Taiwan trade and investment commitments announced in January 2026 directed USD 250 billion in Taiwanese semiconductor investment toward the United States, reinforcing the view that new upstream fab capacity is not moving to Southeast Asia at scale. Because the qualified supplier base in NOR Flash is narrow, local manufacturers cannot easily diversify when allocation is tight. This leaves the Southeast Asia NOR Flash Memory market exposed to geopolitical shocks and supplier prioritization decisions for most of the forecast period.

Other drivers and restraints analyzed in the detailed report include:

- Rising Trend Of Outsourcing In Wearable And Point-Of-Care Device Manufacturing

- Accelerated Deployment Of 5G And Fiber-To-The-Home Network Infrastructure

- Intensified Margin Pressures From Cost-Competitive Chinese Vendors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR Flash accounted for 62.1% of revenue in 2025, representing 62.1% of the South East Asia NOR Flash market share that year. It also posted the fastest projected CAGR among type segments at 7.5% for 2026-2031, showing that leadership is being reinforced rather than eroded. The segment aligns with the regional manufacturing base because SPI connectivity, lower pin counts, and compact board requirements match the microcontroller-heavy designs used in consumer electronics, communications equipment, and a broad range of industrial products. Execute-in-place capability also reduces the need for shadow RAM, which keeps bill-of-materials pressure under control in a region where cost discipline shapes product architecture. In 2026, Winbond continues to extend its higher-density serial NOR and automotive-grade product roadmap, with faster interfaces and low-power form factors that align with this demand pattern.

The practical outcome is that serial NOR serves both high-volume consumer platforms and newer edge devices without forcing major design changes across the Southeast Asia NOR Flash Memory market. Wearables, Wi-Fi modules, IoT endpoints, and smart appliances all benefit from the segment's space efficiency and standardized controller compatibility. That is why the Southeast Asia NOR Flash Memory industry continues to treat serial NOR as the default option for most new designs unless a specific bandwidth or legacy system condition points elsewhere. Parallel NOR Flash still has a role, but it is mostly tied to older industrial controllers, automotive displays, and boot-intensive systems where a wider bus remains operationally useful. Automotive-grade parallel offerings from Infineon and Winbond preserved a protected niche in 2024 for ECUs and infotainment platforms that still require that architecture. Even so, the long-term direction of the Southeast Asia NOR Flash Memory market remains clearly aligned with serial products, as most new regional assembly programs prioritize compact layouts, lower pin count, and easier platform reuse.

Quad SPI held the largest interface revenue share at 44.8% in 2025, reflecting its wide installation base across mainstream electronics assembly. Octal and xSPI are forecast to grow at the fastest CAGR of 7.7% from 2026 to 2031, indicating a steady shift in performance requirements as processors and vehicle systems demand higher read bandwidth. This split captures the current shape of the South East Asia NOR Flash market, where legacy volume and forward-looking design wins are moving at different speeds. Quad SPI remains deeply embedded because many existing microcontroller platforms already support it, and the installed base across communications modules and consumer products is large. That gives it continued volume strength even as engineering teams prepare for faster standards.

Octal and xSPI are gaining ground as real-time code execution becomes more common in automotive processors, AI-capable controllers, and higher-performance embedded systems in the Southeast Asia NOR Flash Memory market. Infineon's SEMPER portfolio supports Octal SPI and HYPERBUS with endurance and retention characteristics optimized for industrial and automotive use, demonstrating that interface upgrades are already aligned with demanding applications. STMicroelectronics also supports XSPI 8-bit and 16-bit configurations in its newer STM32N-series devices, confirming that controller ecosystems are now being built with xSPI readiness in mind. Single and dual SPI channels still matter in low-cost Bluetooth modules, IoT sensors, and entry wearables, especially in cost-sensitive markets such as Vietnam and Indonesia. Yet the direction of platform design is clear, and the South East Asia NOR Flash Memory market will increasingly reward suppliers that can support both the large Quad SPI base and the migration path toward Octal and xSPI.

The more than 32 to 64 megabit category held 27.7% of revenue in 2025, making it the largest density tier in the regional market. This band aligns closely with the firmware needs of mainstream Wi-Fi chips, Bluetooth SoCs, smart meters, and many low-to-mid-tier wearables, which explains its volume advantage in core assembly hubs. It also benefits from broad product catalogs and shorter procurement lead times, which matter for manufacturers running lean inventories. In that sense, the segment captures a large part of the installed base that has kept the Southeast Asia NOR Flash Memory market stable across consumer and communications demand cycles. It is the tier most closely tied to everyday electronics output rather than to specialized high-end applications.

At the top end, the greater than 256 megabit segment is projected to grow at a 7.3% CAGR from 2026 to 2031, which makes it the fastest-growing density range. AI-driven server demand is a major reason, because a GB200-based rack requires far more NOR Flash devices than a conventional rack and has begun to reallocate resources toward higher-capacity parts. Macronix stated that sampling of 3D NOR Flash devices is planned for the second half of 2026, with mass production targeted for 2027, which signals a direct industry response to density limits in traditional 2D NOR structures. Intermediate ranges from 8 megabit to 32 megabit remain important for IoT and portable diagnostics, while 128 megabit to 256 megabit supports network equipment, secure access devices, and vehicle subsystems. This produces a layered demand pattern in the South East Asia NOR Flash Memory market where no single density family can serve every growth pocket. It also means suppliers that span mainstream and high-capacity nodes are better placed to capture demand as purchasing shifts between consumer cycles, infrastructure build-outs, and AI-led allocation pressure.

Complete Report Scope:

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Others - 1.2 V Class and Similar Sub-1.8 V (2.5 V, 5 V, etc.)

- By End-user Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-user Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Geography (Value, Volume)

- Vietnam

- Indonesia

- Philippines

- Thailand

- Malaysia

List of Companies Covered in this Report:

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Puya Semiconductor (Shanghai) Co. Ltd.

- Samsung Semiconductor

- Alliance Memory

- AMIC Technology Corporation (NEW)

- AP Memory Technology Co. Ltd. (NEW)

- Yangtze Memory Technologies Co. Ltd. (YMTC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-Led Incentives Driving Expansion in Electronics Manufacturing

- 4.2.2 Formation and Growth of Automotive Electronics Clusters in the Region

- 4.2.3 Rising Trend of Outsourcing in Wearable and Point-of-Care Device Manufacturing

- 4.2.4 Accelerated Deployment of 5G and Fiber-to-the-Home Network Infrastructure

- 4.2.5 Supply-Chain Re-shoring Initiatives by Global Tier-1 OEMs

- 4.2.6 Surging Demand for NOR Flash in Edge AI Microcontrollers

- 4.3 Market Restraints

- 4.3.1 Heavy Dependence on Foundries Located Outside South East Asia

- 4.3.2 Intensified Margin Pressures from Cost-Competitive Chinese Vendors

- 4.3.3 Increased Adoption of Emerging Alternative Non-Volatile Memory Technologies

- 4.3.4 Chronic Skilled-Labour Gaps in Sub-20 nm Lithography

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory and Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 More than 2 to 4 Megabit

- 5.3.3 More than 4 to 8 Megabit

- 5.3.4 More than 8 to 16 Megabit

- 5.3.5 More than 16 to 32 Megabit

- 5.3.6 More than 32 to 64 Megabit

- 5.3.7 More than 64 to 128 Megabit

- 5.3.8 More than 128 to 256 Megabit

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Others - 1.2 V Class and Similar Sub-1.8 V (2.5 V, 5 V, etc.)

- 5.5 By End-user Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other End-user Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and More

- 5.6.2 65 nm

- 5.6.3 55 nm (including 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

- 5.8 By Geography (Value, Volume)

- 5.8.1 Vietnam

- 5.8.2 Indonesia

- 5.8.3 Philippines

- 5.8.4 Thailand

- 5.8.5 Malaysia

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Micron Technology Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Renesas Electronics Corporation

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.11 Samsung Semiconductor

- 6.4.12 Alliance Memory

- 6.4.13 AMIC Technology Corporation (NEW)

- 6.4.14 AP Memory Technology Co. Ltd. (NEW)

- 6.4.15 Yangtze Memory Technologies Co. Ltd. (YMTC)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis