|

시장보고서

상품코드

2072558

미국의 NOR 플래시 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

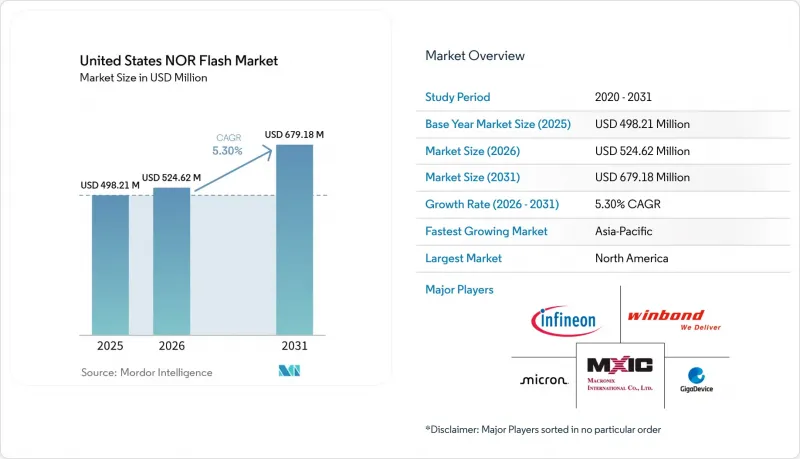

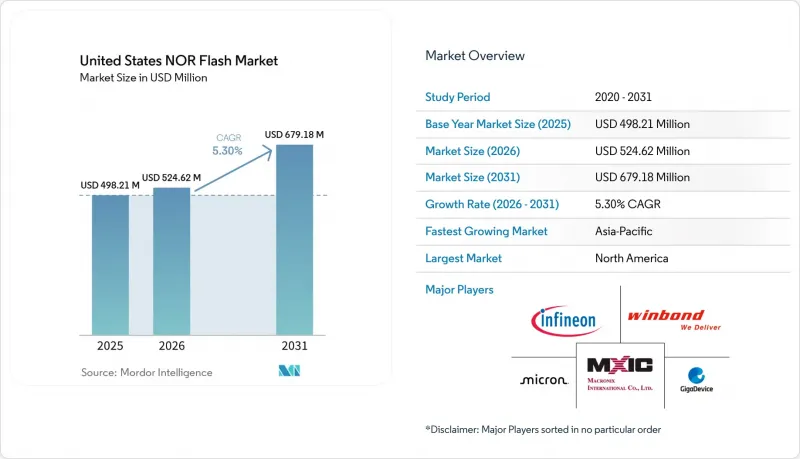

Mordor Intelligence에 의하면, 미국의 NOR 플래시 시장 규모는 2025년에 4억 9,821만 달러로 평가되었습니다. 2026년 5억 2,462만 달러에서 2031년까지 6억 7,918만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 5.3%를 나타낼 전망입니다.

본 보고서는 유형별(직렬 및 병렬), 밀도별(2메가비트 이하 및 그 이상), 전압별(3V급, 1.8V급 이상), 최종 사용자용도별(소비자용 전자기기, 통신기기, 자동차 등), 공정 기술 노드별(65nm, 55nm 등), 패키지 유형별(WLCSP/CSP 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(단위)으로 제시되어 있습니다.

미국의 NOR 플래시 시장 동향 및 인사이트

미국 ADAS 및 기능 안전 ECU 분야에서 고신뢰성 NOR에 대한 수요 급증

레벨 2+ 및 레벨 3 자율주행 기술을 도입한 자동차 제조업체들은 현재 ISO 26262 ASIL-D를 준수하는 플래시 메모리가 필요합니다. 인피니온의 ‘Semper’ 제품군은 이 인증을 획득했으며, 이를 통해 Tier 1 공급업체들은 결정론적 부팅을 보장하면서도 중복성 계층을 줄일 수 있게 되었습니다. 존형 아키텍처에서는 다수의 소형 ECU가 고성능 컨트롤러로 통합되기 때문에 존당 밀도 요구 사항이 128 Mb-512 Mb까지 높아지고 있습니다. 텍사스주에서 생산되는 테슬라의 AI5 플랫폼은 안전상 중요한 펌웨어를 격리하기 위해 외부 시리얼 NOR를 채택하고 있으며, 수년에 걸친 공급 계약은 이미 2029년형 모델까지 연장되었습니다. 이러한 요인들이 복합적으로 작용하여, 시리얼 NOR는 전기차(EV) 생산 확대의 핵심 경로로 자리매김하고 있습니다.

CHIPS법 및 과학법에 따른 인센티브가 국내 NOR 제조를 가속화

2025년 7월까지 ‘CHIPS and Science Act’는 40개 프로젝트에 총 364억 달러를 지원했습니다. 그중 4분의 3은 애리조나주, 뉴욕주, 텍사스주에 집중되어 있으며, 자동차 및 방위 산업 단지가 위치한 인근에 메모리 제조가 가능한 팹을 구축하고 있습니다. 지역 보조금 덕분에 아시아 생산과의 비용 격차가 줄어들고 있으며, 암콜의 피오리아에 위치한 WLCSP 라인은 자동차 제조업체에 ITAR 준수 패키징 옵션을 제공합니다. 웨이퍼 시작 물량은 2028년까지 실질적으로 증가하지는 않겠지만, 고객들은 이미 향후 생산 능력을 확보하기 위해 ‘테이크 오어 페이(take-or-pay)’ 방식의 주문을 진행하고 있으며, 이는 국내 조달을 통한 공급망에 대한 신뢰를 보여주는 것입니다.

28나노미터 노드를 초과하는 SPI-NAND의 높은 제조 비용

SPI-NAND는 28nm 공정 기술을 적용해 1Gb 밀도에서 1Mb당 약 0.015달러의 원가를 실현하고 있으며, 1Mb당 0.05달러를 넘는 수준에 머무르는 NOR에 비해 더 경제적인 선택지가 되고 있습니다. 이러한 현저한 비용 차이로 인해, 비용에 민감한 각 OEM 업체들은 특히 시작 지연 시간이 중요한 요소가 아닌 용도에서 SPI-NAND로의 전환을 추진하고 있습니다. 각 파운드리 업체들은 수익성이 높은 로직 제품 생산을 점점 더 우선시하고 있어, NOR는 구형 제조 장비로만 생산되는 상황이 되고 있습니다. 이러한 구형 장비들은 NAND가 누리고 있는 규모의 경제라는 이점이 부족하여, 비용 격차를 더욱 벌리고 있습니다. 그 결과, NOR 기술은 특히 고밀도 응용 분야에서 비용 효율성 측면에서 경쟁력을 유지하는 데 어려움을 겪고 있습니다.

부문별 분석

2025년, 시리얼 NOR 플래시는 미국의 NOR 플래시 시장 점유율의 60.9%를 차지했습니다. 자동차 OEM 업체들이 기판 크기를 줄이기 위해 부피가 큰 병렬 디바이스를 4포트 및 8포트 디바이스로 교체하고 있기 때문에 이러한 추세는 더욱 확대되고 있습니다. 이러한 추세에 따라 벤더들은 보안 부팅 기능을 프리미엄 마진으로 업셀링할 수 있게 되었으며, 이에 따라 미국의 NOR 플래시 시장이 강화되고 있습니다. 병렬 NOR는 15년간의 폼·핏·기능 보증이 공간적 제약을 상쇄하기 때문에 방위용 내방사선 설계 및 구형 산업용 컨트롤러에서 여전히 사용되고 있습니다. 따라서 공급업체들은 두 인터페이스를 모두 듀얼 소스로 제공하고 있지만, 출하량 증가와 로드맵에 대한 투자는 분명히 시리얼 제품에 유리하게 작용하고 있어, 미국의 NOR 플래시 시장 전체가 확대되고 있음에도 불구하고 병렬 제품의 매출은 정체 상태를 보이고 있습니다.

2세대 시리얼 제품은 400 MB/s 속도의 인플레이스 실행과 AES-256 암호화를 제공하며, 존형 ECU가 DRAM을 거치지 않고 리눅스 이미지를 직접 로드할 수 있게 해줍니다. RISC-V MCU의 보급에 따라 스타트업 기업들은 폭넓은 툴체인 지원을 이유로 시리얼 NOR를 선택하고 있으며, 이로 인해 생태계 효과가 강화되면서 병렬 NOR는 더욱 주변화되고 있습니다. 그 결과, 시리얼 NOR는 자동차 제조업체, 산업용 IoT, 5G 인프라에 있어 전략적 핵심이 되는 반면, 병렬 NOR는 레거시 시장의 수익원으로서의 역할에 그치게 될 것입니다.

2025년에는 쿼드 SPI가 매출의 46.2%를 차지했으나, 옥탈 및 xSPI는 연평균 성장률(CAGR) 10.6%로 더 빠르게 성장하고 있습니다. 이러한 성장은 중복된 펌웨어 이미지를 효율적으로 로드하기 위해 400 MB/s의 대역폭이 필요한 중앙 집중형 자동차용 컨트롤러에 대한 수요 증가에 힘입어 이루어지고 있습니다. 이러한 전환으로 인해 설계자들이 비트당 비용보다 속도와 결정론적 읽기 성능을 우선시하게 되면서, 미국의 NOR 플래시 시장의 고수익 부문이 확대되고 있습니다. 싱글 SPI 및 듀얼 SPI는 비용 효율성을 중시하는 소비자용 부문으로 점차 밀려나고 있지만, 쿼드 SPI는 여전히 중급 시장의 표준으로 자리 잡고 있습니다. 한편, 옥탈 SPI는 뛰어난 성능 덕분에 프리미엄급 선택지로 부상하고 있습니다.

옥탈 SPI 디바이스에는 현재, 과거에는 병렬 버스에서만 지원되던 차동 신호 전송 및 ECC와 같은 고급 기능이 탑재되어 있습니다. JEDEC의 xSPI 2.0 사양에 따라 처리량이 더욱 향상되어, 적은 핀 수의 패키지가 가진 장점을 유지하면서도 PCIe Gen2 수준에 근접하고 있습니다. 이러한 발전으로 인해, 과거 병렬 인터페이스 사용을 정당화했던 성능 격차가 크게 줄어들었습니다. OEM 각사가 2028년형 모델을 위한 제어 유닛의 재설계를 추진하는 가운데, xSPI의 도입이 가속화될 것으로 예측됩니다. 이러한 추세에 따라 xSPI는 고신뢰성 용도를 위한 주요 부팅 표준으로서의 입지를 확립하고, 시장 내 위상을 더욱 공고히할 것입니다.

2025년에는 128 Mb급 제품도 28.7%의 시장 점유율을 유지했으나, 리눅스 기반 인포테인먼트 스택 및 ADAS 센서 융합 기술로 인해 더 대용량의 펌웨어 파티션에 대한 수요가 증가하면서, 수요는 256 MB-1 GB 용량으로 이동하고 있습니다. 이러한 고밀도화로의 전환에 따라, 평균 판매 가격의 상승이 다이 크기의 확대에 따른 단점을 상쇄하고 있기 때문에 미국의 NOR 플래시 시장 규모는 확대되고 있습니다. 한편, 저용량 제품, 특히 8 Mb 이하 제품은 마이크로컨트롤러에 내장된 MRAM 덕분에 64 Mb 미만의 외부 코드 저장 공간이 더 이상 필요하지 않게 되어 감소 추세를 보이고 있습니다. 이러한 추세는 고성능 용도 분야에서 대용량 솔루션에 대한 선호도가 높아지고 있음을 여실히 보여주고 있습니다.

기가비트급 용량을 새로운 리소그래피 기술의 발전에 의존하지 않고 실현하기 위해, 각 벤더사는 하나의 BGA 또는 WLCSP 패키지 내에 512 Mb 다이 2개를 적층하고 있습니다. 이러한 접근 방식을 통해 성숙한 55nm 공정을 계속 활용할 수 있을 뿐만 아니라, 자동차 용도에서 신뢰성을 유지하는 데 필수적인 자동차 인증 기준도 충족할 수 있습니다. 또한, 이 전략은 임베디드형 대체 제품에 의한 저가 시장 잠식을 막기 위한 안전장치 역할도 합니다. 그 결과, 시장에서는 수량 증가가 아닌 밀도를 원동력으로 한 변화가 진행되고 있으며, 2031년까지는 밀도 중심의 제품 구성 변화가 주요 수익원이 될 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the united states NOR flash market size was valued at USD 498.21 million in 2025 and is estimated to grow from USD 524.62 million in 2026 to reach USD 679.18 million by 2031, at a CAGR of 5.3% during the forecast period (2026-2031).

This report is Segmented by Type (Serial, and Parallel), Density (2 Megabit and Less NOR, and More), Voltage (3V Class, 1. 8V Class, and More), End-User Application (Consumer Electronics, Communication Equipment, Automotive and More), Process Technology Node (65 Nm, 55 Nm, and More), and Packaging Type (WLCSP/CSP, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

United States NOR Flash Market Trends and Insights

Surge in Demand for High-Reliability NOR in U.S. ADAS and Functional-Safety ECUs

Automakers that are rolling out Level 2+ and Level 3 autonomy now require flash that meets ISO 26262 ASIL-D. Infineon's Semper family attained that certificate, enabling Tier 1s to reduce redundancy layers while still guaranteeing deterministic boot. Zonal architectures consolidate many small ECUs into high-performance controllers, lifting density needs to 128 Mb-512 Mb per zone. Tesla's AI5 platform produced in Texas relies on external serial NOR to isolate safety-critical firmware, and multiyear supply contracts already stretch to the 2029 model year. These factors collectively place serial NOR on the critical path of EV production ramps.

CHIPS and Science Act Incentives Accelerating Domestic NOR Manufacturing

Through July 2025, CHIPS disbursed USD 36.4 billion across 40 projects, three-quarters of which reside in Arizona, New York, and Texas, anchoring memory-capable fabs near automotive and defense clusters. Local subsidies narrow the cost gap with Asian production, and Amkor's Peoria WLCSP line gives automakers an ITAR-compliant packaging option. While wafer starts will not meaningfully add until 2028, customers are already placing take-or-pay orders that secure futures capacity, signaling confidence in a domestically sourced supply chain.

High Fabrication Cost Versus SPI-NAND Beyond 28-Nanometer Nodes

SPI-NAND achieves a cost of approximately USD 0.015 per Mb at a 1 Gb density on 28 nm technology, making it a more economical choice compared to NOR, which remains above USD 0.05 per Mb. This significant cost difference is prompting cost-sensitive OEMs to transition to SPI-NAND, especially in applications where boot latency is not a critical factor. Foundries are increasingly prioritizing high-margin logic production, leaving NOR confined to older manufacturing equipment. This older equipment lacks the scale-economy advantages that NAND benefits from, further widening the cost gap. As a result, NOR technology struggles to compete in terms of cost efficiency, particularly in high-density applications.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Roll-Out of 5G mmWave Base-Stations Driving NOR Code-Storage Demand

- Industrial IoT Deployments in Harsh U.S. Environments Needing Instant-Boot Memory

- Limited Domestic 300-Millimeter Capacity Constraining High-Density NOR Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR Flash accounted for 60.9% of the United States NOR Flash market share in 2025, a lead that is widening as automotive OEMs replace bulky parallel devices with quad- and octal-variant devices to trim board size. The trend strengthens the United States NOR Flash market by allowing vendors to upsell secure-boot features at premium margins. Parallel NOR still services defense rad-hard designs and legacy industrial controllers where 15-year form-fit-function commitments override space constraints. Vendors therefore dual-source both interfaces, but volume growth and roadmap investment clearly favor serial parts, keeping parallel revenue flat even as the overall United States NOR Flash market size rises.

Second-generation serial parts offer execute-in-place at 400 MB/s and AES-256 encryption, enabling zonal ECUs to load Linux images directly without DRAM staging. As RISC-V MCUs proliferate, start-ups pick serial NOR for its broad tool-chain support, reinforcing an ecosystem effect that further marginalizes parallel. Consequently, serial NOR becomes the strategic linchpin for automakers, industrial IoT, and 5G infrastructure, while parallel NOR becomes a legacy-harvest play.

Quad SPI captured 46.2% of revenue in 2025, yet octal and xSPI are growing faster, with a 10.6% CAGR. This growth is driven by the increasing demand for centralized automotive controllers, which require 400 MB/s bandwidth to load redundant firmware images efficiently. The shift is expanding the high-margin segment of the United States NOR Flash market, as designers prioritize speed and deterministic reads over cost per bit. Single- and dual-SPI are gradually being relegated to cost-sensitive consumer segments, while quad-SPI remains the mid-range standard. Octal SPI, on the other hand, is emerging as the premium choice due to its superior performance capabilities.

Octal devices now incorporate advanced features such as differential signaling and ECC, which were previously exclusive to parallel buses. JEDEC's xSPI 2.0 specification has further enhanced throughput, bringing it closer to PCIe Gen2 levels while maintaining the benefits of low-pin-count packages. This development has significantly reduced the performance gap that once justified the use of parallel interfaces. As OEMs prepare to redesign control units for the 2028 model years, the adoption of xSPI is expected to accelerate. This trend positions xSPI as the leading boot standard for high-reliability applications, solidifying its market position.

The 128 Mb tier retained 28.7% share in 2025, but Linux-based infotainment stacks and ADAS sensor fusion are driving the need for larger firmware partitions, pushing demand toward 256 MB-1 GB capacities. This shift toward higher densities is boosting the United States NOR Flash market size, as the increase in average selling prices outweighs the penalties associated with larger die sizes. Meanwhile, lower-density parts, particularly those <=8 Mb, are witnessing a decline as embedded MRAM within microcontrollers eliminates the requirement for external code storage below 64 Mb. This trend highlights the growing preference for higher-density solutions in advanced applications.

To achieve gigabit capacities without relying on new lithography advancements, vendors are stacking two 512 Mb dies within a single BGA or WLCSP package. This approach allows mature 55 nm processes to remain relevant while preserving automotive qualification standards, which are critical for maintaining reliability in automotive applications. Additionally, this strategy serves as a safeguard against the erosion of low-end sockets by embedded alternatives. As a result, the market is experiencing a shift driven by density rather than unit growth, positioning density-driven mix shifts as the primary revenue driver through 2031.

Complete Report Scope:

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less NOR

- 4 Megabit (More than 2 Mb) NOR

- 8 Megabit (More than 4 Mb) NOR

- 16 Megabit (More than 8 Mb) NOR

- 32 Megabit (More than 16 Mb) NOR

- 64 Megabit (More than 32 Mb) NOR

- 128 Megabit (More than 64 Mb) NOR

- 256 Megabit (More than 128 Mb) NOR

- Greater than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Sub-1.8 V Classes (1.2 V, 2.5 V, 5 V)

- By End-User Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-User Applications

- By Process Technology Node (Value)

- 90 nm and Older

- 65 nm

- 55 nm

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

List of Companies Covered in this Report:

- Infineon Technologies AG

- Micron Technology Inc.

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Renesas Electronics Corporation

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Elite Semiconductor Microelectronics Technology Inc.

- Puya Semiconductor (Shanghai) Co. Ltd.

- Alliance Memory Inc.

- STMicroelectronics NV

- Samsung Semiconductor

- SkyHigh Memory Limited

- Etron Technology Inc.

- AMIC Technology Corp.

- Cypress Semiconductor Corp.

- Teledyne e2v Semiconductors

- Fudan Microelectronics Group Co. Ltd.

- Silicon Storage Technology Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value-Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Surge in Demand for High-Reliability NOR in U.S. ADAS and Functional-Safety ECUs

- 4.3.2 Rapid Roll-Out of 5G mmWave Base-Stations Driving NOR Code-Storage Demand

- 4.3.3 DoD Aerospace and Defense Modernization Requiring Radiation-Tolerant NOR

- 4.3.4 Industrial IoT Deployments in Harsh U.S. Environments Needing Instant-Boot Memory

- 4.3.5 CHIPS and Science Act Incentives Accelerating Domestic NOR Manufacturing

- 4.3.6 Emerging Open-Source RISC-V MCU Ecosystem Standardizing on External NOR for Secure Boot

- 4.4 Market Restraints

- 4.4.1 High Fabrication Cost Versus SPI-NAND Beyond 28 nm Nodes

- 4.4.2 Adoption of Embedded MRAM and RRAM as Alternative Code Storage in MCUs

- 4.4.3 Limited Domestic 300 mm Capacity Constraining High-Density NOR Supply

- 4.4.4 Volatility in Critical Process Gas Supply (Neon, Fluorine) Raising Cost Unpredictability

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory and Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less NOR

- 5.3.2 4 Megabit (More than 2 Mb) NOR

- 5.3.3 8 Megabit (More than 4 Mb) NOR

- 5.3.4 16 Megabit (More than 8 Mb) NOR

- 5.3.5 32 Megabit (More than 16 Mb) NOR

- 5.3.6 64 Megabit (More than 32 Mb) NOR

- 5.3.7 128 Megabit (More than 64 Mb) NOR

- 5.3.8 256 Megabit (More than 128 Mb) NOR

- 5.3.9 Greater than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Sub-1.8 V Classes (1.2 V, 2.5 V, 5 V)

- 5.5 By End-User Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other End-User Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Older

- 5.6.2 65 nm

- 5.6.3 55 nm

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles

- 6.4.1 Infineon Technologies AG

- 6.4.2 Micron Technology Inc.

- 6.4.3 Winbond Electronics Corporation

- 6.4.4 Macronix International Co. Ltd.

- 6.4.5 GigaDevice Semiconductor Inc.

- 6.4.6 Renesas Electronics Corporation

- 6.4.7 Integrated Silicon Solution Inc.

- 6.4.8 Microchip Technology Inc.

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.11 Alliance Memory Inc.

- 6.4.12 STMicroelectronics NV

- 6.4.13 Samsung Semiconductor

- 6.4.14 SkyHigh Memory Limited

- 6.4.15 Etron Technology Inc.

- 6.4.16 AMIC Technology Corp.

- 6.4.17 Cypress Semiconductor Corp.

- 6.4.18 Teledyne e2v Semiconductors

- 6.4.19 Fudan Microelectronics Group Co. Ltd.

- 6.4.20 Silicon Storage Technology Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment