|

시장보고서

상품코드

2072557

아시아태평양의 NOR 플래시 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

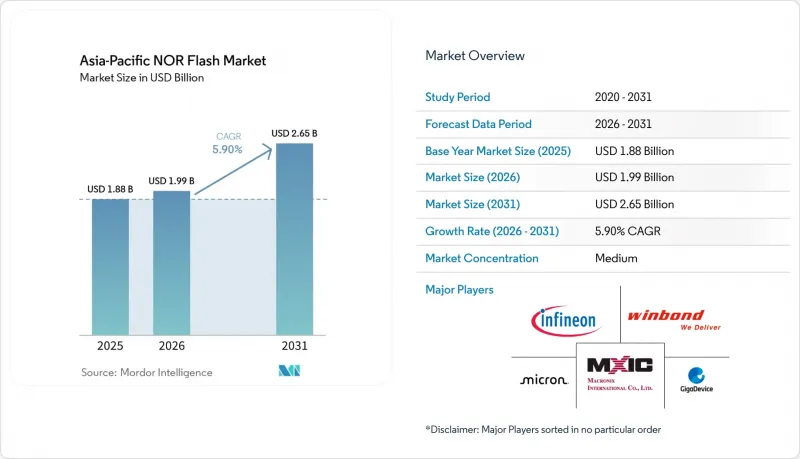

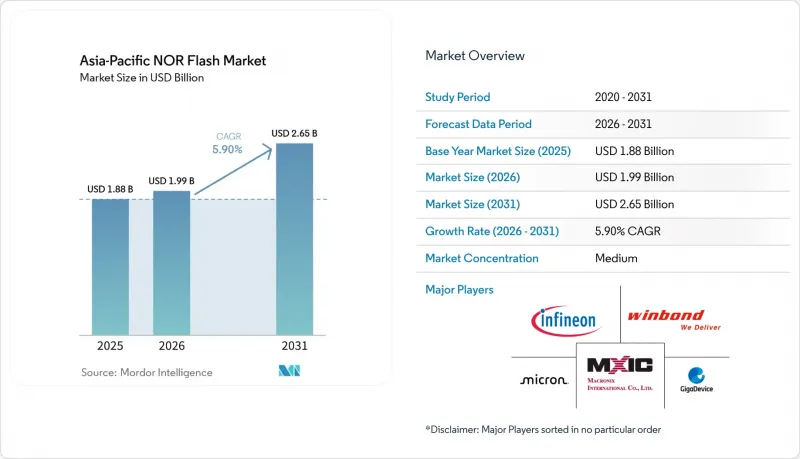

Mordor Intelligence에 의하면, 아시아태평양의 NOR 플래시 시장 규모는 2025년 18억 8,000만 달러로 평가되었습니다. 2026년에는 19억 9,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.9%로 성장을 지속하여, 2031년까지 26억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형(직렬 NOR 플래시 등), 인터페이스(쿼드 SPI 등), 밀도(2메가비트 이하 등), 전압(3V급 등), 최종 사용자용도(소비자용 전자기기 등), 공정 기술 노드(45nm, 55nm 등), 패키지 유형(WLCSP/CSP 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(단위)으로 제시되어 있습니다.

아시아태평양의 NOR 플래시 시장 동향 및 분석

중국과 일본의 자동차용 전자기기 분야에서 ADAS 및 인포테인먼트용 메모리 수요가 급증하고 있습니다.

중국 및 일본의 자동차 시스템에서는 세이프 부트 및 페일 오퍼레이셔널 기능을 위해 중복 NOR 어레이에 대한 의존도가 높아지고 있으며, 차량 1대당 평균 탑재량은 2024년의 32메가비트에서 2028년까지 128메가비트에 달할 것으로 예측됩니다. 일본의 Tier 1 공급업체들은 ISO 26262 ASIL-D 규격을 준수하기 위해 듀얼 채널 NOR를 탑재하고 있습니다. 인피니언의 SEMPER 디바이스는 2025년에 르네사스의 R-CAR Gen4 인증을 획득했으며, 이는 이 시장에서 일반적인 2-3년의 설계 채택 주기를 뒷받침하고 있습니다. ADAS만으로도 이미 이 지역의 자동차용 NOR 매출의 절반 이상을 차지하고 있습니다. 2025년 중국에서 2,700만 대의 자동차가 출하되었으며, 전동화가 진행되는 가운데 이 부문이 장기적인 수요의 기반이 되었습니다.

아시아태평양 설계 기업들의 옥탈 및 HyperBus NOR 아키텍처로의 전환

옥탈 및 xSPI 인터페이스는 2025년 출하량의 불과 15-18%에 불과하지만, 엣지 AI 및 자동차용 게이트웨이 컨트롤러에서 400 MB/s를 초과하는 대역폭에 대한 수요가 증가함에 따라 급속히 확대되고 있습니다. 인피니온은 2026년 3월, LPDDR 호환 NOR 메모리를 발표했습니다. 이로 인해 읽기 처리량이 800 MB/s로 두 배로 증가했으며, 배선도 간소화되었습니다. GigaDevice사의 1.2V 옥탈 제품은 배터리 구동형 IoT 노드에 대응하며, 동작 전류를 최대 40% 절감합니다. 대만과 한국의 설계 회사들이 엣지 AI 가속기를 xSPI로 전환하는 가운데, 공급업체들은 소비자용 전자기기의 가격 압박을 상쇄할 수 있는 수년에 걸친 고수익 계약을 확보하고 있습니다.

중국 본토로의 EUV 및 DUV 장비 수출 규제

2024년 10월에 시행된 ‘외국 직접 생산품 규정(Foreign Direct Product Rule)’ 확대 조치에 따라, 중국의 메모리 공장으로의 첨단 리소그래피 장비 출하가 금지됨에 따라, 당분간 중국 본토의 제조 공정은 40나노미터 및 그 이전 세대로 제한될 것입니다. 28나노미터 자동차용 NOR 메모리는 30-40%의 전력 절감 효과가 예상되므로, 이 규제는 자동차 설계 수주를 목표로 하는 중국 본토공급업체들에게 걸림돌이 될 것입니다. 일본이 미국의 정책에 동조함에 따라 도쿄 일렉트로ンの 에칭 시스템에 대한 접근이 차단되었고, 기술 격차가 더욱 확대되었습니다. 대만과 한국은 22나노미터로 나아가고 있는 반면, 중국은 성숙한 노드에 머물러 있습니다.

부문별 분석

2025년, 시리얼 NOR는 아시아태평양의 NOR 플래시 시장 점유율의 71.8%를 유지했습니다. 이는 SPI 및 Quad SPI 인터페이스가 소비자용 및 IoT용 부트 코드에 대한 수요의 상당 부분을 충족시키고 있기 때문입니다. 병렬 NOR는 매출액에서 차지하는 비중이 28.2%에 그치지만, 산업용 제어 및 안전성이 극히 중요한 자동차용 모듈 분야의 결정론적 지연 시간 요건에 힘입어 연평균 성장률(CAGR) 7.3%로 성장을 지속하고, 있습니다. 병렬 장치는 50나노초 미만의 액세스 시간이 필수적인 에어백 및 ABS에 계속해서 탑재되고 있습니다.

이에 반해, 시리얼 방식공급업체들은 하드웨어를 통한 신뢰의 근원(Root of Trust)과 중복성을 추가하여 병렬 방식의 기존 제조업체들에 도전하고 있으며, 차기 플랫폼 개편 시 경쟁이 더욱 치열해질 것으로 예측됩니다. 시리얼 아키텍처 역시 밀도와 신뢰성 측면에서 꾸준히 향상되고 있습니다. Macronix사의 ArmorBoot MX76은 1기가비트급 보안 부팅 기능을 구현하고 있으며, 과거에는 병렬 NOR에 국한되었던 ‘인플레이스 실행’ 및 보안 기능이 직렬 설계로 전환될 수 있음을 보여줍니다. 이러한 기능 강화를 제공하지 못하는 공급업체는 비용 중심의 소비자용 기기에만 국한될 위험이 있으며, 이 분야에서는 중국에서 새로 진입한 기업들과의 가격 경쟁으로 인해 이익률이 압박받고 있습니다.

SPI 싱글/듀얼은 2025년에 47.6%의 점유율을 차지하며 시장을 휩쓸었습니다. 그러나 대역폭 상한이 약 80 MB/s로 제한되어 있어, 데이터 집약형 시스템에 적용하는 데에는 제약이 있습니다. 이러한 제한이 있음에도 불구하고, 고속 성능이 필수적이지 않은 비용 중심의 용도에서는 여전히 선호되는 선택지입니다. 시장 점유율의 약 35%를 차지하는 쿼드 SPI는 더 빠른 펌웨어 업데이트가 필요한 중급형 스마트폰 및 산업용 게이트웨이에 대응하고 있어 중요한 전환기를 맞이하고 있습니다. 한편, 옥탈 및 xSPI 인터페이스는 총 출하 대수의 20% 미만을 차지할 뿐이지만, 눈부신 성장을 이루고 있습니다. 이러한 첨단 인터페이스는 최대 800 MB/s의 읽기 성능이 필요한 자동차용 이더넷 게이트웨이 및 엣지 AI 가속기에 대한 수요 증가에 힘입어 연평균 성장률(CAGR) 9.6%로 성장하고 있습니다.

인터페이스의 다양화는 공급업체의 로드맵을 수립하는 데 중요한 역할을 하고 있습니다. 대만의 설계 회사는 xSPI 인터페이스를 빠르게 도입하고, 자동차 업계 고객들과 수년에 걸친 계약을 체결함으로써 수익원의 안정화를 도모하고 있습니다. 기존 가전제품 및 백색가전 제조업체들은 여전히 SPI 싱글/듀얼 인터페이스에 의존하고 있습니다. 이러한 선택은 주로 컨트롤러의 핀 수를 최소화하고 비용 효율성을 확보해야 할 필요성에서 비롯된 것입니다. 그 결과, SPI 싱글/듀얼과 같은 성숙한 인터페이스는 고성능이 우선시되지 않는 용도에서의 유용성에 힘입어 장기적인 수익 기반을 유지하고 있습니다.

2025년 아시아태평양의 NOR 플래시 시장에서 64메가비트 이하 디바이스는 27.2%를 차지했습니다. 이는 다양한 용도에서 저비용 마이크로컨트롤러가 널리 사용되고 있기 때문입니다. 이러한 기기들은 합리적인 가격과 기존 시스템과의 호환성 덕분에 여전히 인기를 끌고 있습니다. 그러나 OLED 스마트폰, ADAS 컨트롤러, 엣지 AI 모듈 분야에서 대용량 펌웨어 저장 장치에 대한 수요가 증가함에 따라, 256메가비트를 초과하는 용량의 디바이스는 연평균 성장률(CAGR) 10.9%로 급속히 성장하고 있습니다. Macronix사의 1기가비트 ‘ArmorBoot’ 기술은 무선 업데이트(OTA)를 위한 격리된 보안 파티션을 지원하며, 플래그십 스마트폰에 0.5기가비트급 NOR 플래시의 채택을 촉진하고 있습니다. 이러한 추세는 첨단 용도 분야에서 대용량 NOR 플래시에 대한 수요가 증가하고 있음을 여실히 보여주고 있습니다.

128-256메가비트급 중밀도 제품은 비용과 용량의 균형이 잘 잡혀 있어, 자동차용 인포테인먼트 시스템이나 산업용 인간-기계 인터페이스(HMI)에 가장 적합합니다. 이러한 밀도는 비용을 크게 늘리지 않으면서도 적정한 저장 용량이 필요한 용도에 적합합니다. 2-8메가비트 제품은 최소한의 저장 공간만으로도 충분한 초저가 센서로 계속해서 사용되고 있습니다. 그러나 이러한 저용량 제품들은 현대의 용도에서 더 뛰어난 성능과 효율을 제공하는 시스템 온 칩(SoC)에 통합된 임베디드 플래시 솔루션에 의해 해마다 시장 점유율을 서서히 빼앗기고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the asia-Pacific NOR flash market size is expected to grow from USD 1.88 billion in 2025 to USD 1.99 billion in 2026 and is forecast to reach USD 2.65 billion by 2031 at a 5.9% CAGR over 2026-2031.

This report is Segmented by Type (Serial NOR Flash, and More), Interface (Quad SPI, and More), Density (2 Megabit and Less, and More), Voltage (3 V Class, and More), End-User Application (Consumer Electronics, and More), Process Technology Node (45 Nm, 55 Nm, and More), Packaging Type (WLCSP/CSP, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Asia-Pacific NOR Flash Market Trends and Insights

Booming ADAS and Infotainment Memory Demand in China-Japan Automotive Electronics

Automotive systems in China and Japan increasingly rely on redundant NOR arrays for safe-boot and fail-operational functions, pushing average vehicle content from 32 megabits in 2024 to a projected 128 Megabits by 2028. Japanese Tier-1 suppliers embed dual-channel NOR to achieve ISO 26262 ASIL-D compliance. Infineon's SEMPER devices qualified with Renesas R-CAR Gen4 in 2025, evidencing the two-to-three-year design-win horizon common in this market. ADAS alone already represents more than half of automotive NOR revenue in the region. With China delivering 27 million vehicles in 2025 and electrification rising, the segment anchors long-term demand.

Shift To Octal and HyperBus NOR Architectures Across Asia-Pacific Design Houses

Octal and xSPI interfaces delivered only 15-18% of 2025 volumes yet are scaling fast on the back of bandwidth needs above 400 MB/s in edge-AI and automotive gateway controllers. Infineon introduced an LPDDR-compatible NOR in March 2026, doubling read throughput to 800 MB/s and simplifying routing. GigaDevice's 1.2 V Octal parts serve battery-powered IoT nodes, cutting active current by up to 40%. As Taiwanese and Korean design houses migrate edge-AI accelerators to xSPI, suppliers secure multi-year, higher-margin contracts that offset consumer-electronic price pressure.

Export-Control Curbs on EUV and DUV Tools Into Mainland China

Expanded Foreign Direct Product Rule measures implemented in October 2024 bar advanced lithography shipments to Chinese memory fabs, limiting mainland processes to 40-nanometer and older for the foreseeable future. Automotive-grade NOR at 28 nanometers promises 30-40% power savings, so the restriction hampers mainland suppliers seeking vehicle design wins. Japan's alignment with U.S. policy cut access to Tokyo Electron etch systems, reinforcing the technology split: Taiwan and South Korea advance to 22 nanometers while China remains at mature nodes.

Other drivers and restraints analyzed in the detailed report include:

- Chip-Self-Sufficiency Incentives in China and India

- OLED-Centric Smartphone Designs Pushing High-Density Serial NOR

- 12-Inch Foundry Tightness in Taiwan Driving Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR retained 71.8% of the Asia-Pacific NOR Flash market share in 2025, as SPI and Quad SPI interfaces satisfy most consumer and IoT boot-code needs. Parallel NOR, although only 28.2% of revenue, benefits from a 7.3% CAGR driven by deterministic-latency requirements in industrial control and safety-critical automotive modules. Parallel devices remain embedded in airbags and ABS, where sub-50 ns access cannot be compromised.

In response, serial suppliers add hardware root-of-trust and redundancy to challenge parallel incumbents, foreshadowing tighter competition in the next platform refresh. Serial architectures are also creeping upward in density and reliability. Macronix's ArmorBoot MX76 brings 1 Gigabit secure-boot capability, showing that execute-in-place and security, once exclusive to parallel NOR, can migrate to serial designs. Suppliers that fail to offer these enhancements risk confinement to cost-sensitive consumer devices, where price wars with Chinese entrants squeeze margins.

SPI Single/Dual dominated the market with a 47.6% share in 2025. However, its bandwidth ceilings, capped at approximately 80 MB/s, restrict its application in data-intensive systems. Despite this limitation, it remains a preferred choice for cost-sensitive applications where high-speed performance is not critical. Quad SPI, holding around 35% of the market share, is at a pivotal stage, catering to mid-range smartphones and industrial gateways that require faster firmware updates. Meanwhile, Octal and xSPI interfaces, though accounting for less than 20% of total units, are experiencing significant growth. These advanced interfaces are growing at a 9.6% CAGR, driven by increasing demand for automotive Ethernet gateways and edge-AI accelerators that require read performance of up to 800 MB/s.

Interface fragmentation is playing a critical role in shaping supplier roadmaps. Taiwanese design houses are quickly adopting xSPI interfaces and securing multiyear commitments from automotive clients, helping stabilize their revenue streams. Manufacturers of legacy appliances and white goods continue to rely on SPI Single/Dual interfaces. This choice is primarily driven by the need to minimize controller pin counts and ensure cost efficiency. As a result, mature interfaces like SPI Single/Dual maintain a long revenue tail, supported by their relevance in applications where advanced performance is not a priority.

Devices at 64 megabits or below accounted for 27.2% of the Asia-Pacific NOR Flash market in 2025, driven by the widespread use of low-cost microcontrollers across various applications. These devices remain popular due to their affordability and compatibility with legacy systems. However, densities above 256 megabits are growing rapidly, with a CAGR of 10.9%, as OLED smartphones, ADAS controllers, and edge-AI modules increasingly require larger firmware storage. Macronix's 1 Gigabit ArmorBoot technology supports isolated secure partitions for over-the-air updates, encouraging flagship smartphones to adopt half-gigabit NOR footprints. This trend highlights the growing demand for higher-density NOR Flash in advanced applications.

Mid-tier densities, ranging from 128 to 256 megabits, strike a balance between cost and capacity, making them ideal for automotive infotainment systems and industrial human-machine interfaces (HMIs). These densities cater to applications that require moderate storage without significantly increasing costs. 2-8 Megabit parts continue to find use in ultra-low-cost sensors, where minimal storage is sufficient. However, these lower-density parts are gradually losing market share each year to embedded flash solutions integrated within system-on-chips, which offer better performance and efficiency for modern applications.

Complete Report Scope:

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less NOR

- 4 Megabit and Less (greater than 2 MB) NOR

- 8 Megabit and Less (greater than 4 MB) NOR

- 16 Megabit and Less (greater than 8 MB) NOR

- 32 Megabit and Less (greater than 16 MB) NOR

- 64 Megabit and Less (greater than 32 MB) NOR

- 128 Megabit and Less (greater than 64 MB) NOR

- 256 Megabit and Less (greater than 128 MB) NOR

- Greater than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Others - 1.2 V Class (and similar sub-1.8 V: 2.5 V, 5 V)

- By End-User Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-User Applications

- By Process Technology Node (Value)

- 90 nm and Older

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Geography

- China

- Japan

- South Korea

- Taiwan

- India

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Winbond Electronics Corp.

- GigaDevice Semiconductor Inc.

- Macronix International Co., Ltd.

- Micron Technology Inc.

- Infineon Technologies AG

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Elite Semiconductor Memory Tech (ESMT)

- Puya Semiconductor (Shanghai) Co.

- Wuhan XMC

- Integrated Silicon Solution Inc. (ISSI)

- Samsung Electronics Co. Ltd.

- STMicroelectronics NV

- Alliance Memory, Inc.

- SK hynix Inc.

- AMIC Technology Corp.

- NXP Semiconductors N.V.

- Powerchip Semiconductor Manufacturing Corp.

- Adesto Technologies (renesas)

- BOYA Microelectronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming ADAS and Infotainment Memory Demand in China-Japan Automotive Electronics

- 4.2.2 OLED-Centric Smartphone Designs Pushing High-Density Serial NOR in China and Korea

- 4.2.3 Chip-Self-Sufficiency Incentives (China, India PLI) Accelerate Regional NOR Fabs

- 4.2.4 IoT Manufacturing Clusters in ASEAN Requiring Low-Power Code Storage

- 4.2.5 Industry 4.0 Upgrades in Taiwan and South Korea Industrial Automation

- 4.2.6 Shift to Octal/HyperBus NOR Architectures Across Asia-Pacific Design Houses

- 4.3 Market Restraints

- 4.3.1 Low-Cost NAND and ReRAM Cannibalization in Shenzhen Design Wins

- 4.3.2 12-Inch Foundry Tightness in Taiwan Driving Price Volatility

- 4.3.3 Escalating 28 nm and 22 nm NOR R&D Capex vs. Mainstream Logic Lines

- 4.3.4 Export-Control Curbs on EUV / DUV Tools into Mainland China

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less NOR

- 5.3.2 4 Megabit and Less (greater than 2 MB) NOR

- 5.3.3 8 Megabit and Less (greater than 4 MB) NOR

- 5.3.4 16 Megabit and Less (greater than 8 MB) NOR

- 5.3.5 32 Megabit and Less (greater than 16 MB) NOR

- 5.3.6 64 Megabit and Less (greater than 32 MB) NOR

- 5.3.7 128 Megabit and Less (greater than 64 MB) NOR

- 5.3.8 256 Megabit and Less (greater than 128 MB) NOR

- 5.3.9 Greater than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Others - 1.2 V Class (and similar sub-1.8 V: 2.5 V, 5 V)

- 5.5 By End-User Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other End-User Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Older

- 5.6.2 65 nm

- 5.6.3 55 nm (including 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

- 5.8 By Geography

- 5.8.1 China

- 5.8.2 Japan

- 5.8.3 South Korea

- 5.8.4 Taiwan

- 5.8.5 India

- 5.8.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Winbond Electronics Corp.

- 6.4.2 GigaDevice Semiconductor Inc.

- 6.4.3 Macronix International Co., Ltd.

- 6.4.4 Micron Technology Inc.

- 6.4.5 Infineon Technologies AG

- 6.4.6 Renesas Electronics Corp.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Elite Semiconductor Memory Tech (ESMT)

- 6.4.9 Puya Semiconductor (Shanghai) Co.

- 6.4.10 Wuhan XMC

- 6.4.11 Integrated Silicon Solution Inc. (ISSI)

- 6.4.12 Samsung Electronics Co. Ltd.

- 6.4.13 STMicroelectronics NV

- 6.4.14 Alliance Memory, Inc.

- 6.4.15 SK hynix Inc.

- 6.4.16 AMIC Technology Corp.

- 6.4.17 NXP Semiconductors N.V.

- 6.4.18 Powerchip Semiconductor Manufacturing Corp.

- 6.4.19 Adesto Technologies (renesas)

- 6.4.20 BOYA Microelectronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis