|

시장보고서

상품코드

2072555

유럽의 NOR 플래시 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

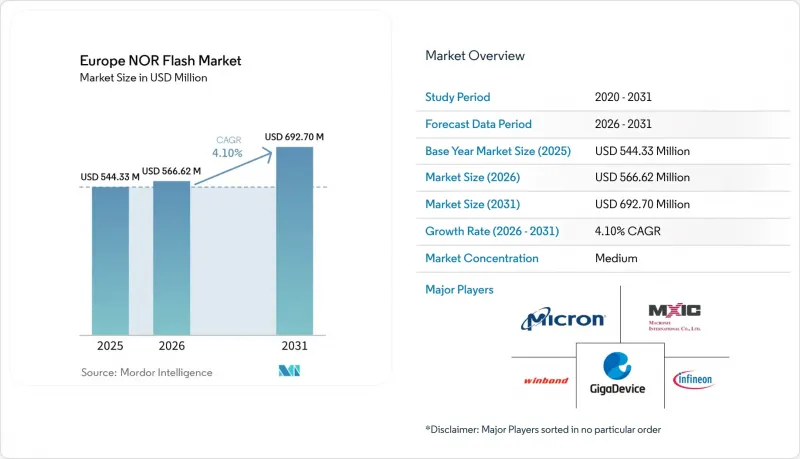

Mordor Intelligence에 의하면, 유럽의 NOR 플래시 시장 규모는 2025년 5억 4,433만 달러로 평가되었습니다. 2026년 5억 6,662만 달러에서 2031년까지 6억 9,270만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 4.10%를 나타낼 전망입니다.

본 보고서는 NOR 플래시의 유형(직렬, 병렬), 인터페이스(SPI, 쿼드 SPI 등), 용량(2메가비트 이하, 그 이상), 전압(3V급, 그 이상), 최종 사용자용도(소비자용 전자기기 등), 공정 기술 노드(55/58 nm, 65 nm, 45 nm 등), 패키지 유형(WLCSP/CSP 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(단위)으로 제시되어 있습니다.

유럽의 NOR 플래시 시장 동향 및 분석

유럽 전기차 시장의 OTA 펌웨어 업데이트로의 전환이 고밀도 SPI NOR 수요를 끌어올리고 있습니다.

유엔 규정 제156호에 따라, 2024년 7월 이후 유럽연합(EU)에서 판매되는 모든 신차에 소프트웨어 업데이트 관리 시스템의 탑재가 의무화됨에 따라, 1차 공급업체들은 한 뱅크를 업데이트하는 동안에도 다른 뱅크에서 실행 중인 코드를 유지할 수 있는 듀얼 뱅크 NOR 설계로 전환해야 하는 상황에 직면해 있습니다. 이러한 요건으로 인해 롤백 이미지를 항상 사용할 수 있는 상태로 유지해야 하므로, ECU 1대당 플래시 메모리의 최소 할당 용량이 증가하게 되었고, 그 결과 유럽의 NOR 플래시 메모리 시장에서 고밀도 제품에 대한 수요가 직접적으로 증가하고 있습니다. 또한, 보안 기능이 통합된 OTA 지원 NOR는 일반적인 코드 저장 장치보다 높은 가격에 판매되므로, 자동차용 등급 부품에 대해 더 유리한 가격 책정이 가능해집니다. 인피니온의 ‘SEMPER X1’은 고속 액세스와 실시간 실행이 중요한 차세대 자동차용 전자 및 전기 아키텍처를 대상으로 한 LPDDR 플래시 제품으로 출시되었습니다. 유럽의 프리미엄 OEM 업체들이 소프트웨어 정의 차량 플랫폼의 표준화를 지속하는 가운데, 이러한 변화로 인해 예측 기간 동안 고밀도 SPI NOR는 유리한 입지를 유지하게 될 것입니다.

자동차 제조업체가 의무화한 플래시 메모리의 품질 목표가 독일 및 북유럽 국가들에서의 채택을 촉진하고 있습니다.

독일의 Tier 1 공급업체와 북유럽의 자동차용 전자기기 제조업체들은 ASIL-D 기능 안전성을 새로운 ADAS 및 게이트웨이 ECU 프로그램의 실질적인 진입 요건으로 계속해서 간주하고 있으며, 이로 인해 유럽의 NOR 플래시 메모리 시장에서 인증 기준이 높아지고 있습니다. GigaDevice사의 자동차용 SPI NOR 제품군 ‘GD25/55’는 2024년 12월에 ISO 26262 ASIL-D 인증을 획득함으로써, 기존에는 평판이 좋은 공급업체로만 제한되었던 인증 활동에 참여할 수 있게 되었습니다. 또한, Macronix사는 2025년 1월, MXSMIO 제품군의 OctaFlash 및 Quad SPI 두 가지 모델 모두에서 ASIL-D 준수 범위를 확대하여 자동차용 등급의 선택지를 다양화했습니다. 새로운 공급업체가 ASIL-D 대응 준비를 갖추게 됨에 따라, 기존 공급업체가 설계 수주를 유지하고 있는 경우에도 조달 팀은 소켓 가격에 대한 협상력을 높일 수 있습니다. AEC-Q100 등급 1의 열 및 신뢰성 선별 검사는 또 하나의 장벽이 되어, 고성능 자동차용 소켓을 역량이 부족한 신규 진입 업체로부터 보호하는 데 일조합니다.

28nm 플로팅 게이트 노드에서 팹 수준의 수율 저하로 인해 ASP의 변동성이 커지고 있습니다.

28nm 공정에서의 첨단 플로팅 게이트 집적 기술은 여전히 전하 손실 및 셀 커플링이라는 과제에 직면해 있으며, 이로 인해 고밀도 NOR 제품에서 지우기 임계값이 확대되고 유효 출력이 저하될 가능성이 있습니다. 수율 기준이 엄격해지면, 공급업체는 대개 프리미엄 자동차용 등급을 최우선으로 하기 때문에 산업용 및 통신 분야 고객은 조달 및 가격 책정 측면에서 유연성을 잃게 됩니다. 유럽의 NOR 플래시 메모리 시장에서 이러한 추세는 중요한 의미를 지닙니다. 왜냐하면 독일이나 프랑스의 자동차 업계 바이어들은 이미 쉬운 대체를 제한하는 엄격한 인증 규정에 따라 사업을 운영하고 있기 때문입니다. AEC-Q100 및 JEDEC의 신뢰성 선별 과정을 통해 추가적인 선별 공정이 더해지기 때문에 기준이 되는 웨이퍼의 생산량은 그대로 판매 가능한 자동차용 다이와 직접적으로 연결되지 않습니다. 그 결과, 첨단 특수 노드에서 인증을 받은 NOR을 필요로 하는 구매자의 경우, 가격 변동이 심해지고 계획 주기가 길어지는 경향이 있습니다.

부문별 분석

2025년, 직렬 NOR 플래시는 유럽의 NOR 플래시 시장 점유율의 66.1%를 차지했으며, 이는 병렬 장치에서 사용되는 폭이 넓은 버스 구조로부터의 오랜 기간에 걸친 전환을 반영한 것입니다. 직렬형 제품은 핀 수를 줄이고 PCB 배선의 복잡성을 완화하며, 소형 자동차용 ECU나 산업용 컨트롤러에 쉽게 탑재할 수 있기 때문에 이 부문은 그 우위를 유지했습니다. 많은 신규 프로젝트에서 기판 면적, 전원 배선, 패키지 통합이 설계상의 우선순위로 점점 더 엄격해지고 있기 때문에 이러한 시스템 수준의 이점은 부품 비용과 마찬가지로 중요하게 여겨지고 있습니다. 따라서 유럽의 NOR 플래시 시장에서는 주류인 MCU 기반 시스템뿐만 아니라, 큰 물리적 실적 없이도 뛰어난 대역폭이 필요한 새로운 컨트롤러 설계에서도 시리얼 부품이 선호되고 있습니다. 윈본드의 옥탈 NOR 제품군은 직렬 아키텍처가 얼마나 발전했는지를 보여주고 있으며, 이 회사는 xSPI 지원 제품에서 최대 400 MB/s의 연속 읽기 처리량을 달성하고 있음을 강조하고 있습니다.

병렬 NOR 플래시는 특정 항공 전자 장비, 국방 통신 및 수명이 긴 산업용 PLC 프로그램 분야에서 여전히 그 가치를 인정받고 있습니다. 이러한 분야에서는 핀 효율보다 기존의 타이밍 특성이나 재설계 위험이 더 중요하게 여겨지기 때문입니다. 이러한 용도는 제한적이지만, 관련 프로그램의 고객들은 아키텍처 변경보다 플랫폼의 지속성을 우선시하는 경우가 많기 때문에 상업적으로는 여전히 중요한 위치를 차지하고 있습니다. ISO 26262와 같은 기능 안전 규격은 두 제품 유형 모두에 적용되지만, 시리얼 NOR는 활발한 공급업체들의 최근 인증 투자와 제품 출시 확대의 혜택을 받고 있습니다. 이러한 광범위한 생태계가 중요한 이유는 자동차 및 산업용 시스템의 조달 팀이 더욱 강력한 도구 지원, 폭넓은 인터페이스 호환성, 그리고 장기적인 로드맵을 갖춘 부품을 점점 더 선호하고 있기 때문입니다. 그 결과, 유럽의 NOR 플래시 메모리 시장은 신규 설계 분야에서 시리얼 솔루션을 중심으로 통합이 진행되는 한편, 병렬 NOR는 특수한 도입 환경에서 유지보수 및 연속성 확보의 역할을 더 많이 담당하고 있습니다.

2025년, 쿼드 SPI는 유럽의 NOR 플래시 시장의 49.7%를 차지했으며, 현재의 MCU 및 SoC 생태계에 깊이 뿌리내리고 있음을 입증하고 있습니다. 이러한 우위는 성숙한 운전자 지원 기능, 폭넓은 칩셋 호환성, 그리고 자동차 및 산업용 시스템 분야에서 다년간 쌓아온 인증 실적에서 비롯됩니다. 재설계 비용이 높고 코드 이전 예산이 제한적인 상황에서 많은 OEM 업체들이 인터페이스의 연속성을 중시하기 때문에 이러한 도입 기반은 여전히 중요한 의미를 지닙니다. 인피니언의 SEMPER NOR 제품군은 급격한 인터페이스 변경보다 검증된 동작을 우선시하는 자동차 및 산업용 플랫폼에서 이러한 주류 임베디드 요구 사항을 지속적으로 지원하고 있습니다. 유럽의 NOR 플래시 시장 대부분에서 대역폭 요구 사항이 현재 인플레이스 실행의 제한 범위 내에 머무르는 한, 쿼드 SPI는 여전히 기본 선택지로 남아 있습니다.

그러나 도메인 컨트롤러, AI 지원 엣지 노드, 첨단 통신 하드웨어가 기존의 Quad SPI 처리량 상한선을 넘어서는 추세에 따라, 균형은 더욱 고성능인 시스템 쪽으로 이동하고 있습니다. 따라서 Octal 및 xSPI는 가장 빠르게 성장하고 있는 인터페이스 부문으로, 시장 전망에 따르면 2031년까지 연평균 성장률(CAGR) 5.9%를 나타낼 것으로 예측됩니다. Macronix는 2025년 3월, 자사의 OctaFlash 제품이 STMicroelectronics의 STM32N6 플랫폼에 채택되어 200 MHz DDR 모드에서 400 MB/s의 처리량을 지원할 수 있다고 발표하며, 이러한 방향성을 제시했습니다. 또한, JEDEC에 의한 xSPI 표준화로 인해 공급업체에 대한 종속성에 대한 우려도 완화되어, 차세대 보드 계획을 추진 중인 각 OEM 업체들에게 옥탈로의 전환이 용이해졌습니다. 그 결과, 유럽의 NOR 플래시 메모리 시장에서는 Quad SPI가 광범위한 도입 기반을 유지하는 한편, Octal 및 xSPI가 고대역폭 용도 분야에서 점유율을 확대하고 있는 시장 구도를 보이고 있습니다.

32-64메가비트 이상의 NOR 부문은 2025년 유럽의 NOR 플래시 메모리 시장에서 25.6%를 차지하며, 매출 기준 최대 용량 구간이 되었습니다. 이는 대용량 대역과 같은 비용 증가를 수반하지 않으면서도 펌웨어 저장이 필요한 단일 ECU 자동차용 전자기기, 산업용 센서 퓨전 노드 및 통신용 고객 가정용 장비의 요구를 반영한 것입니다. 많은 임베디드 프로그램이 여전히 이 범위에 속하기 때문에 이 부문은 견조한 성장세를 유지하고 있습니다. 256메가비트 이하(128MB 초과)의 NOR 부문은 시스템의 복잡성 증가를 배경으로 2031년까지 연평균 성장률(CAGR) 6.1%를 기록하며 성장할 것으로 전망됩니다. 유럽에서는 이러한 변화가 존(zone) 및 도메인 컨트롤러 설계의 보급과 맞물려, 기존에는 소형 ECU에 분산되어 있던 코드베이스가 통합되고 있습니다.

4-8메가비트 초과, 2-4메가비트 초과 및 2메가비트 이하의 저용량 NOR 부문은 구형 산업용 컨트롤러나 간단한 센서 플랫폼에서 안정적인 도입 기반을 유지하고 있습니다. 고객들이 성능 향상보다 설계의 연속성을 우선시하고 있기 때문에 수요는 견조한 추세를 보이고 있습니다. GigaDevice가 2026년 3월에 초저전력 SPI NOR 시리즈 ‘GD25UF’의 용량을 8 Mb에서 256 Mb로 확장한 사례에서 볼 수 있듯이, 공급업체들의 로드맵은 새로운 저전력 용도에 맞추어 더 큰 용량으로 확대되고 있습니다. 이는 NOR 플래시의 특성을 유지하면서, 더 대용량이면서도 저전력인 스토리지가 필요한 AI 컴퓨팅 플랫폼, 의료용 웨어러블 기기, 엣지 AI 시스템을 지원하는 제품입니다. 유럽의 NOR 플래시 메모리 시장은 여전히 중용량 부문이 주를 이루고 있지만, 소프트웨어의 복잡성이 증가함에 따라 중·상위 용량 부문의 성장이 가속화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the europe NOR flash market size is projected to expand from USD 544.33 million in 2025 and USD 566.62 million in 2026 to USD 692.70 million by 2031, registering a CAGR of 4.10% between 2026 to 2031.

This report is Segmented by NOR Flash Type (Serial, and Parallel), Interface (SPI, Quad SPI, and More), Density (2 Megabit and Less, and More), Voltage (3V Class, and More), End-User Application (Consumer Electronics, and More), Process Technology Node (55/58 Nm, 65 Nm, 45 Nm, and More), and Packaging Type (WLCSP/CSP, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Europe NOR Flash Market Trends and Insights

Shift To OTA Firmware Updates In European EVs Boosting High-Density SPI NOR Demand

UN Regulation No. 156 made a software update management system mandatory for all new vehicles sold in the European Union from July 2024, pushing Tier-1 suppliers toward dual-bank NOR designs that can update one bank while the other keeps the live code running. That requirement increases the minimum flash allocation per ECU because rollback images must remain available, thereby directly increasing density demand in the European NOR Flash Memory market. It also supports better pricing for automotive-grade parts because OTA-ready NOR with integrated security features sells at a premium to standard code-storage devices. Infineon's SEMPER X1 was introduced as an LPDDR Flash product aimed at next-generation automotive electronic and electrical architectures where fast access and real-time execution matter. As European premium OEMs continue to standardize software-defined vehicle platforms, this shift keeps high-density SPI NOR in a favorable position across the forecast period.

Automotive OEM-Mandated Flash Quality Targets Driving Design-Ins In Germany And Nordics

German Tier-1 suppliers and Nordic automotive electronics manufacturers continue to treat ASIL-D functional safety as a practical entry requirement for new ADAS and gateway ECU programs, which raises the qualification bar in the Europe NOR Flash Memory market. GigaDevice's GD25/55 automotive-grade SPI NOR family received ISO 26262 ASIL D certification in December 2024, opening access to qualification activities previously reserved for more established suppliers. Macronix also expanded its automotive-grade options in January 2025 by extending ASIL D compliance across both OctaFlash and Quad SPI variants in its MXSMIO family. Once an additional supplier reaches ASIL-D readiness, procurement teams gain greater negotiating power over socket pricing, even when incumbent vendors retain the design win. AEC-Q100 Grade 1 thermal and reliability screening adds another barrier, helping protect premium automotive sockets from low-capability entrants.

Fab-Level Yield Losses On 28 Nm Floating-Gate Nodes Elevating ASP Volatility

Advanced floating-gate integration at 28 nm continues to face charge-loss and cell-coupling challenges, which can widen erase thresholds and reduce effective output in higher-density NOR products. When yield tightens, suppliers usually prioritize premium automotive grades first, leaving industrial and communications customers with less procurement and pricing flexibility. In the Europe NOR Flash Memory market, that pattern matters because automotive buyers in Germany and France already operate under strict qualification rules that limit easy substitution. AEC-Q100 and JEDEC reliability screening add additional filtering steps, meaning baseline wafer volumes do not directly translate into saleable automotive die. The practical result is more volatile pricing and longer planning cycles for buyers who need qualified NOR at advanced specialty nodes.

Other drivers and restraints analyzed in the detailed report include:

- EU Data-Centric Edge-AI Roll-Outs Elevating Serial NOR Adoption In Industrial PLCs

- EU Chips Act Funding For 28 Nm And 45 Nm NOR Lines In Dresden

- Rising 1.8 V NAND Substitutes Below 256 Mb In Consumer IoT Nodes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR Flash held 66.1% of the Europe NOR Flash market share in 2025, which reflected a long-running shift away from the wider bus structure used in parallel devices. The segment kept that lead because serial parts reduce pin count, lower PCB routing complexity, and fit more easily into compact automotive ECUs and industrial controllers. In many new programs, those system-level benefits matter as much as component cost because board area, power routing, and package integration are becoming stricter design priorities. The European NOR Flash market has therefore favored serial parts not only for mainstream MCU-based systems, but also for newer controller designs that need better bandwidth without a large physical footprint. Winbond's Octal NOR portfolio shows how far serial architectures have advanced, with the company highlighting continuous read throughput up to 400 MB/s on xSPI-enabled products.

Parallel NOR Flash still has value in selected avionics, defense communications, and long-life industrial PLC programs, where legacy timing behavior and redesign risk are more important than pin efficiency. Those uses are narrower, but they remain commercially relevant because customers in such programs often prefer platform continuity over architectural change. Functional safety rules such as ISO 26262 apply across both product types, yet serial NOR has benefited from a wider flow of recent certification investments and product launches from active suppliers. That wider ecosystem matters because procurement teams in automotive and industrial systems increasingly favor parts with stronger tool support, broader interface compatibility, and longer forward roadmaps. As a result, the European NOR Flash Memory market continues to consolidate around serial solutions for new designs, while parallel NOR serves more of a maintenance and continuity role in specialized deployments.

Quad SPI accounted for 49.7% of the Europe NOR Flash market in 2025, underscoring its deep embeddedness in current MCU and SoC ecosystems. Its lead comes from mature driver support, broad chipset compatibility, and a long history of qualification across automotive and industrial systems. That installed base still matters because many OEMs prefer interface continuity when redesign costs are high, and code migration budgets are tight. Infineon's SEMPER NOR product range continues to support these mainstream embedded requirements across automotive and industrial platforms that prioritize validated operation over aggressive interface change. For much of the European NOR Flash market, Quad SPI remains the default choice when bandwidth demands stay within current execute-in-place limits.

The balance is shifting toward higher-performance systems because domain controllers, AI-enabled edge nodes, and advanced communications hardware are pushing beyond traditional Quad SPI throughput ceilings. Octal and xSPI therefore represent the fastest-growing interface class, with the market forecast indicating 5.9% CAGR through 2031. Macronix demonstrated this direction in March 2025, when it said its OctaFlash products were selected for STMicroelectronics' STM32N6 platform and could support 200 MHz DDR mode for 400 MB/s throughput. JEDEC xSPI standardization also reduces supplier lock-in concerns, making Octal migration easier for OEMs planning the next board generation. The result is a market mix where Quad SPI maintains its broad installed base, while Octal and xSPI capture a rising share of higher-bandwidth applications in the European NOR Flash Memory market.

The more than 32 to 64 megabit NOR segment accounted for 25.6% of the Europe NOR Flash Memory market in 2025, making it the largest density tier by revenue. It reflects the needs of single-ECU automotive electronics, industrial sensor-fusion nodes, and telecom customer-premises equipment that require firmware storage without the higher cost of density bands. This segment remains durable as many embedded programs still fit within this range. The 256 Megabit and Less (greater than 128MB) NOR tier is forecast to grow at a 6.1% CAGR through 2031, driven by rising system complexity. In Europe, this shift aligns with zonal and domain-controller designs, consolidating code bases previously spread across smaller ECUs.

Smaller-density segments, more than 4 to 8 megabit, more than 2 to 4 megabit, and 2 megabit and less NOR, retain a stable installed base in legacy industrial controllers and simple sensor platforms. Demand remains steady as customers prioritize design continuity over performance upgrades. Supplier roadmaps are extending upward for new low-power applications, as seen in GigaDevice's March 2026 expansion of its GD25UF ultra-low-power SPI NOR series from 8 Mb to 256 Mb. This supports AI computing platforms, medical wearables, and edge-AI systems needing larger low-power storage while retaining NOR flash characteristics. The European NOR Flash Memory market remains anchored in mid-range densities, with growth accelerating in upper-middle tiers due to increasing software complexity.

Complete Report Scope:

- By Type (Value and Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V-3.6 V)

- Others - 1.2 V Class (Sub-1.8 V, 2.5 V, 5 V)

- By End-User Application (Value and Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-User Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (Including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Country

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

List of Companies Covered in this Report:

- Infineon Technologies AG

- Micron Technology Inc.

- Winbond Electronics Corp.

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution Inc.

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Elite Semiconductor Microelectronics Tech. Inc.

- Samsung Electronics Co. Ltd.

- SK hynix Inc.

- SMIC NOR Foundry Services

- Tower Semiconductor

- ISSI Automotive Grade NOR (China)

- Macron Flash Ltd.

- Cypress Semiconductor Corp.

- Alliance Memory Inc.

- Puya Semiconductor (Shanghai) Co. Ltd.

- Hua Hong Semiconductor Ltd.

- EON Silicon Solution Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive OEM-Mandated Flash Quality Targets Driving Design-Ins in Germany and Nordics

- 4.2.2 EU Data-Centric Edge-AI Roll-Outs Elevating Serial NOR Adoption in Industrial PLCs

- 4.2.3 Shift to OTA Firmware Updates in European EVs Boosting High-Density SPI NOR Demand

- 4.2.4 Telecom Open-RAN Deployments in UK and France Requiring Low-Latency Boot Code Storage

- 4.2.5 Medical-Grade Wearables Regulation (MDR) Accelerating Secure NOR Integration

- 4.2.6 EU Chips Act Funding for 28 nm and 45 nm NOR Lines (e.g., Dresden)

- 4.3 Market Restraints

- 4.3.1 Rising 1.8 V NAND Substitutes Below 256 Mb in Consumer IoT Nodes

- 4.3.2 Fab-Level Yield Losses on 28 nm Floating-Gate Nodes Elevating ASP Volatility

- 4.3.3 Tight Allocation of Specialty Photomasks in Europe Hindering Parallel NOR Expansion

- 4.3.4 Post-Brexit Customs Delays Impacting Lead-Times for UK Automotive Tier-1s

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type (Value and Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 More than 2 to 4 Megabit

- 5.3.3 More than 4 to 8 Megabit

- 5.3.4 More than 8 to 16 Megabit

- 5.3.5 More than 16 to 32 Megabit

- 5.3.6 More than 32 to 64 Megabit

- 5.3.7 More than 64 to 128 Megabit

- 5.3.8 More than 128 to 256 Megabit

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V-3.6 V)

- 5.4.4 Others - 1.2 V Class (Sub-1.8 V, 2.5 V, 5 V)

- 5.5 By End-User Application (Value and Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other End-User Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and More

- 5.6.2 65 nm

- 5.6.3 55 nm (Including 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

- 5.8 By Country

- 5.8.1 Germany

- 5.8.2 United Kingdom

- 5.8.3 France

- 5.8.4 Italy

- 5.8.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Micron Technology Inc.

- 6.4.3 Winbond Electronics Corp.

- 6.4.4 Macronix International Co. Ltd.

- 6.4.5 GigaDevice Semiconductor Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Renesas Electronics Corp.

- 6.4.8 Microchip Technology Inc.

- 6.4.9 Elite Semiconductor Microelectronics Tech. Inc.

- 6.4.10 Samsung Electronics Co. Ltd.

- 6.4.11 SK hynix Inc.

- 6.4.12 SMIC NOR Foundry Services

- 6.4.13 Tower Semiconductor

- 6.4.14 ISSI Automotive Grade NOR (China)

- 6.4.15 Macron Flash Ltd.

- 6.4.16 Cypress Semiconductor Corp.

- 6.4.17 Alliance Memory Inc.

- 6.4.18 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.19 Hua Hong Semiconductor Ltd.

- 6.4.20 EON Silicon Solution Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis