|

시장보고서

상품코드

2072560

영국의 NOR 플래시 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United Kingdom NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

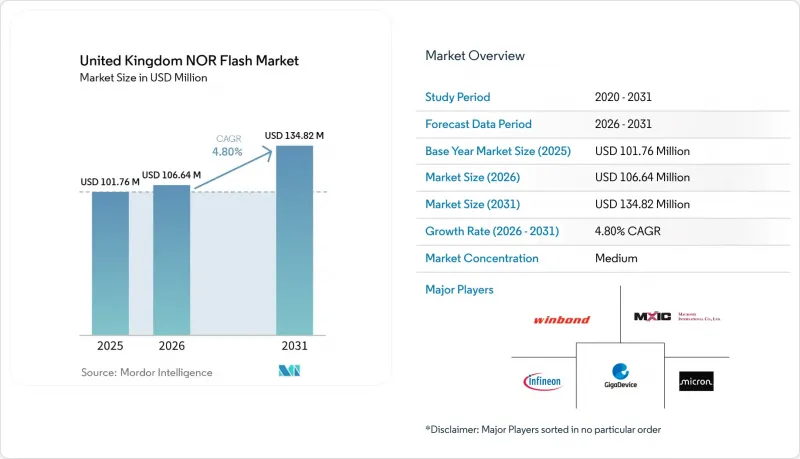

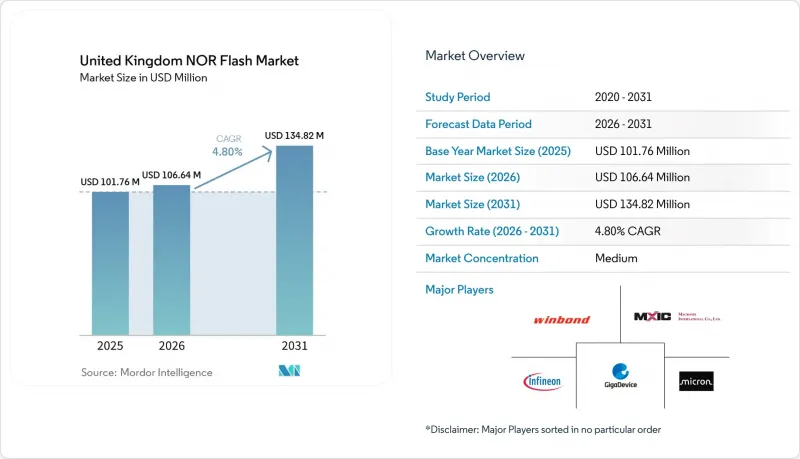

Mordor Intelligence에 의하면, 영국의 NOR 플래시 시장 규모는 2026년 1억 664만 달러에서 2031년까지 1억 3,482만 달러로 확대되며 2026-2031년에 걸쳐 CAGR 4.8%를 나타낼 것으로 예측되고 있습니다.

본 보고서는 유형(직렬 NOR 플래시, 기타), 인터페이스(쿼드 SPI, 기타), 밀도(2메가비트 이하, 기타), 전압(3V급, 와이드 전압, 기타), 최종 사용자용도(통신, 기타), 공정 기술 노드(45nm, 65nm, 기타), 패키징 유형(QFN/SOIC, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러)과 수량(개)으로 제시되어 있습니다.

영국의 NOR 플래시 시장 동향 및 분석

영국 OEM 업체들의 ADAS 및 전기차 플랫폼 채택 확대에 따라 인스턴트 부팅이 필요해지고 있습니다.

현재의 자동차 설계에서는 존 컨트롤러, 디지털 계기판, 인플레이스 메모리에서 안전상 중요한 코드를 실행하는 ADAS 스택이 채택되고 있습니다. 인피니언(Infineon)의 ASIL-D 인증을 획득한 SEMPER 시리즈와 윈본드(Winbond)의 W35T 옥탈 제품군이 대표적인 인증 디바이스로, -40°C-+125°C의 온도 범위 내에서 400 MB/s의 읽기 대역폭을 실현하고 있습니다. 재규어·랜드로버가 2026년 중반 플래시 메모리 부품 부족으로 생산을 중단한 사건은 공급망의 취약성을 여실히 드러냈으며, 각 OEM 업체들로 하여금 이중 조달 및 완충 재고 확충을 서두르게 했습니다. 존 기반 EV 플랫폼에는 10-15개의 NOR 소켓을 탑재할 수 있으며, 이는 기존 방식의 3배 이상에 해당합니다. 이로 인해 자동차 부문은 영국의 NOR 플래시 시장에서 가장 큰 성장 동력이 되고 있습니다.

5G 인프라 구축에 따라 통신 기기용 고신뢰성 코드 스토리지 수요가 가속화되고 있습니다.

버진 미디어 O2가 에릭슨 및 노키아와 체결한 7억 파운드(8억 8,900만 달러) 규모의 업그레이드 예산과, 보다폰 및 쓰리가 SA 지역의 99% 커버리지 달성 공약을 바탕으로 향후 수년에 걸친 기지국 확장 계획이 수립되고 있습니다. 각 무선 유닛에는 혹독한 실외 환경에서의 작동 주기를 견딜 수 있는 부트 코드와 패치 저장을 위해 64-256 Mb의 NOR가 내장되어 있습니다. 약 6,200건의 타워 건설 허가 신청이 규제 절차 지연으로 인해 보류 중이어서 설치가 늦어지고 있지만, 조달 계획의 가시성은 높아지고 있어 영국의 NOR 플래시 시장에 서비스를 제공하는 코드 스토리지 공급업체들에게는 호재가 되고 있습니다.

국내 웨이퍼 팹 생산 능력 부족이 공급망의 취약성을 초래하고 있습니다.

영국에서는 약 25개의 팹이 180nm를 초과하는 공정 기술로 가동을 계속하고 있으며, 구매자들은 모든 첨단 NOR 부품을 수입에 의존할 수밖에 없는 상황입니다. 첨단 NOR 플래시 부품의 국내 생산 능력 부족으로 인해 외부 공급업체에 대한 의존도가 현저히 높아지고 있습니다. 해외에서의 병목 현상이 상황을 더욱 악화시키고 있어, 2026년에는 자동차용 등급 부품의 리드타임이 24주에 달할 것으로 전망됩니다. 이 때문에 OEM 각사는 공급망 혼란을 완화하기 위해 4개월 분량의 안전 재고를 확보할 수밖에 없는 상황입니다. 한편, 뉴포트에서 진행 중인 2억 5,000만 파운드(3억 2,000만 달러) 규모의 설비 현대화 사업은 메모리 생산이 아닌 SiC 파워 반도체에 중점을 두고 있습니다. 그 결과, 영국의 NOR 플래시 시장은 구조적으로 외부 충격에 노출된 상태를 유지하고 있습니다.

부문별 분석

2025년, 시리얼 디바이스는 영국의 NOR 플래시 시장에서 71.8%라는 압도적인 점유율을 차지했습니다. 이러한 우위는 퍼스트 바이트 지연 시간을 유지하면서 PCB 면적을 대폭 줄인 쿼드 및 옥탈 버스의 효율성에서 비롯됩니다. 병렬 NOR는 10 ns 이하의 결정적인 액세스 시간 덕분에 항공 전자 장비 및 방위 분야에서 계속해서 중요한 역할을 수행하고 있습니다. 그러나 시리얼 대역폭이 400MB/s에 달하면서 경쟁 대체 수단으로 부상함에 따라, 해당 제품 시장 점유율은 하락할 것으로 예측됩니다. 또한, 패키징 기술의 발전, 특히 WLCSP로의 전환에 힘입어 시리얼 NOR는 신흥 응용 분야로의 확산을 더욱 가속화하고 있습니다. 여기에는 콤팩트하고 효율적인 설계가 점점 더 중요시되는 웨어러블 기기나 IoT 노드 등이 포함됩니다.

이러한 추세는 시리얼 기술의 장점을 증폭시키는 2차적 효과에 힘입어 더욱 가속화되고 있습니다. 자동차 설계자들은 싱글 엔드 직렬 라인을 소형 하네스에 배선함으로써 기판 면적을 줄이고, 설계 간소화와 비용 절감을 실현하고 있습니다. 동시에, 산업용 OEM 업체들은 EMC 적합성 검사에서 유리한 점인 부품 수가 적다는 점을 이유로 시리얼 NOR를 선호하여 채택하고 있습니다. 이러한 경향이 다양한 산업 분야에서 신규 설계 시 시리얼 기술의 도입을 촉진하고 있습니다. 그 결과, 영국의 NOR 플래시 시장은 고속 SPI 생태계 쪽으로 점점 더 기울고 있습니다. 이러한 변화는 현대의 용도 수요에 부응하는 데 있어 시리얼 NOR의 중요성이 점점 더 커지고 있음을 보여줍니다.

2025년에는 쿼드 SPI가 매출의 43.2%를 차지했으며, 옥탈 및 xSPI 인터페이스는 2031년까지 연평균 9.7%의 성장률을 보일 것으로 전망됩니다. 이러한 성장은 주로 효율적으로 작동하기 위해 200 MB/s를 초과하는 읽기 스트림이 필요한 ADAS 도메인 컨트롤러 수요 증가에 힘입은 것입니다. 옥탈 디바이스는 쿼드 디바이스에 비해 랜덤 액세스 지연 시간을 40% 단축하는 등 큰 이점을 제공하며, 고성능 응용 분야에서 선호되는 선택지가 되고 있습니다. 또한, 이러한 장치는 동시 뱅크 작동을 지원하며, 이는 원활한 무선 업데이트를 실현하기 위한 중요한 기능입니다. 이러한 장점에도 불구하고, 옥탈 및 xSPI 인터페이스의 도입은 마이크로컨트롤러의 리프레시 주기에 의존하기 때문에 지연되는 경향이 있었습니다. 그러나 Tier 1 자동차 부품 공급업체들은 이미 xSPI 메모리 스택의 검증을 진행 중이며, 2027년에 시작될 프로그램에 이를 통합하는 것을 목표로 하고 있습니다.

기존 싱글 및 듀얼 SPI 부품은 합리적인 가격이 중요한 고려 사항인 가전제품이나 공공요금 계량기 등, 비용을 중시하는 분야에서 계속해서 그 역할을 수행하고 있습니다. 이러한 구성 요소들은 시장 규모 확대에 기여하고 있지만, 기술이 구식이기 때문에 부가가치 향상 가능성은 제한적입니다. 버스 폭의 차이를 추상화하는 소프트웨어 툴체인을 통해 옥탈 인터페이스로의 전환이 가속화되고 있으며, 제조업체의 전환 과정이 간소화되고 있습니다. 그 결과, 특히 영국의 NOR 플래시 시장에서 옥탈 인터페이스가 차세대 설계의 표준 선택지가 될 것으로 예측됩니다. 이러한 변화는 기존 SPI 부품으로는 충분히 충족시킬 수 없는 현대적인 용도에서 요구되는 고성능화와 신뢰성에 대한 수요 증가를 반영하고 있습니다. 옥탈 기술의 도입은 시장 상황을 재정의하고, 진화하는 설계 요건과의 호환성을 확보하는 계기가 될 것으로 보입니다.

2025년에는 산업용 및 스마트 에너지 계량기 분야의 임베디드 컨트롤러 수요 증가에 힘입어, 16메가비트(8Mb) 대역이 전체 지출의 21.1%를 차지했습니다. 이러한 컨트롤러는 이러한 용도에서 효율적인 운영과 에너지 관리를 실현하는 데 필수적입니다. 그러나 성장세는 “"128메가비트(64Mb)" 부문으로 전환되고 있으며, 동 기간 동안 7.3%의 성장률이 예상됩니다. 이러한 성장은 주로, 고도의 기능을 지원하기 위해 대용량 펌웨어와 AI 웨이트 캐시가 필요한 EV 게이트웨이의 채택 확대에 기인합니다. 마크로닉스의 “"ArmorBoot" 컴포넌트(512Mb-2GB)는 사이버 보안 규제의 대상이 되는 자산을 위해 보안 부팅 솔루션을 제공함으로써 매우 중요한 역할을 수행하고 있습니다. 이러한 추세에 따라 NOR 플래시는 기존에 NAND 기술이 주류를 이루던 용도 부문으로 진출하고 있습니다.

저사양 2Mb 및 그 이하 용량의 제품은 컴팩트한 크기와 효율성이 장점으로 작용하는 전원 관리 IC 분야에서 계속해서 활용되고 있습니다. 그러나 다이 크기의 축소에 따른 경제성 문제로 인해, 공급업체 입장에서는 이러한 미세한 기하학적 구조의 수익성이 점차 떨어지고 있으며, 이는 생산량 감소로 이어지고 있습니다. 한편, 하이엔드 부문에서의 기술 발전은 새로운 기회를 열어주고 있습니다. 적층형 3D NOR 기술의 도입으로 4Gb 단일 칩 디바이스의 개발이 가능해졌습니다. 이러한 디바이스는 높은 성능과 신뢰성이 요구되는 인포테인먼트 시스템이나 엣지 AI 워크로드에 최적입니다. 이러한 기술적 진보에 힘입어 영국 내 NOR 플래시 시장의 성장 가능성이 크게 확대되고 있으며, 고도화된 용도에 대한 진화하는 수요에 대응할 수 있는 체제가 점차 갖춰지고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the united kingdom NOR flash market size is expected to increase from USD 106.64 million in 2026 to USD 134.82 million by 2031, growing at a CAGR of 4.8% over 2026-2031.

This report is Segmented by Type (Serial NOR Flash, and More), Interface (Quad SPI, and More), Density (2 Megabit and Less, and More), Voltage (3 V Class, Wide-Voltage, and More), End-User Application (Communication, and More), Process Technology Node (45 Nm, 65nm, and More), and Packaging Type (QFN/SOIC, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

United Kingdom NOR Flash Market Trends and Insights

Growing Adoption of ADAS and EV Platforms by UK OEMs Requiring Instant-Boot

Automotive designs now embrace zonal controllers, digital clusters, and ADAS stacks that run safety-critical code from execute-in-place memory. Infineon's ASIL-D qualified SEMPER line and Winbond's W35T octal family headline the approved device roster, enabling 400 MB/s read bandwidth within -40 °C to +125 °C envelopes. Jaguar Land Rover's mid-2026 production halt over missing flash parts underlined supply fragility, prompting OEMs to dual-source and raise buffer stock. Zone-based EV platforms can host 10-15 discrete NOR sockets, more than triple legacy counts, making automotive the single largest growth lever for the United Kingdom NOR Flash market.

5G Infrastructure Roll-Out Accelerating Demand for High-Reliability Code Storage in Telecom Gear

Virgin Media O2's GBP 700 million (USD 889 million) upgrade budget with Ericsson and Nokia, and Vodafone-Three's 99% SA coverage pledge create a multi-year base-station build-out pipeline. Each radio unit embeds 64-256 Mb NOR for boot code and patch storage that survives harsh outdoor duty cycles. Regulatory backlogs around 6,200 pending tower approvals delay installations but extend procurement visibility, benefiting code-storage suppliers serving the United Kingdom NOR Flash market.

Limited Domestic Wafer-Fab Capacity Leading to Supply-Chain Vulnerability

About 25 fabs in the UK continue to operate with geometries exceeding 180 nm, leading buyers to rely on imports for every advanced NOR part. The lack of domestic production capacity for advanced NOR Flash components has created a significant dependency on external suppliers. Offshore bottlenecks have further exacerbated the situation, with lead times for automotive-grade parts extending to 24 weeks in 2026. This has forced OEMs to maintain a safety stock for four months to mitigate supply chain disruptions. Meanwhile, an upgrade in Newport, costing GBP 250 million (USD 320 million), is focusing on SiC power instead of memory production. Consequently, the NOR Flash market in the UK remains structurally exposed to external shocks.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Smart Metering and IoT Deployments Under UK Net-Zero Mandate

- Shift Toward Octal/xSPI Architectures in Edge-AI Modules Manufactured in the UK

- Rising Competitiveness of Low-Cost eMMC and High-Density NAND Solutions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, serial devices claimed a dominant 71.8% share of the United Kingdom's NOR Flash market. This dominance is attributed to the efficiency of quad and octal buses, which have significantly reduced PCB area while maintaining first-byte latency. Parallel NOR continues to play a critical role in avionics and defense applications due to its deterministic sub-10 ns access. However, its market share is projected to decline as serial bandwidth reaches 400 MB/s, offering a competitive alternative. Additionally, advancements in packaging, particularly the transition to WLCSP, are further embedding serial NOR in emerging applications. These include wearables and IoT nodes, where compact and efficient designs are increasingly prioritized.

These trends are further bolstered by secondary effects that amplify the advantages of serial technology. Automotive designers are leveraging board savings by routing single-ended serial lines through compact harnesses, which simplifies design and reduces costs. At the same time, industrial OEMs are favoring serial NOR due to its lower component count, which proves advantageous during EMC compliance testing. These preferences are driving the adoption of serial technology in new designs across multiple industries. As a result, the United Kingdom's NOR Flash market is increasingly leaning towards high-speed SPI ecosystems. This shift underscores the growing importance of serial NOR in meeting the demands of modern applications.

In 2025, Quad SPI accounted for 43.2% of the revenue, while octal and xSPI interfaces are projected to grow at a rate of 9.7% through 2031. This growth is primarily driven by the increasing demand from ADAS domain controllers, which require read streams exceeding 200 MB/s to function efficiently. Octal devices offer significant advantages, including a 40% reduction in random-access latency compared to quad counterparts, making them a preferred choice for advanced applications. Additionally, these devices support simultaneous bank operations, a critical feature for enabling seamless over-the-air updates. Despite these benefits, the adoption of octal and xSPI interfaces has been slower due to their dependence on microcontroller refresh cycles. However, Tier-1 automotive suppliers are already validating xSPI memory stacks, targeting their integration into 2027 launch programs.

Legacy single and dual SPI components continue to play a role in cost-sensitive sectors, such as consumer electronics and utility meters, where affordability is a key consideration. These components contribute to market volume but offer limited potential for value growth due to their outdated technology. The transition to octal interfaces is being accelerated by software toolchains that abstract differences in bus width, simplifying the migration process for manufacturers. As a result, octal interfaces are expected to become the default boot path in next-generation designs, particularly in the UK NOR Flash market. This shift reflects the growing need for higher performance and reliability in modern applications, which legacy SPI components cannot adequately address. The adoption of octal technology is poised to redefine the market landscape, ensuring compatibility with evolving design requirements.

In 2025, the 16-Megabit-and-Less (More than 8 Mb) band accounted for 21.1% of spending, driven by the increasing demand for embedded controllers in industrial and smart-energy meters. These controllers are critical for enabling efficient operations and energy management in these applications. However, the growth trajectory is shifting towards the 128 Megabit and Less (More than 64 Mb) tier, which is projected to grow at a rate of 7.3% during the same period. This growth is primarily attributed to the rising adoption of EV gateways, which require larger firmware and AI weight caches to support advanced functionalities. Macronix's ArmorBoot components, ranging from 512 Mb to 2 GB, are playing a pivotal role by providing secure-boot solutions for cybersecurity-regulated assets. This development is pushing NOR Flash into application spaces that were previously dominated by NAND technology.

Low-end 2 Mb and smaller densities continue to find applications in power-management ICs, where their compact size and efficiency are advantageous. However, the economics of shrinking die sizes are gradually making these smaller geometries less viable for suppliers, leading to a reduction in their production. On the other hand, advancements at the higher end of the spectrum are opening new opportunities. The introduction of stacked 3D NOR technology is enabling the development of single-chip 4 Gb devices. These devices are well-suited for infotainment systems and edge-AI workloads, which demand high performance and reliability. This technological progress is significantly expanding the growth potential of the NOR Flash market in the United Kingdom, positioning it to meet the evolving demands of advanced applications.

Complete Report Scope:

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less NOR

- 4 Megabit and Less (More than 2 Mb)

- 8 Megabit and Less (More than 4 Mb)

- 16 Megabit and Less (More than 8 Mb)

- 32 Megabit and Less (More than 16 Mb)

- 64 Megabit and Less (More than 32 Mb)

- 128 Megabit and Less (More than 64 Mb)

- 256 Megabit and Less (More than 128 Mb)

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V-3.6 V)

- Sub-1.8 V Class (1.2 V, 2.5 V, 5 V)

- By End-User Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial and Energy

- Other Applications

- By Process Technology Node (Value)

- 90 nm and Above

- 65 nm

- 55 nm

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

List of Companies Covered in this Report:

- Infineon Technologies AG

- Micron Technology Inc.

- Winbond Electronics Corp.

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corp.

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan Xinxin Semiconductor Manufacturing Co. Ltd.

- Puya Semiconductor (Shanghai) Co. Ltd.

- Semiconductor Manufacturing International Corp.

- Adesto Technologies Corp. (a Dialog/Renesas Company)

- SMIC-Fabless UK Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G Infrastructure Roll-out Accelerating Demand for High-Reliability Code Storage in Telecom Gear

- 4.2.2 Growing Adoption of ADAS and EV Platforms by UK OEMs Requiring Instant-Boot

- 4.2.3 Expansion of Smart Metering and IoT Deployments Under UK Net-Zero Mandate

- 4.2.4 Defense Modernisation Programmes (Tempest, Skynet 6) Increasing Secure NOR Flash Uptake

- 4.2.5 Semiconductor Design Tax Incentives (UK Semiconductor Strategy 2023) Boosting Local Prototyping

- 4.2.6 Shift Toward Octal/xSPI Architectures in Edge AI Modules Manufactured in the UK

- 4.3 Market Restraints

- 4.3.1 Limited Domestic Wafer-Fab Capacity Leading to Supply-Chain Vulnerability

- 4.3.2 Rising Competitiveness of Low-Cost eMMC and High-Density NAND Solutions

- 4.3.3 High Photolithography Tooling Costs at 28 nm Nodes

- 4.3.4 Brexit-Induced Regulatory Complexity for Cross-Border Semiconductor Trade

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less NOR

- 5.3.2 4 Megabit and Less (More than 2 Mb)

- 5.3.3 8 Megabit and Less (More than 4 Mb)

- 5.3.4 16 Megabit and Less (More than 8 Mb)

- 5.3.5 32 Megabit and Less (More than 16 Mb)

- 5.3.6 64 Megabit and Less (More than 32 Mb)

- 5.3.7 128 Megabit and Less (More than 64 Mb)

- 5.3.8 256 Megabit and Less (More than 128 Mb)

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V-3.6 V)

- 5.4.4 Sub-1.8 V Class (1.2 V, 2.5 V, 5 V)

- 5.5 By End-User Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial and Energy

- 5.5.5 Other Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Above

- 5.6.2 65 nm

- 5.6.3 55 nm

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Micron Technology Inc.

- 6.4.3 Winbond Electronics Corp.

- 6.4.4 Macronix International Co. Ltd.

- 6.4.5 GigaDevice Semiconductor Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Renesas Electronics Corp.

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Wuhan Xinxin Semiconductor Manufacturing Co. Ltd.

- 6.4.11 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.12 Semiconductor Manufacturing International Corp.

- 6.4.13 Adesto Technologies Corp. (a Dialog/Renesas Company)

- 6.4.14 SMIC-Fabless UK Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment