|

시장보고서

상품코드

2063745

IT 및 통신 분야 HCM 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)HCM Software In IT And Telecom - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

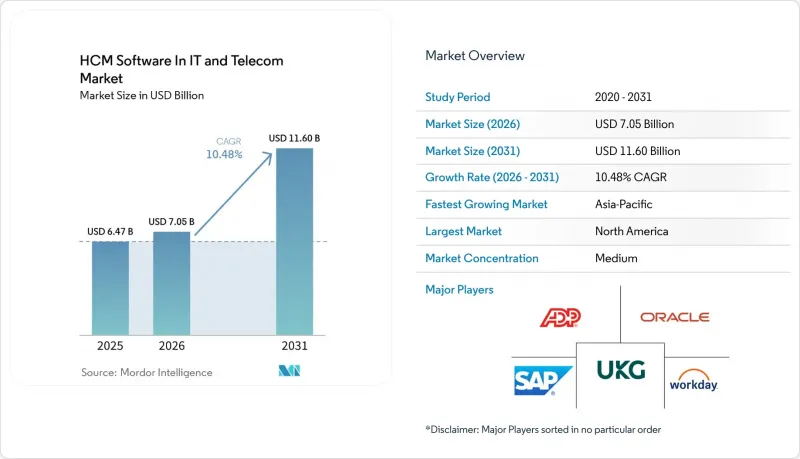

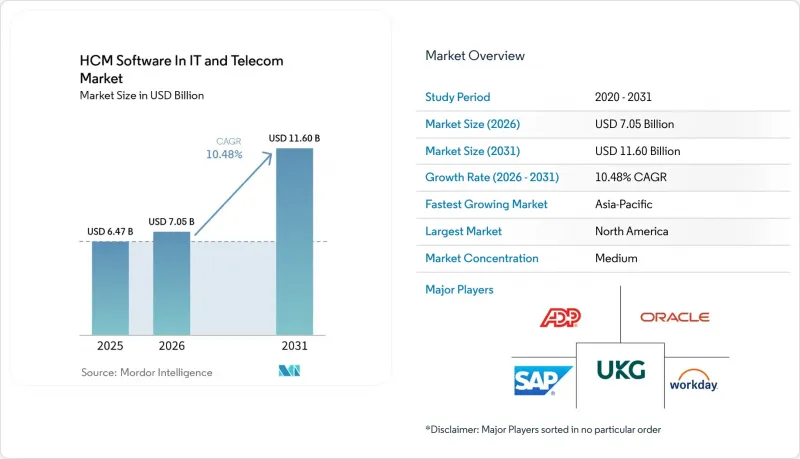

Mordor Intelligence에 의하면, IT 및 통신 분야 HCM 소프트웨어 시장 규모는 2025년 64억 7,000만 달러로 평가되었습니다. 2026년에는 70억 5,000만 달러로 확대되어 2031년까지 116억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 10.48%를 나타낼 것으로 전망됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(On-Premise, 클라우드, 하이브리드), 용도(핵심 HR, 인재 관리, 인력 관리, 급여 계산 등), 기업 규모(중소기업 및 대기업), 최종 사용자 산업(IT 서비스 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 IT 및 통신 분야 HCM 소프트웨어 시장 동향 및 인사이트

IT 스택에서 클라우드 네이티브 도입 확대

IT 서비스 제공업체와 통신 사업자들은 실시간 인력 배치를 위해 1초 미만의 API 응답 시간을 달성하고자, HR 워크로드를 컨테이너화된 마이크로서비스로 재구축하고 있습니다. 2025년 11월에 출시된 Workday의 ‘EU Sovereign Cloud’를 통해 유럽의 통신 사업자들은 기능 저하 없이 데이터를 지역 내에 보관할 수 있게 되었으며, GDPR(EU 개인정보보호규정) 요건을 준수하고 있습니다. SAP SuccessFactors는 2026년에 400개 이상의 클라우드 네이티브 기능을 추가했습니다. 여기에는 47개국에 걸친 세무 조정을 수행하는 급여 계산 봇이 포함됩니다. 이 아키텍처로의 전환을 통해 On-Premise 환경에 비해 인프라 오버헤드를 최대 35% 줄이고, MSP의 온보딩 주기를 몇 주에서 며칠로 단축합니다.

통신 네트워크의 진화를 위한 AI 기반 역량 매핑

아시아태평양의 통신 사업자들은 자격 및 교육 기록을 분석하는 AI 엔진을 도입하여, 어떤 기술자가 구리선 유지보수 업무에서 5G 스몰셀 구축 업무로 전환할 수 있을지 예측했습니다. Eightfold AI는 이직 위험이 높은 엔지니어를 파악하고, 이직 방지를 위한 제안을 제시함으로써 이직률을 22% 낮추고 있습니다. SkillPanel과 같은 플랫폼은 90일 이내에 기술 격차를 해소할 수 있는 맞춤형 역량 강화 경로를 제안함으로써, 통신 사업자가 기존 인력을 Open RAN 프로젝트에 재배치할 수 있도록 지원하고 있습니다.

데이터의 소재지와 주권에 관한 우려

유럽의 GDPR(EU 개인정보보호규정), 중국의 CSL, 인도의 DPDP법에 대응하는 기업은 여러 개의 HCM(인사 관리) 시스템을 운영해야 합니다. 현재 벤더들은 소버린 클라우드 SKU에 대해 15%-20%의 할증 요금을 부과하고 있어, 이미 5G 구축에 자금을 투입하고 있는 통신 사업자들의 IT 예산을 압박하고 있습니다. 이러한 단편화된 상황으로 인해 도입 기간이 최대 6개월까지 연장되고, 인사팀에 부담을 주는 추가적인 감사 절차가 불가피하게 되었습니다.

부문별 분석

이 서비스는 2025년 매출의 31.86%를 차지했으나, 해당 연도의 연평균 성장률(CAGR)이 13.76%인 점을 고려할 때, IT 및 통신 분야 HCM 소프트웨어 시장에서 이 서비스의 점유율은 2031년까지 확대될 전망입니다. 시스템 통합 업체는 AI를 활용한 근무 일정 관리 엔진을 구축하고, On-Premise ERP에서 수십 년에 걸친 급여 내역을 추출하고 있는데, 이는 고객이 단독으로 수행하기에는 주저하게 되는 작업입니다. 소프트웨어 벤더들이 직무 설명서나 보상 제안을 자동으로 작성해 주는 생성형 코파일럿을 탑재하고 있기 때문에 IT 및 통신 분야 HCM 소프트웨어 시장 내 소프트웨어 부문 점유율은 계속해서 높은 수준을 유지할 것으로 보입니다. 그러나 라이선스 갱신 주기가 성숙해짐에 따라 구독 서비스의 성장세는 정체 국면에 접어들고 있습니다.

대형 MSP(관리형 서비스 제공업체)는 고객 포트폴리오 전반에 걸쳐 Dayforce, Oracle HCM Cloud 또는 UKG를 표준화하고, 계약직 직원의 온보딩 과정을 효율화함으로써 지속적인 자문 수수료를 창출하고 있습니다. 이에 대해 벤더 측은 데이터 추출 및 90일간의 하이퍼케어(Hypercare)를 포함한 고정 가격의 마이그레이션 패키지를 제공함으로써 대응하고 있으며, 과거의 일시적인 라이선스 거래를 수년에 걸친 서비스 수익으로 전환하고 있습니다.

2025년에도 클라우드는 56.88%의 점유율로 지배적인 위치를 유지했으나, 하이브리드 부문의 연평균 성장률(CAGR) 12.91%는 예측 기간 동안 IT 및 통신 분야 HCM 소프트웨어 시장 규모 내에서 가장 빠르게 성장하는 분야임을 보여줍니다. 기업은 GDPR(EU 개인정보보호규정) 및 인도의 DPDP 규정을 준수하기 위해 핵심 급여 계산 데이터를 주권 환경에 저장하는 한편, GPU 용량이 확보된 전 세계 각지에서 인재 분석을 수행하고 있으며, 이러한 구성은 AI 워크로드의 지연 시간 목표도 충족하고 있습니다.

하이브리드 모델의 성장은 클라우드의 경제성과 데이터 주권 사이의 긴장 관계를 여실히 드러내고 있습니다. Oracle 등 벤더들은 현재 관리자가 개별 테이블에 지오펜스를 설정할 수 있도록 하고 있어, 급여 데이터가 해외로 유출되는 일은 절대 없지만, 직원 만족도 조사 응답은 감정 분석을 위해 지역 클러스터로 동기화됩니다. On-Premise 도입 규모는 계속 축소될 전망이지만, 노동조합 협약에 구속된 일부 통신 사업자들은 단체 협약을 충족하기 위해 계속해서 시스템을 현지에서 호스팅할 것으로 보입니다.

지역별 분석

북미는 높은 클라우드 보급률, 풍부한 벤처 자금, 그리고 급여 계산 분야에 대한 깊은 전문 지식을 바탕으로 2025년에도 37.12%의 점유율을 차지하며 수익의 주축으로 자리매김했습니다. Workday, ADP, UKG의 초기 도입 사례 대부분은 이곳을 출발점으로 하고 있으며, 갱신률은 90% 가까이 유지되고 있습니다. 그러나 규제 환경이 안정적이기 때문에 AI 모듈의 업셀 가능성은 여전히 남아 있지만, 향후 성장세는 완만해질 것으로 보입니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 11.78%를 기록하며 가장 빠른 성장세를 보이고 있습니다. 이는 인도, 인도네시아, 필리핀의 통신 사업자들이 타워(통신탑)의 에너지 비용을 최적화하기 위해 블루칼라 인력의 디지털화를 추진하고 있기 때문입니다. 인도와 인도네시아의 통신 사업자들은 인사 관리 프로그램의 디지털화를 추진하고 있으며, du Telecom은 2025년에 TCS의 HCM 플랫폼을 도입한 후 50%의 효율 향상을 달성했다고 밝혔습니다. 각국의 데이터 보호법에 따라 벤더들은 국내 데이터 존을 개설해야 하는 상황에 놓여 있으며, 이는 현지 시스템 통합사업자들에게 발판이 되어 IT 및 통신 분야 HCM 소프트웨어 시장 점유율 확대를 뒷받침하고 있습니다. 위험 수당 자동화나 생체 인증을 통한 근태 관리와 같은 통신 업계 특유의 기능들은 분산된 현장 직원을 관리하는 통신 사업자들의 도입을 촉진하고 있습니다.

유럽에서는 엄격한 노사협의회의 참여에 관한 규정과 임금 평등화 지침에 따라 도입 기반이 대폭 확대되고 있습니다. GDPR(EU 개인정보보호규정)로 인한 데이터 주권에 대한 투자가 하이브리드 도입을 뒷받침하고 있지만, 거시경제의 역풍과 장기화되는 ERP 교체로 인해 라이선스 총수 증가세는 둔화되고 있습니다. 그럼에도 불구하고, SAP와 Workday의 소버린 클라우드 출시가 여전히 탄력을 유지하며 시장 점유율 하락을 막고 있습니다.

중동 및 아프리카 시장은 국유화 프로그램에서 민간 노동력의 비율을 입증하기 위한 실시간 대시보드가 필요함에 따라 성장하고 있습니다. 이 지역의 소버린 클라우드에 대한 수요는 유럽과 비슷하지만, 레거시 시스템의 부담이 제한적이기 때문에 On-Premise를 완전히 건너뛰고 그린필드 방식의 SaaS 도입이 가능합니다. 남미에서는 통화 변동에 직면해 있지만, 브라질의 eSocial 보고를 자동화하는 컴플라이언스 플랫폼이 클라우드 전환을 주도하며 한 자릿수 중반대 시장 점유율을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the hCM software in IT and telecom market size is expected to increase from USD 6.47 billion in 2025 to USD 7.05 billion in 2026 and reach USD 11.60 billion by 2031, growing at a CAGR of 10.48% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (On-Premises, Cloud, and Hybrid), Application (Core HR, Talent Management, Workforce Management, Payroll, and More), Organization Size (Small and Medium Enterprises, and Large Enterprises), End User Industry (IT Services, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HCM Software In IT And Telecom Market Trends and Insights

Growing Cloud-Native Adoption in IT Stacks

IT service providers and telecom operators are re-platforming HR workloads onto containerized microservices to gain sub-second API response times for real-time labor allocation. Workday's EU Sovereign Cloud release in November 2025 lets European carriers keep data in-region without losing functionality, aligning with GDPR demands. SAP SuccessFactors added more than 400 cloud-native enhancements in 2026, including payroll bots that reconcile taxes across 47 countries. The architecture shift cuts infrastructure overhead by up to 35% compared with on-premises estates and accelerates MSP onboarding cycles from weeks to days.

AI-Enabled Skill Mapping for Telecom Network Evolution

Asia-Pacific telecom operators deploy AI engines that parse certifications and training records to forecast which technicians can shift from copper maintenance to 5G small-cell builds. Eightfold AI identifies flight-risk engineers and triggers retention offers, lowering attrition by 22%. Platforms such as SkillPanel now propose personalized upskilling paths that close gaps within 90 days, helping carriers repurpose legacy staff for Open RAN projects.

Data Residency and Sovereignty Concerns

Enterprises juggling GDPR in Europe, China's CSL, and India's DPDP Act must maintain multiple HCM instances. Vendors now charge 15%-20% premiums for sovereign-cloud SKUs, squeezing IT budgets at carriers already funding 5G rollouts. The fragmented landscape prolongs implementation timelines by up to six months and forces additional audit layers that strain HR teams.

Other drivers and restraints analyzed in the detailed report include:

- Integrated Analytics Driving ROI Visibility

- Compliance Mandates for Distributed Workforces

- Prolonged Legacy ERP Replacement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services accounted for 31.86% of 2025 revenue, but their 13.76% CAGR means this slice of the HCM software in IT and telecom market size will widen by 2031. Systems integrators configure AI shift-scheduling engines and extract decades of payroll history from on-premises ERPs, workloads that customers are reluctant to tackle alone. The HCM software in IT and telecom market share held by software will remain substantial because vendors embed generative copilots that auto-draft job descriptions and compensation offers, yet subscription growth is leveling as license renewal cycles mature.

Large MSPs standardize Dayforce, Oracle HCM Cloud, or UKG across client portfolios to streamline contractor onboarding, driving recurring advisory fees. Vendors respond with fixed-price migration bundles that include data extraction and 90-day hypercare, turning what was a one-time license transaction into a multiyear services annuity.

Cloud remained dominant at 56.88% in 2025, but hybrid's 12.91% CAGR positions it as the fastest-rising slice of the HCM software in IT and telecom market size over the forecast horizon. Enterprises store core payroll in sovereign environments to respect GDPR or India's DPDP rules while running talent analytics in global regions where GPU capacity sits, a configuration that still meets latency targets for AI workloads.

Hybrid growth underscores the tension between cloud economics and data sovereignty. Vendors such as Oracle now allow administrators to geofence individual tables so salary data never leaves the country, while engagement-survey responses sync to regional clusters for sentiment analysis. On-premises footprints will keep shrinking, though certain carriers bound by union accords continue to host systems locally to satisfy collective agreements.

Geography Analysis

North America remained the revenue anchor with 37.12% share in 2025, supported by high cloud penetration, abundant venture funding, and deep payroll domain expertise. Most early Workday, ADP, and UKG deployments originated here, and renewal rates stay near 90%. Yet regulatory stability means future growth moderates, even as upsell potential persists for AI modules.

Asia-Pacific delivers the fastest growth at an 11.78% CAGR through 2031 as carriers in India, Indonesia, and the Philippines digitize blue-collar labor to optimize tower energy spend. Carriers in India and Indonesia digitize labor management programs, du Telecom cited 50% efficiency gains after a 2025 deployment of TCS's HCM platform. Domestic data-protection laws push vendors to open in-country zones, creating a springboard for local integrators and boosting the region's slice of the HCM software in IT and telecom market size. Telecom-specific functionality, such as hazard-pay automation and biometric attendance, drives take-up among operators managing dispersed field crews.

Europe holds significant installed bases thanks to stringent works-council engagement rules and wage-equalization directives. GDPR-driven data-sovereignty spending lifts hybrid adoption, though macro headwinds and protracted ERP replacement slow total license growth. Still, sovereign-cloud releases from SAP and Workday preserve momentum, preventing share erosion.

The Middle East and Africa market expands because nationalization programs require real-time dashboards to prove citizen workforce ratios. Sovereign-cloud demand here mirrors Europe, yet limited legacy burden enables greenfield SaaS rollouts that skip on-premises entirely. South America faces currency volatility, but compliance platforms that automate Brazil's eSocial reporting keep cloud conversions moving, sustaining a mid-single-digit share.

- Workday Inc.

- SAP SE

- Oracle Corporation

- UKG Inc.

- ADP LLC

- Ceridian HCM Holding Inc.

- Cornerstone OnDemand Inc.

- Paycom Software Inc.

- Paylocity Holding Corporation

- The Sage Group plc

- Infor Inc.

- YourPeople Inc. (Zenefits)

- BambooHR LLC

- Gusto Inc.

- PeopleFluent Inc.

- Ceridian Dayforce, Inc.

- Ramco Systems Limited

- Kronos Systems Incorporated

- Rippling People Center Inc.

- Namely Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Cloud-Native Adoption in IT Stacks

- 4.2.2 Integrated Analytics Driving ROI Visibility

- 4.2.3 Shift Toward Unified Employee Experience Platforms

- 4.2.4 Compliance Mandates for Distributed Workforces

- 4.2.5 Rising M&A Activity Among Pure-Play HCM ISVs

- 4.2.6 AI-Enabled Skill Mapping for Telecom Network Evolution

- 4.3 Market Restraints

- 4.3.1 Data Residency and Sovereignty Concerns

- 4.3.2 Prolonged Legacy ERP Replacement Cycles

- 4.3.3 Shortage of Domain-Specific HCM Integrators

- 4.3.4 Capital-Expenditure Freeze in Telcos Under Margin Pressure

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Core HR

- 5.3.2 Talent Management

- 5.3.3 Workforce Management

- 5.3.4 Payroll

- 5.3.5 Other Applications

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By End User Industry

- 5.5.1 IT Services

- 5.5.2 Telecom Operators

- 5.5.3 Data Centers

- 5.5.4 Managed Service Providers

- 5.5.5 Other End User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 UKG Inc.

- 6.4.5 ADP LLC

- 6.4.6 Ceridian HCM Holding Inc.

- 6.4.7 Cornerstone OnDemand Inc.

- 6.4.8 Paycom Software Inc.

- 6.4.9 Paylocity Holding Corporation

- 6.4.10 The Sage Group plc

- 6.4.11 Infor Inc.

- 6.4.12 YourPeople Inc. (Zenefits)

- 6.4.13 BambooHR LLC

- 6.4.14 Gusto Inc.

- 6.4.15 PeopleFluent Inc.

- 6.4.16 Ceridian Dayforce, Inc.

- 6.4.17 Ramco Systems Limited

- 6.4.18 Kronos Systems Incorporated

- 6.4.19 Rippling People Center Inc.

- 6.4.20 Namely Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment