|

시장보고서

상품코드

2073273

동남아시아의 HCM 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Southeast Asia HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

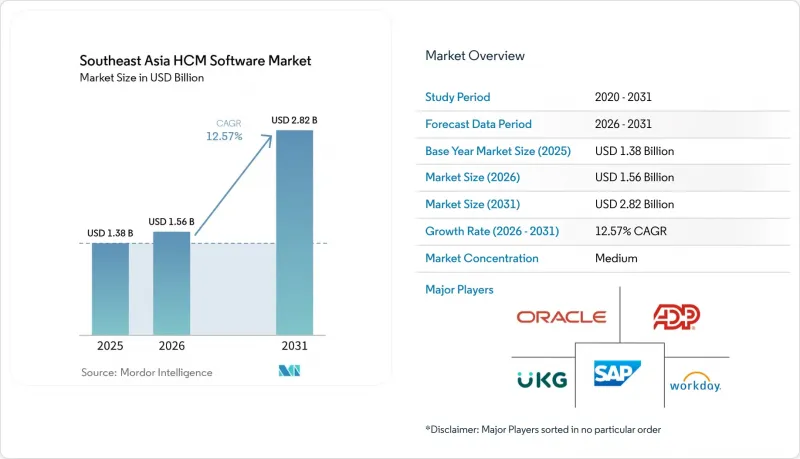

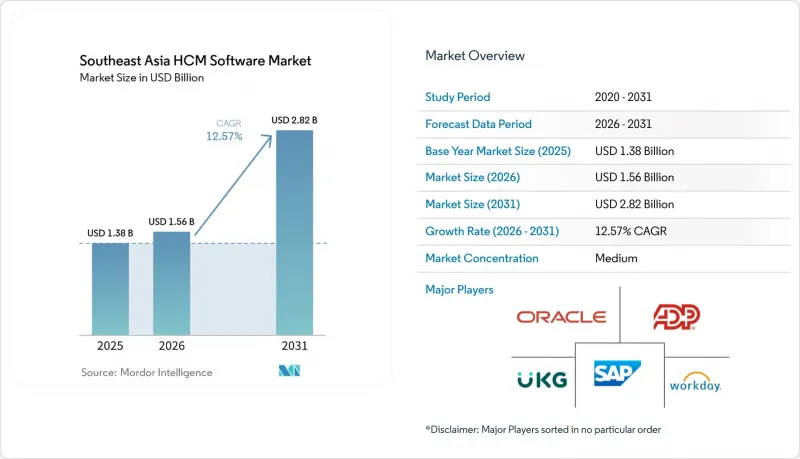

Mordor Intelligence에 의하면, 동남아시아의 HCM 소프트웨어 시장 규모는 2025년에 13억 8,000만 달러로 평가되었습니다. 2026년 15억 6,000만 달러에서 2031년까지 28억 2,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 12.57%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise 등), 조직 규모(대기업 및 중소기업), 용도(핵심 HR, 인재 관리, 인력 관리, 급여 관리 등), 최종 사용자 산업 분야(IT 및 통신, BFSI 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

동남아시아의 HCM 소프트웨어 시장 동향 및 인사이트

가속화되는 '클라우드 퍼스트'의 인사 개혁

인도네시아, 태국, 필리핀의 최고재무책임자(CFO)들은 치솟는 인건비 인플레이션을 억제하기 위해 기존의 On-Premise형 시스템을 대체하고 있으며, Oracle Fusion Cloud HCM으로의 전환을 통해 IT 비용을 39% 절감할 수 있었습니다고 밝혔습니다. 이러한 전환의 배경에는 '모바일 우선' 이러한 행동 양상이 나타나고 있으며, 일선 산업 종사자의 85%가 스마트폰만으로 인사 앱에 접속하고 있습니다. 인도네시아 재무부 등 공공 부문의 선진 사례에서는 "Satu Kemenkeu" 이 플랫폼의 도입으로 인사 업무 처리 시간을 43.7% 단축하여 민간 부문의 기대를 높이고 있습니다.

정부 주도의 디지털 인재 육성 계획

말레이시아 인적자원개발공사(HRDC)는 2025년에 기업 대상 연수에 2억 2,500만 달러의 보조금을 지급했으며, 신청 건수의 40%가 HCM 소프트웨어 비용을 대상으로 했습니다. 필리핀과 싱가포르 간의 디지털 경제 협정에 따라 전자 급여 기록의 상호 이용이 가능해졌으며, 다국적 기업을 대상으로 한 공유 서비스에서 발생하는 마찰이 완화되었습니다. 캄보디아는 세계은행의 지원을 받아 HRMIS를 업그레이드함으로써 28만 4,484명의 공무원의 급여 계산을 표준화하고, 조달 분야에서 선례를 마련했습니다.

아세안 전역에 걸친 법적 규정 준수 체계의 파편화

싱가포르의 CPF, 말레이시아의 EPF, 인도네시아의 BPJS에서는 각각 서로 다른 급여 계산식이 채택되고 있기 때문에 벤더는 여러 개의 계산 엔진을 유지 관리할 수밖에 없어 제품 비용 증가와 기능 표준화의 지연을 초래하고 있습니다. 필리핀에서는 소득 계층이나 고용 형태에 따라 달라지는 사회보장 제도, PhilHealth, Pag-IBIG 기금에 대한 납입금이 상황을 더욱 복잡하게 만들고 있습니다. 한편, 태국의 사회보장 기금과 베트남의 사회보험, 건강보험, 실업보험 제도는 추가적인 현지화 요건을 부과하고 있습니다. 데이터 개인정보 보호 제도의 차이는 국경을 초월한 플랫폼의 확장을 더욱 복잡하게 만들고 있으며, 소규모 제공업체들은 여러 국가에 대한 대응을 미룰 수밖에 없는 상황에 처해 있습니다.

부문별 분석

서비스 수익은 법규 준수 매핑 및 변경 관리에 대한 수요 증가를 반영하여, 2026년부터 2031년까지 13.74%의 성장률이 예상됩니다. 2025년 시점에서는 소프트웨어가 여전히 74.92%를 차지하고 있었지만, 많은 구매자들은 현재 지속적인 규정 업데이트를 보장하기 위해 도입 계약과 관리형 서비스 계약을 세트로 체결하는 추세입니다. Darwinbox가 필리핀에서 시작한 다국적 급여 계산 서비스는 공급업체가 '서비스형 규정 준수(Compliance-as-a-Service)' 이를 통해 어떻게 수익을 창출하고 있는지 보여주는 좋은 예입니다. Oracle의 아시아태평양 서비스 매출은 클라우드 전환 프로젝트를 바탕으로 2025 회계연도에 18% 증가했습니다.

컨설팅 및 매니지드 서비스의 도입은 국경을 넘어 사업을 확장하고 있는 기업들 사이에서 가장 두드러지게 나타나며, 이러한 기업들은 규정이 세분화되어 있어 공급업체를 변경하는 데 비용이 많이 듭니다. 대기업은 클라우드 전환을 가속화하기 위해 데이터 이전을 외부에 위탁하는 반면, 중소기업은 초기 설정을 파트너사에 맡기는 경우가 많습니다. 그 결과, 특히 규제가 엄격한 업종에서 새로운 도입 열풍이 일 때마다 이 서비스의 동남아시아의 HCM 소프트웨어 시장 점유율이 점차 확대되고 있습니다.

2025년에는 클라우드 시장 점유율이 64.41%를 나타냈으며, 연간 14.22%의 성장률이 전망됩니다. 각 벤더사가 데이터 주권 규제를 충족하기 위해 자카르타, 호치민, 쿠알라룸푸르에 데이터센터를 개설함에 따라, 클라우드의 선도적 입지는 더욱 확대될 전망입니다. 국방 및 정부 기관 등 규제가 엄격한 분야에서는 데이터 주권 요건과 레거시 시스템과의 통합 요건으로 인해 On-Premise 방식의 도입이 여전히 주류를 이루고 있지만, 클라우드 제공업체들이 거주 요건을 충족하기 위해 국내에 데이터센터를 설립함에 따라 이 부문은 축소되는 추세입니다.

클라우드 기반 인사 모듈을 활용하면서도 급여 계산은 On-Premise에서 처리하고자 하는 방위·의료 기관에서는 하이브리드 모델이 정착되어 있습니다. 싱가포르의 내셔널 헬스케어 그룹은 2024년에 이러한 하이브리드 스택을 도입했습니다. 가동 시간 향상, 유지보수가 필요 없는 업그레이드, 모바일 사용자 경험(UX) 개선에 힘입어 중소기업의 클라우드 도입이 가속화되고 있습니다. 한편, 이전에는 도입에 소극적이었던 대기업들도 AI 분석을 통합하기 위해 클라우드를 도입하고 있습니다. 그 결과, 2031년까지 클라우드 부문이 동남아시아의 HCM 소프트웨어 시장 점유율의 3분의 2 이상을 차지할 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 주요 요약

제3장 시장 구도

제4장 시장 규모 및 성장 예측

제5장 경쟁 구도

제6장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the southeast asia HCM software market size was valued at USD 1.38 billion in 2025 and is estimated to grow from USD 1.56 billion in 2026 to reach USD 2.82 billion by 2031, at a CAGR of 12.57% during the forecast period (2026-2031).

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud, On-Premises, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and More), End-User Industry (IT and Telecommunications, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

Southeast Asia HCM Software Market Trends and Insights

Accelerated Cloud-First HR Transformation

Chief financial officers in Indonesia, Thailand, and the Philippines are replacing legacy on-premises systems to curb rising labor-cost inflation, citing 39% information-technology savings after migrating to Oracle Fusion Cloud HCM. Mobile-first behavior underpins this pivot, with 85% of staff in frontline industries accessing HR apps solely on smartphones. Public-sector exemplars, such as Indonesia's Ministry of Finance, cut personnel-transaction processing time by 43.7% after rolling out the Satu Kemenkeu platform, raising private-sector expectations.

Government-Led Digital Workforce Initiatives

Malaysia's Human Resource Development Corporation subsidized USD 225 million of enterprise training in 2025, and 40% of claims covered HCM software fees. The Philippines-Singapore Digital Economy Agreement mutualizes electronic payroll records, reducing friction in shared services for multinationals. Cambodia standardized payroll for 284,484 civil servants through a World Bank-backed HRMIS upgrade, setting procurement precedents.

Fragmented Statutory Compliance Across ASEAN

Separate payroll formulas for Singapore CPF, Malaysia EPF, and Indonesia BPJS oblige vendors to maintain multiple calculation engines, inflating product costs and stalling feature parity. The Philippines adds further complexity with Social Security System, PhilHealth, and Pag-IBIG Fund contributions that vary by income bracket and employment type, while Thailand's Social Security Fund and Vietnam's social insurance, health insurance, and unemployment insurance schemes impose additional localization requirements. Divergent data-privacy regimes further complicate cross-border platform rollouts, forcing smaller providers to defer multi-country support.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Millennial and Gen Z Workforce Demographics

- Emergence of Regional Super-Apps Integrating HR Functions

- Limited HR Tech Budgets in Micro-SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is projected to climb at 13.74% from 2026 to 2031, reflecting rising demand for statutory-compliance mapping and change management. In 2025, software still dominated at 74.92%, but many buyers now bundle implementation and managed-services contracts to ensure continuous regulatory updates. Darwinbox's multi-country payroll launch in the Philippines exemplifies how vendors monetize compliance-as-a-service. Oracle's Asia-Pacific services revenue jumped 18% in fiscal 2025 on cloud-migration projects.

Adoption of consulting and managed services is strongest among firms expanding across borders, where fragmented rules create switching costs. Large enterprises outsource data migration to accelerate cloud cutovers, while SMEs lean on partners to handle initial configuration. As a result, services capture an incremental share of the Southeast Asia HCM Software market size for each new deployment wave, especially in regulated verticals.

Cloud captured 64.41% in 2025 and is forecast to grow 14.22% annually, extending its lead as vendors open Jakarta, Ho Chi Minh City, and Kuala Lumpur data centers to satisfy sovereignty rules. On-premises deployments persist in regulated sectors such as defense and government, where data-sovereignty mandates and legacy-system integration requirements favor locally hosted infrastructure, but this segment is contracting as cloud providers establish in-country data centers to satisfy residency rules.

Hybrid models persist for defense and healthcare entities wanting cloud talent modules but on-premises payroll. Singapore's National Healthcare Group adopted such a hybrid stack in 2024. Improved uptime, zero-maintenance upgrades, and mobile UX propel cloud uptake among SMEs, whereas large enterprises, previously hesitant, now embrace cloud to integrate AI analytics. Consequently, the cloud segment is expected to command more than two-thirds of the Southeast Asia HCM Software market share by 2031.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Core HR

- Talent Management

- Workforce Management

- Payroll Management

- Learning and Development

- By End-User Industry

- IT and Telecommunications

- BFSI

- Industrial Manufacturing

- Healthcare and Lifesciences

- Retail and E-commerce

- Government and Public Sector

- Other End-User Industries

- By Country

- Singapore

- Malaysia

- Indonesia

- Thailand

- Philippines

- Rest of Southeast Asia

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- Workday Inc.

- Automatic Data Processing Inc.

- UKG Inc.

- Dayforce, Inc.

- Cornerstone OnDemand Inc.

- BambooHR LLC

- Paycom Software Inc.

- Paylocity Holding Corporation

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- Darwinbox Digital Solutions Pvt. Ltd.

- The Sage Group plc

- Intuit Inc.

- Global Groupware Solutions Limited

- PeopleStrong Technologies Pvt. Ltd.

- HiBob Ltd.

- Rippling People Center Inc.

- Gusto Inc.

- Deel Inc.

- Infor Inc.

- ServiceNow Inc.

- SumTotal Systems LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 EXECUTIVE SUMMARY

3 MARKET LANDSCAPE

- 3.1 Market Overview

- 3.2 Market Drivers

- 3.2.1 Accelerated Cloud-First HR Transformation

- 3.2.2 Government-Led Digital Workforce Initiatives

- 3.2.3 Expanding Millennial and Gen Z Workforce Demographics

- 3.2.4 Emergence of Regional "Super-Apps" Integrating HR Functions

- 3.2.5 AI-Powered Predictive Workforce Analytics Adoption

- 3.2.6 Cross-Border Freelance Platforms Fueling Payroll Complexity

- 3.3 Market Restraints

- 3.3.1 Fragmented Statutory Compliance Across ASEAN

- 3.3.2 Limited HR Tech Budgets in Micro-SMEs

- 3.3.3 Data Residency and Sovereignty Concerns

- 3.3.4 Shortage of HR IT Integration Talent

- 3.4 Industry Value Chain Analysis

- 3.5 Regulatory Landscape

- 3.6 Technological Outlook

- 3.7 Impact of Macroeconomic Factors on the Market

- 3.8 Porter's Five Forces Analysis

- 3.8.1 Bargaining Power of Suppliers

- 3.8.2 Bargaining Power of Buyers

- 3.8.3 Threat of New Entrants

- 3.8.4 Threat of Substitutes

- 3.8.5 Intensity Competitive Rivalry

4 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 4.1 By Component

- 4.1.1 Software

- 4.1.2 Services

- 4.2 By Deployment Mode

- 4.2.1 Cloud

- 4.2.2 On-Premises

- 4.2.3 Hybrid

- 4.3 By Organization Size

- 4.3.1 Large Enterprises

- 4.3.2 Small and Medium Enterprises

- 4.4 By Application

- 4.4.1 Core HR

- 4.4.2 Talent Management

- 4.4.3 Workforce Management

- 4.4.4 Payroll Management

- 4.4.5 Learning and Development

- 4.5 By End-User Industry

- 4.5.1 IT and Telecommunications

- 4.5.2 BFSI

- 4.5.3 Industrial Manufacturing

- 4.5.4 Healthcare and Lifesciences

- 4.5.5 Retail and E-commerce

- 4.5.6 Government and Public Sector

- 4.5.7 Other End-User Industries

- 4.6 By Country

- 4.6.1 Singapore

- 4.6.2 Malaysia

- 4.6.3 Indonesia

- 4.6.4 Thailand

- 4.6.5 Philippines

- 4.6.6 Rest of Southeast Asia

5 COMPETITIVE LANDSCAPE

- 5.1 Market Concentration

- 5.2 Strategic Moves

- 5.3 Market Share Analysis

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 5.4.1 SAP SE

- 5.4.2 Oracle Corporation

- 5.4.3 Workday Inc.

- 5.4.4 Automatic Data Processing Inc.

- 5.4.5 UKG Inc.

- 5.4.6 Dayforce, Inc.

- 5.4.7 Cornerstone OnDemand Inc.

- 5.4.8 BambooHR LLC

- 5.4.9 Paycom Software Inc.

- 5.4.10 Paylocity Holding Corporation

- 5.4.11 Zoho Corporation Pvt. Ltd.

- 5.4.12 Ramco Systems Limited

- 5.4.13 Darwinbox Digital Solutions Pvt. Ltd.

- 5.4.14 The Sage Group plc

- 5.4.15 Intuit Inc.

- 5.4.16 Global Groupware Solutions Limited

- 5.4.17 PeopleStrong Technologies Pvt. Ltd.

- 5.4.18 HiBob Ltd.

- 5.4.19 Rippling People Center Inc.

- 5.4.20 Gusto Inc.

- 5.4.21 Deel Inc.

- 5.4.22 Infor Inc.

- 5.4.23 ServiceNow Inc.

- 5.4.24 SumTotal Systems LLC

6 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 6.1 White-Space and Unmet-Need Assessment