|

시장보고서

상품코드

2063971

북미의 HCM 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

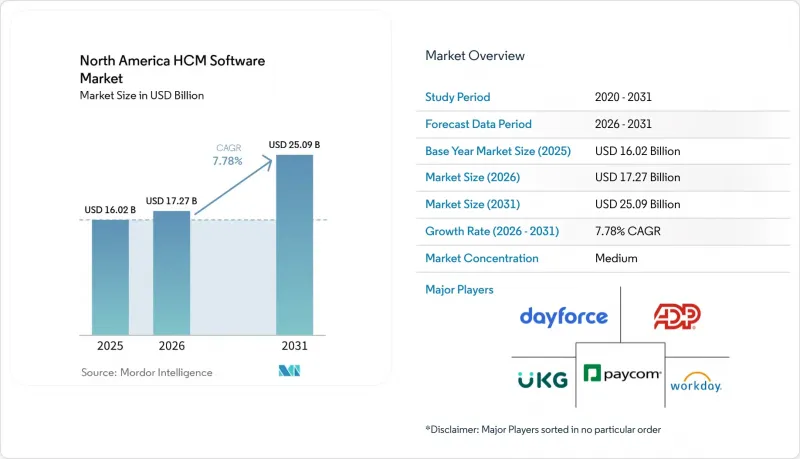

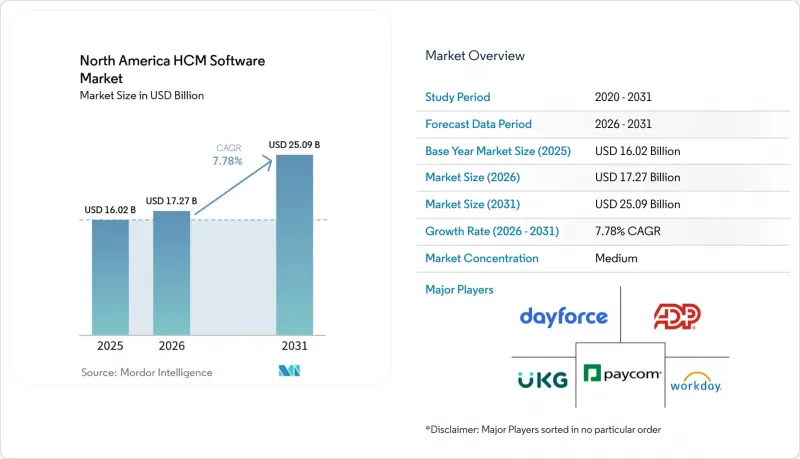

Mordor Intelligence에 의하면, 북미 인사관리(HCM) 소프트웨어 시장 규모는 2025년 160억 2,000만 달러에서 2026년에는 172억 7,000만 달러, 2031년까지 250억 9,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 7.78%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 조직 규모(대기업 및 중소기업), 용도(핵심 HR, 인재 관리 등), 최종 사용자 산업 분야(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 제조업 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미 HCM 소프트웨어 시장 동향과 인사이트

HR 시스템의 클라우드 전환

기업들은 실시간 분석, 모바일 셀프 서비스, 지속적인 기능 출시를 활용하기 위해 On-Premise 인프라에서 클라우드 플랫폼으로의 전환을 계속하고 있습니다. 은행이나 의료 관련 기업들은 데이터 상주 요건을 충족하기 위해 급여 계산 처리를 사내 환경에서 유지하고 있기 때문에 하이브리드 도입의 성장 속도는 순수 클라우드 도입보다 더 빠릅니다. 미국의 ‘HR 2.0’ 프로그램은 220만 명의 민간 직원을 공유 클라우드 서비스 센터로 이전하고 있는 반면, 캐나다 연방 정부의 Dayforce 도입 사례는 노동조합의 급여 규정을 표준화된 워크플로로 전환하는 데 따르는 복잡성을 여실히 보여주고 있습니다. 이러한 주목할 만한 프로젝트들은 클라우드의 경제성을 입증하는 것이며, 주 및 지방 자치 단체 기관들에도 유사한 노력을 기울일 것을 촉구하고 있습니다.

AI를 활용한 인재 분석의 부상

2026년 SHRM 조사에 따르면, 채용 및 성과 관리에 AI를 활용하고 있는 조직은 39%에 달했으며, 지난 3년 동안 급격히 증가했습니다. 이직 예측 모델은 현재 6-9개월 전에 이직 위험을 감지하며, 기술 추론 엔진은 그렇지 않았다면 간과되었을 내부 후보자들을 부각시킵니다. 그러나 변경 관리는 매우 중요합니다. 현장 직원 중 64%가 실직을 우려하고 있어, 공급업체들은 투명성을 확보하고 재교육 경로를 마련할 수밖에 없는 상황입니다. Workday가 2025년에 Paradox를 인수함에 따라, 채용 담당자의 개입 없이 면접 일정을 예약해 주는 대화형 어시스턴트가 통합되었으며, 이를 통해 AI가 어떻게 부가가치가 낮은 업무를 제거하면서도 후보자의 경험을 향상시킬 수 있는지 입증했습니다.

데이터 개인정보 보호 및 사이버 보안에 대한 우려

Paychex와 Workday에서 최근 발생한 정보 유출 사건, 그리고 Oracle의 중요한 CVE-2024-21287 패치는 중앙 집중화된 직원 데이터가 위협 행위자들을 유인한다는 사실을 여실히 보여주고 있습니다. 각 주의 개인정보 보호법은 직원들에게 데이터 접근 및 삭제에 관한 광범위한 권리를 인정하는 반면, 멕시코의 LFPDPPP(개인정보보호법)는 매출액의 최대 2%에 해당하는 과징금을 부과하고 있습니다. 따라서 기업들은 공급업체가 암호화, 접근 제어, 신속한 사고 대응 능력을 입증할 때까지 클라우드 전환을 연기하고 있습니다. 현재 해당 제공업체는 신뢰를 회복하기 위해 SOC 2 보고서와 제로 트러스트 로드맵을 공개하고 있습니다.

부문별 분석

2025년에는 소프트웨어가 72.86%의 점유율을 차지해, 이는 핵심인 인사, 급여, 인재 관리 모듈에서 발생하는 라이선스 수익이 주를 이룰 것임을 반영한 것입니다. 또한 기업들이 HCM 플랫폼과 레거시 ERP 시스템의 통합, 알고리즘을 통한 감사 추적 설정, AI 지원형 의사결정 도구에 대한 관리자 교육 등 전문적인 지식이 필요하기 때문에 서비스 부문은 2031년까지 연평균 8.94%의 성장률을 기록하고 있습니다. 기업들이 데이터 마이그레이션, AI 거버넌스 구축, 레거시 ERP 시스템 통합에 대한 지원을 요청함에 따라 서비스 매출은 소프트웨어 매출을 앞지르는 속도로 증가하고 있습니다. 도입 프로젝트는 대개 12-24개월에 걸쳐 진행되며, 여러 국가에 걸친 급여 계산의 통합을 수반합니다. 또한, 급여 계산이나 복리후생 관리를 아웃소싱하는 것을 선호하는 중소규모 고용주들 사이에서도 매니지드 서비스 도입이 증가하고 있습니다.

클라우드 아키텍처 덕분에 모듈을 단계적으로 구매할 수 있어, 소프트웨어 판매는 호조를 유지하고 있습니다. 벤더들은 구독 계층 구조를 통해 혁신을 수익화하고 있지만, 규정 준수 요건이나 기술 역량 프레임워크로 인해 맞춤형 워크플로가 필요한 경우, 해당 서비스가 더 큰 지갑 점유율을 확보하게 됩니다. 제품 수익과 컨설팅 수익 간의 상호작용은 라이선스 매출 성장세가 둔화되고 있음에도 불구하고 북미 HCM 소프트웨어 시장 규모가 계속해서 확대되고 있는 이유를 여실히 보여주고 있습니다.

클라우드 도입은 초기 투자 비용 절감, 자동 업데이트, On-Premise 시스템으로는 실현할 수 없는 모바일 우선의 직원 경험을 배경으로, 2025년에는 63.42%의 점유율을 차지했습니다. 그러나 기업들이 민첩성과 데이터 저장 위치 및 감사 요건 간의 균형을 모색하는 가운데, 하이브리드 구성이 9.21%라는 가장 높은 성장률을 보이고 있습니다. 인재 관리 및 학습 모듈 분야에서는 클라우드가 여전히 주요 선택지이지만, 은행이나 병원이 기밀성이 높은 급여 데이터를 사내 인프라에 보관하고 있기 때문에 하이브리드 도입이 가장 빠르게 성장하고 있습니다. 이러한 분할 구조를 통해 데이터 주권 규정을 침해하지 않으면서도 신속한 혁신이 가능해집니다.

북미 HCM 소프트웨어 시장에서 On-Premise 도입은 점차 감소하는 추세이지만, 방위 관련 기업이나 일부 캐나다 정부 부처에서는 여전히 독립형 환경을 유지하고 있습니다. 중소기업은 비용 예측 가능성 때문에 순수 클라우드를 선호하는 반면, 전 세계 기업들은 서로 다른 법적 규제 요건에 대응하기 위해 하이브리드 방식을 선택하고 있으며, 이로 인해 하이브리드는 북미 HCM 소프트웨어 시장의 중요한 성장 동력으로서의 입지를 공고히 하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the north america hCM software market size is projected to expand from USD 16.02 billion in 2025 to USD 17.27 billion in 2026 and USD 25.09 billion by 2031, registering a CAGR of 7.78% between 2026 and 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, and More), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America HCM Software Market Trends and Insights

Cloud Migration of HR Systems

Enterprises continue to replace on-premises infrastructure with cloud platforms to gain real-time analytics, mobile self-service, and continuous feature releases. Hybrid adoption grows faster than pure cloud adoption because banking and healthcare firms keep payroll processing in private environments to meet data residency mandates. The U.S. HR 2.0 program is migrating 2.2 million civilian employees to shared cloud service centers, while Canada's federal rollout of Dayforce confirms the complexity of converting union pay rules to standardized workflows. These marquee projects validate the economics of the cloud and encourage state and provincial agencies to follow suit.

Rise of AI-Driven Talent Analytics

A 2026 SHRM survey showed 39% of organizations using AI for recruiting or performance management, up sharply in three years. Predictive attrition models now flag flight risks six to nine months in advance, and skills-inference engines surface internal candidates who would otherwise stay invisible. Yet change management is critical; 64% of frontline staff fear displacement, forcing vendors to supply transparency and reskilling pathways. Workday's 2025 purchase of Paradox embedded conversational assistants that book interviews without recruiter input, demonstrating how AI can remove low-value tasks while enhancing candidate experience.

Data-Privacy and Cyber-Security Concerns

Recent breaches at Paychex and Workday, plus Oracle's critical CVE-2024-21287 patch, highlight how centralized employee data attracts threat actors. State privacy laws grant workers broad rights to access and delete data, while Mexico's LFPDPPP levies fines up to 2% of revenue. Enterprises, therefore, delay cloud migrations until vendors demonstrate encryption, access controls, and rapid incident response. Providers now publish SOC 2 reports and zero-trust roadmaps to rebuild confidence.

Other drivers and restraints analyzed in the detailed report include:

- Compliance Mandates on Payroll and Tax

- Skills-Based Hiring Framework Adoption

- Algorithmic Bias and AI-Audit Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held a 72.86% share in 2025, reflecting the dominance of licensing revenue from core HR, payroll, and talent management modules, yet services are expanding at 8.94% through 2031 as enterprises require specialized expertise to integrate HCM platforms with legacy ERP systems, configure algorithmic audit trails, and train managers on AI-assisted decision tools. Services revenue is rising faster than software revenue as enterprises seek support for migrating data, configuring AI governance, and integrating legacy ERP systems. Implementation projects often span 12-24 months and involve multi-country payroll harmonization. Managed services adoption is also increasing among small employers that prefer to outsource payroll and benefits administration.

Software sales remain robust because cloud architectures enable incremental module purchases. Vendors monetize innovation through subscription tiers, yet services capture greater wallet share when compliance mandates or skills frameworks require customized workflows. The interplay of product and consulting revenue underscores why the North America HCM software market size continues to expand even as license growth moderates.

Cloud deployments commanded a 63.42% share in 2025, driven by lower upfront capital expenditure, automatic updates, and mobile-first employee experiences that on-premises systems cannot match, yet hybrid configurations are growing fastest at 9.21% as enterprises balance agility with data residency and audit requirements. Cloud remains the primary choice for talent and learning modules, but hybrid deployments grow fastest as banks and hospitals keep sensitive payroll data on private infrastructure. This split configuration allows rapid innovation without breaching data sovereignty rules.

On-premises adoption in the North America HCM software market is gradually shrinking, though defense contractors and some Canadian ministries still maintain standalone environments. Small businesses gravitate toward pure cloud for cost predictability, whereas global enterprises choose hybrid to meet divergent jurisdictional mandates, reinforcing hybrid as the pivotal growth engine in the North America HCM software market.

List of Companies Covered in this Report:

- Workday, Inc.

- Ultimate Kronos Group

- Dayforce, Inc.

- Automatic Data Processing, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Namely Inc.

- TriNet Zenefits Inc.

- Gusto, Inc.

- Rippling People Center Inc.

- HiBob Ltd.

- Deel Inc.

- Factorial HR Software SL

- Personio GmbH

- Ramco Systems Limited

- SumTotal Systems LLC

- PeopleStrategy, Inc.

- Lattice, Inc.

- ClearCompany, Inc.

- iSolved HCM LLC

- Zoho Corporation Pvt. Ltd.

- 15Five, Inc.

- TriNet Group, Inc.

- Saba Software LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration of HR Systems

- 4.2.2 Rise of AI-Driven Talent Analytics

- 4.2.3 Compliance Mandates on Payroll and Tax

- 4.2.4 Skills-Based Hiring Framework Adoption

- 4.2.5 Generative AI Copilots for HR Workflows

- 4.2.6 Expansion of Total Workforce Management for Gig Labor

- 4.3 Market Restraints

- 4.3.1 Data-Privacy and Cyber-Security Concerns

- 4.3.2 High Implementation Costs for SMEs

- 4.3.3 Algorithmic Bias and AI-Audit Exposure

- 4.3.4 Legacy ERP-HCM Integration Complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday, Inc.

- 6.4.2 Ultimate Kronos Group

- 6.4.3 Dayforce, Inc.

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Cornerstone OnDemand, Inc.

- 6.4.8 BambooHR LLC

- 6.4.9 Namely Inc.

- 6.4.10 TriNet Zenefits Inc.

- 6.4.11 Gusto, Inc.

- 6.4.12 Rippling People Center Inc.

- 6.4.13 HiBob Ltd.

- 6.4.14 Deel Inc.

- 6.4.15 Factorial HR Software SL

- 6.4.16 Personio GmbH

- 6.4.17 Ramco Systems Limited

- 6.4.18 SumTotal Systems LLC

- 6.4.19 PeopleStrategy, Inc.

- 6.4.20 Lattice, Inc.

- 6.4.21 ClearCompany, Inc.

- 6.4.22 iSolved HCM LLC

- 6.4.23 Zoho Corporation Pvt. Ltd.

- 6.4.24 15Five, Inc.

- 6.4.25 TriNet Group, Inc.

- 6.4.26 Saba Software LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment