|

시장보고서

상품코드

2073276

중동 및 아프리카의 HCM 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Middle East and Africa HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

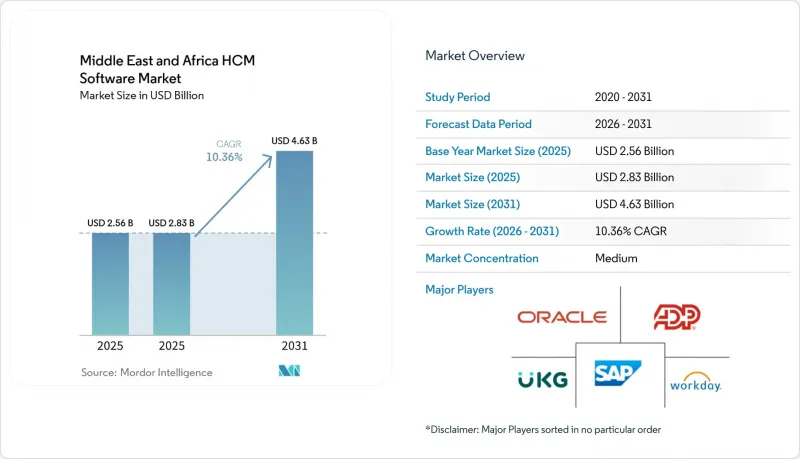

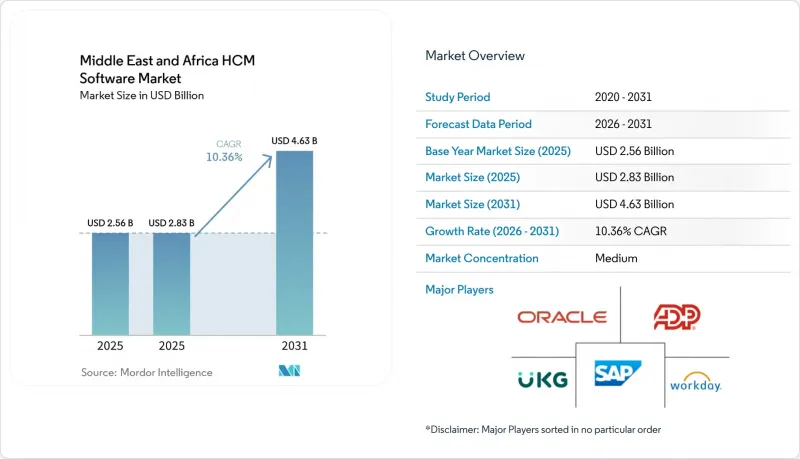

Mordor Intelligence에 의하면, 중동 및 아프리카의 HCM 소프트웨어 시장 규모는 2025년 25억 6,000만 달러로 평가되었습니다. 2026년에는 28억 3,000만 달러, 2031년까지 46억 3,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.36%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 조직 규모(대기업 및 중소기업), 용도(핵심 HR, 인재 관리, 인력 관리 등), 최종 사용자 산업(IT 및 통신 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동 및 아프리카의 HCM 소프트웨어 시장 동향 및 인사이트

GCC 지역 기업들의 클라우드 도입 가속화

걸프 연안 국가들의 고용주들은 각국의 변혁 계획에 포함된 실시간 보고 기준을 충족하기 위해 구식 인사 데이터베이스의 현대화를 급속히 추진하고 있습니다. 사우디아라비아에서는 2024년에 정부 서비스의 디지털화율이 95%에 달했으며, 현재 민간 기업의 이사회도 이러한 기준을 벤치마크로 삼고 있어 클라우드 기반 HCM 도입에 긍정적인 영향을 미치고 있습니다. 아랍에미리트(UAE)는 노동 시장 규정 준수 API를 민간 HCM 제품군과 통합하여 감사 주기를 분기별에서 월별로 단축하는 한편, 원활한 클라우드 연결을 유지하는 기업에 인센티브를 제공합니다. 카타르의 공무원 및 정부개발국은 2025년, 8만 5,000명 이상의 직원을 대상으로 SAP SuccessFactors와 제휴하여, 현재 비공개 기업이 재사용하고 있는 구성 청사진을 공개했습니다. 사우디아라비아와 아랍에미리트 내에서 소버린 클라우드 노드를 운영하는 업체들은 데이터 상주 요건에 대한 우려를 해소함으로써 판매 주기를 단축했습니다. 하이퍼스케일러의 리전이 가동을 시작함에 따라, 하이브리드 보안 정책이 은행 및 유틸리티자의 우려를 해소해 주면서, 연기되었던 전환이 점차 실현되고 있습니다.

임금 보호 및 규정 준수 자동화를 위한 규제 추진

임금 보호 체계에 따라 급여 계산은 미션 크리티컬한 규정 준수 프로세스로 변화했습니다. 아랍에미리트의 '임금 보호 시스템 2.0' 따라서 고용주는 인증 기관을 통해 10영업일 이내에 급여를 입금해야 할 의무가 있으며, 위반을 반복할 경우 고액의 벌금이나 취업 허가 정지 처분을 받게 됩니다. 사우디아라비아의 "Mudad" 이 플랫폼은 급여 데이터를 사회보험 및 출입국 관리 기록과 대조하여, 2025년까지 계약 준수율을 85-90%로 높였습니다. 이로 인해 기업들은 사일로화된 인사 모듈을, Qiwa에 데이터를 자동으로 연동하는 통합형 제품군으로 대체할 수밖에 없게 되었습니다. 쿠웨트에서는 현재 생체 인증을 통한 근태 기록이 의무화되어 있으며, 오만에서는 고용 후 30일 이내에 디지털 계약서를 제출해야 합니다. 이로 인해 HCM이 대응해야 할 규정 준수 범위는 더욱 확대되고 있습니다.

데이터 개인정보 보호 및 데이터 소재지에 관한 규제가 도입 과정을 더욱 복잡하게 만들고 있습니다.

각국의 데이터 보호법에 따라 공급업체는 직원 기록을 현지화해야 할 의무가 있으며, 본래는 단일 멀티테넌트형 클라우드로 충분했을 것이 관할 구역별로 분할된 인스턴스로 세분화되고 있습니다. 아랍에미리트(UAE)는 데이터 수출 메커니즘에 대한 화이트리스트 제도를 유지하고 있어, 구매자가 규제 당국의 승인을 기다리는 동안 조달 기간이 최대 6개월까지 연장되는 상황이 발생하고 있습니다. 남아프리카공화국의 정보 규제 당국이 집행 통지서 발부를 시작함에 따라, 보수적인 은행들 사이에서 전환이 지체되는 원인이 되고 있는 법적 책임에 대한 우려가 커지고 있습니다. 나이지리아에서는 현재 고위험 인사 처리에 대해 데이터 보호 영향 평가가 의무화되어 있으며, 중소규모 고용주들은 턴키 방식의 규정 준수 서비스를 요청함으로써 이러한 부담을 공급업체에 전가하고 있습니다. 그 결과로 발생하는 파치워크 같은 환경 때문에 공급업체는 여러 인프라를 유지 관리할 수밖에 없게 되었고, 수익원가가 증가하며 로드맵 달성이 지연되고 있습니다.

부문별 분석

서비스 시장의 성장률은 소프트웨어 시장을 상회할 것으로 예상되며, 2031년까지 연평균 성장률(CAGR) 11.24%로 확대될 것으로 전망됩니다. 중동 및 아프리카의 HCM 소프트웨어 시장은 도입, 통합, 관리형 서비스에 힘입어 성장하고 있습니다. 이는 모든 걸프 연안 국가들이 독자적인 연금 규정, 다국어 인터페이스, 정부 게이트웨이와의 연동을 지원하는 급여 계산 시스템을 통합하고 있기 때문입니다. Oracle이 2025년에 e사와 체결한 계약에는 38개국의 규정 준수 갱신을 포괄하는 3년간의 관리형 서비스 계층이 포함되어 있으며, 이는 핵심 모듈이 가동을 시작하면 공급업체가 어떻게 지속적인 수익원을 확보할 수 있는지를 보여줍니다. Jisr과 같은 스타트업은 사우디아라비아의 '사우디화' 경영진이 직접 활용할 수 있는 자동화된 대시보드에 기준을 반영함으로써, 지속적인 컨설팅 수수료를 확보하고 있습니다. 에티오피아와 시에라리온에서는 공공 부문의 보조금을 통해 공무원 제도 개혁이 추진되고 있으며, 현지 파트너들은 전 세계 공급업체들이 현지 인력을 배치하지 않은 상태에서 교육 및 변화 관리 업무를 제공할 기회를 얻고 있습니다.

2025년 지출 중 소프트웨어가 여전히 73.48%를 차지했으며, 영구 라이선스 업그레이드와 SaaS 구독이 모든 프로젝트의 기반이 되었습니다. 그렇긴 하지만, 중견 기업의 구매자들이 오픈 API 생태계와 모놀리식 제품군을 비교 검토함에 따라 가격 경쟁은 치열해지고 있습니다. 지역 신생 기업들은 출근 관리 시스템, 보험 통합, 급여 선지급 서비스를 직원 1인당 단일 요금제로 묶어 제공하고 있는 반면, 대형 플랫폼들은 민첩성을 유지하기 위해 특정 마이크로 서비스를 분리하는 움직임을 보이고 있습니다. 예측 기간 동안 중동 및 아프리카의 HCM 소프트웨어 시장에서 서비스 부문의 전체 점유율은 30%대 초반에 달할 것으로 예상되며, 이는 제품화만으로는 해당 지역의 현지화 부담을 완전히 감당할 수 없습니다는 점을 뒷받침하고 있습니다.

클라우드 솔루션은 2025년 시장 가치의 68.92%를 차지하며 연평균 성장률(CAGR) 11.56%로 성장할 전망이지만, 법규 및 전력망 사정으로 인해 SaaS형 인사 관리 모듈을 제외하면 순수한 퍼블릭 아키텍처는 일반적이지 않습니다. 은행이나 정부 기관의 구매자는 급여 계산을 국내 노드에서 처리하면서, 분석 기능은 멀티 리전 클라우드에 맡기는 '스플릿 스택' 점점 더 토폴로지를 선택하고 있습니다. 중동 및 아프리카의 HCM 소프트웨어 시장에서 하이브리드 방식의 도입으로 시장 점유율이 상승할 것으로 전망됩니다. 이는 마이크로소프트, Oracle, SAP가 현재 기밀성이 높은 테이블을 국내 스토리지에 복제하는 지역별 전용 인스턴스를 제공하고 있기 때문입니다.

특히 외부 인터넷 접속을 금지하고 있는 정부 부처 내에서는 여전히 On-Premise 환경이 남아 있지만, 이러한 사이트에서도 패치 적용을 자동화하기 위해 컨테이너화된 오케스트레이션을 도입하고 있습니다. 케냐에서 중단된 데이터센터 프로젝트는 전력 부족으로 인해 하이퍼스케일러의 확장이 지연되고, 디젤 발전기를 갖춘 예비 데이터룸이 계속해서 사용되고 있음을 보여주었습니다. 동기화 에이전트 및 제로 트러스트 게이트웨이를 제공하는 벤더들은 클라이언트가 코드를 수정하지 않고도 주권형과 퍼블릭형 모드를 전환할 수 있도록 함으로써 시장 점유율을 확보하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the middle east and Africa HCM Software market size is projected to expand from USD 2.56 billion in 2025 to USD 2.83 billion in 2026 and USD 4.63 billion by 2031, registering a CAGR of 10.36% between 2026 and 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, and More), End-User Industry (IT and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Middle East and Africa HCM Software Market Trends and Insights

Accelerating Cloud Adoption Across GCC Enterprises

Gulf employers are rapidly modernizing legacy HR databases to meet real-time reporting standards embedded in national transformation plans. Saudi Arabia reached 95% digitization of government services in 2024, and private-sector boards now benchmark against those standards, creating a halo effect for cloud HCM rollouts. The United Arab Emirates integrated its labor-market compliance APIs with private HCM suites, cutting audit cycles from quarterly to monthly and rewarding firms that maintain seamless cloud connectivity. Qatar's Civil Service and Government Development Bureau partnered with SAP SuccessFactors in 2025 for more than 85,000 workers, publishing configuration blueprints that private companies now reuse. Vendors that operate sovereign-cloud nodes inside Saudi Arabia and the United Arab Emirates have shortened sales cycles by reducing data-residency objections. As hyperscaler regions come online, hybrid security policies are easing concerns among banks and utilities, unlocking postponed migrations.

Regulatory Push for Wage Protection and Compliance Automation

Wage-protection frameworks have turned payroll into a mission-critical compliance process. The United Arab Emirates' Wage Protection System 2.0 obliges employers to transfer salaries within 10 working days through accredited institutions, with hefty fines and work-permit suspensions for repeat breaches. Saudi Arabia's Mudad platform cross-references payroll with social-insurance and immigration records, delivering 85-90% contract compliance in 2025 and forcing companies to replace siloed HR modules with integrated suites that automatically feed Qiwa. Kuwait now mandates biometric attendance capture, while Oman requires digital contract filings within 30 days of hire, further expanding the compliance footprint that HCM must cover.

Data Privacy and Residency Regulations Increasing Deployment Complexity

Sovereign data-protection acts oblige vendors to localize employee records, fragmenting what could be a single multi-tenant cloud into jurisdiction-specific instances. The United Arab Emirates maintains a whitelist of data-export mechanisms, extending procurement by up to 6 months as buyers await regulatory clearance. South Africa's Information Regulator has begun issuing enforcement notices, raising liability concerns that are stalling migrations among conservative banks. Nigeria now requires data-protection impact assessments for high-risk HR processing, a burden that small employers pass through to vendors by demanding turnkey compliance services. The resulting patchwork forces suppliers to maintain multiple infrastructure footprints, inflating the cost of goods sold and slowing roadmap delivery.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Workforce Analytics and AI-Powered Insights

- Rising Mobile and Remote Workforce Requiring Unified HCM Platforms

- Limited Cloud-Skilled Talent Pool in Several African Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are forecast to outpace software growth, expanding at an 11.24% CAGR through 2031. The Middle East and Africa HCM Software market is expanding, driven by implementation, integration, and managed services, as every Gulf country integrates payroll with unique pension rules, multi-lingual interfaces, and government gateway connections. Oracle's 2025 deal with e and embedded a three-year managed-services layer that covers compliance updates for 38 countries, illustrating how vendors lock in annuity streams once core modules go live. Start-ups such as Jisr secure recurring consulting fees by mapping Saudization thresholds into automated dashboards that executives can self-serve. As public-sector grants fund civil-service reforms in Ethiopia and Sierra Leone, local partners gain opportunities to deliver training and change-management work that global vendors do not staff locally.

Software still accounted for 73.48% of 2025 spending, as perpetual-license upgrades and SaaS subscriptions anchor every project. Nevertheless, price pressure intensifies as mid-market buyers weigh open API ecosystems against monolithic suites. Regional challengers bundle attendance scanners, insurance aggregation, and earned-wage access inside a single per-employee fee, prompting large platforms to unbundle specific micro-services to retain agility. Over the forecast window, the share of total services in the Middle East and Africa HCM Software market is expected to reach the low-30% range, confirming that productization alone cannot absorb the region's localization load.

Cloud solutions delivered 68.92% of the 2025 value and are set to grow at an 11.56% CAGR, yet legal and power-grid realities mean purely public architectures are uncommon beyond software-as-a-service talent modules. Buyers in banking and government increasingly opt for split-stack topologies that house payroll on sovereign nodes while pushing analytics to multiregion clouds. The Middle East and Africa HCM Software market share attributed to hybrid deployments will likely climb because Microsoft, Oracle, and SAP now offer region-specific instances that replicate sensitive tables to in-country storage.

On-premises footprints persist, particularly inside ministries that forbid external internet routes, but even these sites adopt containerized orchestration to gain patch automation. Kenya's suspended data-center project demonstrated that power scarcity can slow hyperscaler rollout, keeping standby diesel-based data rooms in play. Vendors that supply synchronization agents and zero-trust gateways capture wallet share because they let clients toggle between sovereign and public capacity without rewrites.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Core HR

- Talent Management

- Workforce Management

- Payroll Management

- Learning and Development

- By End-User Industry

- IT and Telecommunications

- BFSI

- Industrial Manufacturing

- Healthcare and Lifesciences

- Retail and E-commerce

- Government and Public Sector

- Other End-User Industries

- By Geography

- Middle East

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Oman

- Bahrain

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Kenya

- Rest of Africa

- Middle East

List of Companies Covered in this Report:

- Automatic Data Processing, Inc.

- BambooHR LLC

- Bayzat Technology LLC

- Dayforce, Inc.

- Cornerstone OnDemand, Inc.

- GulfHR FZ LLC

- HiBob Ltd.

- Infor, Inc.

- MenAITech for Information Technology

- Oracle Corporation

- Paycom Software, Inc.

- Paycor HCM, Inc.

- Paylocity Holding Corporation

- Ramco Systems Limited

- Rippling People Center Inc.

- Sage Group plc

- SeamlessHR Ltd.

- SAP SE

- UKG, Inc.

- Workday, Inc.

- ZenHR Solutions LLC

- Zoho Corporation Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Cloud Adoption Across GCC Enterprises

- 4.2.2 Regulatory Push for Wage Protection and Compliance Automation

- 4.2.3 Growing Demand for Workforce Analytics and AI-Powered Insights

- 4.2.4 Rising Mobile and Remote Workforce Requiring Unified HCM Platforms

- 4.2.5 Saudi NEOM Mega-Projects Driving Labor-Tracking Digitization Demand

- 4.2.6 Africa's Fintech-Led Payroll Infrastructure Leapfrogging Legacy HR Systems

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Residency Regulations Increasing Deployment Complexity

- 4.3.2 Limited Cloud-Skilled Talent Pool in Several African Markets

- 4.3.3 Fragmented Arabic Dialects Hindering NLP Adoption in HCM Software

- 4.3.4 High Cost of Regional Data Center Power Impacting SaaS Pricing

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 Middle East

- 5.6.1.1 Saudi Arabia

- 5.6.1.2 United Arab Emirates

- 5.6.1.3 Qatar

- 5.6.1.4 Kuwait

- 5.6.1.5 Oman

- 5.6.1.6 Bahrain

- 5.6.1.7 Rest of Middle East

- 5.6.2 Africa

- 5.6.2.1 South Africa

- 5.6.2.2 Nigeria

- 5.6.2.3 Egypt

- 5.6.2.4 Kenya

- 5.6.2.5 Rest of Africa

- 5.6.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 BambooHR LLC

- 6.4.3 Bayzat Technology LLC

- 6.4.4 Dayforce, Inc.

- 6.4.5 Cornerstone OnDemand, Inc.

- 6.4.6 GulfHR FZ LLC

- 6.4.7 HiBob Ltd.

- 6.4.8 Infor, Inc.

- 6.4.9 MenaITech for Information Technology

- 6.4.10 Oracle Corporation

- 6.4.11 Paycom Software, Inc.

- 6.4.12 Paycor HCM, Inc.

- 6.4.13 Paylocity Holding Corporation

- 6.4.14 Ramco Systems Limited

- 6.4.15 Rippling People Center Inc.

- 6.4.16 Sage Group plc

- 6.4.17 SeamlessHR Ltd.

- 6.4.18 SAP SE

- 6.4.19 UKG, Inc.

- 6.4.20 Workday, Inc.

- 6.4.21 ZenHR Solutions LLC

- 6.4.22 Zoho Corporation Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment