|

시장보고서

상품코드

2073278

중국의 HCM 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

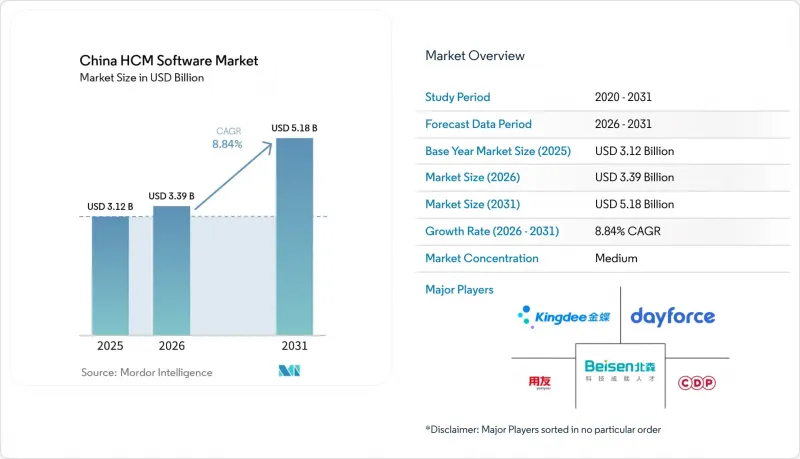

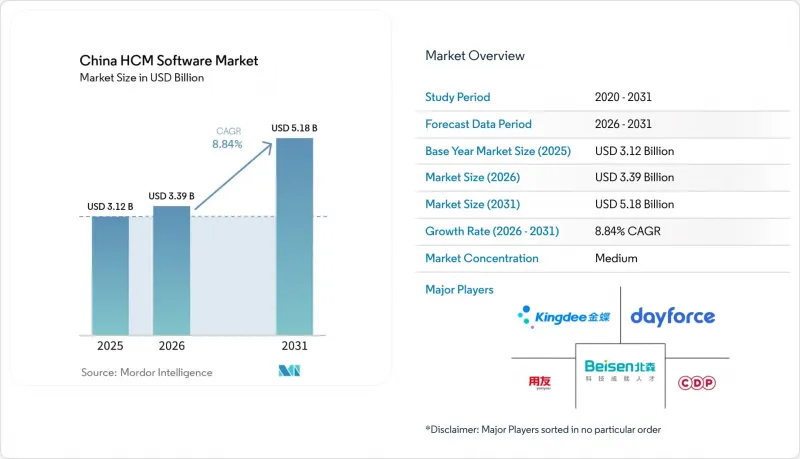

Mordor Intelligence에 의하면, 중국의 HCM 소프트웨어 시장 규모는 2025년에 31억 2,000만 달러로 평가되었습니다. 2026년에는 33억 9,000만 달러, 2031년까지 51억 8,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 8.84%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 조직 규모(대기업 및 중소기업), 용도(핵심 HR, 인재 관리, 인력 관리, 급여 관리 등), 최종 사용자 산업 분야(IT 및 통신, BFSI 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 HCM 소프트웨어 시장 동향 및 분석

기업 내 디지털 전환 추진

구식 On-Premise형 제품군으로는 실시간 분석을 제공할 수 없고, 급변하는 노동 법규를 준수하기 어렵기 때문에 기업들은 시스템 업데이트 주기를 앞당기고 있습니다. 닝보은행 등 조기에 시스템을 도입한 기업들은 채용, 성과 평가, 후계자 계획을 통합한 플랫폼을 도입한 결과, 신입 사원의 연수 기간을 30% 단축했습니다. 양저우 등 여러 도시에서 시행되고 있는 중소기업 지원 프로그램은 공공 자금을 통한 공동 출자가 예산상의 제약을 보완하고, 첫 도입을 촉진할 수 있음을 입증하고 있습니다. 소매업체들은 고령 근로자 보호를 위한 새로운 규정을 준수하기 위해 긱 워커를 지원하는 스케줄링 모듈을 도입하고 있으며, 제조업체들은 수주 변동에 대응하기 위해 HCM을 생산 실행 시스템에 통합하고 있습니다. 클라우드 솔루션은 민첩성과 설비 투자(CAPEX) 절감이라는 두 가지 측면에서 우위를 점하고 있으며, 공급업체 구성이 분산되는 추세가 이어지면서 중소기업 사용자 간의 가격 경쟁이 치열해지고 있습니다. 이러한 노력들이 어우러져 대상 고객층을 확대하고, 고객사 1곳당 평균 모듈 도입률을 높임으로써 중국의 HCM 소프트웨어 시장을 활성화하고 있습니다.

국내 소프트웨어에 대한 정부의 '클라우드 퍼스트' 정책

2026년 정부 활동 보고서에서는 공공 부문용 소프트웨어에 대한 '클라우드 퍼스트' 이러한 방침이 명문화됨에 따라, 사실상 국내 호스팅을 입증할 수 있는 업체로 수요가 유도되게 되었습니다. Beisen사와 Yonyou사는 이 지침을 바탕으로 여러 성급 계약을 수주했으며, 양사 모두 데이터 주권을 감독하는 당국의 우려를 불식시키기 위해 산업정보화부의 인증을 강조하고 있습니다. 여전히 구식 ERP 급여 시스템에 의존하고 있는 국영 기업에서는 하이브리드 방식의 도입이 일반적이지만, 그런 기업들조차 정책 목표를 달성하기 위해 신규 입사자를 대상으로 클라우드 기반 HCM의 시범 도입을 추진하고 있습니다. 정기적인 구독 모델은 공급업체의 가시성을 높이는 한편, 의무화된 데이터 현지화 조항은 전환 비용을 높여 시장의 정착도를 높이고 있습니다. 중국의 HCM 소프트웨어 시장에서 이러한 요인은 예측 기간 동안 클라우드 시장의 두 자릿수 성장을 확고히할 것입니다.

엄격한 “개인정보보호법”준수 비용

“개인정보보호법”따라서 명시적인 동의, 데이터 현지화 및 정기적인 개인정보 보호 감사가 의무화되었으며, 이로 인해 도입 기간이 최대 6개월 연장되었습니다. Workday와 같은 다국적 기업은 보안 심사를 통과하기 위해 현지 데이터센터를 운영하거나 국내 클라우드 사업자와 제휴해야 하므로, 프로젝트 비용 부담이 증가하고 있습니다. 소규모 현지 공급업체들은 규정 준수 담당자의 인건비나 기술적 업그레이드에 필요한 자금 조달에 어려움을 겪고 있어, 경쟁의 다양성이 제한되고 있습니다. 생체 인증을 활용한 근태 관리 기능의 경우, 동의를 확보하기 위해 재설계가 필요하여 새 버전의 출시가 지연되고 있습니다. 규정 준수와 관련된 간접 비용 증가는 중국의 HCM 소프트웨어 시장 전반에 걸쳐 공급업체와 구매자 양측의 이익률 확대를 억제하고 있습니다.

부문별 분석

소프트웨어 라이선스는 2025년 매출의 75.24%를 차지했으며, 이는 중국의 HCM 소프트웨어 시장에서 자본화된 핵심 제품군이 역사적으로 선호되어 왔음을 여실히 보여주고 있습니다. 그러나 기업들이 대화형 에이전트 훈련, ‘프라이버시 바이 디자인’에 기반한 코드 검토, 이중 급여 계산 엔진의 유지보수를 외주화함에 따라, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 9.62%를 기록하며 성장할 것으로 전망됩니다. 각 벤더사는 현재 31개 부처에 걸친 사회보험 규정 변경 사항을 모니터링하는 관리형 서비스를 패키지로 제공하고 있으며, 이를 통해 일회성 도입 프로젝트를 지속적인 수익원으로 전환하고 있습니다. Beisen사의 서비스 부서는 'AI Family 2.0' 이러한 추세를 배경으로, 2026년도 상반기에는 전년 동기 대비 12% 증가를 기록했습니다. 중소기업은 전담 IT 인력을 보유하고 있지 않아 공급업체가 운영하는 설정 워크숍에 의존하고 있는 반면, 국영 기업은 수십 년에 걸친 인사 데이터를 이전하기 위해 장기간에 걸친 변경 관리 지원이 필요합니다.

성과 기반 가격 책정으로의 전환이 두드러지고 있으며, 구매자들은 총 보상액을 채용 속도나 이직률 감소와 같은 정량화 가능한 KPI와 연계하고 있습니다. 앞으로 이 서비스는 중국 인사 관리(HCM) 소프트웨어 시장 규모에서 더 큰 점유율을 차지하게 될 것이며, 동시에 소프트웨어 수익은 정액제 클라우드 구독 모델로 전환될 것입니다. 단계적 도입을 의무화하는 PIPL 감사에 따라, 이 서비스의 전략적 중요성은 더욱 높아지고 있습니다. 사내에 법무 및 보안 부서를 보유한 공급업체는 높은 일당을 청구할 수 있지만, 소규모 경쟁사들은 대개 전문 컨설팅 회사와 제휴하기 때문에 이익률을 확보하기 어렵습니다. 그 결과, 서비스의 급증으로 인해 대규모 기존 기업과 틈새 시장의 신규 시장 진출기업 간의 실적 격차가 확대되고 있으며, 이러한 추세는 예측 기간 내내 지속될 것으로 보입니다.

2025년에는 클라우드가 지출의 62.82%를 차지하며 연평균 성장률(CAGR) 9.18%의 성장 궤도에 올라, 중국 인사 관리(HCM) 소프트웨어 시장에서 클라우드의 중심적 위상이 더욱 공고해졌습니다. 2026년 『정부 활동 보고서』에서 의무화된 '클라우드 퍼스트' 조달 방침에 따라, 정부 기관의 예산은 국내 호스팅 서비스를 제공하는 SaaS 공급업체로 배정되고 있습니다. 알리바바 클라우드와 화웨이 클라우드는 최고 수준의 보안 인증을 획득하여, 공공 부문에서의 도입 장벽이 완화되었습니다. 민간 기업도 이와 같은 혜택을 누리고 있습니다. 멀티테넌트 방식을 통한 업데이트로 인해 AI 기능 강화가 분기마다가 아닌 매월 제공되게 되어, 경쟁력이 한층 더 높아지고 있습니다. 하이브리드 환경은 On-Premise형 ERP에 얽매여 있는 기업들에게는 여전히 일시적인 과도기적 수단이지만, 듀얼 스택으로 인한 비용 증가가 완전한 전환을 위한 로드맵을 가속화하고 있습니다.

지방자치단체의 보조금 프로그램에서는 On-Premise 하드웨어가 아닌 구독 요금만 보조 대상에 포함되기 때문에 중소기업들은 설비 투자(CAPEX)를 최소화하기 위해 클라우드로 몰리고 있습니다. 그 결과, 사용자 수가 증가하고, 인사 AI 모델 학습에 활용되는 벤더의 데이터 레이크가 확충되며, 클라우드와 On-Premise형 솔루션 간의 차별화를 한층 더 강화하는 선순환이 형성되고 있습니다. 2031년까지 정책적 지원과 기능적 강화가 맞물리면서, 중국의 HCM 소프트웨어 시장 규모의 4분의 3 이상이 순수 클라우드 도입으로 집중될 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the china HCM software market size reached USD 3.12 billion in 2025 and is expected to reach USD 3.39 billion in 2026 and USD 5.18 billion by 2031, growing at a CAGR of 8.84% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and More), End-User Industry (IT and Telecommunications, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

China HCM Software Market Trends and Insights

Rising Enterprise Digital Transformation Mandates

Corporations are accelerating refresh cycles because legacy on-premises suites cannot provide real-time analytics or comply with fast-shifting labor laws. Early adopters such as Ningbo Bank cut onboarding time by 30% after deploying an integrated platform that unifies recruitment, performance, and succession planning. Subsidized SME programs in cities like Yangzhou prove that public co-funding can offset budget limitations and stimulate first-time adoption. Retailers are buying gig-friendly scheduling modules to conform with new over-age worker protections, and manufacturers are embedding HCM with execution systems to cope with order volatility. Cloud alternatives win on both agility and lower capex, fragmenting the vendor roster and heightening price competition among SME buyers. Collectively, these initiatives boost the China HCM software market by widening the eligible customer pool and lifting average module penetration per customer.

Government Cloud-First Policies for Domestic Software

The 2026 Government Work Report codified a cloud-first stance for public-sector software, effectively channeling demand to vendors that can prove domestic hosting. Beisen and Yonyou secured multiple provincial contracts on the back of this directive, each emphasizing Ministry of Industry and Information Technology certification to reassure data-sovereignty watchdogs. Hybrid rollouts remain common in SOEs that still rely on legacy ERP payroll, but even those entities now pilot cloud HCM for new hires to satisfy policy targets. Recurring subscription economics improve vendor visibility, while mandatory data-localization clauses raise switching costs, reinforcing market stickiness. For the China HCM software market, this driver cements double-digit cloud growth well into the forecast window.

Stringent Personal Information Protection Law Compliance Costs

The Personal Information Protection Law requires explicit consent, data-localization, and regular privacy audits, lengthening implementation timelines by up to six months. Multinationals such as Workday must run local data centers or partner with domestic clouds to pass security reviews, adding to project cost bases. Smaller local vendors struggle to fund compliance staff and technical upgrades, constraining competitive diversity. Biometric time-tracking features need redesign to secure consent, delaying new releases. Higher compliance overhead tempers margin expansion for both suppliers and buyers across the China HCM software market.

Other drivers and restraints analyzed in the detailed report include:

- AI-Native Intelligent Agent Adoption in HR Workflows

- Xinchuang Compliance Push

- Integration Complexity with Legacy ERP Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software licenses retained 75.24% of 2025 revenue, underscoring the historical preference for capitalized core suites within the China HCM software market share. Yet services are projected to grow at a 9.62% CAGR through 2031 as enterprises commission conversational-agent training, privacy-by-design code reviews, and dual payroll-engine maintenance. Vendors now bundle managed services that monitor social-insurance rule changes across 31 provinces, converting one-time implementations into annuity revenue. Beisen's services line rose 12% year-over-year during the first half of fiscal 2026 on the back of AI Family 2.0 rollouts. SMEs lean on vendor-run configuration workshops because they lack specialist IT staff, while SOEs require prolonged change-management support to migrate decades of personnel data.

The shift toward outcome-based pricing is visible as buyers tether fee pools to quantifiable KPIs such as onboarding speed or resignation-rate reduction. Over time, services will claim a larger slice of the China HCM software market size while software revenues migrate toward ratable cloud subscriptions. The strategic importance of services is further heightened by PIPL audits that compel phased deployments. Vendors that maintain in-house legal and security practices can charge premium day-rates, whereas smaller competitors often partner with boutique consultancies, reducing margin capture. Consequently, the services surge widens the performance gap between scaled incumbents and niche newcomers, a trend likely to persist throughout the forecast period.

Cloud captured 62.82% of spending in 2025 and is on track for a 9.18% CAGR, reinforcing its centrality to the China HCM software market. Mandatory cloud-first procurement in the 2026 Government Work Report redirects agency budgets to SaaS providers that provide domestic hosting. Alibaba Cloud and Huawei Cloud achieved top-tier security certification, easing public-sector onboarding hurdles. Private enterprises see parallel benefits: multi-tenant updates deliver AI enhancements monthly rather than quarterly, sharpening competitive edge. Hybrid remains a temporary bridge for firms saddled with on-premises ERP, but dual-stack costs are accelerating full migration roadmaps.

As municipal subsidy programs reimburse only subscription fees, not on-prem hardware, SMEs flock to the cloud to minimize capex. The resulting uptick in user seats improves vendor data lakes that train HR AI models, creating a feedback loop that further differentiates cloud from on-prem alternatives. By 2031, policy pull and feature push together are set to consolidate more than three-quarters of the China HCM software market size under pure-cloud deployments.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Core HR

- Talent Management

- Workforce Management

- Payroll Management

- Learning and Development

- By End-User Industry

- IT and Telecommunications

- BFSI

- Industrial Manufacturing

- Healthcare and Lifesciences

- Retail and E-commerce

- Government and Public Sector

- Other End-User Industries

List of Companies Covered in this Report:

- Beisen Cloud Computing Co., Ltd.

- Yonyou Network Technology Co., Ltd.

- Kingdee International Software Group Company Limited

- CDP Holdings Co., Ltd.

- Dayforce, Inc.

- Cornerstone OnDemand Inc.

- Ultimate Software Group Inc.

- PeopleStrong Technologies Pvt. Ltd.

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- Workday Inc.

- SAP SE

- Oracle Corporation

- Automatic Data Processing Inc.

- UKG Inc.

- Gaea Soft Group Co., Ltd.

- Xinren Xinshi Technology Co., Ltd.

- Ant Payslip Technology Co., Ltd.

- Honghai Cloud Computing Technology Co., Ltd.

- BenQ Guru Software Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Enterprise Digital Transformation Mandates

- 4.2.2 Government Cloud-First Policies for Domestic Software

- 4.2.3 AI-Native "Intelligent Agent" Adoption in HR Workflows

- 4.2.4 Xinchuang (Domestic IT Stack) Compliance Push

- 4.2.5 Cross-Border Expansion Demanding Global Payroll Compliance

- 4.2.6 Analytics-Driven Workforce Planning for Ageing Workforce

- 4.3 Market Restraints

- 4.3.1 Stringent Personal Information Protection Law Compliance Costs

- 4.3.2 Integration Complexity with Legacy ERP Systems

- 4.3.3 Vendor Churn Risk in Volatile SME Segment

- 4.3.4 Fragmented Provincial Social Insurance Rules

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Beisen Cloud Computing Co., Ltd.

- 6.4.2 Yonyou Network Technology Co., Ltd.

- 6.4.3 Kingdee International Software Group Company Limited

- 6.4.4 CDP Holdings Co., Ltd.

- 6.4.5 Dayforce, Inc.

- 6.4.6 Cornerstone OnDemand Inc.

- 6.4.7 Ultimate Software Group Inc.

- 6.4.8 PeopleStrong Technologies Pvt. Ltd.

- 6.4.9 Zoho Corporation Pvt. Ltd.

- 6.4.10 Ramco Systems Limited

- 6.4.11 Workday Inc.

- 6.4.12 SAP SE

- 6.4.13 Oracle Corporation

- 6.4.14 Automatic Data Processing Inc.

- 6.4.15 UKG Inc.

- 6.4.16 Gaea Soft Group Co., Ltd.

- 6.4.17 Xinren Xinshi Technology Co., Ltd.

- 6.4.18 Ant Payslip Technology Co., Ltd.

- 6.4.19 Honghai Cloud Computing Technology Co., Ltd.

- 6.4.20 BenQ Guru Software Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment