|

시장보고서

상품코드

2063972

유럽의 HCM 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

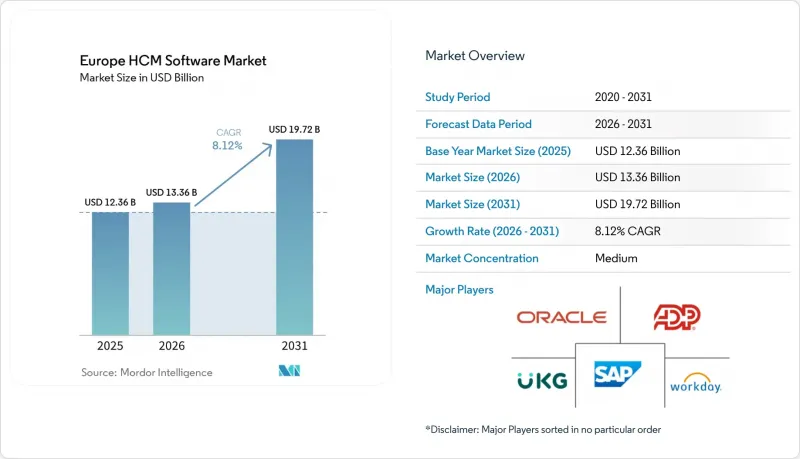

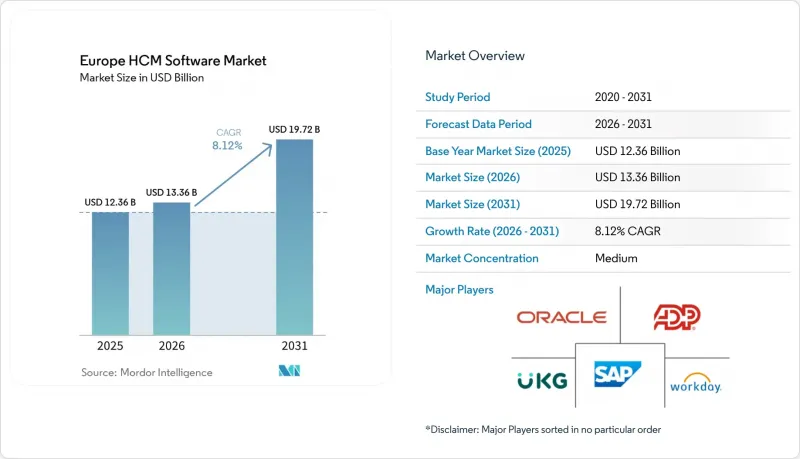

Mordor Intelligence에 의하면, 유럽 HCM 소프트웨어 시장 규모는 2025년에 123억 6,000만 달러에 이르고, 2026년에는 133억 6,000만 달러, 2031년까지 197억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 8.12%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 조직 규모(대기업 및 중소기업), 용도(핵심 HR, 인재 관리 등), 최종 사용자 산업 분야(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 제조업 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽 HCM 소프트웨어 시장 동향과 인사이트

클라우드 기반 HCM 플랫폼으로의 전환이 가속화되고 있습니다.

2025년, 클라우드는 유럽 HCM 소프트웨어 시장의 67.21% 점유율을 차지했는데, 이를 촉진한 요인은 비용 효율성에 그치지 않고, 일괄 처리 중심의 On-Premise 시스템으로는 실현할 수 없는 규제 대응의 민첩성까지 포함됩니다. 이에 반해 Workday는 2025년에 프랑크푸르트와 암스테르담에서 ‘EU 소버린 클라우드’를 출범시켰습니다. 이 클라우드는 유럽에 거주하는 관리자가 전담하여 운영하며, 고객은 머신러닝 모델을 활용하면서도 GDPR(EU 개인정보보호규정)의 데이터 거주 요건을 충족할 수 있습니다. SAP의 보고서에 따르면, 유럽 고객의 72%는 이미 하이브리드 방식을 도입하여 급여 계산은 ERP에서 계속 처리하는 한편, 인사 관리 모듈은 SuccessFactors에서 운영하고 있으며, 이는 점진적인 현대화의 방향을 보여주고 있습니다. 거의 실시간으로 정보를 공개하도록 의무화하는 지침이 늘어남에 따라, 클라우드의 보급은 더욱 가속화될 전망입니다.

인재 분석 및 AI 기반 인사이트에 대한 수요 증가

유로스타트의 2025년 조사에 따르면, EU 인구의 불과 56%만이 기본적인 디지털 역량을 갖추고 있는 것으로 나타났으며, 기업들은 사후 대응형 채용에서 예측적 인재 계획으로 전환할 수밖에 없는 상황에 놓여 있습니다. 더블린에 위치한 Workday의 AI 센터는 1만 개 고객사에서 수집한 익명화된 데이터를 활용하여, 90일 이내 이직 위험 예측에서 82%의 정확도를 달성했습니다. Oracle은 스킬 온톨로지 그래프를 도입하여, 댄스케 은행이 데이터 엔지니어링 직군 채용 기간을 40% 단축할 수 있도록 지원했습니다. 그러나 SD Worx의 조사에 따르면, 직원 수 250명 미만의 기업 중 예측 분석을 활용하고 있는 곳은 고작 22%에 불과한 것으로 나타나, 중소기업 대상 벤더들에게는 아직 개척되지 않은 시장이 존재함을 시사하고 있습니다. 각 벤더사는 인간의 감독과 관련된 EDPS 지침을 준수하기 위해 모델 신뢰도 점수를 추가하고 있습니다.

GDPR(EU 개인정보보호규정)에 따른 데이터 보안 및 개인정보 보호에 대한 우려

슈렘스 II 판결로 인해 대서양을 횡단하는 데이터 흐름은 여전히 복잡해지고 있으며, 공급업체들은 표준 계약 조항 외에도 암호화 및 가명화 도입을 피할 수 없게 되었습니다. 워크데이의 ‘EU 소버린 클라우드’는 처리를 EU 역내로 제한하고 있지만, 데이비슨 모리스는 2025년 보고서에서 영국 고용주의 58%가 이미 GDPR(EU 개인정보보호규정) 감사를 받았으며, 그중 12%는 부적절한 데이터 보관 관행으로 인해 공식 경고를 받았다고 보고했습니다. 차등 프라이버시나 연방 학습과 같은 프라이버시 보호형 분석 기술이 등장하고 있지만, 이러한 기술에는 많은 중견 시장 대상 통합 업체들이 갖추지 못한 전문적인 기술이 필요하며, 이에 따른 비용과 복잡성이 수반됩니다.

부문별 분석

2025년에는 소프트웨어가 유럽 HCM 소프트웨어 시장 점유율의 72.04%를 차지했으나, 서비스 매출은 2026년부터 2031년까지 연평균 성장률(CAGR) 9.21%로 확대될 것으로 전망됩니다. 도입 프로젝트는 데이터 이전, 변경 관리, ERP 통합을 포괄하는 경향이 강해지고 있으며, 기업들은 라이선스 비용에서 컨설팅 비용으로 예산을 전환하고 있습니다. 이러한 인력 부족을 배경으로 지역 전문가에 대한 수요가 증가함에 따라, 아웃소싱 업체가 일상적인 설정 관리를 담당하는 매니지드 서비스 계약이 널리 보급되고 있습니다.

소프트웨어 부문의 성장은 견조한 추세를 보이고 있지만, 구독 모델이 영구 라이선스 판매를 대체하고 있으며, 조합형 아키텍처로 인해 수요가 세분화되면서 이익률은 축소되고 있습니다. 로우코드 툴과 사전 훈련이 완료된 규정 준수 템플릿을 패키지로 제공하는 벤더들은 총 소유 비용을 절감하며 시장 점유율을 유지하고 있습니다. 유럽의 HCM 소프트웨어 시장에서는 소프트웨어와 자문 노하우를 결합한 업체들이 유리한 입지를 차지하고 있기 때문에 2031년까지 서비스 부문의 매출이 순수 라이선스 매출을 계속해서 상회할 것으로 예측됩니다.

하이브리드 배포는 조직이 GDPR(EU 개인정보보호규정)의 데이터 거주 요건과 퍼블릭 클라우드 분석의 확장성 및 혁신 속도 간의 균형을 맞추어감에 따라, 2026년부터 2031년까지 연평균 성장률(CAGR) 9.74%를 나타낼 것으로 예측되며, 이는 모든 배포 방식 중 가장 높은 성장률입니다. 2025년에는 SaaS 공급업체들이 지속적인 기능 업데이트와 기성 규정 준수 템플릿을 제공할 수 있게 된 것을 배경으로, 클라우드 시장 점유율이 67.21%를 차지했습니다. 그러나 SAP나 Oracle 등의 벤더들이 레거시 버전에 대한 지원을 단계적으로 중단함에 따라, 순수한 On-Premise 배포는 감소하는 추세에 있습니다. 규제 산업에서는 데이터 상주성이라는 이유로 급여 계산을 On-Premise 환경에서 유지하면서, 인재 관리, 학습, 분석은 SaaS로 전환하고 있습니다.

워크데이의 ‘EU Sovereign Cloud’와 SAP의 하이브리드형 SuccessFactors 도입 사례는 기업이 독자적인 급여 계산 로직을 유지하면서 유연한 분석 기능을 활용할 수 있는 중간적인 길을 제시하고 있습니다. 공공 기관에서는 여전히 설비 투자를 선호하는 경향이 있어 On-Premise 도입이 계속되고 있지만, 5년간의 총 소유 비용은 30%에서 50% 더 높습니다. 하이브리드화의 물결은 벤더 통합을 가속화할 것입니다. 왜냐하면 기존의 On-Premise 전문 벤더들은 플랫폼 전환에 필요한 자금이 부족하기 때문입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the europe hCM software market size reached USD 12.36 billion in 2025 and is expected to reach USD 13.36 billion in 2026 and USD 19.72 billion by 2031, growing at a CAGR of 8.12% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, and More), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe HCM Software Market Trends and Insights

Accelerated Migration to Cloud-Based HCM Platforms

Cloud held 67.21% share of the Europe HCM Software market in 2025, but the driver extends beyond cost efficiency to regulatory agility that batch-oriented on-premises systems cannot match. Workday responded by launching an EU Sovereign Cloud in Frankfurt and Amsterdam in 2025, staffed exclusively by European-resident administrators, letting customers leverage machine-learning models while satisfying GDPR data-residency rules. SAP reported that 72% of its European base is already on hybrid deployments in which payroll remains on ERP but talent modules run on SuccessFactors, demonstrating a phased modernization path. As more directives require near-real-time disclosures, cloud penetration is set to accelerate further.

Growing Need for Workforce Analytics and AI-Driven Insights

Eurostat showed in 2025 that only 56% of the EU population held basic digital skills, forcing companies to switch from reactive hiring to predictive workforce planning. Workday's AI Center in Dublin uses anonymized data from 10 000 customers to reach 82% accuracy in predicting 90-day attrition risk. Oracle embedded skills-ontology graphs that helped Danske Bank cut time-to-fill for data-engineering roles by 40%. Yet SD Worx found that only 22% of firms under 250 employees use predictive analytics, indicating white space for SME-focused vendors. Vendors are adding model-confidence scores to comply with EDPS guidance on human oversight.

Data Security and Privacy Concerns Under GDPR

The Schrems II ruling continues to complicate transatlantic data flows, forcing vendors to adopt standard contractual clauses plus encryption and pseudonymization. Workday's EU Sovereign Cloud keeps processing inside EU borders, but DavidsonMorris reported in 2025 that 58% of UK employers had already faced GDPR audits, with 12% receiving formal warnings for poor data-retention practices. Privacy-preserving analytics like differential privacy and federated learning are emerging, yet they require specialized skills that many mid-market integrators lack, introducing cost and complexity.

Other drivers and restraints analyzed in the detailed report include:

- Stringent and Evolving EU Labor Compliance Requirements

- Rise of Digital Employee Experience Platforms Integrating Well-Being and DEI Metrics

- Integration Complexity With Legacy ERP and Payroll Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is forecast to expand at a 9.21% CAGR between 2026 and 2031, even though software captured 72.04% of the Europe HCM Software market share in 2025. Implementation projects increasingly span data migration, change management, and ERP integration, so enterprises are shifting budget from licenses to consulting. This shortage is spawning regional specialists and managed-services arrangements in which outsourcers administer day-to-day configuration.

Software growth remains steady, but margins are tightening as subscription models replace perpetual sales and as composable architectures fragment demand. Vendors that package low-code tools and pretrained compliance templates lower the cost of ownership and protect share. The European HCM Software market rewards players that couple software with advisory know-how, so service lines are expected to keep outpacing pure license revenue through 2031.

Hybrid deployment is forecast to grow at 9.74% CAGR from 2026 to 2031, the fastest rate among deployment modes, as organizations balance GDPR data-residency mandates with the scalability and innovation velocity of public-cloud analytics. Cloud held 67.21% market share in 2025, driven by SaaS vendors' ability to deliver continuous feature updates and pre-built compliance templates, yet pure on-premises deployments are declining as vendors such as SAP and Oracle phase out support for legacy versions. Regulated industries keep payroll on-premises for data-residency reasons while moving talent, learning, and analytics to SaaS.

Workday's EU Sovereign Cloud and SAP's hybrid SuccessFactors deployments demonstrate a middle path that lets firms preserve custom payroll logic but tap elastic analytics. On-premises deployments persist in public agencies that still favor capital expenditure, although the total cost of ownership remains 30% to 50% higher over five years. The hybrid wave will accelerate vendor consolidation because legacy on-premises specialists lack the capital to re-platform.

List of Companies Covered in this Report:

- SAP SE

- Workday, Inc.

- Oracle Corporation

- Automatic Data Processing, Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- Cornerstone OnDemand, Inc.

- Sage Group plc

- Personio GmbH

- HiBob Inc.

- SD Worx NV

- Cegid Group SA

- Ramco Systems Limited

- Visma AS

- Paycor HCM, Inc.

- Paycom Software, Inc.

- Zoho Corporation Pvt. Ltd.

- Rippling People Center Inc.

- SD Worx People Solutions UK Limited

- Cornerstone OnDemand Limited (U.K.)

- Zucchetti S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Migration to Cloud-based HCM Platforms

- 4.2.2 Growing Need for Workforce Analytics and AI-driven Insights

- 4.2.3 Stringent and Evolving EU Labor Compliance Requirements

- 4.2.4 Rise of Digital Employee Experience Platforms Integrating Well-being and DEI Metrics

- 4.2.5 Expansion of ESG-linked Human Capital Reporting Mandates from European Investors

- 4.2.6 Adoption of Privacy-Preserving HR Tech to Navigate GDPR Constraints

- 4.3 Market Restraints

- 4.3.1 Data Security and Privacy Concerns under GDPR

- 4.3.2 Integration Complexity with Legacy ERP and Payroll Systems

- 4.3.3 Shortage of HR Tech Implementation Talent across Mid-Market System Integrators

- 4.3.4 Inflation-Driven IT Budget Compression in Public Sector Organizations

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Nordics

- 5.6.7 Russia

- 5.6.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Workday, Inc.

- 6.4.3 Oracle Corporation

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Ceridian HCM Holding Inc.

- 6.4.7 Cornerstone OnDemand, Inc.

- 6.4.8 Sage Group plc

- 6.4.9 Personio GmbH

- 6.4.10 HiBob Inc.

- 6.4.11 SD Worx NV

- 6.4.12 Cegid Group SA

- 6.4.13 Ramco Systems Limited

- 6.4.14 Visma AS

- 6.4.15 Paycor HCM, Inc.

- 6.4.16 Paycom Software, Inc.

- 6.4.17 Zoho Corporation Pvt. Ltd.

- 6.4.18 Rippling People Center Inc.

- 6.4.19 SD Worx People Solutions UK Limited

- 6.4.20 Cornerstone OnDemand Limited (U.K.)

- 6.4.21 Zucchetti S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment