|

시장보고서

상품코드

2064462

독일의 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Germany GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

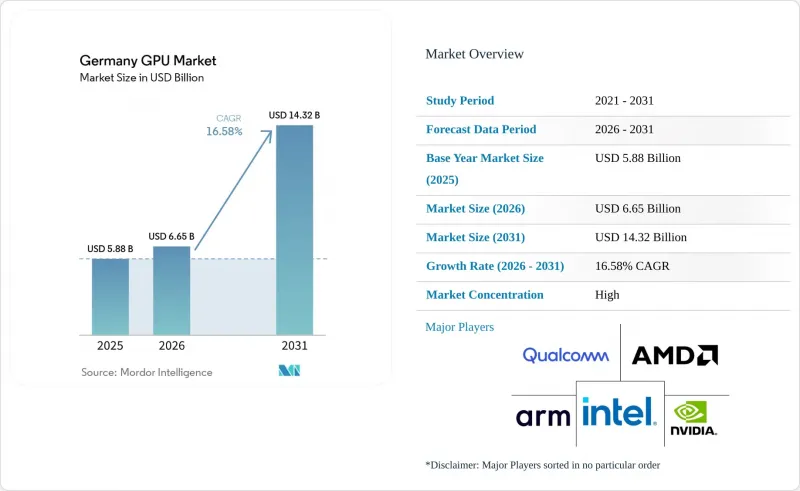

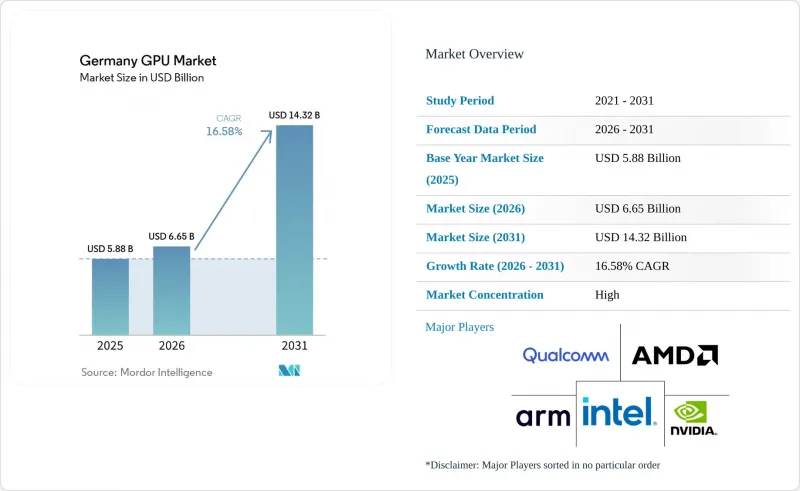

Mordor Intelligence에 의하면, 독일의 GPU 시장 규모는 2025년 58억 8,000만 달러로 평가되었고, 2026년에는 66억 5,000만 달러로 추정되고, 2031년까지 143억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 16.58%로 성장할 전망입니다.

본 보고서는 통합형별(통합형 GPU, 디스크리트 GPU)과 기기 용도별(모바일 기기 및 태블릿, PC 및 워크스테이션, 서버 및 데이터센터 가속기, 게임기 및 휴대용 게임기, 자동차/ADAS, 기타 임베디드 및 엣지 기기)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일의 GPU 시장 동향 및 인사이트

AI 및 HPC 워크로드의 급속한 성장

독일 기업들은 EU AI법에 부합하고 해외에서의 데이터 요구를 회피하기 위해 온프레미스형 GPU 클러스터를 우선적으로 도입하고 있습니다. 2026년 2월부터 가동을 시작해 1만 대의 NVIDIA Blackwell GPU를 구축한 뮌헨의 도이체 텔레콤 ‘Industrial AI Cloud’는 지멘스(Siemens)와 EY를 포함한 주요 고객사들에게 해당 용량의 3분의 1 이상을 이미 선판매했습니다. 슈바르츠 그룹은 국가 AI 인프라에 110억 유로(126억 5,000만 달러)를 배정했으며, IPCEI 마이크로전자공학 프로그램을 통한 국가 보조금 덕분에 자본 비용이 20-30% 절감되었습니다. 가우스 슈퍼컴퓨팅 센터 내 연구센터에서는 현재 최신 NVIDIA 및 AMD 가속기로의 업그레이드가 병행되어 진행되고 있으며, 이를 통해 기후 모델링, 신약 개발, 재료 과학 분야에서 고대역폭 메모리 설계가 얼마나 필수적인지가 부각되고 있습니다.

e스포츠의 성장이 하이엔드 게이밍 GPU 시장을 견인하고 있습니다.

독일이 e스포츠를 공식 스포츠로 인정함에 따라, 경기장과 훈련 시설에 대한 공공 자금이 확보되었고, GPU를 많이 사용하는 인프라가 제도화되었습니다. 4,500만 명 이상의 활성 게이머들이 240Hz 출력과 실시간 레이 트레이싱을 지원하는 독립형 그래픽 카드의 꾸준한 교체 주기를 이끌고 있습니다. 프로 e스포츠 팀인 G2 e스포츠, Berlin International Gaming, SK Gaming은 10밀리초 미만의 지연 시간을 구현하는 NVIDIA GeForce RTX 5080과 AMD Radeon RX 9070 XT를 탑재한 훈련 센터를 운영하고 있습니다. 스트리밍 크리에이터들은 초당 144프레임 이상의 프레임 속도를 유지하면서 4K60 인코딩을 수행하기 위해 듀얼 GPU 구성을 널리 활용하고 있으며, 이로 인해 하이엔드 추가 카드 시장이 더욱 활성화되고 있습니다.

반도체 공급망의 혼란

TSMC의 CoWoS 첨단 패키징 라인은 예약이 모두 마감되어 GPU의 리드타임이 12개월 이상으로 늘어났으며, 2026년 초로 예정되어 있던 독일 내 도입이 지연되고 있습니다. HBM3e 모듈공급 부족으로 인해 현물 가격이 상승하면서, 기업들은 하이퍼스케일러와의 계약, 자동차 프로젝트, 국가 AI 클러스터 사이에서 할당량을 조정할 수밖에 없는 상황에 처해 있습니다. EU 반도체법에서는 국내 반도체 제조 시설에 430억 유로를 투자하겠다고 약속하고 있지만, 신규 시설이 가동되는 것은 2027년 이후가 될 것이므로 당분간은 공급 부족 상황이 지속될 전망입니다.

부문별 분석

2025년, 독일 GPU 시장 점유율의 65.73%를 디스크리트 GPU가 차지했으며, 대규모 언어 모델(LLM) 훈련 클러스터의 주력 제품으로 자리매김하고 있습니다. 독일의 디스크리트 가속기 시장 규모는 EU의 데이터 주권 규정을 충족하도록 설계된 도이치 텔레콤의 뮌헨 내 1만 대 GPU 도입과 슈바르츠 그룹의 여러 거점에서의 확장에 힘입어 성장하고 있습니다. 한편, 통합형 GPU는 전력 제약이 엄격한 자동차 콕핏, 퀄컴(Qualcomm), AMD, 인텔(Intel)의 SoC가 다이 상에서 최대 80 TOPS를 처리하는 Copilot+ 탑재 노트북에서 꾸준히 시장 점유율을 확대되고 있습니다.

게이밍 및 컨텐츠 제작 작업 부하는 애호가들이 더 큰 프레임 버퍼와 인증된 드라이버를 우선시하기 때문에 전용 GPU에 대한 수요를 촉진하고 있습니다. 반면, 지속적인 부하가 가해지면 통합형 솔루션에서는 열 스로틀링이 발생하여 실제 사용 시 처리량이 저하됩니다. 에너지 예산이 제한적인 상황에서는 통합형 디바이스가 우수하지만, 수 시간에 달하는 레이트 레이싱 시퀀싱나 70억 개의 매개변수를 가진 모델을 활용한 AI 추론의 경우, 여전히 디스크리트 카드가 성능 면에서 우위를 점하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the germany gPU market size is expected to increase from USD 5.88 billion in 2025 to USD 6.65 billion in 2026 and reach USD 14.32 billion by 2031, growing at a CAGR of 16.58% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

Germany GPU Market Trends and Insights

Rapid Growth of AI and HPC Workloads

German enterprises are prioritizing on-premises GPU clusters to comply with the EU AI Act and avoid extraterritorial data requests. Deutsche Telekom's Industrial AI Cloud in Munich, operational since February 2026 with 10,000 NVIDIA Blackwell GPUs, has pre-sold more than one-third of its capacity to anchor tenants that include Siemens and EY. The Schwarz Group earmarked EUR 11 billion (USD 12.65 billion) for sovereign AI infrastructure, while national subsidies under the IPCEI Microelectronics program lower capital costs by 20-30%. Research centers inside the Gauss Center for Supercomputing are concurrently upgrading to the latest NVIDIA and AMD accelerators, underscoring how high-bandwidth-memory designs are now indispensable for climate modeling, drug discovery, and materials science.

Esports Expansion Driving High-End Gaming GPUs

Germany's recognition of esports as an official sport has unlocked public funding for arenas and training facilities, institutionalizing GPU-intensive infrastructure. More than 45 million active gamers drive steady refresh cycles for discrete graphics cards capable of 240 Hz output and real-time ray tracing. Professional teams, G2 Esports, Berlin International Gaming, and SK Gaming, run training centers equipped with NVIDIA GeForce RTX 5080 and AMD Radeon RX 9070 XT boards that deliver sub-10-millisecond latency. Streaming creators often use dual-GPU setups for 4K60 encoding while maintaining 144-plus frame rates, reinforcing the market for high-end add-in-boards.

Semiconductor Supply-Chain Disruptions

TSMC's fully booked CoWoS advanced-packaging lines extend GPU lead times beyond 12 months, delaying German deployments slated for early 2026. Shortfalls in HBM3e modules raise spot prices and compel enterprises to ration allocations among hyperscaler contracts, automotive projects, and sovereign AI clusters. Although the EU Chips Act commits EUR 43 billion to onshore fabs, new facilities will not come online before 2027, leaving near-term supply tight.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Adoption for ADAS Visualization

- Aerospace and Defence Simulation Workloads

- Escalating Average Selling Prices of dGPUs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs held 65.73% of the Germany GPU market share in 2025 and remain the workhorse for large-language-model training clusters. The Germany GPU market size for discrete accelerators benefits from Deutsche Telekom's 10,000-GPU Munich installation and the Schwarz Group's multi-site build-out, each designed to meet EU data-sovereignty rules. Integrated GPUs are nonetheless gaining ground in power-constrained automotive cockpits and Copilot+ laptops that rely on Qualcomm, AMD, and Intel SoCs delivering up to 80 TOPS on die.

Gaming and content-creation workloads reinforce discrete demand, as enthusiasts prioritize larger frame buffers and certified drivers. Conversely, sustained loads expose thermal throttling in integrated solutions, trimming real-world throughput. Integrated devices shine where energy budgets are fixed, yet for multi-hour ray-traced sequences or AI inference on 7-billion-parameter models, discrete cards still carry the performance edge.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Arm Ltd.

- Imagination Technologies Ltd.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- ASUSTeK Computer Inc.

- Giga-Byte Technology Co., Ltd.

- Micro-Star International Co., Ltd. (MSI)

- Zotac Technology Limited

- Sapphire Technology Limited

- Tenstorrent, Inc.

- PowerColor (TUL Corporation)

- ASRock Inc.

- InnoVision Multimedia Ltd. (Inno3D)

- Matrox Electronic Systems Ltd.

- Huawei Technologies Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth of AI and HPC Workloads

- 4.2.2 Esports Expansion Driving High-End Gaming GPUs

- 4.2.3 Automotive OEM Adoption for ADAS Visualization

- 4.2.4 Aerospace and Defence Simulation Workloads

- 4.2.5 Renewable-Energy Digital-Twin Simulations

- 4.2.6 German R&D Tax Incentives for Semiconductor IP

- 4.3 Market Restraints

- 4.3.1 Semiconductor Supply-Chain Disruptions

- 4.3.2 Escalating Average Selling Prices of dGPUs

- 4.3.3 Energy-Efficiency Caps on Datacentre Hardware

- 4.3.4 Talent Shortage in GPU Software Optimisation

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacentre Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Arm Ltd.

- 6.4.6 Imagination Technologies Ltd.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 Apple Inc.

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Giga-Byte Technology Co., Ltd.

- 6.4.11 Micro-Star International Co., Ltd. (MSI)

- 6.4.12 Zotac Technology Limited

- 6.4.13 Sapphire Technology Limited

- 6.4.14 Tenstorrent, Inc.

- 6.4.15 PowerColor (TUL Corporation)

- 6.4.16 ASRock Inc.

- 6.4.17 InnoVision Multimedia Ltd. (Inno3D)

- 6.4.18 Matrox Electronic Systems Ltd.

- 6.4.19 Huawei Technologies Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment