|

시장보고서

상품코드

2065611

유럽의 통합 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Integrated GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

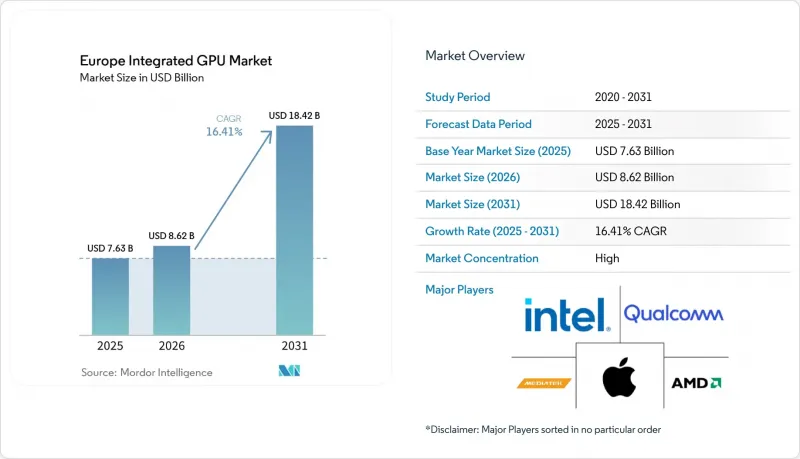

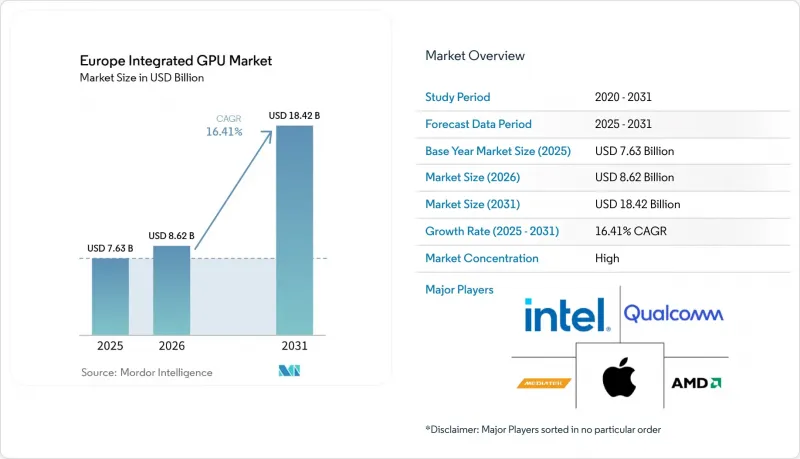

Mordor Intelligence에 의하면, 유럽의 통합 GPU 시장 규모는 2025년에 76억 3,000만 달러로 평가되었고, 2026년에 86억 2,000만 달러로 추정되고, 2031년까지 184억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 16.41%로 성장할 전망입니다.

본 보고서는 디바이스 카테고리별(데스크톱 및 노트북용 프로세서, 모바일 SoC(스마트폰 및 태블릿), 임베디드 및 산업용 SoC, 통합 그래픽이 탑재된 서버 및 데이터센터용 프로세서), 성능 수준별(엔트리 레벨(50달러 미만), 메인스트림(50-150달러), 퍼포먼스(150-300달러), 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 통합 GPU 시장 동향 및 인사이트

AI 지원 노트북의 보급률 상승이 통합 GPU 수요 구성을 재편하고 있습니다.

기업들이 전체 교체 주기를 통해 로컬 AI 기능을 지원할 수 있는 시스템을 요구하는 가운데, AI 지원 노트북은 유럽의 통합 GPU 시장에서 뚜렷한 구매 카테고리로 자리 잡고 있습니다. 인텔은 CES 2026에서 최대 12개의 Xe3 GPU 코어와 50 TOPS의 NPU를 탑재한 ‘Panther Lake Core Ultra Series 3’를 발표했습니다. 이 플랫폼은 그래픽스와 AI가 이제 클라이언트 컴퓨팅 논의에서 동등한 위치로 다뤄지게 되었음을 분명히 보여주고 있습니다. 실용적인 측면에서 볼 때, NPU와 iGPU는 일상적인 업무 환경에서 동영상 화질 향상, 배경 분할, 문서 처리와 같은 복합 워크로드를 분담하게 되었습니다. 이로 인해, 과거에는 표준적인 사무용 기기로 여겨지던 노트북에서도 그래픽 사양의 최저 기준이 높아졌습니다. 따라서 유럽의 통합 GPU 시장은 판매 대수 증가뿐만 아니라, AI 지원 노트북이 틈새 시장 범주에서 기업의 주류 수요로 전환됨에 따라 수요 구성의 강화라는 이점도 누리고 있습니다.

Windows 11 Refresh와 Windows 10 지원 종료가 PC 하드웨어의 구조적 업데이트를 촉진

Windows 10은 2025년 10월 14일에 공식 지원이 종료됨에 따라, TPM 2.0이나 시큐어 부트와 같은 Windows 11의 최소 보안 요건을 충족하지 못하는 유럽 내 모든 기기에 대해 하드웨어 교체를 촉구하는 압력이 가해졌습니다. 이는 유럽의 통합 GPU 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 이번 업데이트는 소프트웨어 주도가 아닌 하드웨어 주도이기 때문에 일반적인 OS 전환보다 프로세서 출하량을 대폭 끌어올릴 것이기 때문입니다. 많은 중소기업들이 2024년 내내 업그레이드를 미루어 왔기 때문에 이미 도입된 기기의 상당 부분은 완전히 교체하지 않고서는 전환할 수 없었습니다. 또한 구매자들은 최소 사양을 충족하는 시스템보다는 AI 지원 플랫폼을 선택하는 경향이 있으며, 이는 메인스트림 및 고성능 부문에서 가치를 한층 더 높이는 데 기여하고 있습니다. 그 결과, 유럽의 통합 GPU 시장은 과거 Windows 지원 종료 시점이 시사했던 것보다 더 큰 수요 증가세를 보이고 있습니다.

AI 가속기 및 프리미엄 모바일 SoC를 둘러싼 첨단 노드 경쟁이 공급을 제약하고 있습니다.

유럽의 통합 GPU 시장은 선진 파운드리 업체들의 생산 능력에 의존하고 있습니다. 이는 프리미엄 노트북이나 스마트폰이 더 낮은 전력 소비 제한 내에서 높은 그래픽 성능을 구현하기 위해 최첨단 노드가 필요하기 때문입니다. AI 가속기와 프리미엄 모바일 프로세서가 모두 3nm-4nm급 생산 능력을 놓고 경쟁하고 있어, 이로 인해 구조적인 공급 문제가 발생하고 있습니다. 이 문제는 AMD, MediaTek, Qualcomm과 같은 벤더들에게 중요합니다. 왜냐하면, 이 기업들은 웨이퍼 투입량 측면에서 사실상 자사의 고수익 제품 라인과 경쟁하고 있기 때문입니다. 그 결과, 차세대 제품의 출시가 지연되거나 가격이 급등하거나, 유럽 OEM 고객을 대상으로 한 양산 수준 공급이 제한될 가능성이 있습니다. 따라서 최종 사용자 수요가 견조함에도 불구하고, 유럽의 통합 GPU 시장은 단기적으로 실질적인 제약을 겪고 있습니다.

부문별 분석

2025년, 모바일 SoC는 유럽 통합 GPU 시장 점유율의 49.45%를 차지했으며, 해당 지역의 매출 구성에서 가장 큰 비중을 차지하는 기기 카테고리가 되었습니다. 이러한 우위는 유럽 내 프리미엄 스마트폰의 높은 보급률과, 중상급 및 플래그십급 안드로이드 단말기가 하드웨어 레이 트레이싱, 고속 미디어 엔진, 강력한 온디바이스 AI 지원을 갖춘 고성능 통합 그래픽스 블록으로 지속적으로 전환되고 있음을 반영합니다. 삼성의 ‘Exynos 1680’과 미디어텍의 ‘Dimensity 9500’ 제품군은 유럽 통합 GPU 업계의 모바일 분야가 단순히 판매량 증가에만 의존하는 것이 아니라, 첨단 공정에서 그래픽 성능 향상을 추구하는 방향으로 전환되고 있음을 보여줍니다. 데스크톱 및 노트북용 프로세서는 2025년부터 2026년에 걸쳐 Windows 11의 업데이트 주기에 따라 기업용 노트북 및 데스크톱 PC 전반에 걸쳐 교체 수요가 지속됨에 따라, 계속해서 2위 카테고리를 차지했습니다.

통합 그래픽을 탑재한 서버 및 데이터센터용 프로세서는 2031년까지 연평균 성장률(CAGR) 16.97%를 나타낼 것으로 예측되며, 유럽 통합 GPU 시장 규모 전망에서 가장 빠르게 성장하는 디바이스 카테고리가 될 것으로 보입니다. 유럽의 클라우드 서비스 제공업체와 기업 데이터센터에서는 모든 이용 사례에서 전용 애드인 가속기가 필요 없이 연산, 비디오 트랜스코딩, 경량 추론, 시각화를 처리할 수 있는 통합형 프로세서에 대한 관심이 높아지고 있습니다. 2026년 상반기에 출시될 예정인 인텔의 ‘Xeon 6+Clearwater Forest’에 대한 미리 보기는 이러한 변화를 뒷받침하는 속도로 첨단 노드의 통합 그래픽 기능이 서버급 플랫폼에 도입되고 있음을 보여줍니다. 임베디드 및 산업용 SoC는 절대적인 규모로는 작지만, 독일, 프랑스, 이탈리아의 공장 및 산업 장비에서 엣지 AI가 확대됨에 따라 전략적 중요성이 커지고 있습니다. NXP의 i.MX 93W와 르네사스의 Irida Labs 인수는 유럽의 통합 GPU 업계도 임베디드 플랫폼으로 전환되고 있으며, 고객의 의사결정 과정에서 그래픽, AI, 연결성, 그리고 소프트웨어를 통한 차별화가 종합적으로 중요시되고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSHAccording to Mordor Intelligence, the europe integrated GPU market size is projected to be USD 7.63 billion in 2025, USD 8.62 billion in 2026, and reach USD 18.42 billion by 2031, growing at a CAGR of 16.41% from 2026 to 2031.

This report is Segmented by Device Category (Desktop and Laptop Processors, Mobile SoCs (Smartphones and Tablets), Embedded and Industrial SoCs, and Server and Data Center Processors With Integrated Graphics), Performance Tier (Entry-Level (Less Than USD 50), Mainstream (USD 50-USD 150), Performance (USD 150-USD 300), and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Integrated GPU Market Trends and Insights

Rising AI-Capable Notebook Penetration Reshapes Integrated GPU Demand Mix

AI-capable notebooks have become a defined buying category across the Europe integrated GPU market as enterprises look for systems that can support local AI features over a full replacement cycle. Intel launched Panther Lake Core Ultra Series 3 at CES 2026 with up to 12 Xe3 GPU cores and a 50 TOPS NPU, making the platform a clear signal that graphics and AI now sit together in the same client computing conversation. The practical change is that the NPU and iGPU now share mixed workloads such as video enhancement, background segmentation, and document processing in everyday business use. That raises the graphics specification floor even in notebooks that were once treated as standard office machines. The Europe integrated GPU market is therefore benefiting not only from more units, but also from a stronger mix as AI-ready notebooks move from a niche class into mainstream enterprise demand.

Windows 11 Refresh and Windows 10 Retirement Drive Structural PC Hardware Replacement

Windows 10 reached its official end of support on October 14, 2025, and that created direct hardware replacement pressure across European device fleets that did not meet Windows 11 security minimums such as TPM 2.0 and Secure Boot. This matters for the Europe integrated GPU market because the refresh is hardware-led rather than software-led, which lifts processor shipments more strongly than a normal operating system transition. Many small and medium enterprises delayed upgrades through 2024, so a meaningful share of installed devices could not move forward without full replacement. Buyers are also tending to choose AI-capable platforms instead of minimum-spec compliant systems, and that supports stronger value across the Mainstream and Performance tiers. The Europe integrated GPU market is therefore seeing a larger uplift than earlier Windows sunsets would have suggested.

Advanced-Node Supply Competition From AI Accelerators and Premium Mobile SoCs Constrains Supply

The Europe integrated GPU market depends on advanced foundry capacity because premium notebooks and smartphones now need leading-edge nodes to deliver higher graphics capability within lower power limits. This creates a structural supply problem because AI accelerators and premium mobile processors are chasing the same 3nm-4nm class capacity. The issue is important for vendors such as AMD, MediaTek, and Qualcomm because they are effectively competing against their own higher-margin product lines for wafer starts. That can delay next-generation launches, raise pricing, or limit supply at the volume tier for European OEM customers. The Europe integrated GPU market therefore faces a real near-term brake even when end-user demand remains healthy.

Other drivers and restraints analyzed in the detailed report include:

- Premium Smartphone SoC Migration to Richer Graphics and Advanced Nodes Expands Mobile iGPU Value

- Demand for Power-Efficient Graphics in Thin-and-Light Devices Elevates Advanced-Node iGPU Design Spend

- High-End Creator and Gaming Workloads Sustain Discrete GPU Demand at the Top End

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile SoCs held 49.45% of the Europe integrated GPU market share in 2025, making them the largest device category across the region's revenue mix. Their lead reflects Europe's dense premium smartphone base and the ongoing move of upper-mid and flagship Android devices toward richer integrated graphics blocks with hardware ray tracing, faster media engines, and stronger on-device AI support. Samsung's Exynos 1680 and MediaTek's Dimensity 9500 family show how the mobile layer of the Europe integrated GPU industry is moving toward higher graphics value at advanced nodes rather than relying only on unit growth. Desktop and Laptop Processors remained the second-largest category because the Windows 11 refresh cycle sustained replacement demand across enterprise notebooks and desktops in 2025 and into 2026.

Server and Data Center Processors with Integrated Graphics are projected to expand at a CAGR of 16.97% through 2031, which makes them the fastest-growing device category in the Europe integrated GPU market size outlook. European cloud operators and enterprise data centers are increasingly looking at unified processors that can handle compute, video transcoding, lightweight inference, and visualization without a dedicated add-in accelerator in every use case. Intel's preview of Xeon 6+ Clearwater Forest, expected in the first half of 2026, illustrates how advanced-node integrated graphics capability is moving into server-grade platforms at a speed that supports this shift. Embedded and Industrial SoCs are smaller in absolute value, but they are gaining strategic importance as edge AI expands in factories and industrial equipment across Germany, France, and Italy. NXP's i.MX 93W and Renesas' acquisition of Irida Labs show that the Europe integrated GPU industry is also shifting toward embedded platforms where graphics, AI, connectivity, and software differentiation now matter together in customer decisions.

List of Companies Covered in this Report:

- Intel Corporation

- Advanced Micro Devices, Inc.

- QUALCOMM Incorporated

- Apple Inc.

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- Arm Limited

- Imagination Technologies Limited

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- NVIDIA Corporation

- Broadcom Inc.

- UNISOC (Shanghai) Technologies Co., Ltd.

- Rockchip Electronics Co., Ltd.

- Amlogic Co., Ltd.

- Allwinner Technology Co., Ltd.

- Google LLC

- Socionext Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Windows 11 Refresh and Windows 10 Retirement

- 4.2.2 Rising AI-Capable Notebook Penetration

- 4.2.3 Demand for Power-Efficient Graphics in Thin-and-Light Devices

- 4.2.4 Premium Smartphone SoC Migration to Richer Graphics and Advanced Nodes

- 4.2.5 EU Ecodesign and Energy Labeling Pressure Favoring Lower-Power Designs

- 4.2.6 Industrial Edge AI Rollouts Expanding Embedded SoC Demand

- 4.3 Market Restraints

- 4.3.1 Advanced-Node Supply Competition From AI Accelerators and Premium Mobile SoCs

- 4.3.2 Memory and Storage Cost Inflation Limiting Replacement Budgets

- 4.3.3 Cyber Resilience Act Compliance Burden for Connected Embedded Platforms

- 4.3.4 High-End Creator and Gaming Workloads Still Pulling Demand Toward Discrete GPUs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Category

- 5.1.1 Desktop and Laptop Processors

- 5.1.2 Mobile SoCs (Smartphones and Tablets)

- 5.1.3 Embedded and Industrial SoCs

- 5.1.4 Server and Data Center Processors with Integrated Graphics

- 5.2 By Performance Tier

- 5.2.1 Entry-Level (Less than USD 50)

- 5.2.2 Mainstream (USD 50 - USD 150)

- 5.2.3 Performance (USD 150 - USD 300)

- 5.2.4 High-Performance (Greater than USD 300)

- 5.3 By Country

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 QUALCOMM Incorporated

- 6.4.4 Apple Inc.

- 6.4.5 MediaTek Inc.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Arm Limited

- 6.4.8 Imagination Technologies Limited

- 6.4.9 NXP Semiconductors N.V.

- 6.4.10 STMicroelectronics N.V.

- 6.4.11 Texas Instruments Incorporated

- 6.4.12 Renesas Electronics Corporation

- 6.4.13 NVIDIA Corporation

- 6.4.14 Broadcom Inc.

- 6.4.15 UNISOC (Shanghai) Technologies Co., Ltd.

- 6.4.16 Rockchip Electronics Co., Ltd.

- 6.4.17 Amlogic Co., Ltd.

- 6.4.18 Allwinner Technology Co., Ltd.

- 6.4.19 Google LLC

- 6.4.20 Socionext Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment